Earnings reviews from this week:

Earnings reviews from this season:

- Nu & Airbnb earnings reviews

- Cava & On Running earnings reviews

- Datadog & Sea Limited Earnings Reviews (sections 1 & 2)

- Palo Alto & Spotify Earnings Reviews (sections 1 & 2)

- AMD Earnings Review (section 4)

- Trade Desk, Duolingo & DraftKings earnings reviews

- Uber & Shopify earnings reviews

- Lemonade, Hims & Coupang Earnings Reviews

- Mercado Libre & Palantir Earnings Reviews

- Amazon & Microsoft Earnings Reviews

- Meta & Robinhood Earnings Reviews

- SoFi & PayPal Earnings Reviews

- Alphabet & Tesla Earnings Reviews

- Chipotle Earnings Review.

- ServiceNow Earnings Review

- Netflix & Taiwan Semi Earnings Reviews

- Starbucks & Apple Earnings Reviews

& my current portfolio/performance.

Table of Contents:

- Okta, Marvel & Affirm – Brief Earnings Snapshots

- Snowflake – Detailed Earnings Review

- DraftKings – Credit Cards

- Duolingo – Noisy Week

- Headlines

- Macro

1. Okta, Marvel and Affirm – Brief Earnings Snapshots

a. Okta

Demand:

- Beat revenue estimates by 2.2% & beat guidance by 2.4%.

- Beat current RPO (cRPO) estimates by 7% & beat guidance by 12%.

- Beat subscription revenue estimates by 1.8%.

Profits:

- Beat FCF estimates by 20%.

- Beat $0.85 EPS estimate by $0.06 & beat guidance by $0.075.

Balance Sheet:

- $2.9B in cash & equivalents.

- $859M in convertible senior notes.

- 3.8% Y/Y share dilution.

Guidance & Valuation:

- Raised annual revenue guidance by 0.9%, which beat estimates by 0.7%.

- Raised annual EBIT guidance by 2.8%, which beat estimates by 2.7%.

- Raised annual EPS guidance by $0.10, which beat estimates by $0.085.

- Raised 27% FCF margin guidance to 28%, which beat 27% margin estimates.

