Today’s Piece is Powered by our Friends atLong Term Mindset:

1. PayPal (PYPL) -- Alex Chriss & Adyen

a. Alex Chriss

Section 1a is very similar to the thread I posted on Twitter this past week. If you read that, this may seem redundant and I’d skip to section 1b.

Context:

Dan Schulman will retire as PayPal CEO next month. This is a bit earlier than expected and finally wraps up a challenged tenure. The company has fallen slightly behind players like Shopify within branded checkout flow. It has made its fair share of poor M&A decisions. It was perhaps one of the biggest examples of over-hiring & fixed cost bloat via getting too excited during the pandemic. It struggled with messaging when it came to a needed shift from prioritizing account quantity to quality. It has been frustratingly slow with monetizing Venmo. It has also been frustratingly slow with expanding into higher margin Braintree & PayPal Commerce Platform products. Execution has been underwhelming… but the asset base remains compelling.

The assets:

The company still leads branded checkout share & adoption by a large margin. That adoption lead actually grew vs. Apple Y/Y in 2022. Apple is by far the closest 2nd for adoption.

Speaking of Apple (& Google)… PayPal is now deepening its partnership with that giant just like it did a decade ago with card networks to fend off the previous competitive threat. Card networks were supposed to make PayPal a "dinosaur" & instead made them a key partner. The same is playing out with tech giants. When you represent 400 million accounts and nearly 100 million monthly active users who fiercely trust your brand, you are inherently an attractive partner. Even for Apple.

PayPal still features large merchant checkout boosts for conversion, authorization, basket size & chargeback rates. The conversion edge vs. the sector recently grew from 6% to 8%. That edge is massive when considering what an extra 8 sales per 100 shoppers means to a merchant.

Venmo is a verb & a product that my generation lives on. FedNow is clunky & lacks comparable consumer protection programs. But even if it takes P2P share, P2P contributes 0 to PayPal's profits. Its just a top of funnel source of new users that it will have to maintain or replace. Venmo checkout is just now ramping with Amazon, Starbucks, CVS, LiveNation etc.

Braintree continues to kill it. It’s now as large as Stripe & Adyen in terms of comparable volume. From a margin perspective, it’s well behind those two. Why? Because its entire book of business is gigantic brands like Uber & Airbnb. The more volume a client contributes, the better deal they can command. Braintree's book is made up of these kinds of sweetheart deals.

To round out the product suite highlights, Hyperwallet gives merchants unmatched breadth for payment methods. Zettle & cards are getting PayPal's foot in the door to brick & mortar growth. Honey (now PayPal Gold) continues to see rapid growth in adoption of its loyalty program.

When putting this all together, branded checkout share is stable while Braintree’s continues to sharply rise. Some don’t believe PayPal when they say that, but its branded growth is in line to slightly ahead of all of the closest sector benchmarks with unbranded well ahead of its own benchmarks.

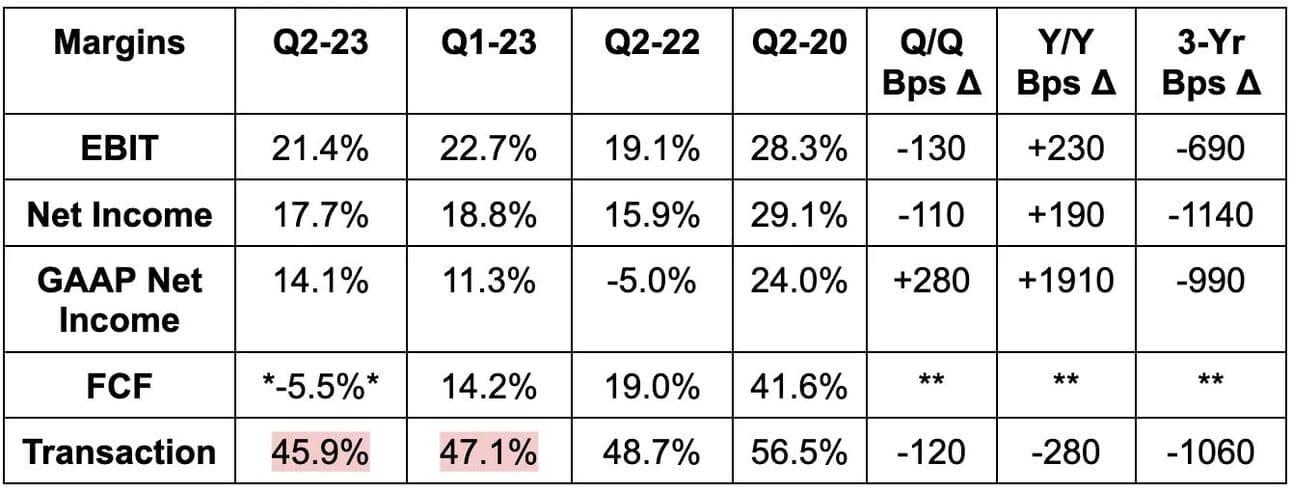

Braintree’s rapid growth is heavily weighing on the firm’s transaction margin. That margin pressure easing is top priority for Chriss. Second priority is effectively extracting value out of its quality assets. The two priorities are tightly connected.

