Table of Contents

Hims sells men’s and women’s health products with a direct-to-consumer (DTC) business model. It allows users to more comfortably access sensitive prescriptions within areas like erectile dysfunction or hair loss, without going to an office or a pharmacy. Products are mailed right to a consumer’s door.

It offers standard and personalized medicine and subscriptions. Personalization is enabled & amplified by its electronic medical record (EMR) system. From its early days, Hims built this EMR foundation to enable scalable data ingestion, automate tedious provider work and foster rapid product expansion. That remains absolutely vital in the firm’s future. It paved the way for MedMatch, which is the company’s tool that uses all customer interactions and data to uncover valuable consumer insight and nudge best provider practices. It also enabled Clever Routing, which contextualizes individual user needs to prioritize and match demand with proper levels of care.

a. Key Points

- Investing aggressively in future growth and accepting some margin pressure.

- Ongoing GLP-1-related investigations.

- Accelerating pace of new category and product introductions.

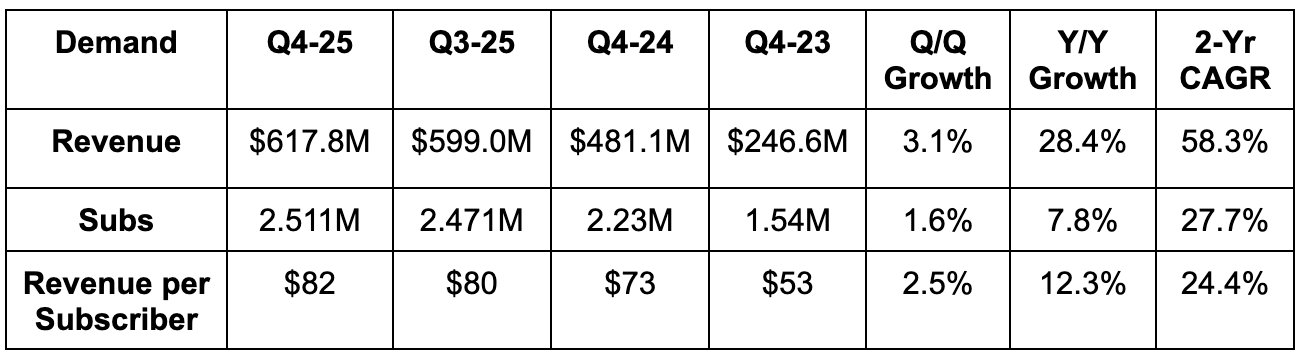

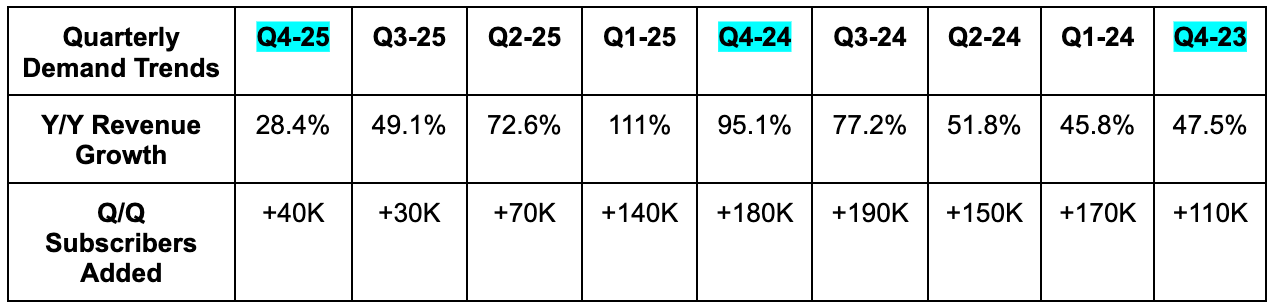

b. Demand

- Slightly beat revenue estimates & slightly beat revenue guidance.

- Missed subscriber estimates by 3.5%.

- Non-personalized subscriptions fell by 10% Y/Y; personalized rose by 33% Y/Y.

2025 Hims brand revenue rose 30% Y/Y despite sexual health business disruption headwinds from an intentional shift to daily solutions. That headwind will be lapped later in 2026. The Hers brand for 2025 delivered 100%+ Y/Y growth. It’s now close to $1B/year in revenue on its own and is already 40% of the company’s total U.S. business.

Note that HIMS is switching weight loss demand fulfillment from 3rd parties to using its own facilities. This results in smaller shipments to customers, lower revenue per order and some timing-based revenue growth headwinds. This resulted in a $40M revenue headwind during Q3 & Q4, which was $17.5M larger than expected.

