For a quick and informative overview of Micron’s business, click here.

Table of Contents

a. Key Points

- Supply tightness expected to last through 2027.

- Signing more multi-year customer commitments.

- Record growth and margins.

b. Demand

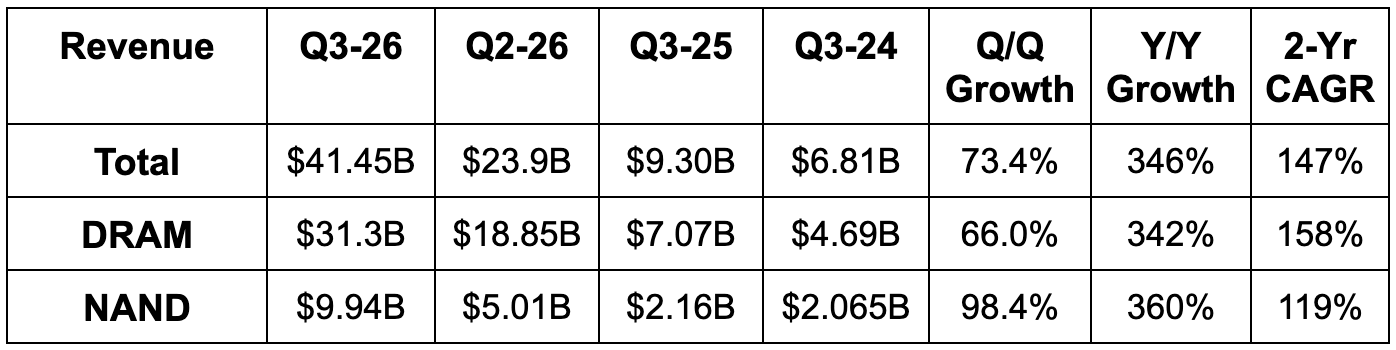

- Beat revenue estimate by 16.8% & beat guide by 23.7%.

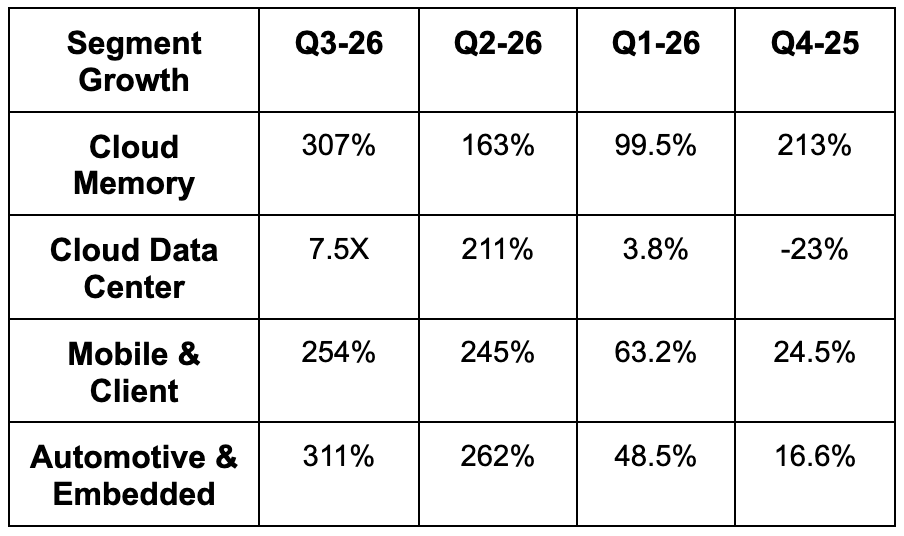

- Beat cloud memory revenue estimate by 15%.

- Beat core data center revenue estimate by 69%.

- Beat mobile & client revenue estimate by 18%.

- Beat auto & embedded revenue estimate by 32%.

