Welcome back to earnings season! Over the next several weeks, I will be sending 40 detailed reviews on popular, high-quality companies. The Netflix article will be published later tonight, with ServiceNow, Tesla, Robinhood, Meta, SoFi, AMD, Palantir and so many others coming thereafter.

If you'd like access to all of those reports, consistently thorough weekly news, my real-time performance/portfolio updates and access to a large Discord channel of seasoned investors, lock in your annual deal below.

This is where investors (including Fortune 500 executives) come for signal over noise and to invest with good reason.

Other recent content includes:

a. Taiwan Semi 101

Taiwan Semi manufactures chipsets for designers like Nvidia, Amazon, AMD, Broadcom and Qualcomm. It does so in its highly expensive and complex chip fabrication plants. These are called “fabs” for short.

Needed Definitions:

- Fab means a factory.

- Nanometer (NM) describes the chip manufacturing technology. Smaller NM is more advanced, as it uses smaller transistors. This means TSM can pack more transistors into a single chip, making those chips more energy efficient and cost-effective.

- “Advanced Technology” revenue is revenue from 3-nanometer (N3), N5 & N7 technology. Anything under N7 is “advanced.”

- These labels describe the actual manufacturing technology process.

- Wafer refers to the raw materials (usually silicon) that are used to manufacture chips. Wafers are the “substrate” that integrated circuits (ICs) are built on top of. The transistors within these ICs guide and facilitate functions. Nvidia’s Blackwell chips are considered ICs.

- Lithography is the process of using photomasks (chip blueprints) and light to print chip patterns onto wafers. A light-sensitive material is added to wafers, with light pushed through the masks to guide the chip's design. This closely guides how light and chemicals generate desired patterns and create specific use cases. Lithography is paramount to TSM’s production."

- While traditional foundry services entail the actual testing and creation of a chip on a silicon wafer, packaging involves storing, integrating and prepping chip components with thermal protection, connectivity equipment and encapsulation (physical damage protection).

- These categories (packaging, testing and mask-making) are part of TSM’s “Foundry 2.0” – or the firm’s updated overall foundry total addressable market (TAM).

- Chip-on-wafer-on-substrate (CoWoS) is a packaging process that combines chips into a single unit. It allows things like GPUs, high-bandwidth memory (HBM) and custom chips to be vertically stacked and connected on a single substrate. This improves the compute speed and performance generated from these chips. TSM is a key partner for all HBM manufacturers. It doesn't actually build the memory layer of these memory chips, but does provide the infrastructure to layer on and package other needed components.

- Substrates also help protect chip components and manage heat.

- Vast processing needs from GenAI and Agentic AI require the vertical stacking CoWoS facilitates to ensure needed access to scalable data.

- AI Accelerators, as the name indicates, accelerate high-performance compute (HPC) workloads in the realm of AI. GPUs are a type of AI accelerator, along with Application Specific Integrated Circuits (ASICs) (custom chips) and Google’s Tensor Processing Units (TPUs; for machine learning). TSM also includes high-bandwidth memory in this category. HBM facilitates ultra-low latency, high-bandwidth support for querying and data processing tasks as a wonderful complement to GPUs, for example.

b. Key Points

- N2 is scaling on schedule.

- TSM needs more N3 capacity to meet demand.

- Supply conditions remain tight.

- Modestly raised CapEx guidance.

