Hey guys. The Snowflake and Trade Desk reviews will come in the next couple of days. I caught a nasty bug on Thursday that really slowed me down. Apologies. They’re on the way.

I’d also love to survey 1-2 dozen of you to get your take on Stock Market Nerd product roadmap plans. Feel free to respond to this email if you’re game. Thanks in advance.

Reviews already sent this week include:

You can find 15 other earnings reviews from this season, my current portfolio/performance, an Axon deep dive and so much more here.

Next week, I will be sending the 2 catch-up reviews on Snowflake and Trade Desk alongside reviews on CrowdStrike, Broadcom, and a few more.

1. Earnings Snapshots – Duolingo, Salesforce & Rocket Labs

a. Duolingo

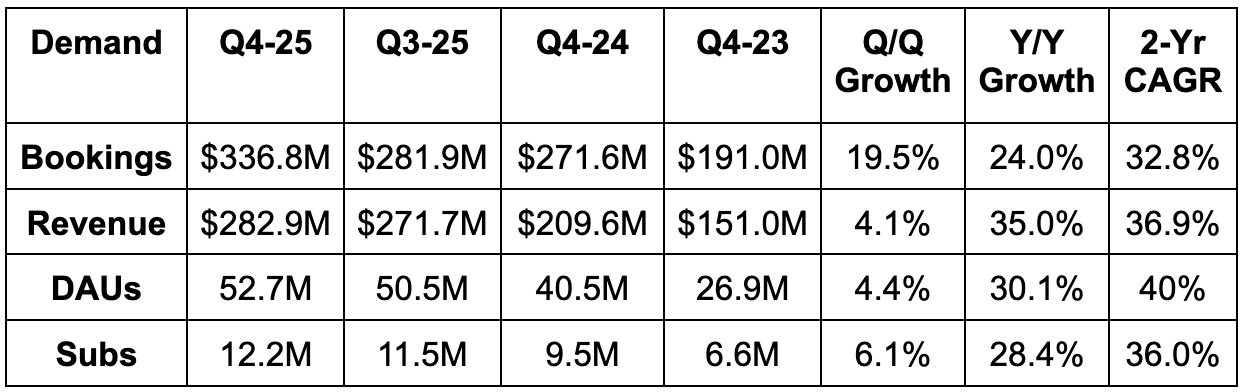

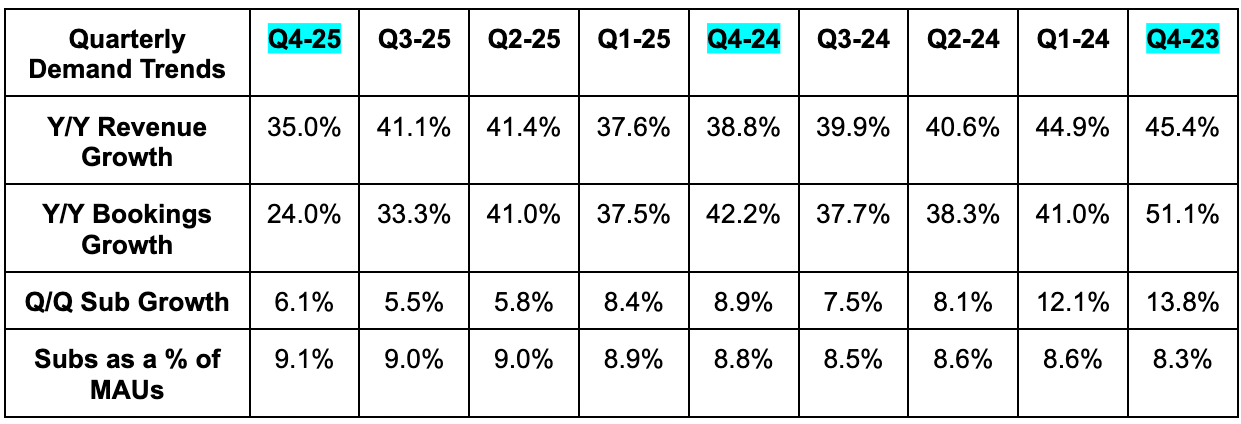

Demand:

- Beat bookings estimate by 0.9% & beat guide by 1.6%.

- Beat revenue estimate by 2.5% & beat guide by 2.9%.

- Daily active users & subs both slightly beat estimates.

- Monthly active users missed estimates by 3.6%.