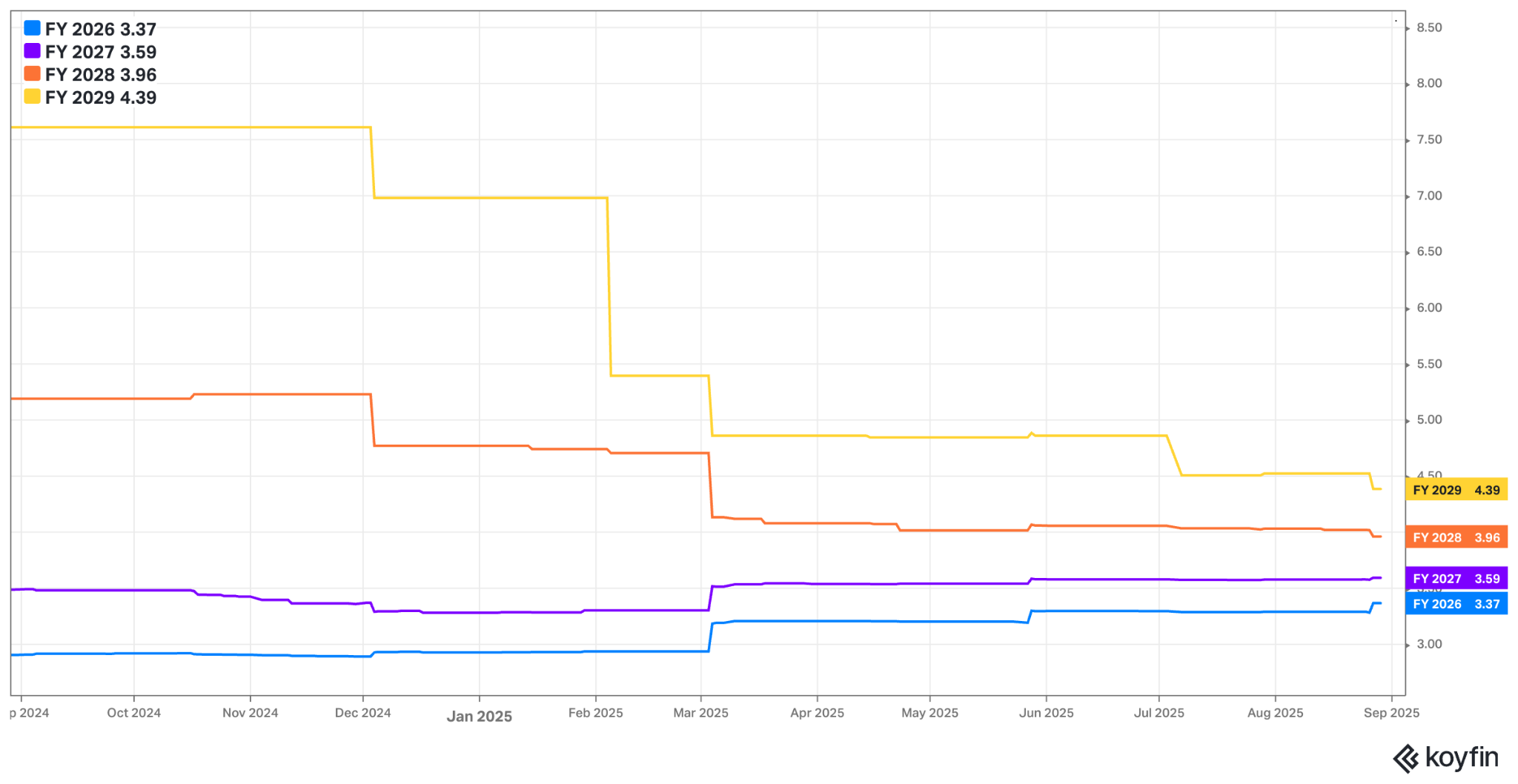

Okta trades for 28x forward EPS. EPS is expected to grow by 19.8% this year and by 6.7% next year.

b. Marvel (MRVL)

Demand:

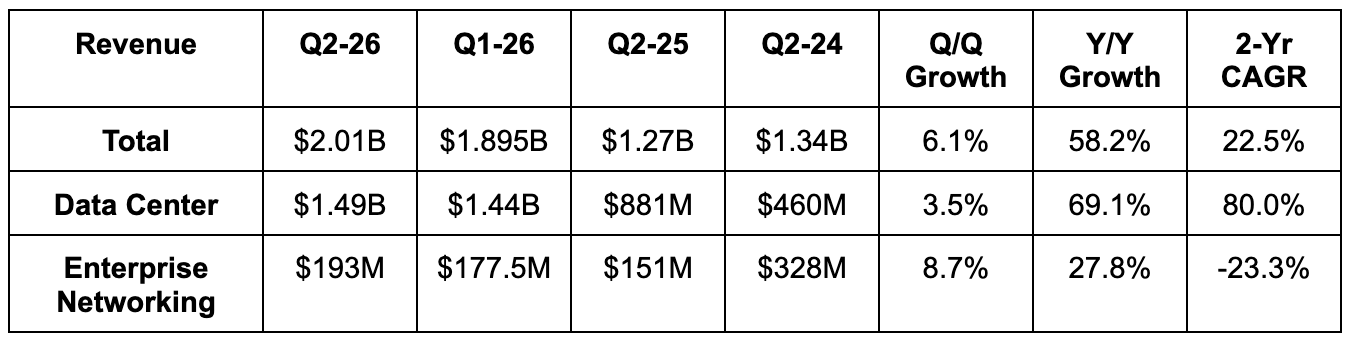

- Slightly missed revenue estimate & slightly beat guidance.

- Missed data center revenue estimate by 1.7%.

- Beat enterprise networking revenue estimate by 5%.

Profits:

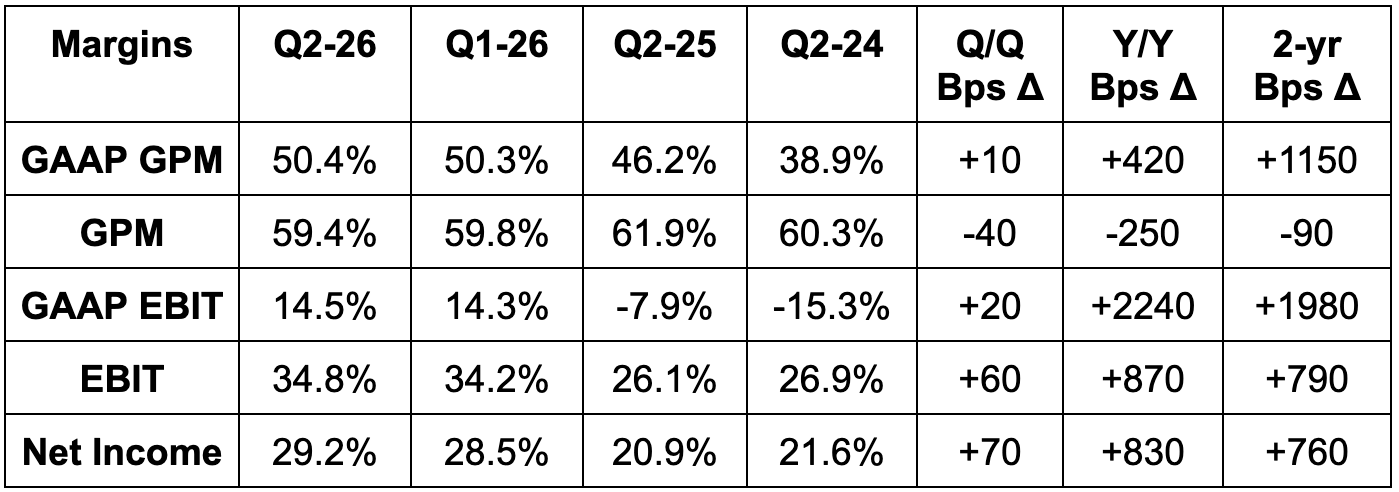

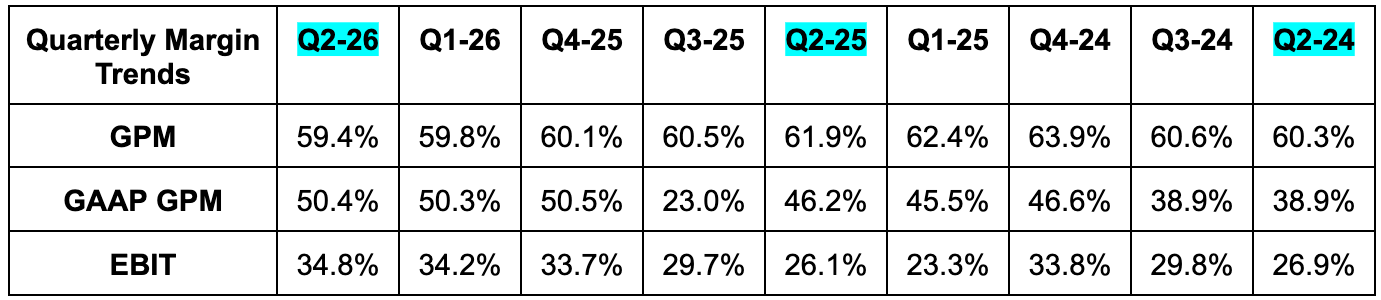

- Missed 50.5% GAAP GPM estimates by 10 bps.

- Missed 59.5% GPM estimates and identical guidance by 10 bps each.

- Slightly missed EBIT estimates by 0.3% & missed guidance by 1.2%.

- Missed GAAP EBIT estimates by 1.6%.

- Missed FCF estimates by 10%.

- Met $0.67 EPS estimates and identical guidance.

Balance Sheet:

- $1.24B in cash & equivalents.

- $1.05B in inventory +29% Y/Y.

- $4.45B in total debt

- Diluted share count slightly fell Y/Y.

Guidance & Valuation:

- Q3 revenue guidance missed estimates by 2.6%.

- Q3 GPM guidance beat 59.3% estimates by 50 bps.

- Q3 EBIT guidance beat estimates by 1.7%.

- Q3 EPS guidance beat $0.73 estimates by a penny.

MRVL trades for 21x forward EPS. EPS is expected to grow by 78% Y/Y this year and by 22% Y/Y next year.

c. Affirm

Demand:

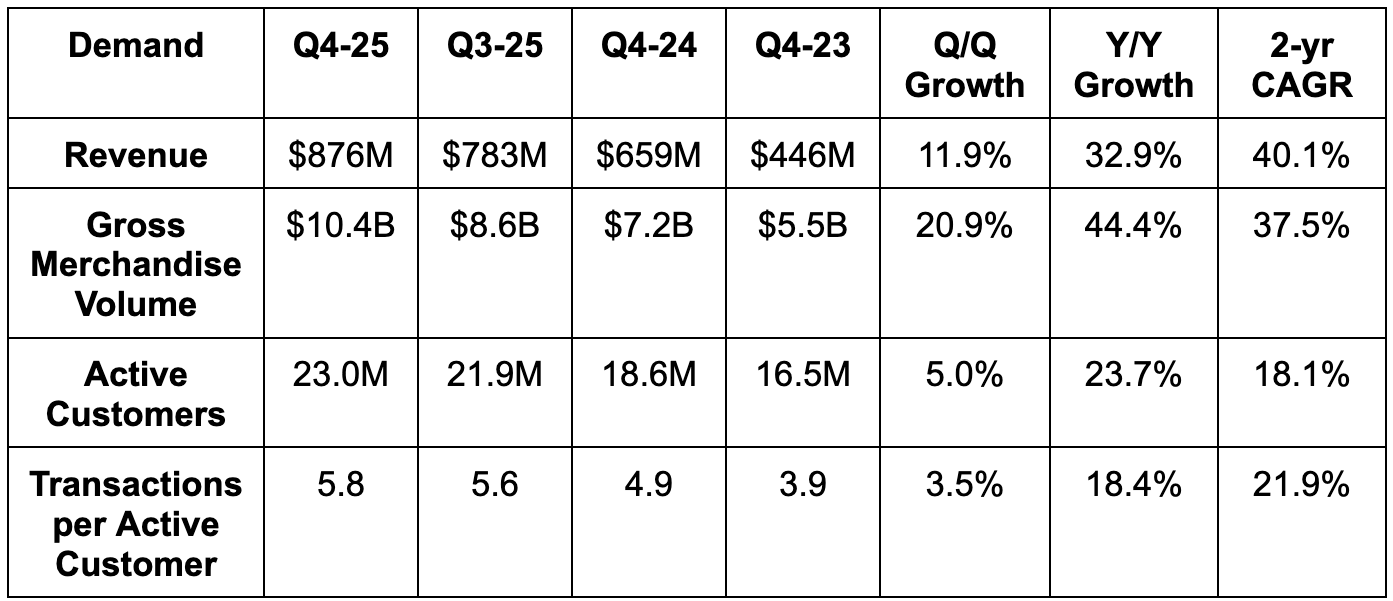

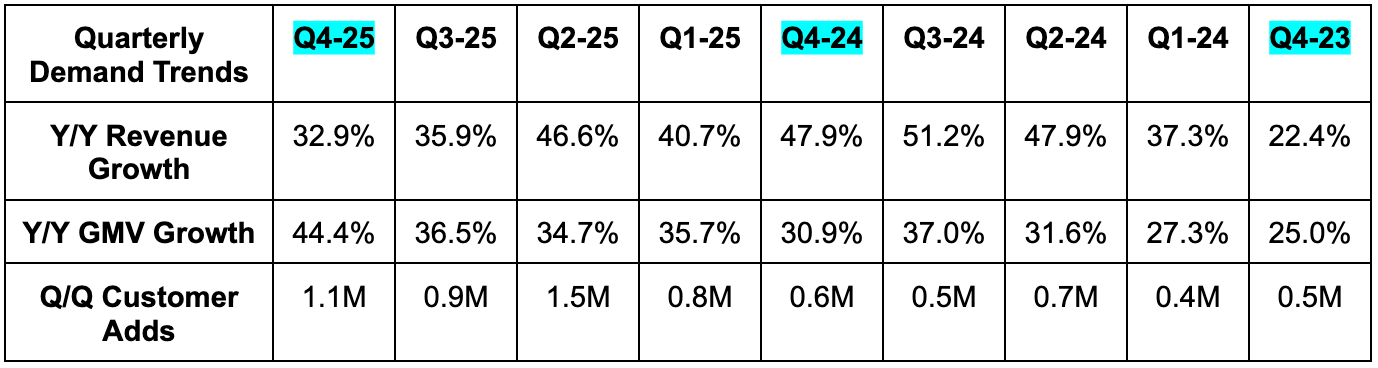

- Beat GMV estimates by 8% and beat guidance by 8.9%.

- Beat revenue estimates by 4.7% and beat guidance by 5.5%.

- Beat revenue - transaction cost guidance by 8.3%.

Profits:

- Beat $166M EBIT guidance by 43%.

- Beat $17M GAAP EBIT estimates and guidance by $41M.

- Beat $0.11 GAAP EPS estimates by $0.04.

