a. Key Points

- Total watch hours continue to grow at a sluggish pace.

- Removing quarterly watch hour growth disclosures.

- Bought back $5B in stock this quarter, marking a new record.

- Revenue still continues to grow at a solid pace thanks mainly to pricing power and ads.

- The free cash flow miss was noisy. Annual free cash flow expectations were reiterated.

b. Demand

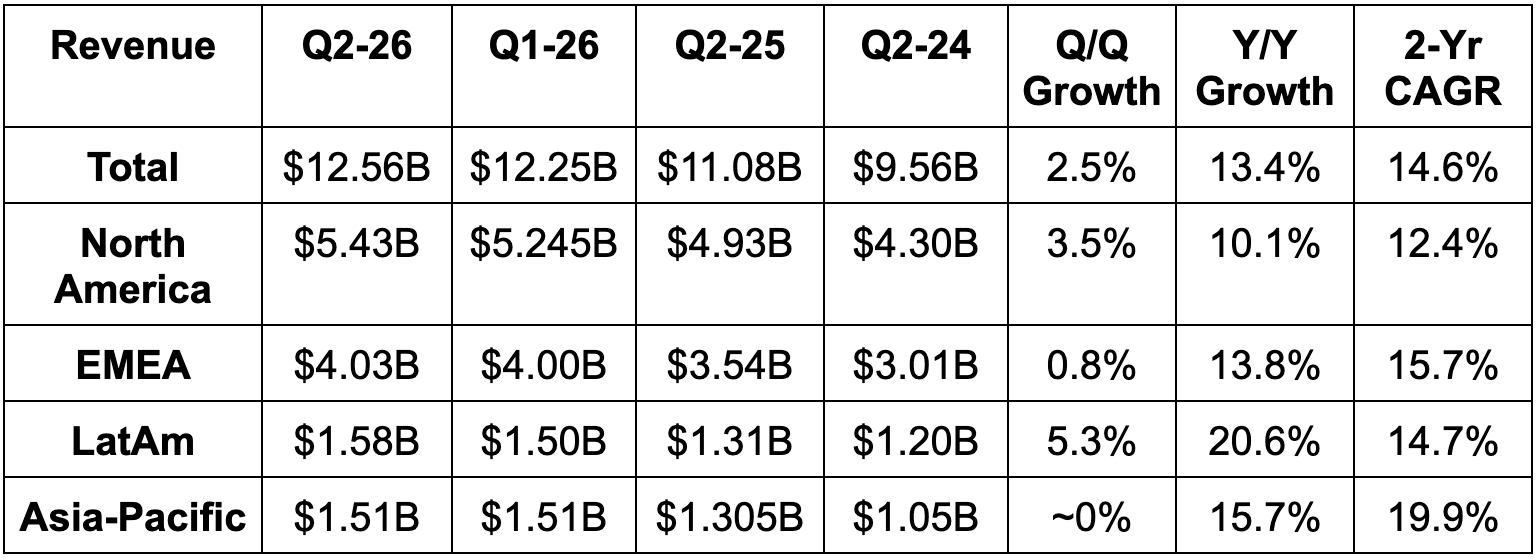

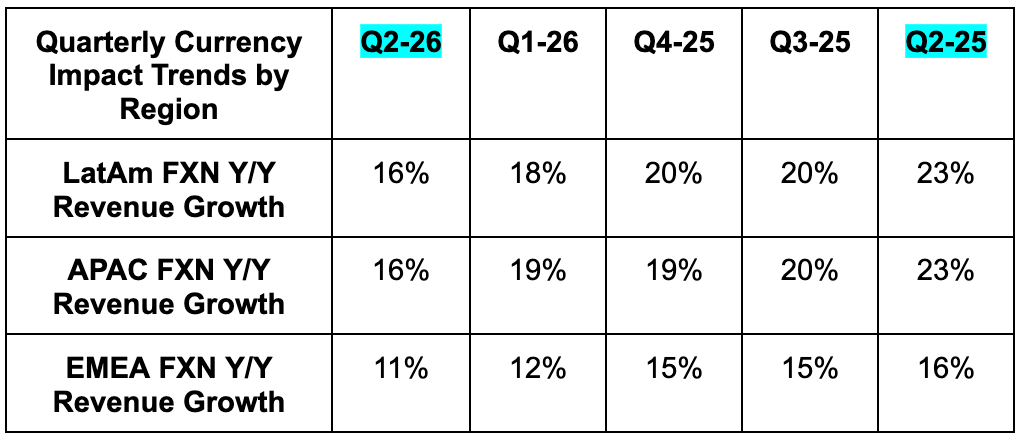

- Slightly missed total revenue estimates. 12% foreign exchange neutral revenue growth met estimates. The tiny miss was related to currency headwinds.

- Ad revenue from rising ad load, price hikes and some member growth drove the Y/Y revenue expansion.

- Missed U.S. + Canada (UCAN) revenue estimates by 1.5%.

- Slightly beat Europe, Middle East & Africa (EMEA) revenue estimates.