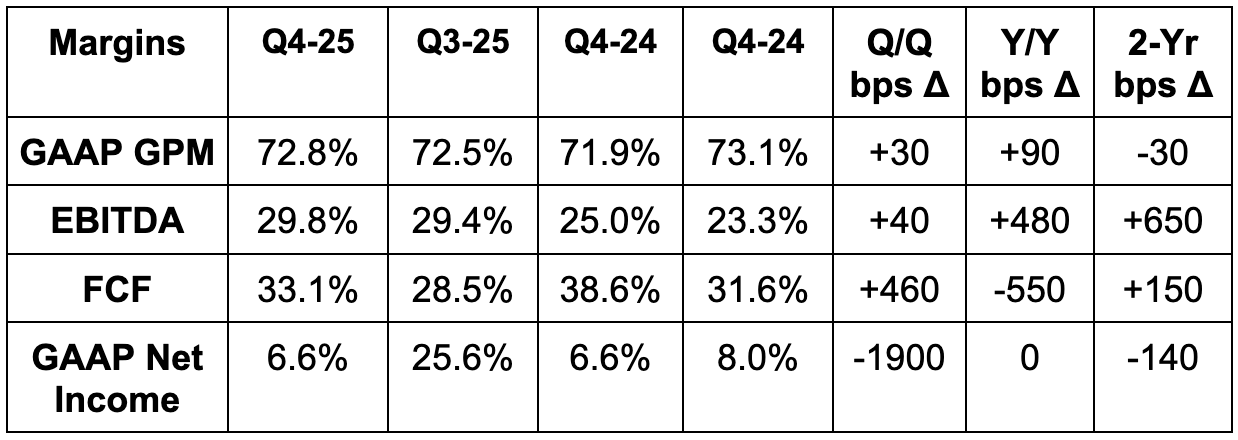

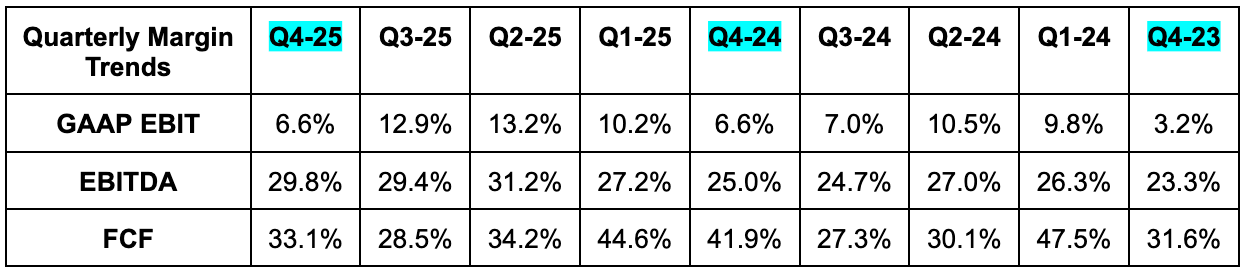

Profits & Margins:

- Beat EBITDA estimate by 8% & beat guide by 10%.

- Beat 72.1% GPM estimate by 70 basis points (bps; 1 basis point = 0.01%).

- Missed FCF estimate by 6%.

Balance Sheet:

- $8885M in cash & equivalents,

- No debt.

- 0.6% Y/Y dilution.

Guidance & Valuation:

- For Q1, bookings missed by 9%, revenue missed by 1%, and EBITDA missed by 13%.

- For 2026, bookings missed by 8%, revenue missed by 4.4% & EBITDA missed by 22%.

