1. The Trade Desk (TTD) – Earnings Review

a. The Trade Desk 101

The Trade Desk is a leading buy-side player in open internet advertising. The firm’s two most compelling revenue segments are streaming and retail media. In these segments, it has tight relationships with most of the leading streamers and stores. Its platform allows advertisers to bid on & purchase impressions with surgical precision, scale and open reporting. Purchases are essentially made on an impression-by-impression basis, uplifting targeting efficacy and doubling return on ad spend (ROAS). Needed data is infused into every purchasing decision to ensure placements provide optimal value. With this company, advertisers are not required to commit millions upfront to reach audiences. They can commit to smaller targeted purchases in real-time and with fantastic accuracy. No more guessing. No more “spray and pray.”

Kokai is the name of its data-driven, AI-copilot-powered platform. It combines TTD’s leading open internet scale with its vast roster of partners to inject more data and signal into each decision. It’s what tells advertisers who they should be targeting. Kokai does so through TTD’s decade of experience that allows it to essentially find groups of high-intent “copycat customers” with similar interests. Advertisers onboard their own data (what TTD calls “concentrated data seeds”) and The Trade Desk does the rest. Kokai allows buyers to focus on whichever variable, key performance indicator (KPI) or campaign objective they’d like to. Finally, Kokai emulates the ease of data onboarding that has made Alphabet and Meta so popular.

Unified ID 2.0 (UID2) is its open internet, omnichannel identifier. It uses hashed emails to responsibly ensure consumer and brand security. It knows exactly who is accessing what site or app. Kokai tells you who to target, while UID2 is what tells you where they are.

Other products include:

- OpenPath allows publishers on the sell-side to directly plug into TTD’s buy-side platform. It “shines a light on where advertising value is, where that value is being obscured and what signals advertisers value the most.” It does not replace sell-side programmatic players like Magnite, as it does not do things like yield management for these publishers. It’s just TTD’s way of cleaning up the supply chain and letting publishers with their own resources connect more easily. This way, publishers gain a better understanding of impression value and buyers get a better view into what they’re buying.

- Galileo is the firm’s product for ensuring seamless, automated first-party data onboarding.

- TV Quality Index (TVQI) uncovers the incremental value of professionally produced content as compared to user-generated content.

- Deal Desk offers conflict of interest-free “deal quality scores” for both parties to know exactly how well campaigns are performing. It’s a supply chain optimization tool. This comes with an easy ability to rapidly tweak inventory tied to a specific channel if performance isn’t good.

OpenPath and UID2 are meant to support the sell-side rather than supplant it. TTD does not want to build a sell-side platform. It wants to exclusively represent the buy-side to eliminate conflict of interest. Helping sell-siders with identity and supply chain is meant to help its buyers enjoy more success.

b. Key Points

- Another underwhelming forward guide.

- They’re confident that changes made in 2025 are working.

- Joint Business Plan (JBP) volume grew by 100% Y/Y.

- They expect a flat Y/Y EBITDA margin for 2026.

