1. GoodRx (GDRX) — Mark Cuban Competition

Mark Cuban launched an online pharmacy to sell 100 generic drugs at deeply discounted prices by 2023. This will provide new competition for GoodRx but the company should be able to seamlessly cope (in my view) for the following reasons:

- Nobody matches GoodRx’s PBM scale of ~15. This means GoodRx can generally offer better pricing than the rest of its competition thanks to more pricing points. SingleCare comes the closest and GoodRx still boasts “dominantly better pricing” than it does with those leads expanding. The new start-up could offer lower prices on the occasional medication — but for the vast majority GoodRx will be better.

- Formidable competitors like Amazon have tried to take a piece of this market. The company has had “no success to date” and boasts just a few hundred monthly users for its competing product. Countless start-ups have come and gone with no traction.

- This is a $564 billion market with the primary growth hurdle for GoodRx being the 70% of Americans who still do not know drug prices vary. This is a massive, greenfield opportunity. It’s hard to believe the outcome will be winner take all (but if it is GoodRx is better-positioned to be that winner).

- The company is actively expanding into branded drugs thanks to leveraging its massive scale. Cuban’s project has miles to go before it can try mirroring this incremental value by attracting enough branded makers.

- The vast majority of GoodRx’s transaction revenue is collected via brick and mortar pharmacies. There are many reasons that consumers have been hesitant to evolve prescription shopping to online — mainly that the person must be at the door to sign for most deliveries. Online penetration rates topped out at 5% during peak pandemic pain and have since fallen.

GoodRx’s success will be the effect of its product suite’s traction and management’s execution. One start-up with a wealthy founder is not alarming — but rather more proof of concept for this massive opportunity being worth pursuing.

Click here for my GoodRx Deep Dive.

2. Upstart (UPST) — New Referral Partner

Upstart announced Corning Credit Union as the newest member of its referral network. This is partner number 33 — although that amount is likely higher as Upstart generally doesn’t report on new relationships until months after consummation. The two entities began working together in September 2021, but Corning is now ready to join Upstart’s referral network which represented 62% of its total sales in the last quarter. With more than $2 billion in assets under management (AUM), Corning is a top 250 credit union in the nation by size which boasts 140,000 members spread across 1,700 employer groups.

Since the National Association of Federally-Insured Credit Unions (NAFCU) named Upstart as a preferred partner for its network, the company has rapidly added credit unions to its partner ecosystem. Considering NAFCU represents 72% of all federally-insured credit unions and Upstart is just 1 of 8 partners — this affiliation is likely boosting the momentum.

“There’s growing recognition and interest in credit unions offering unsecured personal loans to their members. We overlooked credit unions in our early days of partnerships which I think was a big miss on our part to be frank. We under-appreciated how much more consumer oriented credit unions are — a credit union the same size as a small community bank will do a lot more personal lending because they’re more interested in being consumer facing.” — Upstart SVP of Business Development Jeff Keltner

My Upstart Deep Dive will be published tomorrow.

3. Penn National Gaming (PENN) — Ontario and Louisiana

Penn National Gaming’s “theScore Bet” sportsbook in Canada received “RG Check iGaming Accreditation” from the Responsible Gaming Council (RGC). This is considered one of the largest hurdles to going live in Ontario — the Country’s most populous Province — and theScore Bet is the first private market player there to gain the label. Sports betting is now set to launch in Ontario on April 4th — and theScore Bet will be ready.

Penn National Gaming bought Score Media last year mainly to augment and vertically integrate its technology stack — but that wasn’t the only reason. The Score is the number 1 sports app in Canada (number 3 in the USA) — it has built a large, loyal following with our neighbors to the North. With Ontario having more people than 46/50 states, theScore should be poised to dominate there going forward. Barstool will be the lead brand for sports wagering and entertainment in the United States with Penn planning to lead with Score in Canada.

“Our team at theScore has been hard at work preparing for the Ontario market opening. As Canada’s preeminent digital sports media brand, theScore is uniquely positioned to capitalize on the introduction of the open and regulated internet gaming market in Ontario, its home territory. Launching theScore Bet in Ontario will mark an exciting expansion of our online gaming business into a major new market where we already have an established mobile sports media product in theScore app and a wide base of loyal users.” — Penn CEO Jay Snowden

Not only does Penn gain access to a team of software engineers to improve its user interface (UI), but it gains another cult-like brand in another country. Penn will continue to lean on its stable, brick and mortar business to serve as a cash cow to feed the rest of these exciting growth projects.