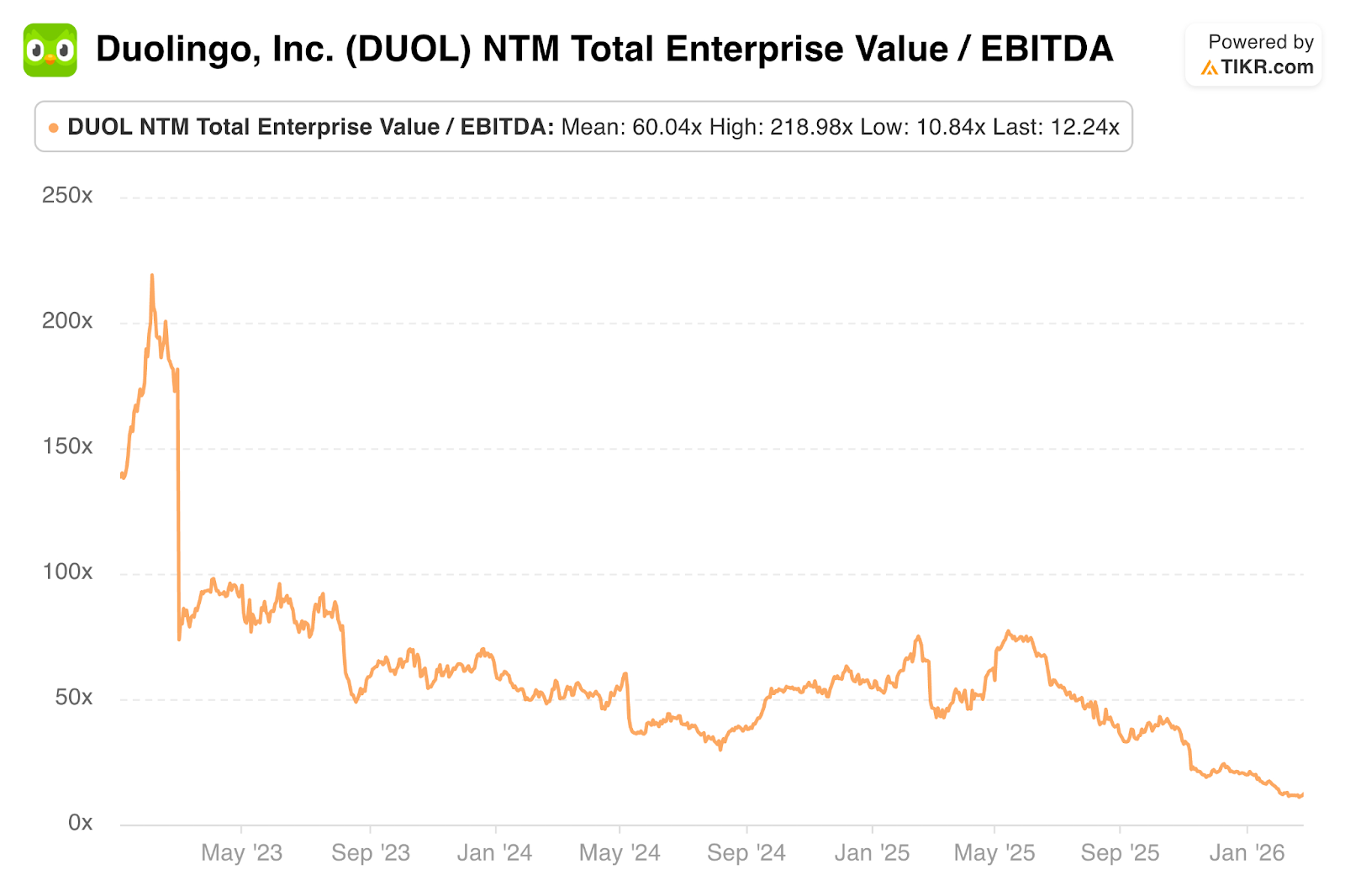

Estimates are going to keep falling over the coming days, so it’s best to use DUOL’s actual guidance right now to gauge forward multiples. Based on that guidance, it trades for 15x forward EBITDA with EBITDA expected to modestly fall Y/Y in 2026.

Quick Take:

As Max readers know, I exited this position last year around $200/share after trimming much higher several times. The social media data I was closely tracking continued to deteriorate, and that is the single most important part of their growth engine. That should make the poor bookings guide, which is their forward-looking demand metric, unsurprising. They have not been able to recover any semblance of social media momentum even as growth comps get much easier. The team can say they’re prioritizing engagement, teaching quality and user growth over monetization in the near term. All I’d say is that if they were doing so effectively, user metrics would look a lot better. I have no interest in re-entering at any price based on current fundamental trends.