c. Demand

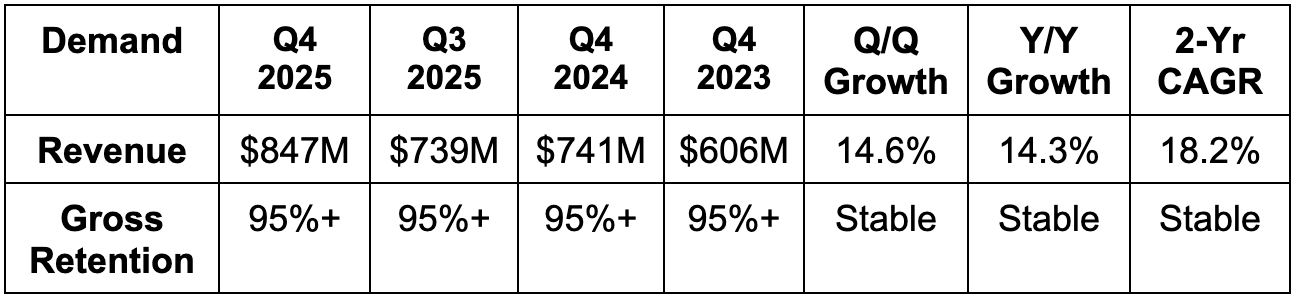

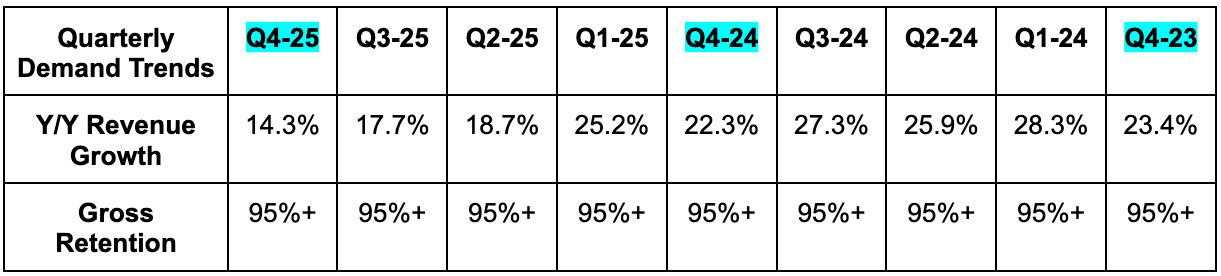

The Trade Desk beat revenue estimates by 0.7% & beat its “at least” guidance by 0.8%. Revenue growth ex-political spend was 19% Y/Y. Audio was its fastest-growing segment, while connected TV (CTV) continued to outpace overall company growth as well.

Take rate was 21.6% vs. 20.3% Y/Y and nearly 20% two years ago. They continue to grow their take rate (annual revenue divided by total spend), despite that being a clear concern amongst bears. I think that's a very encouraging sign, considering all of the articles we've seen about Amazon endlessly undercutting TTD’s fees and winning more budgets.