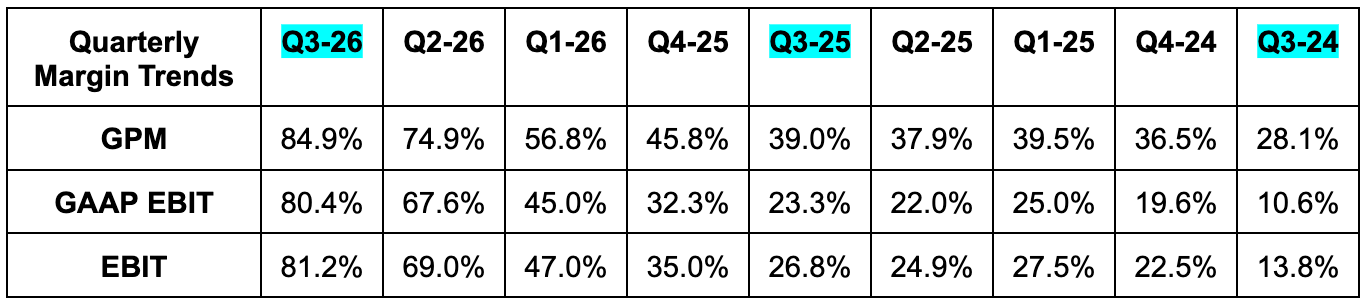

c. Profits & Margins

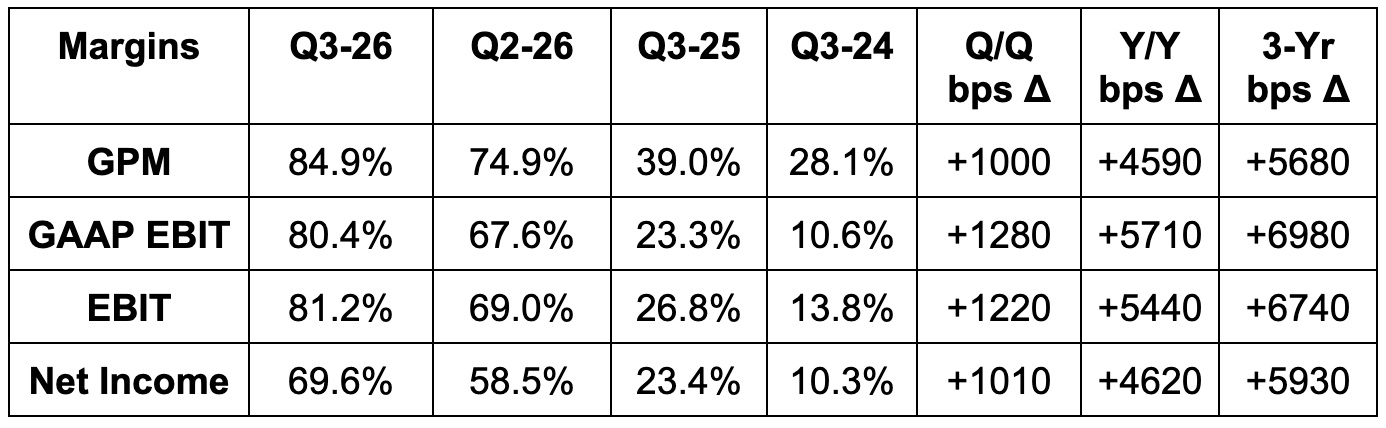

- Beat 82.2% GPM estimates by 270 basis points (bps) & beat guidance by 390 bps.

- Beat EBIT estimates by 22% and beat guidance by 25%.

- Beat $20.39 EPS estimates by $4.72 & beat guidance by $5.96.

- The company earned $1.91 last year compared to $25.11 this year. Incredible earnings growth.

d. Balance Sheet

- $26B cash & equivalents.

- $5B investments.

- 4% Y/Y inventory growth.

- $5.6B debt.

- 1.8% Y/Y dilution.

- Received credit rating upgrades from the 3 major agencies.

e. Q4 Guidance & Valuation

- Revenue guide beat estimate by 16.8%.

- 84% GPM guide beat estimate by 200 basis points.

- $31 EPS guide beat estimates by $6.