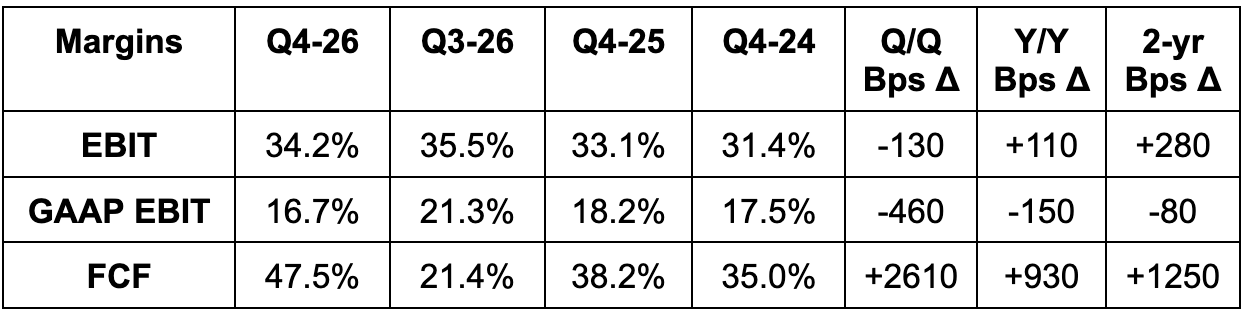

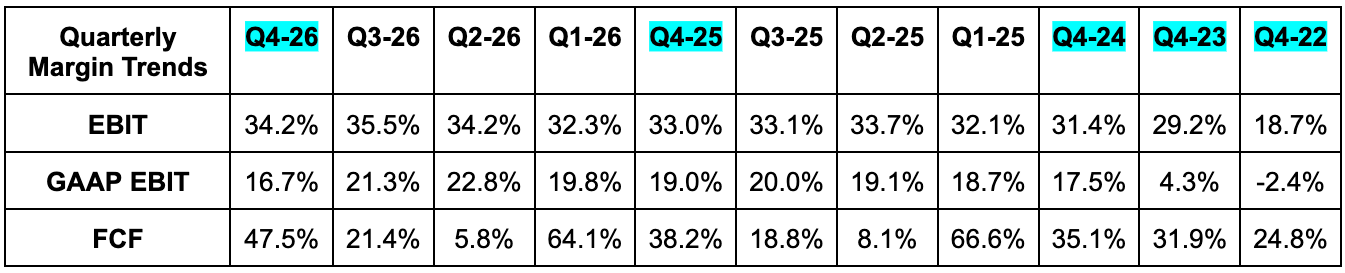

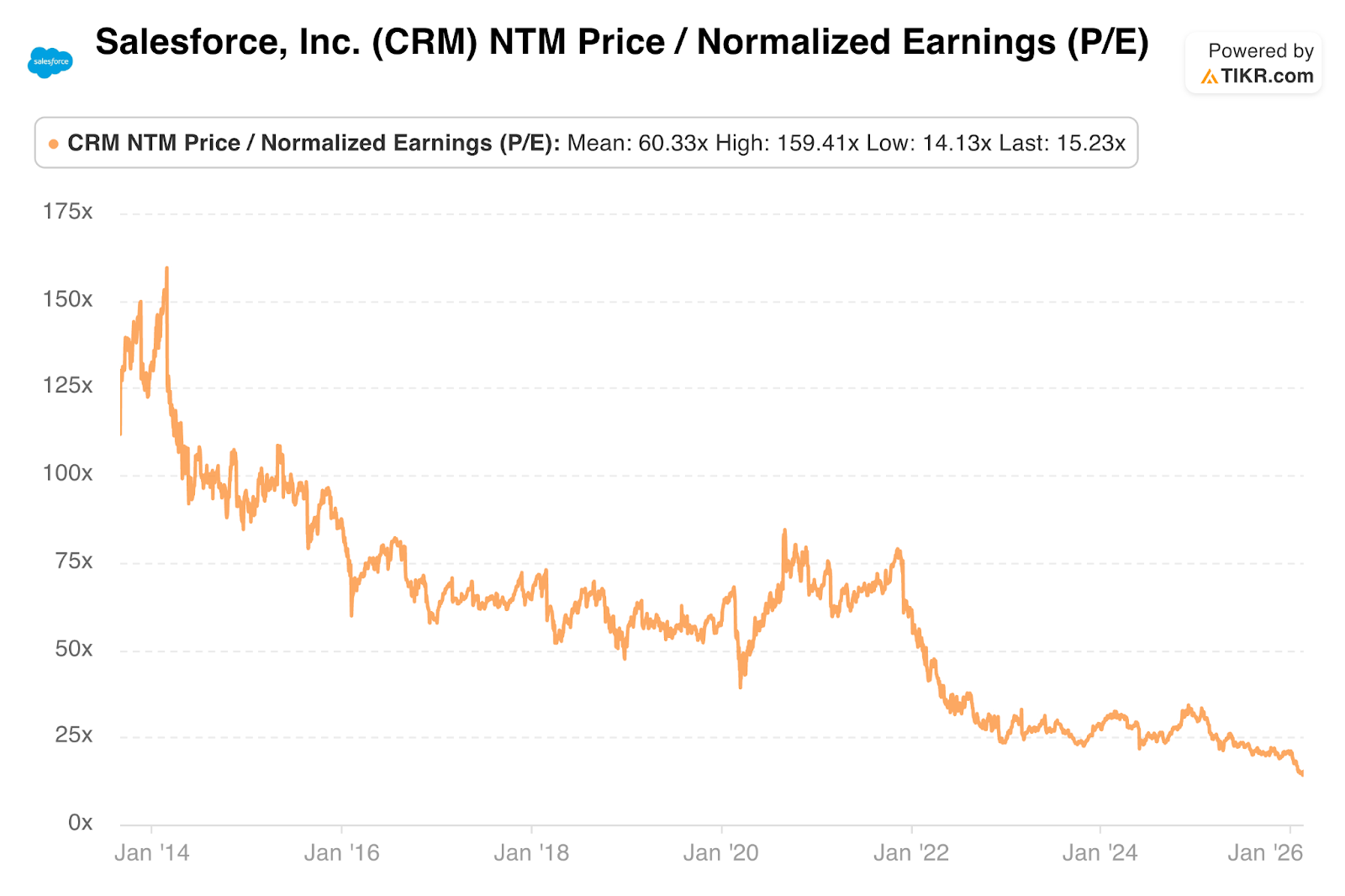

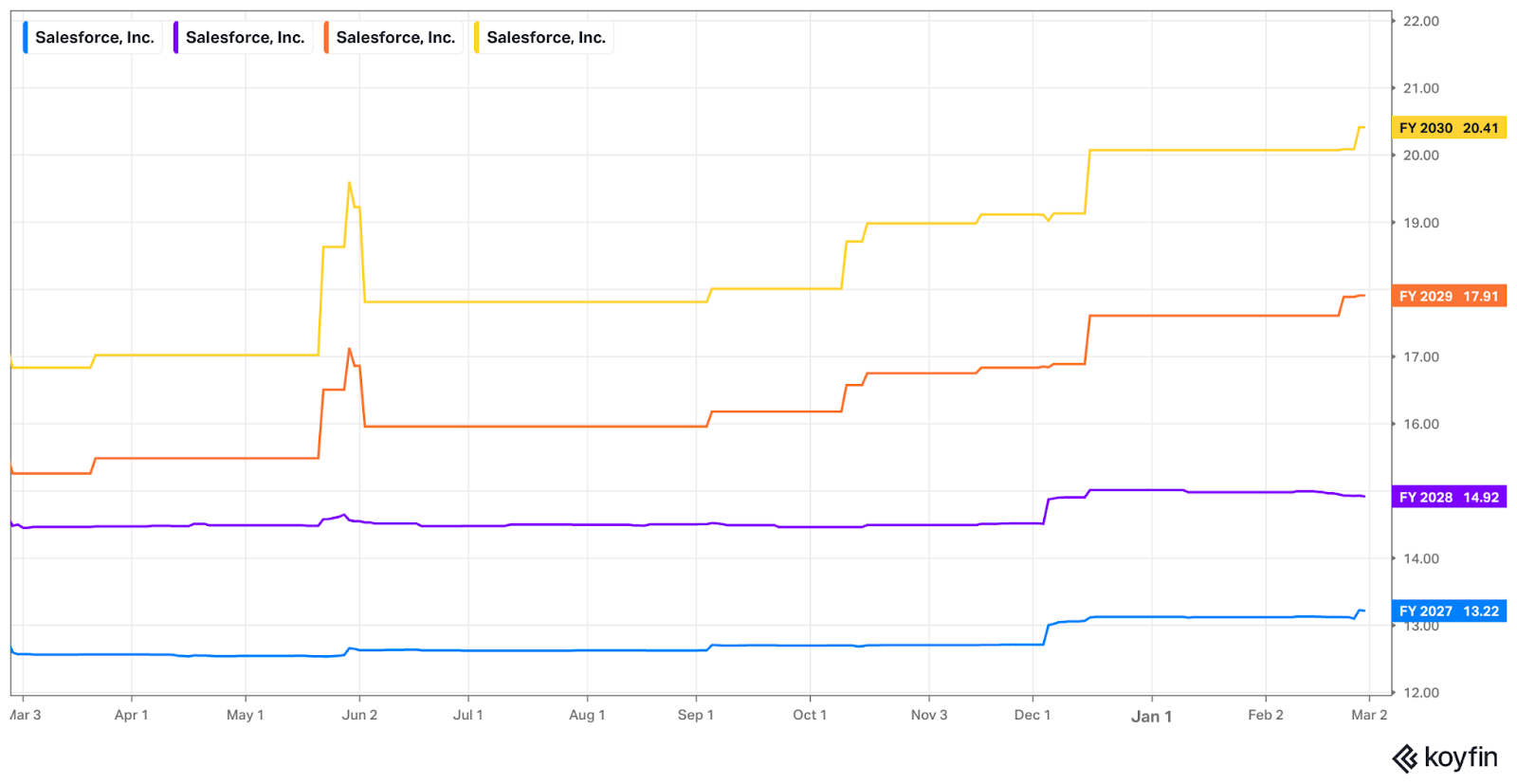

b. Salesforce (CRM)

Demand:

- Slightly beat revenue estimates & slightly beat guidance.

- Revenue grew by 8% Y/Y organically (ex-Informatica).

- Slightly beat subscription & support estimates & slightly beat guidance.

- Subscription & support revenue grew by 9% organically (ex-informatica).

- Beat current remaining performance obligation (cRPO) estimates by 2% (RPO was 1.5% ahead).

- Bet billings estimates by 6.6%.

Profits & Margins:

- Slightly beat EBIT estimates.

- Beat $3.05 EPS estimate by $0.76. This was helped by an $811M equity portfolio gain. Without this, EPS would have been a small miss.

Balance Sheet:

- $9.6B in cash & equivalents.

- $7.6B in strategic investments.

- $14.4B in total debt.

- Share count fell by 3.5% Y/Y.

Guidance & Valuation:

- For Q1, revenue guidance beat by 0.6%, EPS beat $3.02 estimates by $0.10

- For 2026, revenue guidance met, EBIT guidance missed by 1.7%, EPS guidance met and cash flow growth guidance met.

