Table of Contents

During the week, I published a piece on recent AI infrastructure developments that can be found here. I also published my latest holdings, portfolio management approach & updated performance vs. the S&P 500.

1. Meta (META) – Various News

Capacity Plans:

While it was a quiet news week for most public companies, the same was not true for Meta. Following a $10B Canadian data center announcement, headlines from Bloomberg broke about the company planning to double compute capacity in 2027. It’s worth noting that this does NOT mean CapEx will double Y/Y in 2027. That is highly unlikely, with a lot of this added capacity coming from spend incurred before 2027. Some large accounts on social media are concluding that CapEx will double based on this news. That’s not the right takeaway. Furthermore, while this is absolutely a sign that Meta is pushing ahead on capacity plans, we don't know if this is a reiteration of previous internal intentions or a change. So while this does still seem bullish for AI infrastructure, that makes it hard to gauge exactly how bullish. That 2027 CapEx commentary on the Q3 call (if we get it and I think we will) should be interesting. Growth rates will almost surely slow compared to 2026, but the question is... by how much?

Public Cloud Entry Context:

Next, it sounds like recent news that Meta is joining the public cloud market has everything to do with how compelling the offers it's receiving are. They’re too good to resist. So while they are renting out some capacity, it sounds like that’s coming at the expense of using the compute elsewhere rather than just not needing it anymore. That makes complete sense, considering they’ve spoken constantly about how many use cases they have for this spend and how fungible it is.

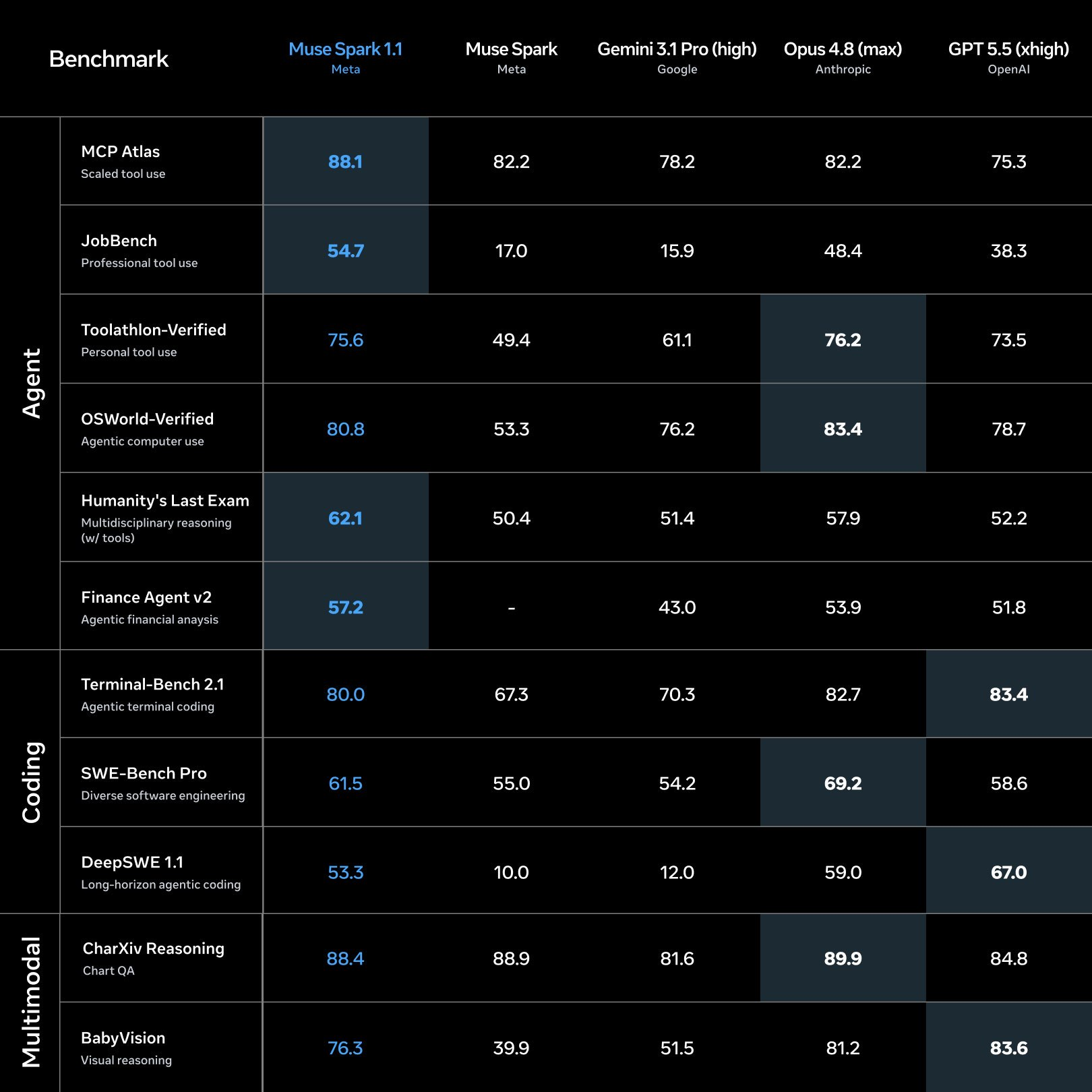

Improving Model Momentum:

And for more Meta news, they’re now rolling out paid developer APIs to access their new multi-modal Muse Spark 1.1 model as they add another leg to their AI monetization. While this new model isn't the best out there, Meta is very pleased with its performance and even went as far as saying it's better than they were hoping for.