c. Demand

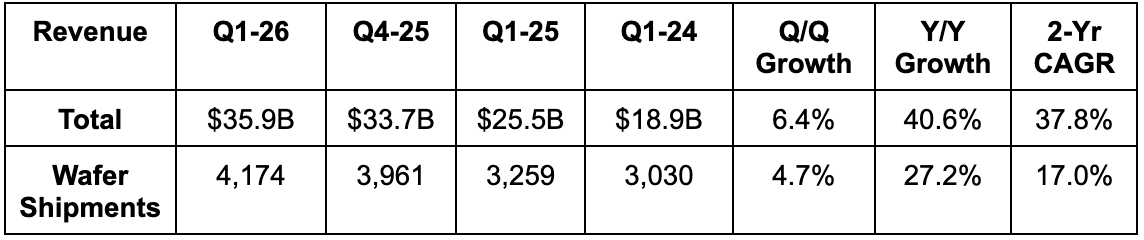

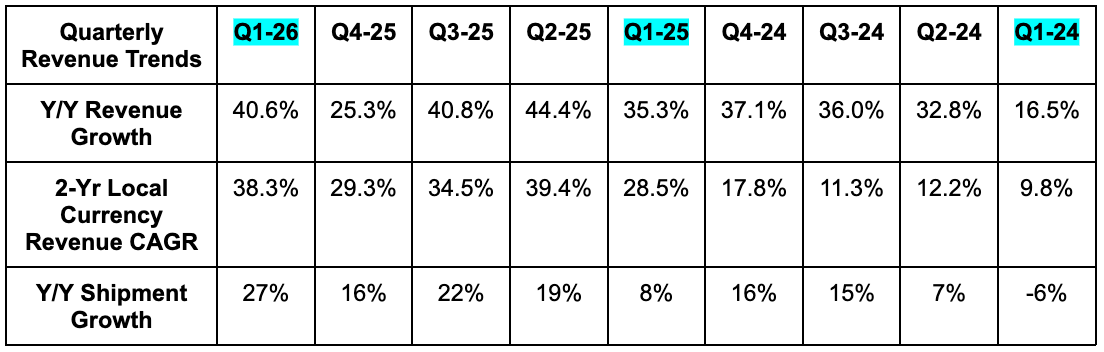

Taiwan Semi beat revenue estimates by 1.4% & beat guidance by 2%. Its 37.8% 2-year compounded annual growth rate (CAGR) (in U.S. dollars) compares to 21.1% last quarter and 38.4% two quarters ago. Advanced technology demand stemming from the explosion in AI agents again drove the strong growth this quarter.

Splits by Technology:

- N7 was 13% of revenue vs. 14% last quarter and 15% Y/Y.

- N5 was 36% of revenue vs. 35% last quarter and 36% Y/Y.

- N3 was 25% of revenue vs. 28% last quarter and 22% Y/Y.

- Advanced Tech was 74% of revenue vs. 77% last quarter and 73% Y/Y.

Splits by End Market:

- High-Performance Compute (HPC) revenue was 61% of total vs. 55% Q/Q & 59% Y/Y.

- HPC revenue rose by 20% Q/Q vs. 4% growth last quarter.

- Smartphone revenue was 26% of total vs. 32% Q/Q and 28% Y/Y.

- Smartphone revenue rose by -11% Q/Q vs. 11% growth last quarter.

- Internet of Things (IoT) revenue was 6% of total vs. 5% Q/Q & 5% Y/Y.

- Auto revenue was 4% of total vs. 5% Q/Q & 5% Y/Y.