Revenue guidance for the full year represents 10.5% constant currency growth or 7.5% constant currency growth on an organic basis (ex-informatica). Subscription & support revenue growth guidance on an organic constant currency basis was set at 8%. It also expects organic growth to accelerate during the 2nd half of the year.

CRM trades for 15x forward EPS. EPS is expected to grow by 6% this year and by 13% next year.

Quick Take:

I think that the negative sentiment and sell off for this name are both overdone. At the same time, I think that's true for pretty much every software name outside of the point solution-oriented business models and user interface wrappers that truly are vulnerable to AI disruption. While I do not hate the idea of Salesforce as an investment at these prices, I simply prefer allocating my finite investment dollars to other software names with higher growth rates that I am more confident in going forward.

c. Rocket Labs (RKLB)

Demand:

Revenue beat estimates by 0.8% and beat guidance by 2.7%.

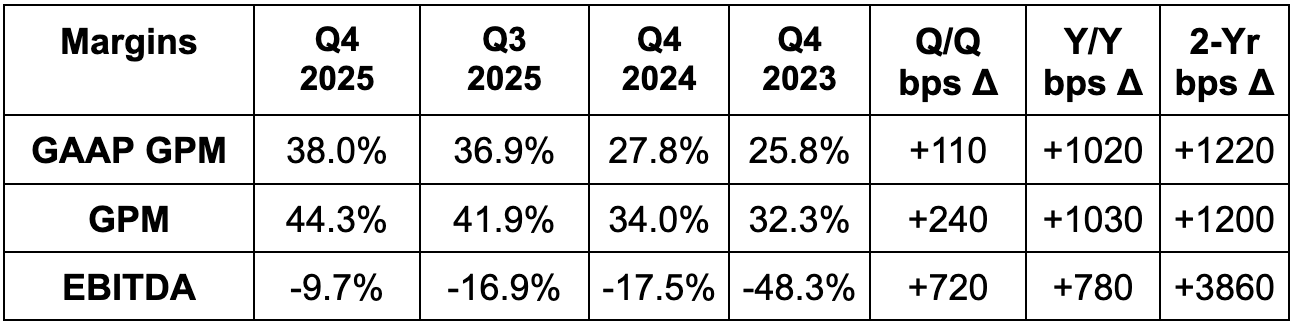

Profits & Margins:

- Met GAAP GPM estimates & guidance.

- Met GPM estimates & beat guidance by 30 bps.

- Missed EBITDA estimates by 1.3% & missed guidance by 0.8%.

- Beat -$58.5M GAAP EBIT guidance by $7.5M.

Balance Sheet:

- $1B in cash & equivalents.

- $158M in inventory vs. $119M Y/Y.

- $152M in convertible senior notes.

- 14% Y/Y diluted share count growth.

Guidance & Valuation:

- Q1 revenue guidance beat estimates by 4%.

- Q1 40% GPM guidance missed estimates by 280 bps.

- Q1 -$24.5M EBITDA guidance missed estimates by $9M.

- Q1 -$41M EBIT guidance missed estimates by $13M.