Why I think Chriss is a good hire:

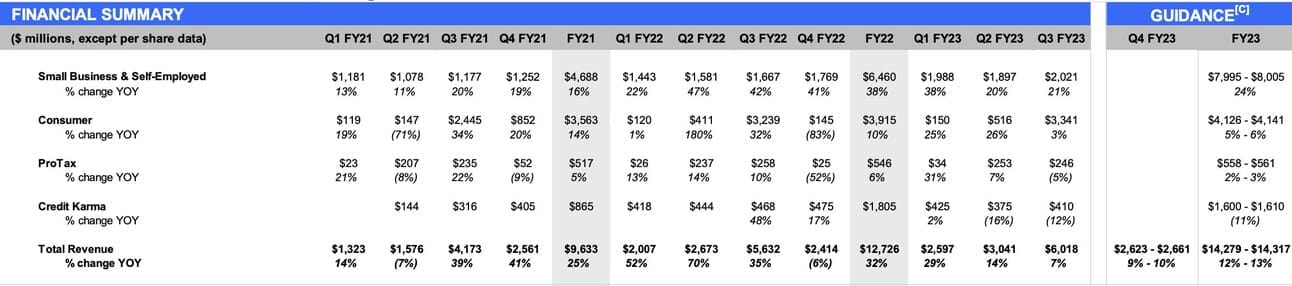

Chriss’s background is in running the small business & self-employed segment at Intuit. He spent 19 years there in roles like Chief Product Officer and also worked for Microsoft in the past. While he wasn’t the CEO of Intuit, he did lead a segment representing a third of the $140 billion enterprise’s revenue. It was over half of revenues until the Credit Karma purchase. As you see below, this is also Intuit’s most promising organic growth bucket.

Schulman met with nearly 2 dozen key investors including Elliott (which recently exited its PayPal stake) before making this decision. PayPal interviewed several FinTech & consumer bellwether CEOs, but thought his resume was the most compelling. And if you think about it, that makes sense. Why? Because Braintree has 3 margin levers to pull & Chriss is the man to pull them.

First is expansion into small and medium businesses (SMBs). Selling value-add software to small businesses is Chriss’s bread & butter. It is what he did with Intuit for products like QuickBooks and more. PayPal's marketing & loyalty programs are another key up-sell channel with Chriss having experience there as well in Mailchimp (more later). His software-centric, SMB-focused experience is ideal to say the least. The second margin lever is international expansion. Well? Chriss led a segment full of financial service products offered in 170 countries. He inherently has a deep understanding of the sensitive, fragile & complex relationships that global financial services firms must maintain with regulators. He has been threading that needle for years & years.

The third margin lever is up-selling value add software like Hyperwallet. Again… that is exactly what Chriss did with Intuit. He should have a keen sense of go-to-market strategies for these attractive products. Taking the PayPal job indicates that he sees these products as truly attractive.

Mailchimp:

The one black eye on Chriss’s resume is Intuit overpaying for Mailchimp. It has since written down the $14 billion acquisition by $3.4 billion. Like PayPal tried (and thankfully failed) to buy Pinterest, Intuit and many others sought ill-advised acquisitions while money was free, valuations were egregious, and growth at any cost was rewarded. While he wasn’t the CEO or CFO picking the price tag or offering the final stamp of approval to send the proposal to the board... he led the transaction. As counterintuitive as this may sound, I view this black eye as a positive.

Chriss should have a deep understanding of how difficult transformative M&A is to seamlessly integrate & execute. He should directly understand how C-suites are vulnerable to becoming too excited with presumed synergies. He should have a VERY high bar to clear for future M&A.

I don’t see PayPal as needing to plug an asset gap with another purchase. I see them as needing to execute within their existing asset base a lot better. Chriss has already learned a difficult lesson in Mailchimp. That should make him less prone to try and buy a Pinterest… for example.

Where we go from here:

This is not an “all clear.” Chriss can’t come in and wave a magic wand to make this a fintech darling overnight once more. It will take time for his strategy to be implemented and it will take time for that to show up in results within the massive book of business.

This is a step in the right direction… but a transaction margin trough is the step I want to see to resume adding to my stake. Chriss’s resume should have PayPal investors feeling cautiously optimistic that he can deliver. We’ll see how he does, but I’ll be giving him a full year to show real signs of turning the tide.

b. Adyen

Adyen, Stripe and Braintree round out the 3 highest profile white label processors around the globe. Adyen reported challenged first half results this past week that significantly missed on the top and bottom line while sending the shares falling nearly 40% in a single session. It missed revenue estimates by 4.4%, EBITDA by 12%, EBIT by 14.4% and $9.45 EPS estimates by $0.38. While this wasn’t a good quarter on the surface, this absolutely is a wonderful company with years upon years of lofty revenue compounding at gaudy margins. So then what happened?