d. Profitability & Margins

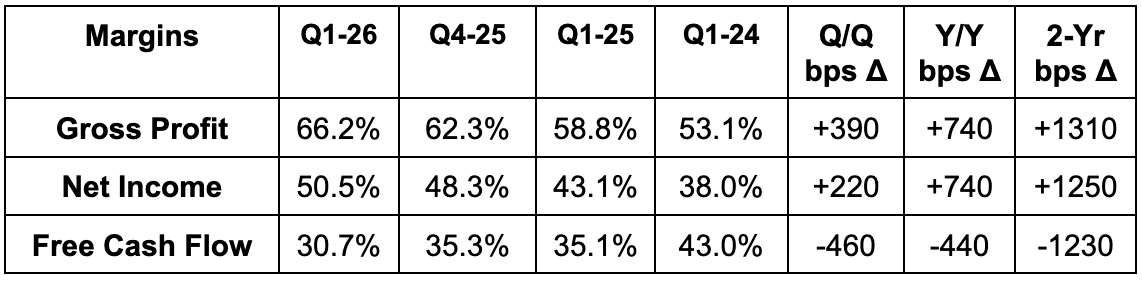

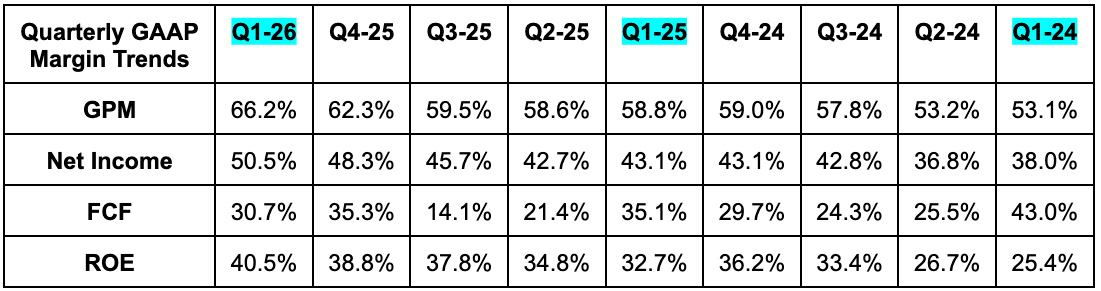

- Beat 64.3% gross profit margin (GPM) estimates by 190 bps & beat guidance by 220 basis points (bps; 1 basis point = 0.01%).

- Beat EBIT estimates by 5.9% & beat guidance by 7.5%. Its 58.1% EBIT margin beat 57% margin guidance.

- Beat $0.66 EPS estimates by $0.04.

- EPS rose 58% Y/Y in local currency.

- Beat 38% return on equity (ROE) estimates.

Better capacity utilization, ongoing cost discipline and some non-structural foreign exchange help all boosted profitability. These tailwinds are far stronger than any headwinds impacting the company at the moment, and are powered by exceedingly strong AI-based demand as well as ongoing supply tightness. For context, their long-term GPM target is 56%, which they were more than 10 points ahead of during the quarter. The margin won't remain this strong forever, as a supply-demand equilibrium will be found at some point. But? As of right now, that balance is nowhere in sight. And fantastic pricing power, paired with consistently disciplined cost management, paved the way for this impressive result.

There are some smaller headwinds preventing GPM from being even higher than it already is. Intentional manufacturing footprint diversification to the United States and other parts of the world will remain a 2-3% margin headwind for the next few years. As most of their capacity is in Taiwan, and considering heightened geopolitical tensions there, this makes sense. They are a fiercely trusted and relied upon vendor for all of their customers. They need to ensure that these customers can get the highly valuable hardware they need, even if tensions in Taiwan escalate. This is an easy margin headwind to accept, considering how powerful the offsets currently are. And as an added bonus, as they've talked about in the past, the “made in the USA" label does fetch premium pricing, and could help ease the margin headwind down the road.

The ramp of their N2 technology will also lower GPM by another 2% to 3% during 2026. The company always deals with this headwind when a manufacturing node initially ramps. It generally takes them 3-4 years for the new products' GPM to reach and surpass the blended GPM of the overall company. That's what is expected to happen for N3 (N2's predecessor) later this year in that product line's 4th year of existence. This margin headwind is always prevalent for TSM because they are always ramping up a new manufacturing process for customers. It's simply part of the business.

e. Balance Sheet

- $105B cash & equivalents.

- Inventory +6% Y/Y.

- $31.6B bonds payable.

- ~0% Y/Y diluted share growth.

- Accounts Receivable Turnover was 26 days vs. 26 Q/Q and 28% Y/Y. Inventory Turnover was 80 days vs. 74 Q/Q but still lower than 83 days Y/Y.

f. Guidance & Valuation

Q2 guidance:

- Q2 revenue guidance beat estimates by 4%.

- Q2 66.5% GPM guidance beat estimates by 230 bps.

- Q2 EBIT guidance beat estimates by 6.6%.

- Tax rate is expected to be 20% for Q2, compared to 17.5% for the full year, as the company accrues undistributed retained earnings. That will be a modest Y/Y EPS growth headwind next quarter.