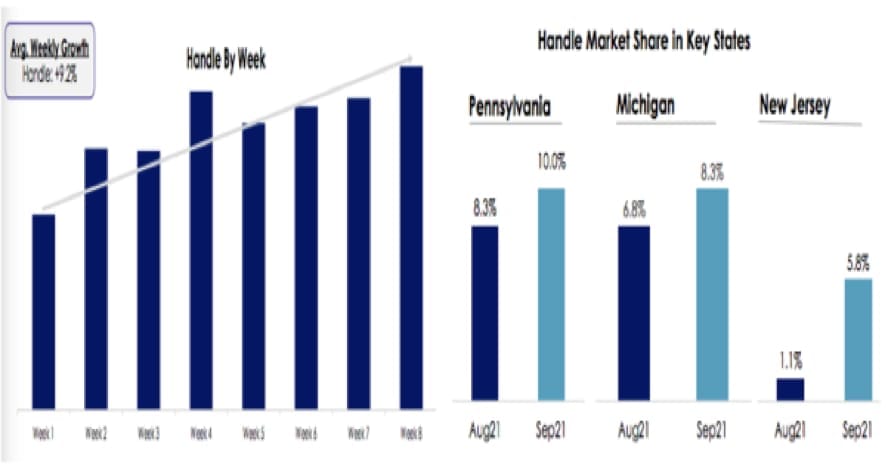

For a quick note on sports gambling — I’m not a fan of the sector overall. Competition is spending like drunken pirates to take market share and net losses across the board are wildly bloated — except for Barstool Sportsbooks. Barstool has a unique ability to tap into its more than 70 million monthly active consumers (across all social channels) and beloved personalities to market its product more efficiently. Its revenue market share per state (which was rising in key states as of last quarter) consistently outpaces its handle (bet) market share per state because the company doesn’t need to spend as much to acquire its users. Data from Pennsylvania shows that Barstool’s handle and revenue in the state has continued to tick up through the end of December.

Barstool essentially provides limitless free marketing which has allowed Penn to de-couple itself from the competition of who can burn through the most cash on promotions. Conversely, Penn expects this standalone product to be EBITDA breakeven sometime this year — before any others. Eventually, irrational market share spend will slow down and brand loyalty will become a more important piece of the equation. Nobody in the space fetches a level of loyalty that Barstool brings to the table.

In other news, Barstool has received final approval to operate its sportsbook in Louisiana. It went live on Friday. This is state number 12 for Barstool’s digital product.

4. Ozon (OZON) — Staying the Course

Ozon — the stock not the company — has had a tough quarter. A potential Russian invasion of The Ukraine is serving up daunting headline risk for the company’s share price. Its label as a hyper-growth stock in this tightening macro-environment certainly doesn’t help either. Russia is stockpiling military personnel and resources at the Ukrainian border, Ambassadors from around the world are being evacuated from the nation and The United States is asking all Americans in the Ukraine to leave the country. While seeing a stock go from $60 to $15 in a rather straight line is never fun, this is the kind of dip that I’ve been cautiously accumulating into. Why?

The worst-case scenario for Ukrainian conflict is intensifying sanctions on the Russian economy hurting its consumer. While this could impact Ozon, the company has dealt with Russian sanctions for a large part of its existence — this is nothing new. Even if a worst case scenario were to come to fruition, it’s hard to think the domestic Russian e-commerce revolution would halt (or even materially slow) as a result. Furthermore — if the sanctions actually work — Russia would be motivated to play nice which could rapidly ease this concern.

I added to my stake this week not with the expectation that we’ve found a bottom, but based on the company now sporting what I perceive to be extremely favorable risk-reward. Ozon now carries a forward gross profit multiple under 3x. The stock could continue being hurt by consistent political headlines, but these headlines have little to do with Ozon-the-company’s fabulous success and traction to date and the opportunity it has ahead of it. Short term pain could continue — but the long term potential gains are still fully intact.

In its most recent quarter, Ozon posted its fastest user growth rate in nearly 2 years. Revenue soared 85%, gross merchandise value (GMV) spiked 145.6% and active buyers as well as their order frequency continued to precipitously ascend. As a result, Ozon raised its 2021 GMV growth outlook to 120% vs. 110% in the previous quarter and vs. 90% at the beginning of 2021. Importantly, CapEx guidance has not changed with this spike and operating costs per delivery recently dropped 16.1% year over year. Both show very early signs of operating leverage with a long way to go.

From a margin perspective, the company continues to both briskly expand its gross margin (+340bps YoY to 36.6%) and remain in cash burn mode with a free cash flow (FCF) margin of (34.9%). While cash burn is never ideal, the company already demonstrated its ability to be FCF positive last year before it started ramping up logistics, fulfillment and other growth investments. These investments will give Ozon the largest and broadest delivery footprint in the nation already with a 98% on-time delivery rate.

I wholeheartedly support this spend because it’s working. The company’s expedient courier capabilities contribute to top of mind brand awareness for Ozon in Russia with the lead consistently growing. This top of mind brand awareness should be quite lucrative based on the make-up of Russia. The nation boasts an e-commerce penetration rate of just 10% vs. 21% in the U.S. and 27% in China. Conversely, Russia’s internet and smartphone penetration is roughly similar to these two nations. Translation? There’s ample low hanging fruit for Ozon to leverage its network and brand loyalty and shift commerce online. Consumers in Russia have the tools needed to enjoy e-commerce — now Ozon is providing the convenient, reliable service.