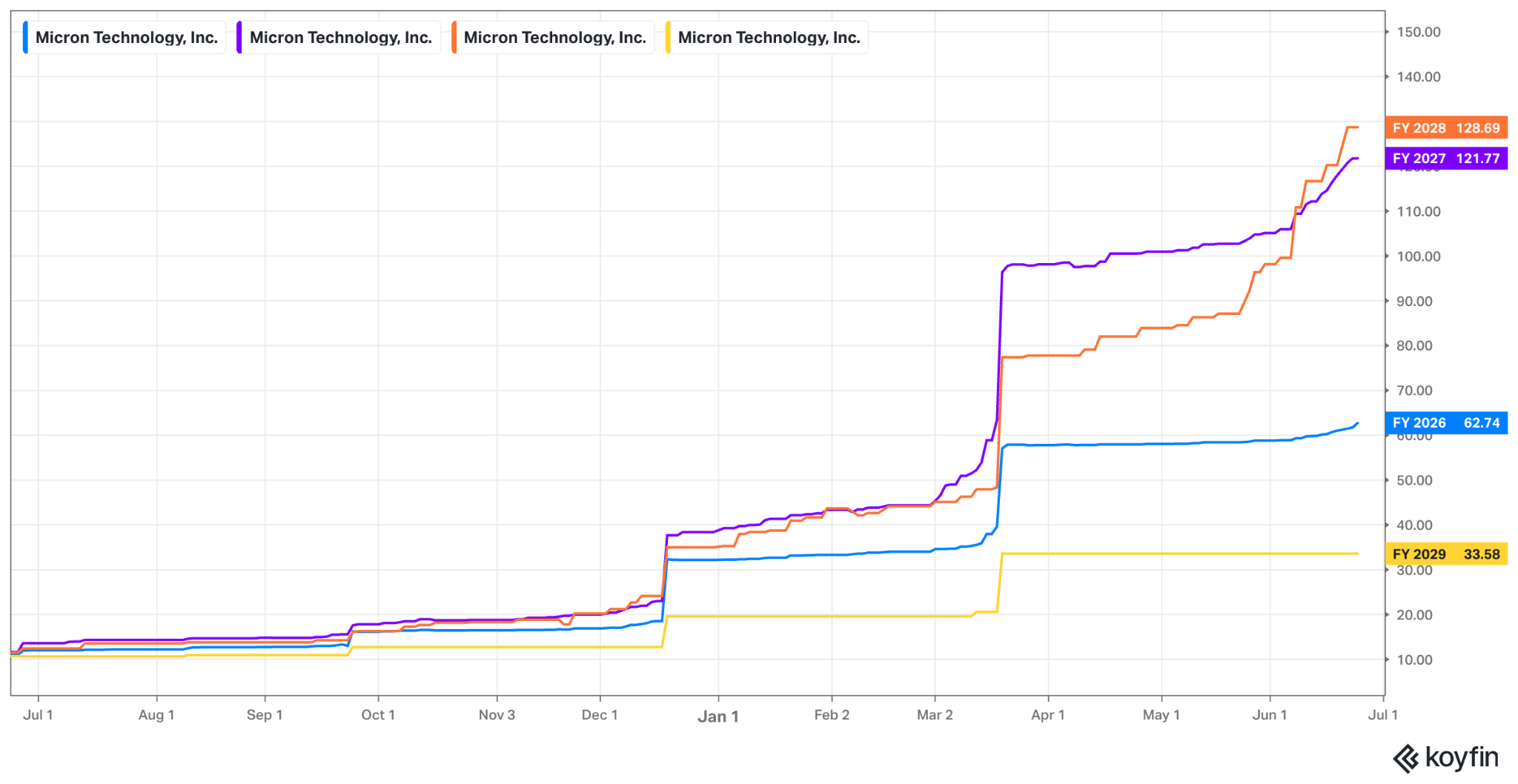

- It guided to $10B in Q4 CapEx, meaning it raised annual CapEx guidance from $25B to $27B. FCF is still expected to meaningfully improve in Q4. They think 2027 CapEx will be over $40B.

- In 2027, two years after the CHIPS agreement, Micron will increase shareholder returns