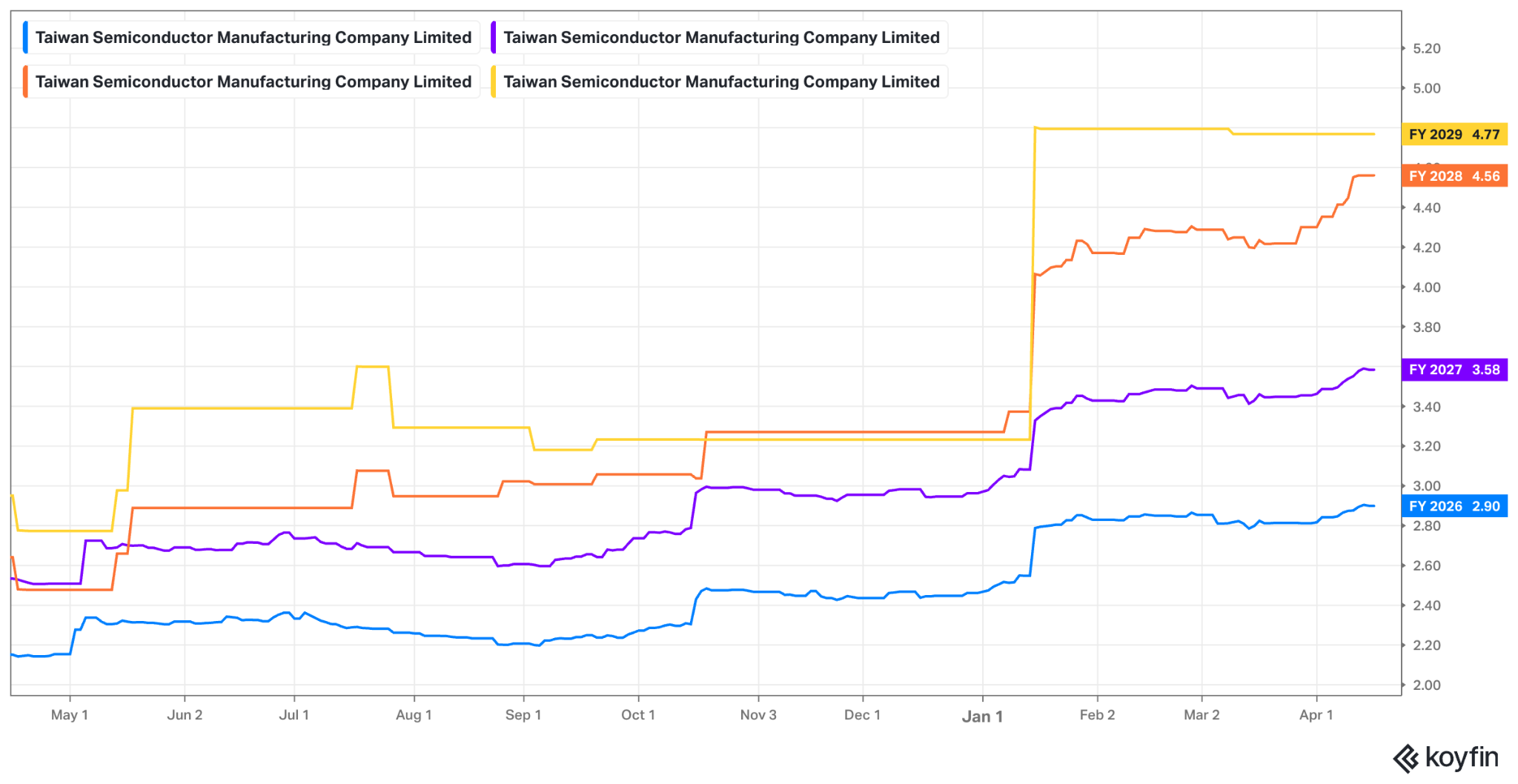

2026 Guidance:

- Raised 2026 CapEx guidance from $54B to ~$56B, above $54.5B estimate. CapEx intensity (CapEx/revenue) is not expected to rise in the coming years. CapEx growth will be offset by more revenue.