The spend hasn’t just been on fulfillment — but on new verticals and geographies as well. Ozon’s debit card issuances soared 60% sequentially to 1.6 million. These holders order from Ozon 60% more frequently than non-holders. Ozon’s flexible payment plan for sellers saw 109% sequential growth as well with Ozon credit now actively issuing loans to its vendors. Its one-hour delivery service extended outside of Moscow last quarter with 20,000 SKUs including private label goods like coffee and snacks. It’s pushing into Belarus and Kazakhstan (28 million more people in total vs. 144 million in Russia).

The fundamental thesis remains fully intact — and yet the geopolitical and macroeconomic risks remain intense.

So?

I have not paused adding to this name, but I have widened to multiple compression bands needed to justify adding to my stake (similarly to Lemonade due to its newness and deep cash burn). As ridiculously appealing as the valuation looks today, it could always get cheaper as war is known to create wildly irrational short term price action — along with Jerome Powell. The deep cash burn as global monetary policy tightens only amplifies the exogenous issues for the firm. Knowing this, I am leaving significant room to average down into a black swan event. I fully believe there are brighter skies ahead — but storms could continue for now.

Click here for my broad overview of Ozon.

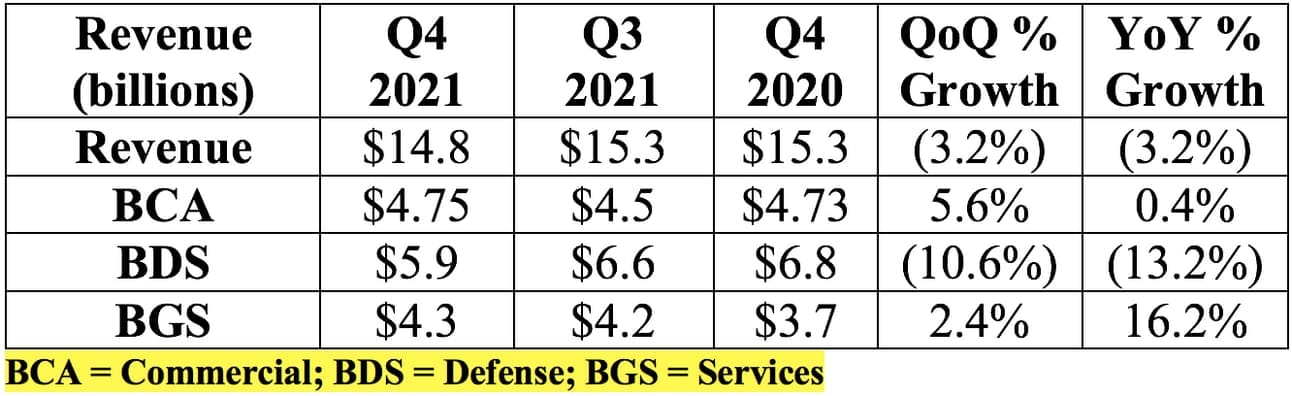

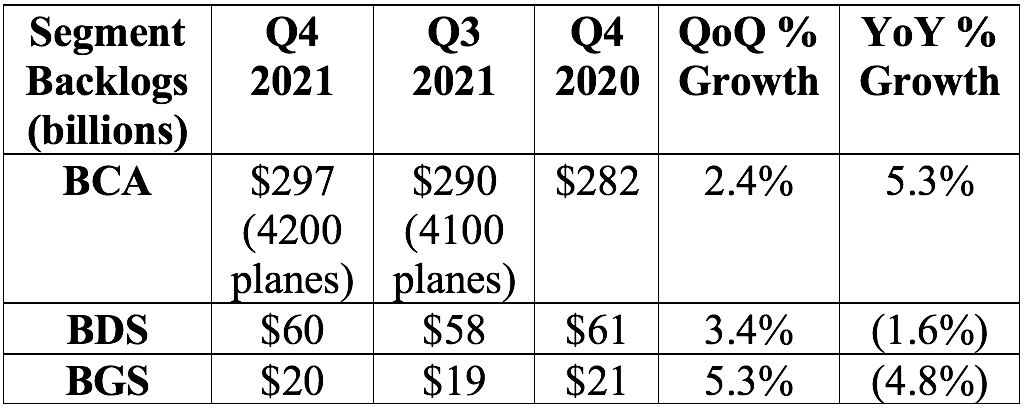

5. The Boeing Company (BA) — Earnings Review

a Demand and Backlogs

Boeing was expected to generate $17.1 billion in sales for the quarter. It posted $14.8 billion which missed expectations by 13.4%.