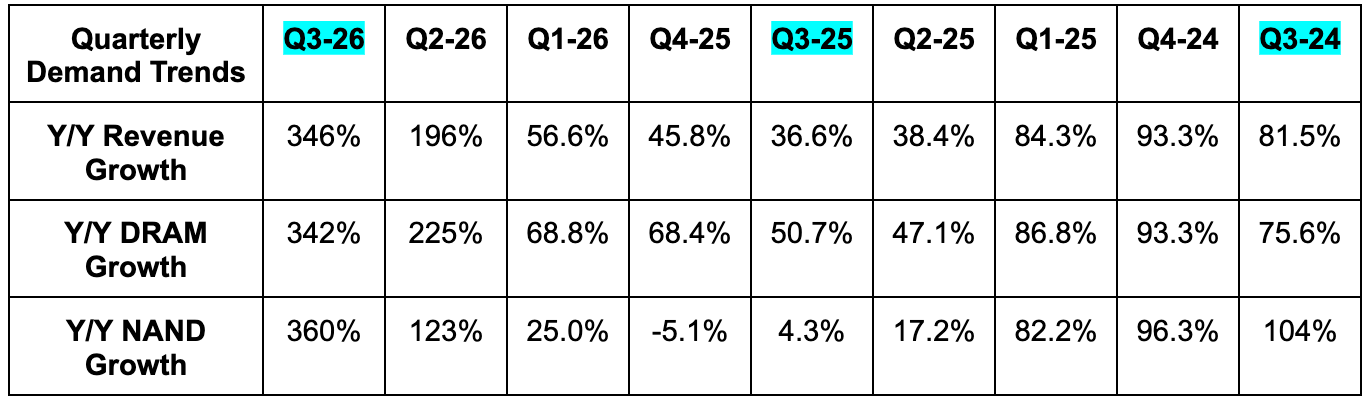

Micron now sees about 23% DRAM volume growth for the year, which is a little better than previously guided to. They continue to see about 20% NAND volume growth. The sharp outperformance and guidance beat vs. consensus is coming from fantastic pricing power, with sequential pricing across DRAM and NAND rising by 60%+.

Micron trades for 10x forward EPS and likely closer to 8x or 9x following this report. EPS is expected to grow by 650% this year, 94% next year and 6% the year after.

f. Call & Release

Cycle Longevity:

The most important update on the call was leadership’s positive view of how long AI-driven memory supply tightness would persist. They’re racing as quickly as they can to add supply, but that takes a long time and is only getting more complicated with new hardware iterations. In part because of this, Micron now expects “tightness” to last “beyond” calendar 2027, with “no line of sight as to when memory supply catches up to demand.” That’s essentially them saying this could last well into 2028 if current conditions persist. And better yet for Micron when supply does start to improve in 2028, they only expect it to do so "gradually" while demand keeps climbing on its long-term AI trajectory. Demand is rocking. Supply is scarce. The supercycle marches on.

Supply scarcity is also not just a DRAM-specific reality. It extends to NAND as well. Industry suppliers have been shifting cleanroom capacity from NAND to DRAM for several quarters now. Strong levels of demand are compounding this issue and creating NAND scarcity with fantastic pricing power.

An Improving Business Model:

While visibility for memory providers has never been a strength, Micron is taking advantage of historically strong demand to productively evolve its business model to something a tad more predictable. Their ongoing shift to multi-year Strategic Customer Agreements (SCAs) is going quite well, with 16 contracts signed including 7 larger customers. In total, these deals represent 20% of committed DRAM volume and 33% of NAND volume through calendar 2030. That’s expected to reach 50% of total volume in the coming quarters (40% under fixed or semi-fixed pricing). And these aren't informal agreements. They’re binding commitments that require purchasing set volumes regardless of need over the course of the contract.

In total, these 3-5 year arrangements represent $100B in backlog. And management said that should be seen as a minimum, with ample upside beyond this level. Vitally, some of the contracts feature fixed prices and others offer price bands with minimums, allowing Micron to net a gross margin above any previous cycle peaks. And to make this even more attractive from a cash conversion cycle point of view, Micron has already notched $22B in future deposit commitments from signed SCAs to date (roughly $18B of that in cash deposits, the rest in letters of credit). They’ve just started collecting, with about $10B of cash landing in fiscal Q4.

I do not agree with those who believe memory is no longer cyclical. I think this specific cycle is especially remarkable and not showing signs of slowing down, but there will be an end to it at some point in the coming years. Micron locking in favorable financial terms through 2030 with solid expected margins and large volumes makes all the sense in the world. It allows them to flex their current market strength to ensure their financials don’t cycle quite as sharply in the future.

One more note on cycle health driving remarkable demand at lofty prices. Micron now expects blended DRAM cost per bit to rise from current levels in the years ahead. That’s very notable, considering the memory sector has featured bit deflation for years and years. Mix-shift to higher-value products and expensive capacity investments are the reasons. This is why SCAs are so important. If Micron is going to be eating higher costs, they need to know they’ll be compensated fairly for doing so. This helps a ton in that regard.