c. Profits & Margins

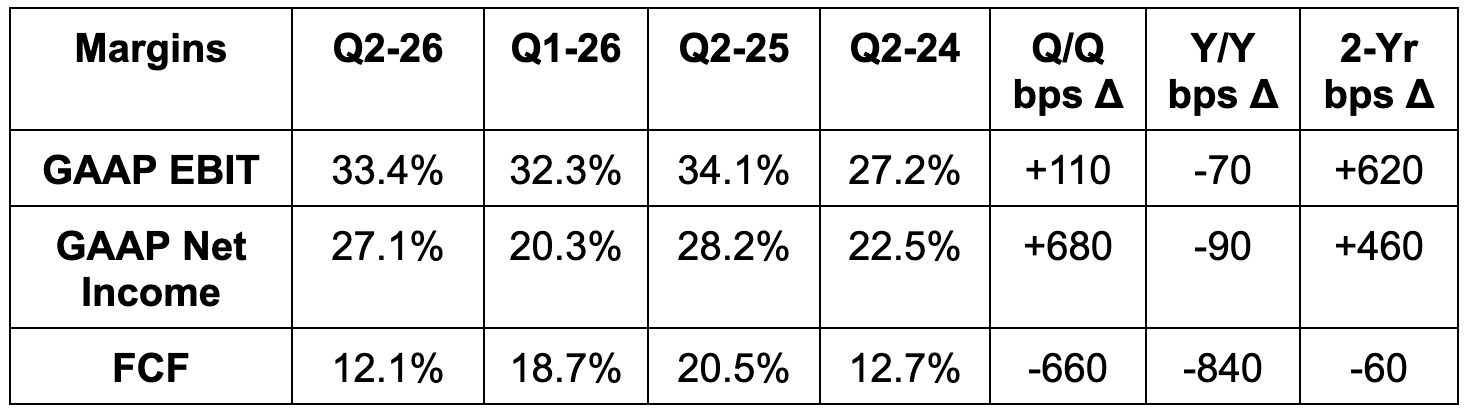

- Beat EBIT estimate by 1.5% & beat guide by 2.1%.

- EBIT margin fell Y/Y as expected due to content amortization timing for 2026. They expect slower cost growth for the rest of the year to enable Y/Y EBIT margin leverage. They also reiterated annual EBIT expectations.

- Beat EPS estimate by $0.02 & beat guide by $0.01. EPS rose by 11% Y/Y.

- Missed FCF estimate by 44%. This metric is very noisy on a quarterly basis due to content spend timing.

- FCF was also hurt by cash tax payment timing related to the Warner Bros. termination fee they collected.

d. Balance Sheet

- $9B cash & equivalents.

- $14.5B total debt.

- -2% Y/Y dilution. They bought back nearly $5B in stock this quarter, marking a record. They have $27B left in buyback capacity.