- They now expect 2026 revenue growth to be above 30% Y/Y compared to around 30% Y/Y guided to last quarter.

As always, CapEx guidance is the forward-looking demand signal for TSM. That number is intimately correlated with customer interest in their products, looking out over the next several years. When they spend more, it's because customers are asking them to manufacture more. That is what's happening, and it's why the CapEx guidance was sequentially raised by $2 billion this quarter. It's a very similar idea compared to the giant public cloud vendors right now. They are raising their CapEx estimates because they do not have enough capacity to meet demand. While this is a near-term cash flow drag, it is good news for run rate, revenue and profit ceilings, for all of these companies. It is good news for those willing to zoom out and not so obsessively fixate on optimizing a profit number for a single quarter. TSM is playing the long game – as they should be. And despite this raise, they remain committed to profitable growth and boosting their dividend.

Annual guidance balances a few things. On the positive side, and most importantly, AI-related demand remains exceptionally strong. On the other hand, they have baked in a bit more prudence due to all of the global uncertainty currently unfolding. As we'll explore later in the piece, that hasn't yet impacted operations. But they are including this impact in their range of outcomes presented in Q2 and 2026 guidance.

Long-Term Guidance:

No changes to long-term guidance. They continue to target a 56% GPM, a nearly 30% ROE and a 25% revenue CAGR from 2024-2029. That revenue CAGR includes a 57% AI revenue CAGR over the same period. Conversations with customers continue to fortify confidence in these expectations.