A few things. First was aggressive hiring. Adyen leadership in 2021 did not participate in Fintech’s and Software’s hiring binge. It held back on adding headcount due to fierce competition for talent and so elevated comp demands. That fierce competition has since subsided and so Adyen, with its pristine balance sheet, has accelerated its pace of hiring. That’s why profit margins were below consensus across the board as the team told us “it could have optimized” for profitability but chose to invest in the long term.

The demand disappointment stemmed from its sales team not yet being large or trained enough due to this same pandemic-related talent competition issue. Interestingly however, the disappointment was also via increased pricing competition in North America. There are no rumors and no news anywhere about Stripe cutting rates… so this is referring to PayPal’s Braintree. This is yet another sign of how strong the momentum is for this now large part of PayPal’s total operations.

As I’ve discussed at length, the main PayPal risk today is where the transaction margin bottom is. When and where will we see an inflection? The margin compression is almost entirely related to Braintree’s rapid growth. While “pricing competition” doesn’t inspire confidence in Braintree’s margin potential, a successful expansion into smaller clients, more geographies and more software up-sells like Chargehound will. It’s inning one of these three endeavors.

Furthermore, Braintree can likely afford this added pricing competition. Why? Because when PayPal lands a large Braintree client, it generally is able to win better branded placements for both Venmo and branded PayPal checkout. Branded is high margin. Finally, in what was an abnormally weak quarter for Adyen, it still posted a robust 43% EBITDA margin. If Braintree even approached HALF of that margin as these new revenue streams kick in, that would work wonders for revenue and in reversing the erroneous narrative that white label processing can’t be high margin business. Adyen clearly proves that it can be. Based on using price as a competitive lever, Braintree likely won’t ever see the level of EBITDA margin Adyen saw in this report… and it doesn’t need to for the unit to morph into a profit driver at PayPal. That won’t happen this quarter… it likely won’t happen in Q4… it should absolutely start to play out in 2024.

2. Sea Limited (SE) -- Q2 2023 Earnings Review

a) Results vs. Expectations

- Missed revenue estimates by 4.6%.

- Beat EBITDA estimates by 3.2%; beat GAAP EBIT estimates by 8.8%.

- Beat $0.46 GAAP EPS estimates by $0.08.

b) Balance Sheet

- $5.7B in cash & equivalents. We exclude long term investments from this metric which SE includes.

- $3.3B in convertible notes.

c) Call & Release Highlights

Macro:

Sea Limited sees its Asia Pacific markets as showing strong resilience and weathering the current global economic uncertainty.

Continued Pivot:

Starting a few quarters ago, Sea Limited pivoted from an aggressive growth approach to one that prioritized profitability more strongly. The global money printer turned off and it adjusted accordingly. It thinks it has now demonstrated “self-sufficiency” and proven the profitability of the model. Now, it’s ready to re-accelerate investments in growth and warned investors that this intentional move may weigh on margins in some quarters.

- Sales & marketing fell 49% Y/Y.

- General & administrative fell 19% Y/Y.

- Provision for credit losses rose 37% Y/Y.

- Research and development fell 24% Y/Y.

E-Commerce:

Core marketplace revenue rose by a robust 37.6% while orders jumped by over 10% sequentially. Its EBITDA margin here also sharply inflected positively from -38% to 4.8% Y/Y as it became the only large and profitable e-commerce marketplace in that region. New buyer tools like order scheduling and tracking led to a 10% Y/Y rise in net promoter score while it continues to cut costs by adding pick-up points throughout its markets.

Interestingly, its live streaming service is creating some great cross-platform growth for Shopee. Its July streaming campaign drove 12x transaction volume vs. a normal day while its August campaign was met with similar success. It’s the number 1 live streaming platform in Indonesia per Populix.

Digital Entertainment:

- Free Fire (one of its popular games) saw sequential bookings growth for the first time in nearly 2 years.

- Quarterly paying users rose 14.6% sequentially to continue an encouraging reversal of Q/Q declines.

- EBITDA margin was 45.2% vs. 42.6% Y/Y.

Financial Services:

Revenue here continues to rapidly grow at a 53% Y/Y clip. The segment also turned convincingly profitable Y/Y with a 32% EBITDA margin vs -40% Y/Y.

The most important thing for this segment is credit quality… and credit quality is stable. 90+ day non-performing loan rate is flat at 2% of gross profit. It spent the last quarter sharpening its underwriting and deepening its access to 3rd party funding sources. It made good progress in both areas per the team.

Long-Term Mindset is a FREE weekly newsletter emailed each Wednesday. Each issue contains five pieces of timeless content to encourage you to think long-term. All issues can be read in less than 1 minute. There’s a reason why we are consistent readers and think you should be too. Subscribe here.

3. Bill.com (BILL) -- Earnings Review

Bill.com sells back-office financial service software mainly to small and medium businesses (SMBs). With the majority of SMBs still using manual payment & financial reconciliation tools, digitization within this niche is a key structural Bill.com tailwind.

a) Results vs. Expectations

- Beat revenue estimates by 4.7% & beat guidance by 6.3%.

- Beat $0.41 EPS estimates by $0.18 & beat guidance by $0.19.

- Beat EBIT estimates by 60%.