d. Profits & Margins

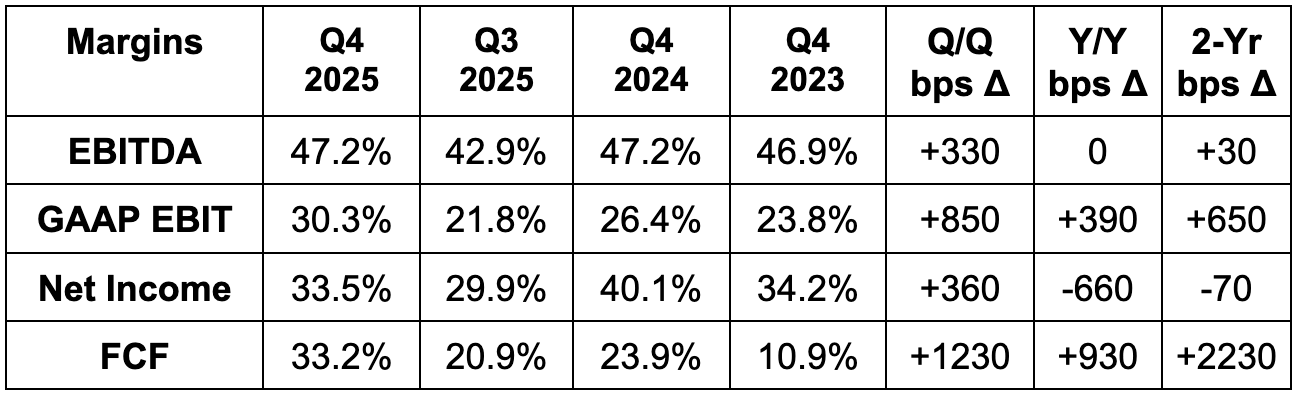

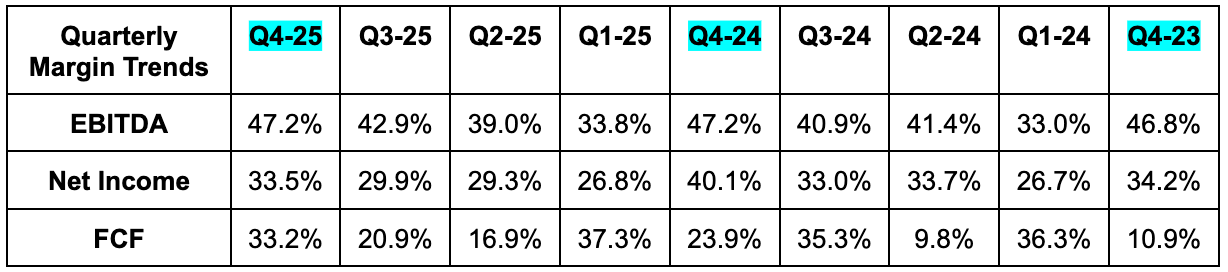

- Beat EBITDA estimates by 6.4% & beat guidance by 6.6%.

- OpEx rose by 15% Y/Y while GAAP OpEx rose by 8% Y/Y.

- Beat $0.58 EPS estimates by $0.01.

- EPS was flat Y/Y.

- GAAP EPS and EPS are quickly converging, which is great to see and is a byproduct of stock-based compensation modestly declining Y/Y. Still over 20% of revenue, but moving in the right direction.

- GAAP EPS rose from $0.36 to $0.39 Y/Y.

e. Balance Sheet

The company added more buyback capacity during the quarter to reach $500M in total. That's around 4% of the market cap.

f. Guidance & Valuation

Guidance reflects prudence surrounding ongoing weakness seen within their automotive and consumer packaged goods verticals. Much more on this later. For the full year, they expect EBITDA margin to be relatively flat vs. 2025. The expected decline in Q1 EBITDA margin is related to infrastructure build-out timing as they transition to their own data centers. Following the call, revenue estimates for 2026 fell by another 5%, while EBITDA estimates for the same year fell by another 7%. This follows ongoing negative estimate revisions for the last year. For more context, current fiscal year 2026 revenue estimates are 18% lower than they were just 12 months ago.

g. Call & Release

Macro:

Green spent more of his prepared remarks talking about the macro backdrop than during any TTD quarter I can remember. He talked about how strong spend was for several verticals throughout 2025, but that consumer packaged goods and auto specifically were notable weak spots. Those industries represent two very large customer cohorts for this firm and slowed down Y/Y growth rates by a full 5 points this quarter. Some of these customers are still in position to play offense and are leaning into biddable programmatic advertising, more granular decision-making, and The Trade Desk’s platform. These customers are enjoying good outcomes and results like they normally would. At the same time, some customers within these two industries are struggling with tariffs and what Trade Desk is calling geopolitical and economic uncertainty. They're in cost-cutting mode, and marketing is among the easiest buckets to reduce during times of uncertainty.

They're right about that, but I just can't help but think we are not hearing the same things from Amazon, Meta, Google, or other pure-play advertising companies. I realize some large brands are talking about weakness and slowing down marketing spend in global investor events. I realize TTD skews to larger customers that are more global and pay more tariffs. I realize TTD gets nearly 25% of their revenue from these two industries. Still… macro isn’t starkly different for other advertising companies that seem to be faring much better at the moment.