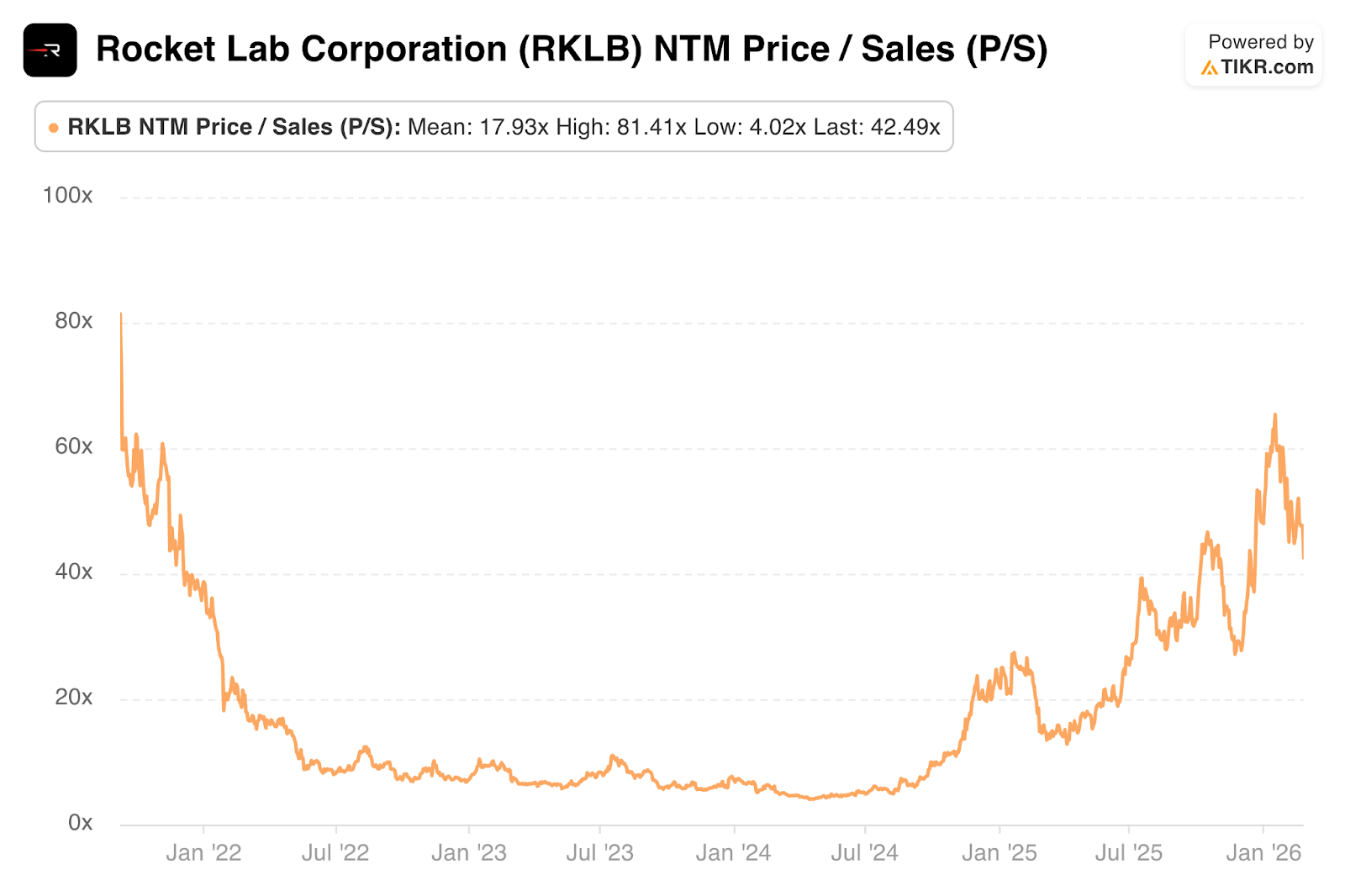

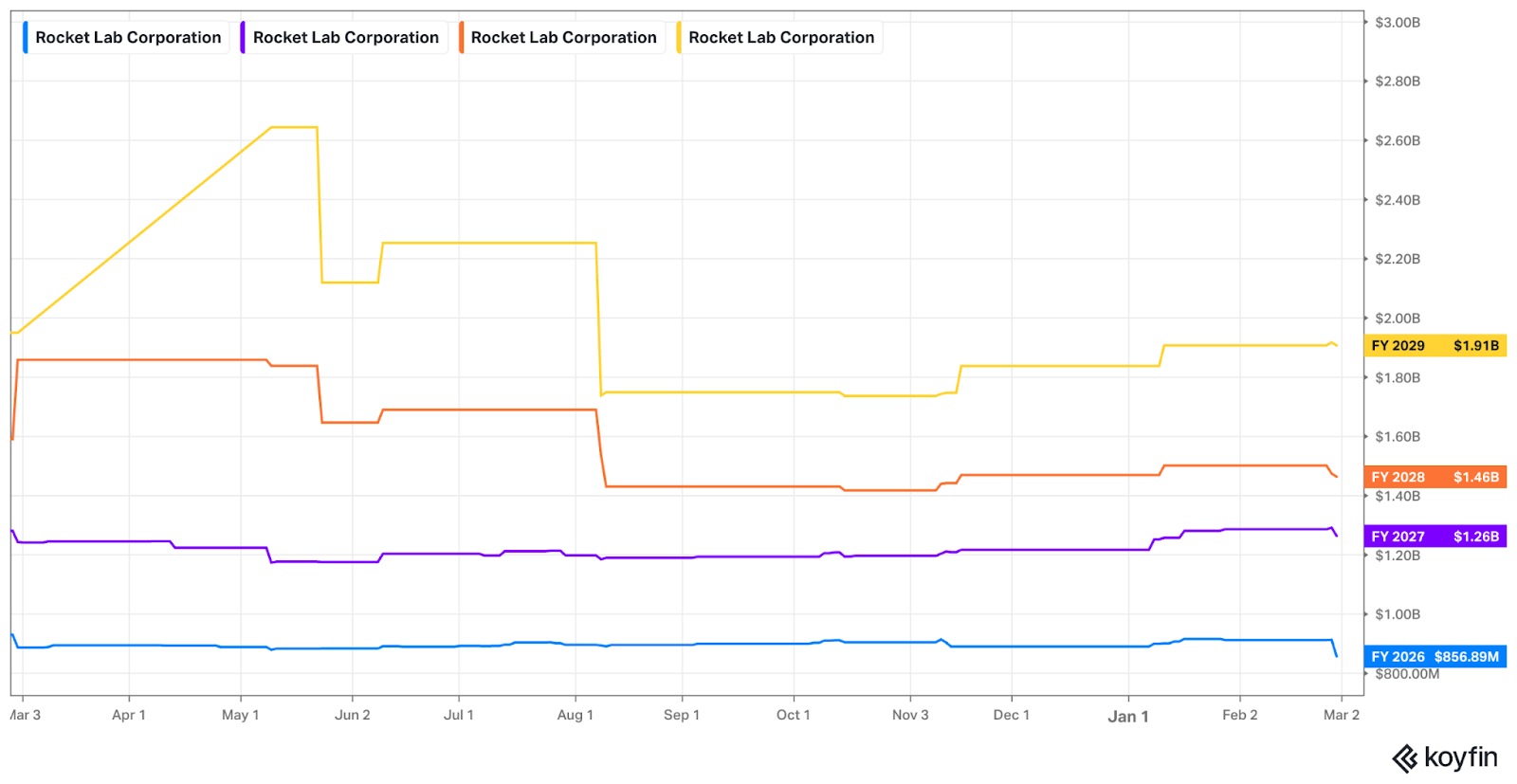

RKLB trades for 42x forward sales. They are expected to grow by 40% this year and by 46% next year. They’re also expected to turn EBITDA positive this year. They trade for 220x 2027 EBITDA.

Quick Take:

My take here isn’t valuable (yet). I don’t know much about this company at all, but Max readers have chosen it as the next deep dive topic. So stay tuned.

2. Uber (UBER) – AV Services

Uber announced a suite of autonomous services this week. The products within the announcement have all been teased and talked about before, but now Uber is officially bringing them to market. Services include data pipelines to share Uber’s unmatched scale with operators. This also includes a relationship with Lucid where Uber is running a fleet of empty autonomous cars solely to amplify its data collection and sharing capabilities. Other infrastructure solutions include planned fleet financing, regulatory compliance service and a hardware-agnostic tablet that allows customers to set temperature and music. Agnostic is important, as Uber is trying to be the de facto demand aggregator for all future vendors. Creating products that are interoperable across all platforms is key to attaining that goal. Uber is also launching rider support and a remote assistance platform to help autonomous rides that are having issues. This platform will plug right into Uber’s hybrid network to match a rider with a new driver if there’s an issue with the trip. Next, it again talked up the importance of fleet maintenance for these expensive assets that will get way more usage than a manned vehicle. And finally, they’ll offer a fleet control dashboard to partners, allowing them to see their assets in action and how they’re performing.

Uber has two very important jobs in terms of solidifying its AV positioning. It needs to help more competitors to fully commercialization (alongside Nvidia) to create more market fragmentation that will favor this demand aggregator. And? They need those winners to be using as many Uber services as possible to drive retention and lifetime value. These launches help a lot in that regard.