Balance Sheet:

- $1.35B in cash & equivalents.

- $7B in loans held for investment.

- $1.6B in finding debt.

- 8.6% Y/Y diluted share count growth; 3.6% Y/Y basic share count growth.

Guidance & Valuation:

Affirm guided to at least $3.86B in revenue for next year. This led to estimates for the year rising by 2.8% to $3.99B. It also guided to 26%+ EBIT margin, which led to EBIT estimates for the year rising by about 20%. 6% GAAP EBIT margin guidance led to EPS estimates rising from $0.75 to $0.89 Y/Y.

Affirm trades for 35x forward EPS. EPS is expected to grow by 41% this year and by 37% next year.

2. Snowflake (SNOW) – Earnings Review

a. Snowflake 101

Data Cloud Foundation:

Snowflake’s overarching platform is called the (AI-fueled) Data Cloud – a “single foundation to eliminate data silos” – with a relational database makeup. Relational uses structured query language (SQL) and means data is stored in rows and columns to make insight gleaning straightforward. This differs from document-oriented database vendors like MongoDB, which use Not Only SQL (NoSQL) and stores data in (as the name indicates) flexible documents. Snowflake is considered best suited for online analytical processing (OLAP), while document-oriented is considered best for online transactional processing (OLTP). Both would subjectively argue that their approaches are best suited for handling unstructured data and for AI. And both are trying to encroach on the other’s territory.

Snowflake’s infrastructure unlocks affordable data storage, organization, querying and learning at gigantic scale. It offers these services with elastic compute capabilities, allowing for flexible scaling up and down of usage. The architecture naturally separates the functions of data storage and consumption, unlike legacy data warehouse solutions. That’s why it’s perfect for OLAP, as it means data consumption capacity is untethered from public computing resources. In turn, this helps control costs and waste, handle diverse workloads and resolve potential scale bottlenecks.

Under this framework, I can store as much data as I want to without the requirement of immediate processing. In Snowflake’s case, the storage is done in a centralized data repository in the Data Cloud and processed only as needed. Data is utilized virtually, which removes the need for dedicated customer hardware. Snowflake does all of this for clients in a managed fashion, minimizing talent and infrastructure needs. All of this routinely delivers 50% total cost of ownership (TCO) reductions for its customers.

Snowflake splits its products into 4 categories:

Analytics Category:

This includes the Snowflake Data Warehouse, which is where structured data is stored and (on command) processed. Structured data is formatted data. It’s utilized for record keeping and report creation. Data can be easily fetched via structured query language (SQL). The Data Lake does what the warehouse does for unstructured data. Unstructured data is unformatted and used to uncover new insights and patterns. This also includes its business intelligence product, which turns mountains of data into optimal suggestions.

Data Engineering Category:

Key products here include Snowpark. This is its developer platform and data-equipped playground to build new things. It enables working with data in any source code language. With it, they can process and visualize data (through Snowpark functions) and build apps (through Snowpark Native Apps). GenAI models are voracious data consumers. Snowpark Container Services allow GenAI models to run closer to the data that they require. This enhances performance, expedites model training and diminishes costs. Movement of apps, workloads and developer attention from Apache Spark to Snowflake is a key source of growth here.

Dynamic Tables is a newer data streaming tool. It automates pieces of structured data querying within the data warehouse. It offers auto-updates to reports as new data is added to its cloud.

Unistore is SNOW’s hybrid table product, which can ingest, store and organize both transactional and analytical workloads. Snowflake has long been an analytical workload specialist within the data warehouse part of the business, and this unlocks transactional workload demand.

Snowconvert is another product that helps with easier migrations, as it automates conversion and modernization of source code and data.

AI and Applications Category:

Cortex AI is another important new product. It’s what Snowflake calls its “AI layer” and offers a slew of GenAI-powered tools to (as Snowflake always says) bring AI, application-building and analytics “right to a customer’s data.” That conjoining routinely lowers data transfer and storage costs. Cortex AI offers unstructured text summary, sentiment analysis, helps beginners write SQL etc.

- Cortex Search: Brings to life Snowflake CEO Sridhar Ramaswamy’s vision of making complex data querying seamlessly conversational. With it, anyone who knows Sequel can practice advanced, multi-stage queries and work directly with cutting-edge large language models (LLMs) from its partners.

