Table of Contents

a. Key Points

- Ongoing supply constraints limited the degree of revenue outperformance.

- Apple is grouping a few services into a newly organized product called Apple Business.

- Margins continue to steadily tick higher on an annual basis.

- Apple is moving away from its net cash neutral goal.

b. Demand

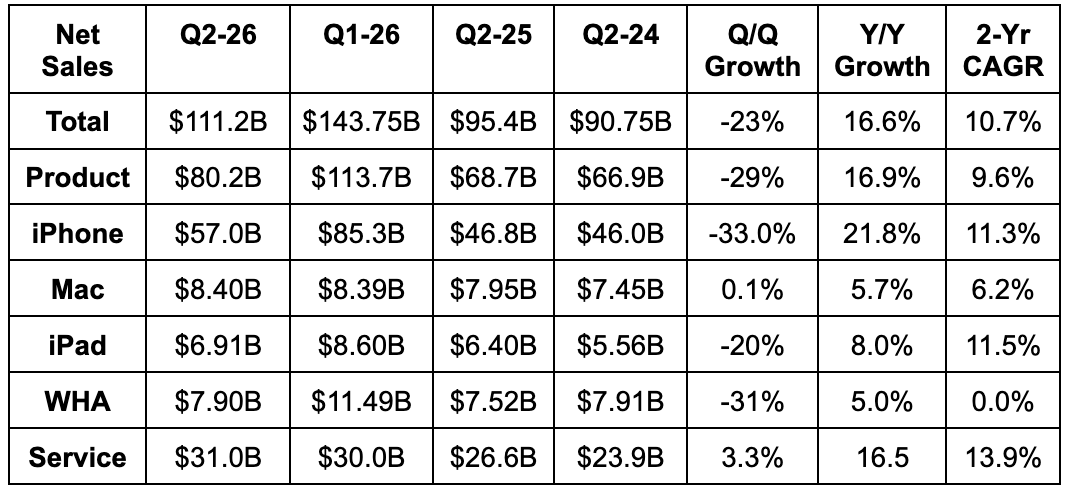

- Beat revenue estimate by 1.4% and beat guidance by 1.8%.

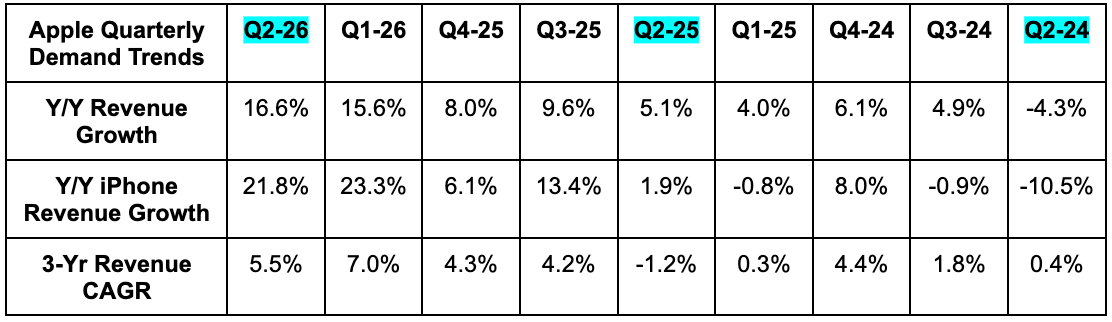

- The revenue beat was despite supply constraints. Currency boosted revenue growth by 2.5 points while supply constraints lowered growth by a modestly higher amount than that. No specific disclosure offered.

- Met iPhone revenue estimate.

- Beat Mac revenue estimate by 3.2%.

- Beat iPad revenue estimate by 4%.

- Beat wearables, home and accessories (WHA) revenue estimate by 2.3%.

- Beat China revenue estimate by 8.4%.

- Beat product revenue estimate by 1%.

- Beat service revenue estimate by 2%.

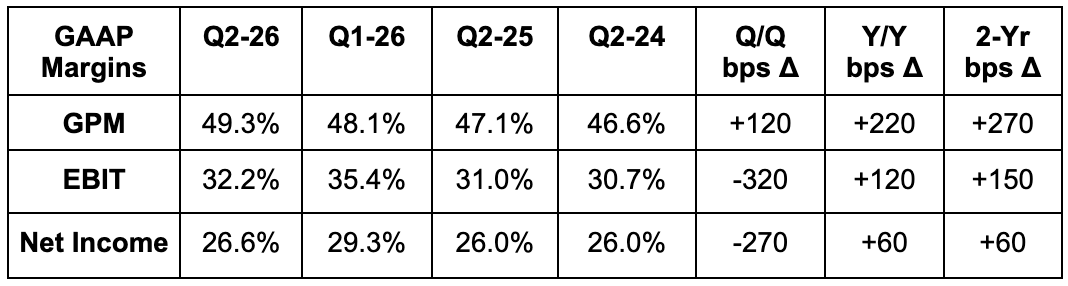

c. Profits

- Beat 48.5% GPM estimate & identical guidance by 80 basis points (bps; 1 basis point = 0.01%) each.

- Product GPM was helped a bit by lower tariffs.

- Beat EBIT estimate by 3.8% and beat guidance by 4.3%.

- OpEx rose by 24% Y/Y.

- Beat $1.96 EPS estimate by $0.05.

- EPS rose by 22% Y/Y.

- Missed FCF estimate by 5%.