- Uber Air also started its air taxi partnership with Joby Aviation. It will begin this year in Dubai.

- Freight Alley CEO Craig Fuller has been noticeably elated about recent freight trends. He has been talking up demand and pricing strength and an expectation that this will continue. Perhaps Uber Freight is finally poised to grow a little bit.

3. Block (XYZ) – Layoffs

A headline this week about Block firing 40% of its staff created more anxiety for software and the overall economy. While that’s understandable, I think Block is a unique case. They are an inefficient, wildly bloated company that has a CEO who likes to throw $60M parties with shareholder money. They compounded headcount at a 50% clip from 2019 to 2022 and topped out around 13,000 total. For context, that’s nearly triple SoFi’s headcount despite Block’s market cap being just 40% higher. Getting down to 6,000 employees is a sign of XYZ actually taking margins and profitable growth seriously. They can blame it on AI, but I blame it on Dorsey undoing years of mistakes.

AI will lead to lower headcount needs in some parts of the economy. I just don’t think 40% layoffs are going to come remotely close to the new norm. And I’m also confident that the AI boom will create new jobs that aren’t yet on anyone’s radar.

4. Headlines & Macro

Company notes:

- Rumors are circulating that Google secured a multi-billion-dollar chip order from Meta.

- Meta will relaunch its stablecoin this year.

- Amazon was part of a new $110B fundraising round for OpenAI.

Output Data:

- The Chicago PMI for February was 57.7 vs. 52 expected and 54 last month.

Inflation Data:

- The Producer Price Index (PPI) for January was 0.5% M/M vs. 0.3% expected and 0.4% last month.

- The Core PPI for January was 0.8% M/M vs. 0.3% expected and 0.6% last month.

Consumer/Employment Data:

- Conference Board Consumer Confidence for February was 91.2 vs. 87.4 expected and 89 last month.

- Initial Jobless Claims were 212K vs. 217K expected and 208K last month.