Table of Contents

a. Updated Performance Heading Into Earnings

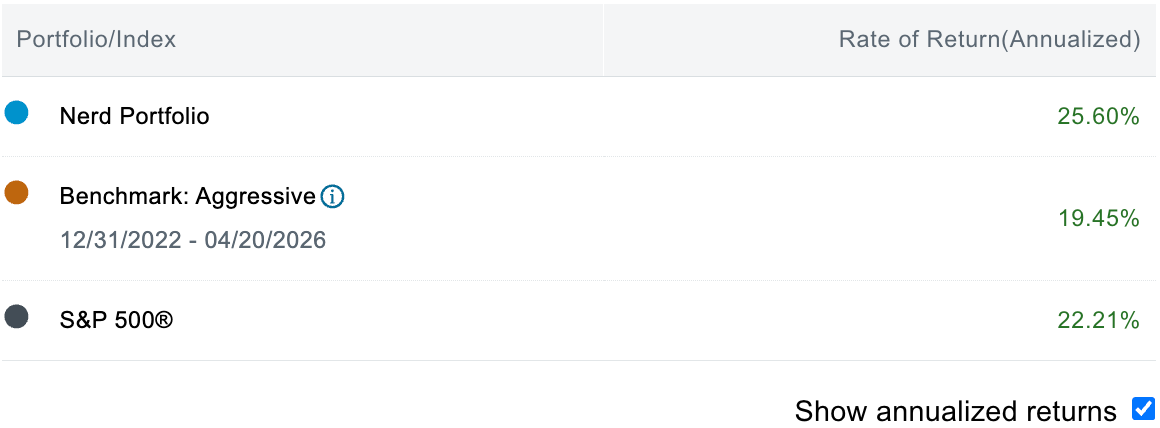

Annualized Performance Since Inception Heading Into Earnings Season (12-31-2022 through today):

b. A Bit on Software

It has been another three months of highly tumultuous price action and negative sentiment aimed at the enterprise software sector. Multiples have continued to plummet with tanking prices paired with stable or even rising estimates. Bears have become more emboldened to dramatically proclaim the death of the entire space. Hedge fund exposure has reached even more extreme lows compared to last quarter alongside relative performance of software vs. chips.

My opinion on this space has not changed. There will be winners that harness this profoundly encouraging technology and use it as a durable financial accelerant. There will be losers that are left behind amid all of the change. The companies that can use these tools and pair them with proprietary data, edge-case mastery, governance perfection, secure operations and better outcomes at lower cost will be just fine. Why would a company spend their finite developer hours building a custom CRM for higher costs instead of focusing on their core operations and using Salesforce for less money? They wouldn’t. They won’t.

I think we’re in for another quarter of strong results and robust guidance for the names that I cover. Channel checks have looked quite good across the board while major integrations, cyber security alliances and partnerships with AI companies continue to form. Business models have been re-shaped to focus on charging for data, API calls and, generally speaking, incremental value. It’s no surprise to see these transitions going so well, as better outcomes will always be monetizable. It doesn’t matter if seats are no longer the best way to express that value. If you’re giving your customers x% more reach or x% lower cost intensity than the other guys can, they’ll stick with you. And? They’ll do so via autonomous agents that can extract work from existing software applications exponentially more frequently than a single seat (person) can. These software companies also have years (often decades) of scaled data ingestion with which to train agents more effectively than others can. Beyond that, they also have the luxury to pick and choose different models with specific specialties to power their new offerings.

All of this is to reiterate that I believe financial results will remain strong for this sector. I remain confident that the putrid price action the industry has experienced over the last several months will be a blip on the long-term radar and is not emblematic of fundamental prospects going forward.

I am less confident that strong reports will lead to explosively positive price action and a normalization in sentiment during this specific quarter. That is not certain and markets are weird. There is no playbook for how much evidence or time investors will need to grow comfortable with these firms again. There is no concrete timeline.

I will continue to fixate on the financial performance of these companies. If they keep delivering in that regard but the stock doesn’t immediately respond? I will remain patient and slowly take advantage of any continued multiple contraction. If the companies stop fundamentally winning? I’ll emotionlessly cut ties, take my loss, and focus on the ones that are performing. That is the plan. The plan does not change because price action has been bad for a few months.

Now, onto specific names and my expectations for each report. As a reminder, these are my best educated expectations for how I think reports will go this season. It is inevitable that I will be wrong in some of these, so please do not take them as certainties. Furthermore, I focus closely on fundamental data rather than the immediate share price reaction following an earnings call. I do not predict how a stock will react, and focus on how the company will perform instead. Our view is that over the long term, price follows fundamentals.