- Cortex Analytics: Uncovers patterns, insights and trends from massive, entirely unstructured datasets to sharpen things like trend forecasting. Both tools are enjoying strong early adoption.

- Cortex Agents: Provides powerful agents to “orchestrate seamless planning and execution of tasks” across all company data.

They see the overarching company theme of “bringing data to your work” as a key differentiator here, as agents are only as good as the data they’re trained on and Snowflake offers the destination to get whatever data a company needs.

Collaboration Category:

This is where the Snowflake app marketplace and its data connectors reside. Snowflake Data Sharing is its secure product for, as the name indicates, sharing data among the rest of Snowflake’s participating users. As more opt in, a compelling network effect of relevant data builds and the firm’s value proposition deepens. As Snowflake builds a larger customer base, inviting these customers to openly share information with each other creates a compelling edge vs. sub-scale players.

Model:

Snowflake’s revenue model is consumption-based in nature. Customers book and pay in advance, with billings and revenue recognition coming as credits are utilized. This means visibility compared to SaaS business models is not as strong. It also means customers can more easily scale down (or up) usage when times are bad (or good).

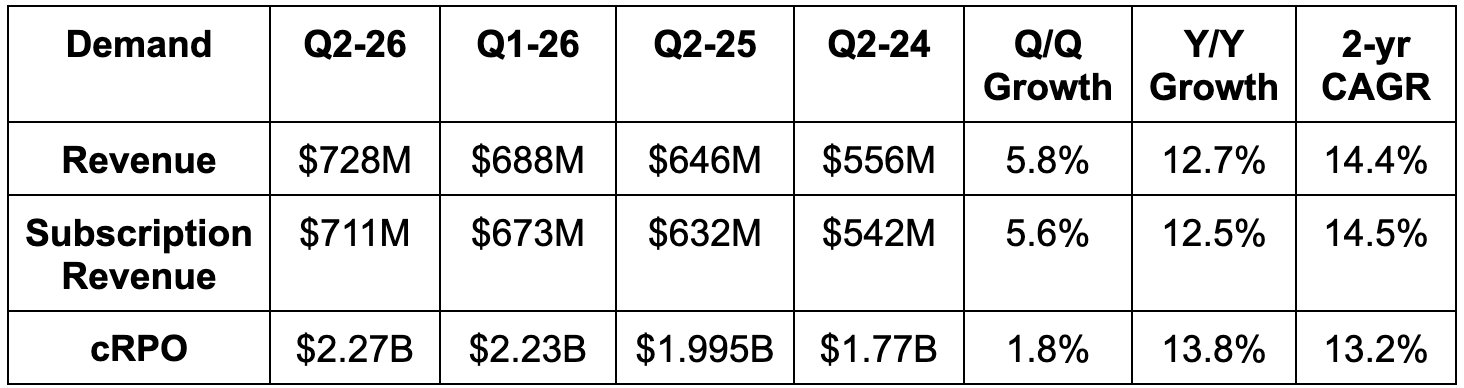

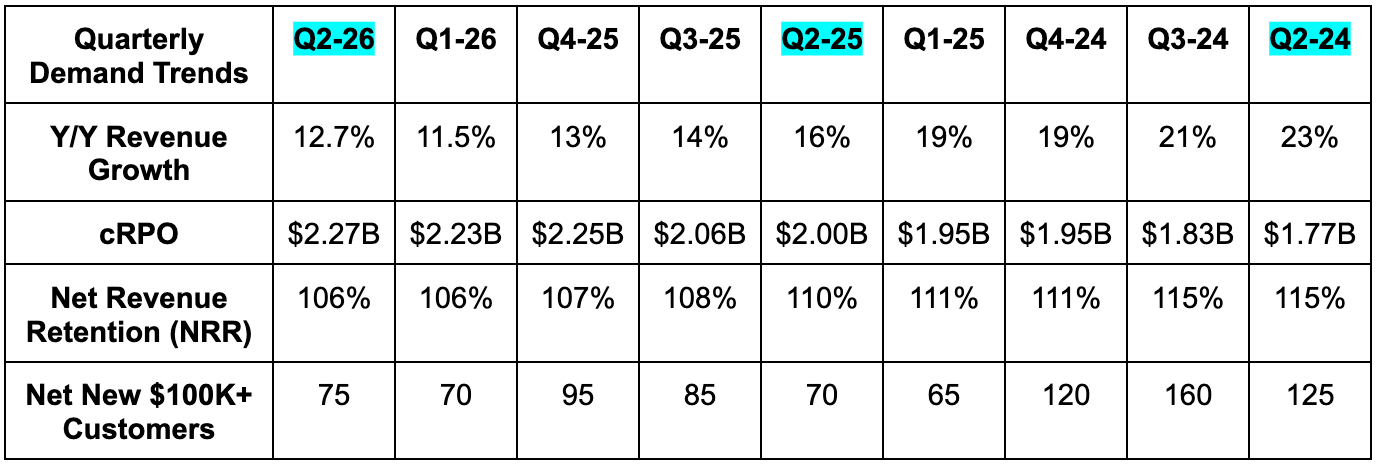

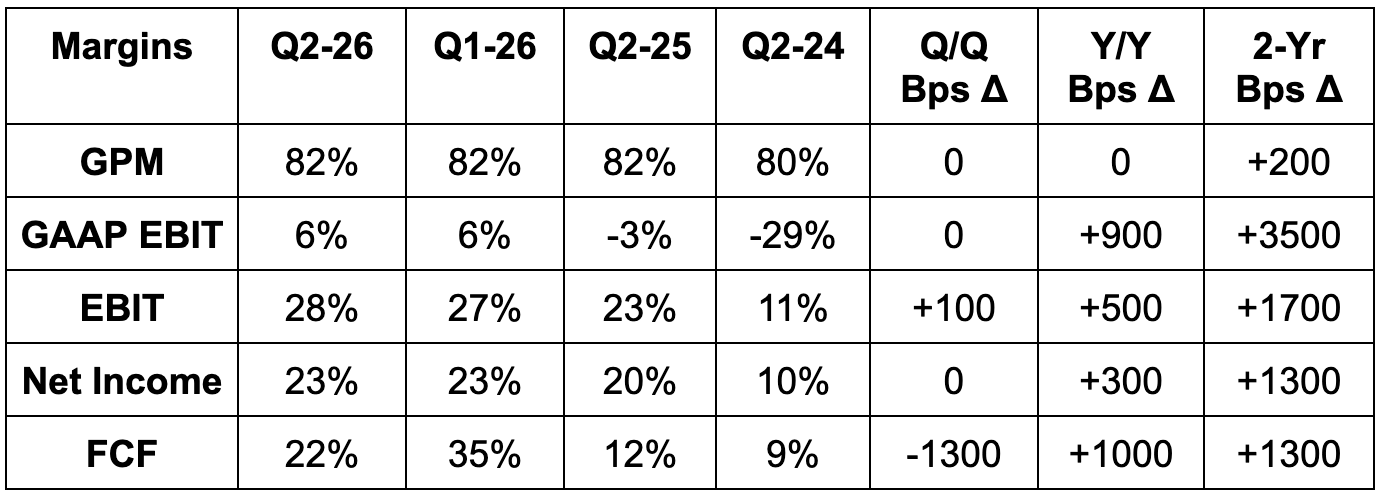

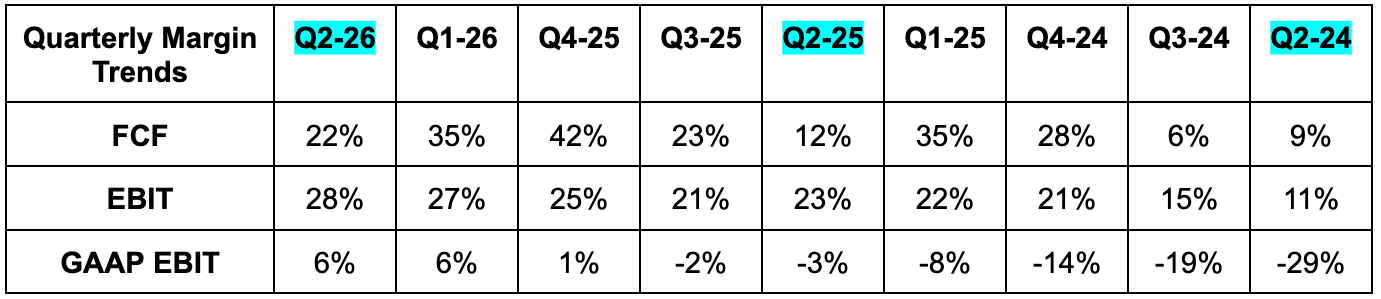

b. Key Points

Subscribe to read the rest of this article and so much more.