We are not hearing Amazon or Google or AppLovin talk about CPG or auto as a weak point. What we are seeing is advertising trends remain at least stable, if not improving for those companies. Furthermore, we've now seen underwhelming execution for this company for most of the last five quarters. It's a lot easier to accept a macro excuse when it does not coincide with a messy Kokai launch, rapid C-suite turnover, overhauled team structures and the underwhelming guidance we see above. The combination of Trade Desk making more macro excuses than pretty much everyone else, and these last five quarters in which we've seen forward sell-side estimates plummet, leads bears to loudly proclaim Amazon is eating their lunch and agentic AI is disintermediating their relationship with brands. It's very hard to argue against that thinking right now. There’s not enough concrete evidence for me to confidently do so. And believe me… I want to. I want to own this company again. I want to believe in Jeff Green again. I just won’t while the most positive part of this call was him saying how amazing everything is for the company’s future. Those words don’t mean much right now. Better results with sustainably accelerating growth would… and it doesn’t sound like that’s coming in Q1. I hope I’m wrong.

Long-Term Opportunity:

TTD remains highly confident in the long-term opportunity. In fairness, they say this every single quarter and talk as if everything is fantastic and amazing. Still, it is nice to hear they remain optimistic. According to Green, 2025 marked the largest year for supply growth in a long time. Considering TTD supports buyers, that creates more of a buyer's market and favors their demand side niche.

Next, they do think all of the rather disruptive changes (and then more changes) they made throughout 2025 are beginning to work. The clearest sign of this is 100% year-over-year growth in joint business partnership volume. That was by far the most positive part of the call and is something I found exciting. More evidence like that, please.

They also remain convinced that their platform delivers better results than the competition. Green pushed back against the appeal of "cheap reach" that giants like Amazon can offer customers. He offered a case study showing how Trade Desk's more relevant data + their seemingly superior ability to use it is a winning combination. For a leading appliance manufacturer, they were able to drive 70% more reach at 30% lower cost. Trade Desk also delivered a 6x better campaign goal delivery rate vs. Amazon in a head-to-head showdown.

Amazon does have more access to customer data. It can materially undercut TTD and use its own demand side platform as a loss leader to fuel customer relationships and growth across the rest of its commerce and cloud products. That does give them some significant advantage. At the same time, Trade Desk is far more focused on programmatic advertising than Amazon. They don't have 50 other priorities. TTD’s goal to take care of advertisers is priority one of one.

They have decades of experience in using highly relevant and granular customer data to precisely match buyers with the perfect impression. And? They are unbiased. They do not own any supply and do not have any conflict of interest in the process of pairing demand with supply. Amazon has a natural incentive to place their networks' demand with their own impressions across the commerce marketplace and Prime Video. They simply make way more money when that's where dollars are spent, as they get to double dip. Well, that's awesome for them and is turning Amazon's advertising business into a juggernaut very quickly. It also leaves a large space in the market for someone who can help these buyers without making them feel like they're also competing with them. TTD is adamant that they will continue to be that platform, and they remain exceedingly optimistic that they will "take the lion's share" of the programmatic advertising opportunity. And in Jeff Green's conversations with large advertisers, he does think they're beginning to understand that a lower upfront fee from Amazon and Google doesn't actually mean higher return on ad spend. How campaigns actually perform is far more important for stretching ad dollars as far as they can go.

All of this explains why TTD does not think the competitive environment is deteriorating, despite all of the drama over the last five quarters. On the other hand, they’ve stopped saying that Amazon is not a competitor. I realize the opportunity is gigantic and Amazon growing will in no way prevent TTD from also growing, but they are competing for the same pie. Just like Google DV360 Amazon is competition, even if they're not doing things the exact same way Trade Desk is doing them. Full funnel advertising (from dollar to sale with one single vendor like Amazon) is very appealing to many and is part of this overall market. Now they're arguing that Amazon will never be as strong of competition as Google was, because they compete with way more of their potential advertisers than Google ever has. That's a lot more fair.

The last year to them is a blip on the radar, and they expect to get back to their normal self at some point this year. We shall see. They've done a lot of fun talking for several quarters, and I want to see them prove it before I get excited.