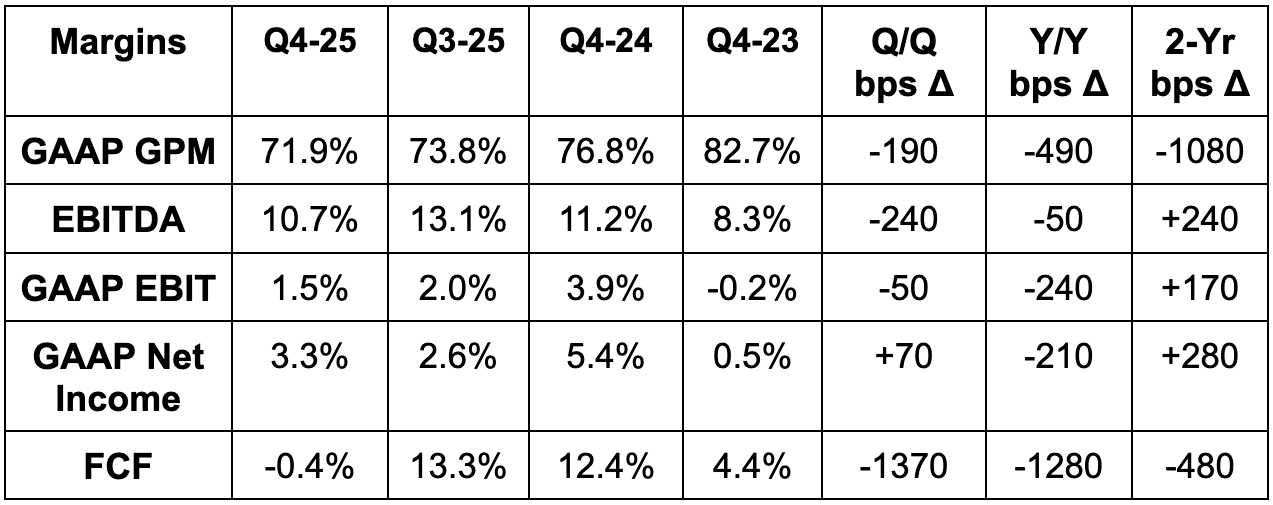

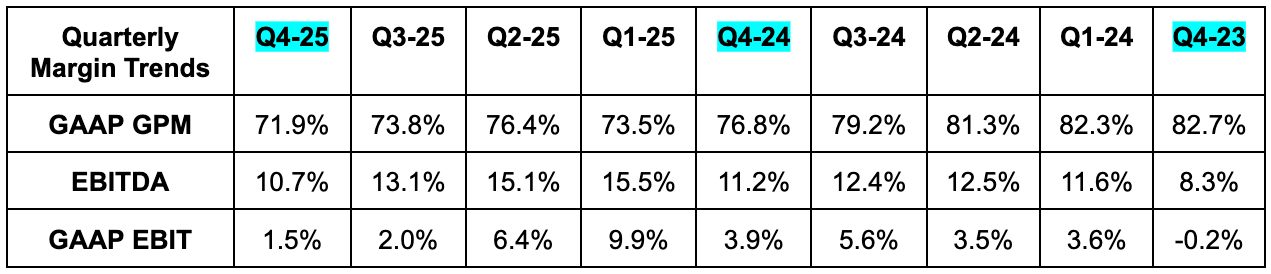

c. Profits & Margins

- Missed GAAP GPM estimates by 200 basis points (bps; 1 basis point = 0.01%).

- GPM was pressured by international growth and investments, as well as new specialty launches.

- Beat $0.05 GAAP EPS estimates by $0.03.

- Beat EBITDA estimates by 9.8% & beat guidance by 10.5%.

- Missed $12M FCF estimates by $15M.

For 2025, EBITDA margin expanded by about 200 bps. Pretty much all of the leverage is coming from sales and marketing, as that expense line as a percentage of revenue for the year was 39% versus 46% for 2024. Rising brand awareness, more cross-selling, and more data-driven refinement are all helping drive efficiency and EBITDA leverage despite the GPM contraction. G&A was flat as a percentage of total revenue for 2025.

While net income rose by just 8% Y/Y, EBT (pre-tax income) for 2025 rose by more than 100%; slower net income growth was due to lapping a $50M+ tax benefit. FCF for the full year fell from $139M to $60M due to CapEx rising from $17M to $167M as the company aggressively pursues growth.

d. Balance Sheet

- $570M in cash & equivalents.

- $350M in investments.

- $972M in convertible senior notes.

- 3.1% Y/Y diluted share growth.

HIMs spent $1.15B in total for Eucalyptus (international telehealth company). Of that amount, $240M will be paid via upfront cash considerations, with the rest paid out over time as fundamental milestones are reached through 2029. Leadership hinted at being open to accessing debt or equity markets to bolster balance sheet flexibility if they see a great opportunity to do so. At the same time, they plan to fund "the majority" of this deal with cash generated by the business.