This general model momentum is even allowing them to swap existing 3rd party model usage with their own image creation model released this past week. The encouraging news comes just months after discussing disappointment in pace of improvement. Zuck sees a clear ability to use improving models and new APIs like the one discussed above to offer cheaper tokens and intelligence at still strong margin. It sounds like they plan to deeply undercut OpenAI and Anthropic.

- Finally, headlines broke that Meta is facing a $1.4 trillion fine from states about teen mental health issues. The company will likely end up paying some kind of sizable fine, but it will be a tiny fraction of that gigantic amount.

2. Netflix (NFLX) – Evolving Approach

Netflix is exploring different ways to provide its content via channels and different bundles. Per WSJ, this is a response to softer engagement trends and declining TV viewership market share (now at 12+ month lows). I know this has been a darling for quite some time, but I do think these struggles could easily continue. Google, Apple & Amazon all continue to push further into entertainment. And? They don’t need to make any money on these libraries. They can operate at razor thin margin & use this as a vehicle to cross-sell more things/ads to consumers. Netflix does not have that luxury. They have to compete with several of the richest companies in the world and do so more profitably. This (I think) belongs in the too hard pile. I know that’s not a popular opinion, and I hope in a year I look extremely wrong and bulls can laugh at me.

3. Starbucks (SBUX) – Homegrown AI Apps?

Starbucks is reportedly using AI models to customize apps that will replace Microsoft, Oracle and IBM. I think these headlines will turn into enterprises boomerang-ing back to 3rd party vendors more times than not, but this is something to keep an eye on. If SBUX is able to use their 1P data with models and agents to supplant 3P contracts and save money, that is bad news for the retention and growth metrics of the companies involved. It would be surprising to me, but it’s always possible.

This sounds like a lot of workflow and collaboration automation, which leaves Snowflake, Axon, Rubrik, and I think Shopify very safe. Data infrastructure and cybersecurity themes aren’t related to this type of homegrown solution creation. The software holding most directly tied to this negative news with the most similar apps/product/value prop is ServiceNow. They do a lot in data and cybersecurity, but workflow automation is their bread and butter. I do not see this turning into a trend. Companies need to prioritize work and expensive AI consumption and building/maintaining a CRM or point of sale or HR app isn’t at all mission critical. That is not a best use of finite resources (in my opinion). It makes way more sense to pay best in class platforms for these tedious tasks and focus on profitable growth. Still, this needs to be tracked. If it does turn into more of a theme and I am wrong (always possible), that could lead to renewed app layer concerns across ServiceNow, the three companies mentioned, Salesforce, Workday and those types of platforms.

4. Nu (NU) – Mexico

Nu received regulatory approval to operate as a multiple banking institution in Mexico. This gives it all of the same benefits and permissions as legacy incumbent banks in the country. Finally enjoying the same flexibilities and cost advantages that these competitors enjoy will pair perfectly with its digitally native operations and owned tech stack. These features already allowed it to operate at far lower cost than others can. Now, that existing cost advantage will merely deepen and emulate its thriving Brazilian business.

5. Headlines & Macro

Company headlines:

- SoFi web traffic rose 32% Y/Y in June. This is not perfectly correlated with revenue or profit by any means. But a good data point.

- Uber has paused most EU market expansion efforts to focus on taking over Delivery Hero. This could be a sign that it's getting closer to obtaining control.

- Apple is "increasing spend" with Broadcom as it leans more heavily into custom chips. This comes as AI model labs and most hyperscalers also work diligently on their own custom chips.

- Snowflake's new Paris headquarters is now open as it pushes more aggressively into Europe.

- AWS and Warner Brothers are building a new ad platform together. Amazon is also developing more multi-step tasks for Alexa AI (project code name is Moonraker). Amazon also raised $25B in new debt to help fund ongoing CapEx plans (received $62B in peak demand).

- ServiceNow and Hitachi Digital Services are partnering on joint infrastructure monitoring.

- Rubrik Security Cloud launched on AWS's EU Sovereign Cloud, expanding coverage and access convenience for shared customers.

- Waymo is adding 4 new cities to its expansion plans.

In macroland, manufacturing data was a bit softer than expected and employment data was a bit better than expected across the board.