AI:

100% of TTD clients are now running on the AI-powered Kokai platform. They view this as "the most advanced AI-fueled buying platform ever pointed at the open internet.” It was certainly a messy launch, but, from my outsider perspective it seems like they fixed a lot of the front-end issues and adoption rates followed suit.

In terms of defensibility against agentic AI disruptors and vibe-coded alternatives to TTD’s campaign-building platform, the company remains adamant that they're safe. Their massive open internet scale means massive access to proprietary customer data that OpenAI and Anthropic don't innately have. They see 20 million ad opportunities per second and pair that with first-party data from countless Global 2000 brands to create a scaled, high-quality data repository and drive better campaigns.

On the other side of the competitive equation, Google and Amazon obviously have a lot more data to train their own AI campaign algorithms, but TTD thinks it has more specific and relevant data for each individual customer. They think they understand exactly what data is useful in each instance and apply that into highly complex campaigns with a simplistic, intuitive user interface. They don’t think that will be replaced by AI darlings or mega-caps.

Finally, they do not think agentic AI will change a customer’s relationship with, and love for brands. They think brand awareness, quality scores, and how those brands interact with customers will remain highly important. I partially agree. I think the acceleration of agentic commerce could pair customers with beloved brands more efficiently through chatbot interfaces. That is possible in my mind, and it could erode website traffic and app traffic that TTD uses as part of its overall inventory access.

Conversely, I don't think customers will stop having deep connections with brands or pre-existing concrete ideas of what they want to buy before ever asking a chatbot to find it. Their audio business and their CTV business (their fastest growing segments) also aren’t at all vulnerable to this issue. If anything, vastly enhanced productivity will mean people have much more time on their hands, which should mean more impressions across TV, movies, podcasts, and music. Entertainment would benefit from that scenario.

- Like many other companies, TTD is using AI to get far more efficient and prolific in code writing.

Product Innovation:

As a reminder, Audience Unlimited allows companies to tap into TTD’s 3P data access more seamlessly and affordably. The company thinks third-party data has been “massively underutilized” due to a lack of price discovery. If TTD can be the vendor that uncovers what third-party data a customer should want for their campaigns and gives them affordable access, they should build more sticky and valuable customer relationships. That's the idea here. This is TTD leveraging its long list of relationships with high-profile streamers, retailers, auto manufacturers, and so many other industries to borrow insight from each of them, aggregate that insight, and apply it to campaigns on behalf of its customers. So far, campaigns using Audience Unlimited are enjoying better results vs. those that aren't, and TTD has more measurement and AI upgrades to make this year to grow that benefit.

Ongoing Kokai user interface simplification has been a key part of improved adoption trends. They’re making the platform easier to interact with, which helped IKEA cut customer acquisition cost by 17% and Best Western boost reach by 89%. Not because the tech got better… but because the bells and whistles got easier to use.

This is also making it easy to compare TTD results to the mega cap competitors on an apples-to-apples manner. They’re confident that will help clearly illustrate their value proposition and their ability to deliver better outcomes.

- Deal Desk enhances deal transparency, tracking and, in turn, quality. It’s delivering a noticeable uplift in advertising performance vs. customers not using this Kokai features. In tandem with OpenPath, it’s clear how this can cut the inefficiency and bloat from the supply chain, improve publisher/advertiser work efficiency and make every valuable part of the supply chain better off.

- Green was asked about press reports that said some industry participants were pushing back against OpenPath. He didn't deny this, he just also said it wasn't surprising. The entire point of this product is to clean up the supply chain and remove leeches from it that are taking more than they're giving. Those leeches are obviously going to be upset if a product like this becomes popular, because it threatens their ability to unfairly extract dollars from the overall ecosystem.

More:

- Announced Databricks as a new UID2 partner.

- Added Intuit’s MediaLab product to its platform.

- NBC Universal offered programmatic inventory throughout the Winter Olympic Games through The Trade Desk’s platform.