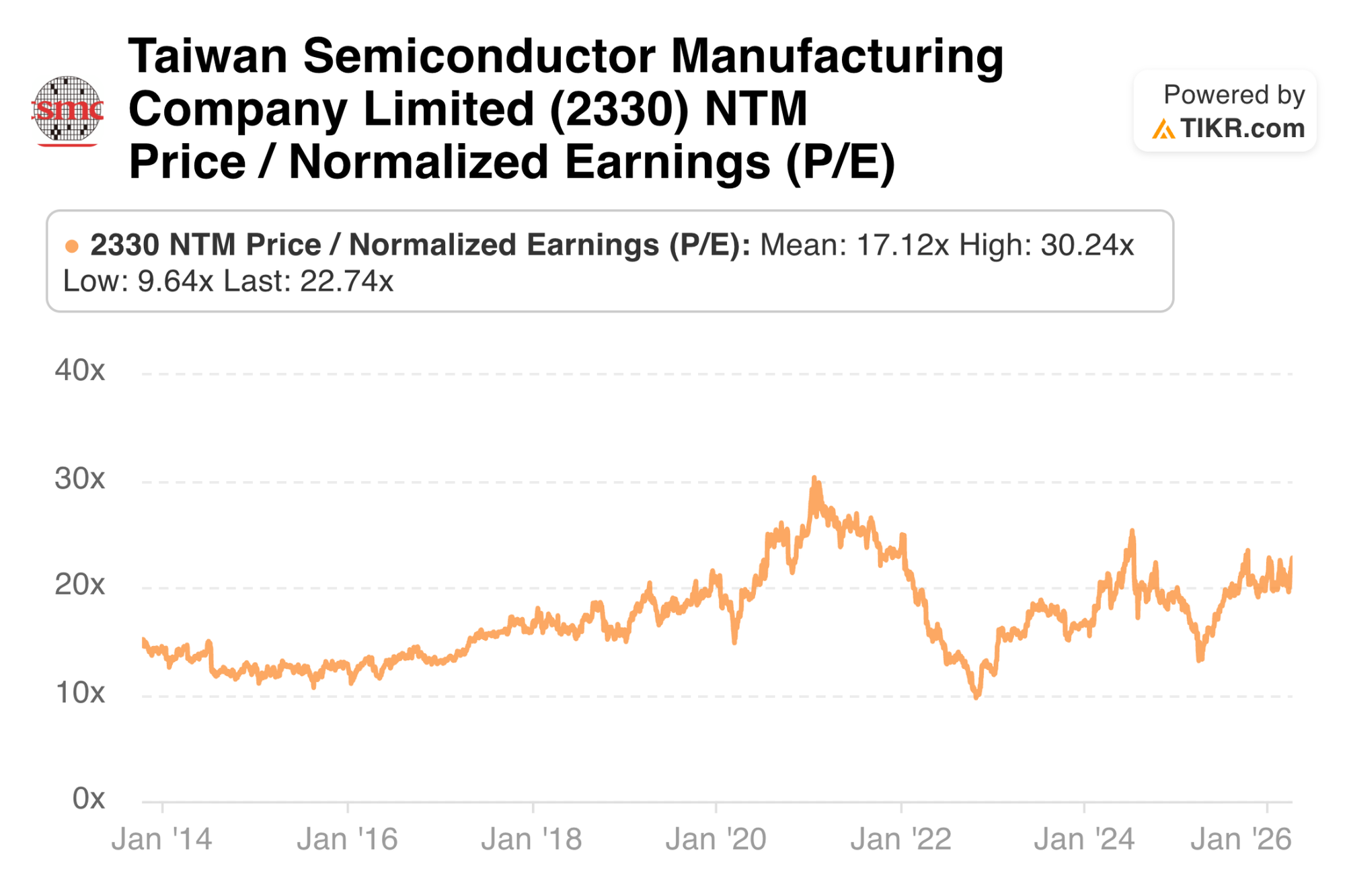

Valuation:

TSM trades for 23x forward EPS. EPS is expected to grow by 38% this year and by 24% next year.

g. Call & Release

More GPM Puts & Takes – Iran War:

There's a new variable to consider for this earnings report that wasn't prevalent three months ago: War. The biggest impact from escalating Middle Eastern tensions on TSM's business would be added pressure on its already tight supply chain. Thankfully, the company’s savvy leadership, deep experience and responsible operations are insulating them from this challenge. Specialty chemical and gas supply is collected from multiple suppliers in different regions around the world. They have plenty of helium, hydrogen, and other needed materials on hand. They do not expect any near-term impact on supply availability or price inflation here.

Energy is the other big consideration, as natural gas and other input costs for companies like TSM rise amid the conflict. In Taiwan, where they continue to boast the convincing majority of their manufacturing footprint, the government has already gotten ahead of the situation and secured needed natural gas supply through the end of next month, at the very least. That means no impact to TSM's Taiwan business, at least in the next six weeks, with the government there working very hard to extend the timeline and subtle signs of easing tensions forming.

Runway:

The multi-year runway continues to look very good in the eyes of TSM leadership, which is why long-term guidance and CapEx expectations remain so lofty. Their customers continue to come back asking for more, and they are doing whatever they can to meet that demand.

As a reminder, TSM does not care if GPU darlings or custom chip disruptors win more market share. They serve the major players on both sides of the equation, and have told investors consistently that the margin profile associated with these different product categories is roughly similar. They are chip designer agnostic.

Wafer & Packaging Competition?

There was a plethora of questions pertaining to established and emerging competition within TSM's chip manufacturing market share domination. Leadership was specifically asked about Tesla's planned TerraFab facility, and whether or not they're concerned about losing some demand from that large customer. They were also asked about ongoing Intel competition, as that US-based competitor tries to enter the chip manufacturing space more meaningfully in the coming years.

As leadership put it, they take every competitor seriously. And these two are certainly no exception. At the same time, they said multiple times that there “are no shortcuts” in building capacity to meet customer demand. These facilities take a couple years to build and a couple years after that to ramp production. They are wildly complex, factories with a web of expensive and cutting-edge technological components that must be perfectly assembled, perfectly implemented, and constantly optimized along the way. It's hard to compete with TSM in this space, which is why the company holds an A position that far more closely resembles a monopoly than Nvidia (a customer) in GPUs or Micron (a customer) in HBM. They remain perpetually paranoid and constantly looking over their shoulder to ensure they remain ahead of the pack. They also remain quite confident that they will remain ahead of this pack.