HBM4:

The HBM4 12-high product is scaling at twice the pace of its predecessor, with Micron already crossing $1B in total HBM4 revenue and this product being a big reason why. This should approach yield maturity faster than the old model as well, which will support even more operating leverage and provide another margin tailwind.

One more note on HBM. Micron is intentionally keeping its HBM market share close to its overall DRAM share rather than chasing it higher. Why? Because HBM uses a disproportionate amount of wafer capacity, which pressures non-HBM supply. By keeping HBM share capped, Micron protects its ability to serve the diversified non-HBM demand across consumer, auto, and industrial. All of these markets are bit-constrained and Micron needs to account for that in its planning.

Technology Roadmap and Product Leadership:

- The 1-gamma DRAM node and G9 NAND node are both ramping nicely and on track to become the highest-volume nodes in the company's history. Next-generation nodes beyond these are in development and on schedule to begin volume production in about a year.

- On the server DRAM side, its new Double Data Rate Registered Dual In-Line Memory Module (DDR RDIMM) officially shipped samples and is poised to be highly popular for large data storage needs as a complement to HBM utility.

- On DRAM pricing in general, they expect market conditions to support more increases in the quarters to come. Complexity is rising, supply conditions aren’t improving and Micron has earned the right to flex its pricing power.

In DRAM:

- Its newest high-performance laptop low-power memory product (LP5X SOCAMM2) are in high-volume production on schedule.

- Its newest smartphone memory product (1-gamma LPDDR5X) just started volume production.

- Its newest automotive memory product (1-gamma LPDDR5), which is purpose built for extremely volatile physical conditions, “reached product readiness” with samples now on the way.

In NAND:

- Its newest high-performance data center storage (G9-based PCIe Gen6 SSD) is now in high-volume production.

- Shipments have officially commenced for its massive, high-capacity SSD (245TB QLC SSD).

- Its latest automotive-grade storage (G9-based UFS 4.1), which provides high-speed, safety-compliant data access for AI-driven vehicles, has begun its first volume shipments.

- Its data center SSD business crossed $5B, representing 100%+ Q/Q growth.

Micron also signed a multiyear EUV supply agreement with ASML to support increased EUV adoption at the 1-delta node and beyond. That's a tangible step toward securing the most critical (and scarcest) lithography tooling for future node transitions.

Demand by End Market:

Data center demand continues to lead the way for Micron. Shipments are expected to double Y/Y during calendar 2026, as agentic AI creates an explosion in memory needs. Whether that’s for rapid GPU-based processes or helping CPU-based compute orchestrate work and store needed information, tailwinds for Micron’s products remain abundant. This momentum helped them raise their industry server unit growth forecast from about 12% to about 18% for 2026. There's a small item worth noting here. That higher unit count is partly enabled by customers accepting lower average DRAM content per server. Why? Because memory is so tightly allocated right now that buyers are choosing to maximize the number of servers they ship rather than max out the memory in each one. More boxes, a little less memory per box.

On the personal computer (PC) side of things, web-based assistants like OpenClaw and NemoClaw are creating a boom in memory needs and another leg of demand for Micron’s business amid this technological revolution. And there’s more. In automotive, Level 2+ autonomy cars are expected to move from 20% of total to 40% of total over the next 5 years. And? These cars consume 5x more memory than older models. And with humanoid robotics, the picture is even more promising with those products using 10x more memory than autonomous cars. Everywhere you look, tailwinds for Micron’s business keep raging.

Manufacturing Footprint:

The Idaho and New York facilities are on schedule. Output from the first Idaho facility will begin in about a year, with ramps across all 3 helping to ease supply constraints into 2028. Elsewhere in the states, it just started production in its new Virginia facility. They also expect their purchased location in Taiwan to begin production in about a year, which is one quarter earlier than previously forecasted. Finally, they've begun building a second, similar-sized cleanroom in Taiwan to house future EUV equipment. Generally speaking, ongoing work to shrink installation times, expedite ramps and improve tooling are bearing fruit.

g. Take

This can be short and sweet. Phenomenal quarter. Pricing power is amazingly impressive right now and should remain that way as long as supply/demand dynamics remain tight. Based on leadership commentary, they think they have at least another 6 quarters of that. Meaning? The cycle continues to rock and this is one of the primary beneficiaries.