Back to Intel for a moment. There are modestly growing concerns that Intel's Embedded Multi-Die Interconnect Bridge (EMIB) technology will improve chip connection efficiency by reducing some reliance on silicon interposers (the floor a chip sits on). There are also concerns that this technology will allow Intel to leap ahead of TSM in something called reticle size. TSM and competitors pursue incremental step changes in performance in two ways. First is packing more transistors into the same amount of real estate, which bolsters density and performance per unit. Separately, reticle size refers to the maximum surface area that a lithography machine can work with. As that size rises, TSM's customers enjoy more room to pack more chiplets into, which accomplishes incremental chip performance and latency advantages in a different way.

CoWoS is viewed by some as not being as capable as EMIB when it comes to maximizing reticle size. This led to two questions. First, analysts wanted to know if TSM is willing to partner with Intel and allow them to use their EMIB packaging technology as part of TSM manufacturing programs. They seemed to be amenable to this idea. Second, sell-siders asked TSM when their response to the reticle threat would be ready. This response is called Chip on Panel on Substrate (CoPoS) which eliminates the circular silicon wafer size bottleneck. It does so by moving lithography etching processes to a rectangular panel. The circular design leads to wasted space that this updated process resolves, while the rectangular innovation will eventually be capable of nearly 10Xing maximum CoWoS reticle size. That means more flexibility to pack incremental HBM capacity or other high-performance compute into the same unit, bolstering performance and energy efficiency too.

There are some design challenges like the substrate running into stability issues (called warpage or how materials bend amid heat) as surface area grows. They are almost excited about these issues, as they’re confident in specialized and proprietary materials easing the issues. And? They like when manufacturing is harder because they think they’re better at solving problems than others. CoPoS is on track to debut in June and they also still think their current CoWoS offering is ahead of what Intel currently offers at scale in terms of reticle size.

Tech Roadmap Update & Notable N3 Demand:

Their N2 manufacturing footprint in Taiwan is scaling as expected after reaching high-volume manufacturing capacity during Q4. Perhaps more interesting was the N3 throughput news this quarter. Taiwan Semi doesn't tend to boost production magnitude for a mature node 4 years into its life cycle. They're doing so for N3 as of this quarter because demand levels remain so historically good. This N3 technology is well suited for certain HPC and AI workloads that don't require the latest and greatest Node technology that N2 provides. They expect to bring added output potential online early next year in Taiwan.

They’re doing whatever they can to grow N3 capabilities because the market requires it. In Arizona, their second facility is done and will begin growing production from now through the second half of 2027. There’s also a 2nd facility in Japan that will begin producing N3-based units in 2028. Leadership also continues to shift whatever volume they can from N5 and older product lines to N3 while ensuring these mature nodes have the resources needed to continue meeting demand.

A14 is on schedule for scaled production in 2028. Leadership continues to believe this innovation will deliver a profound step change in key benchmarks. It should deliver 12.5% speed improvements vs. N2 with the same amount of power, or 27.5% power improvements with the same speed, compared to its predecessor. Chip density is expected to be 20% higher as well. They are optimistic that A14 will be yet another successful launch, and will keep the company's best-in-class reputation firmly intact.

Other Notes:

- Memory inflation has impacted their low-end smartphone end market demand but not the high-end where they do more business.

- Their approach to price hikes is unchanged. They will take price when value and cost inflation obviously justify it. They will not abuse that lever.

h. Take

Broken Record Alert: Another great quarter from a world-class company and an elite team. What else is new for Taiwan Semiconductor? This is the chip manufacturing king with a dominant market share position that looks wonderfully defensible. They continue to sprint on their product roadmap and stay ahead of the competition to command the lion's share of the AI chip manufacturing pie. That's not by accident. It's a byproduct of their years of hard work to guarantee their products and reliability are best-in-class.

If there was one company in the AI infrastructure category that I added exposure to, it would be this one. My views on cycle longevity, uncertainty pertaining to when that peak occurs and Taiwan tensions are the only things that keep me on the sidelines for this firm. The lackluster share price reaction is not materially important to me, as it's a byproduct of positioning and sentiment heading into the report more than anything else. The actual numbers and forward guidance were all very good. Bulls should be pleased, in my opinion.