The big news from this week was Micron earnings. Our full review was already published and can be found here. Outside of that, it was a very quiet few days and will likely remain that way until mid-to-late July. This is the slowest part of the year when Wall Street goes on vacation.

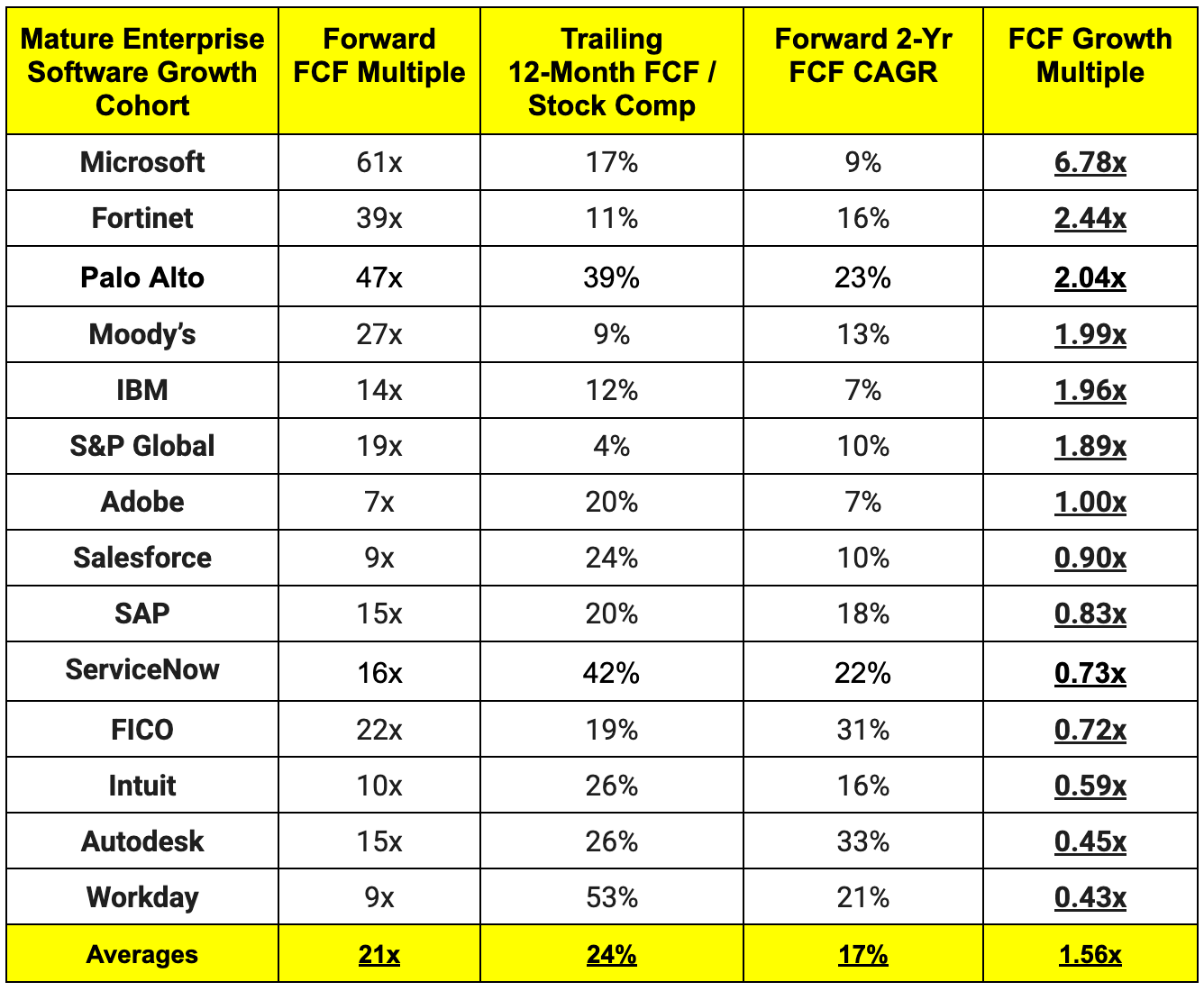

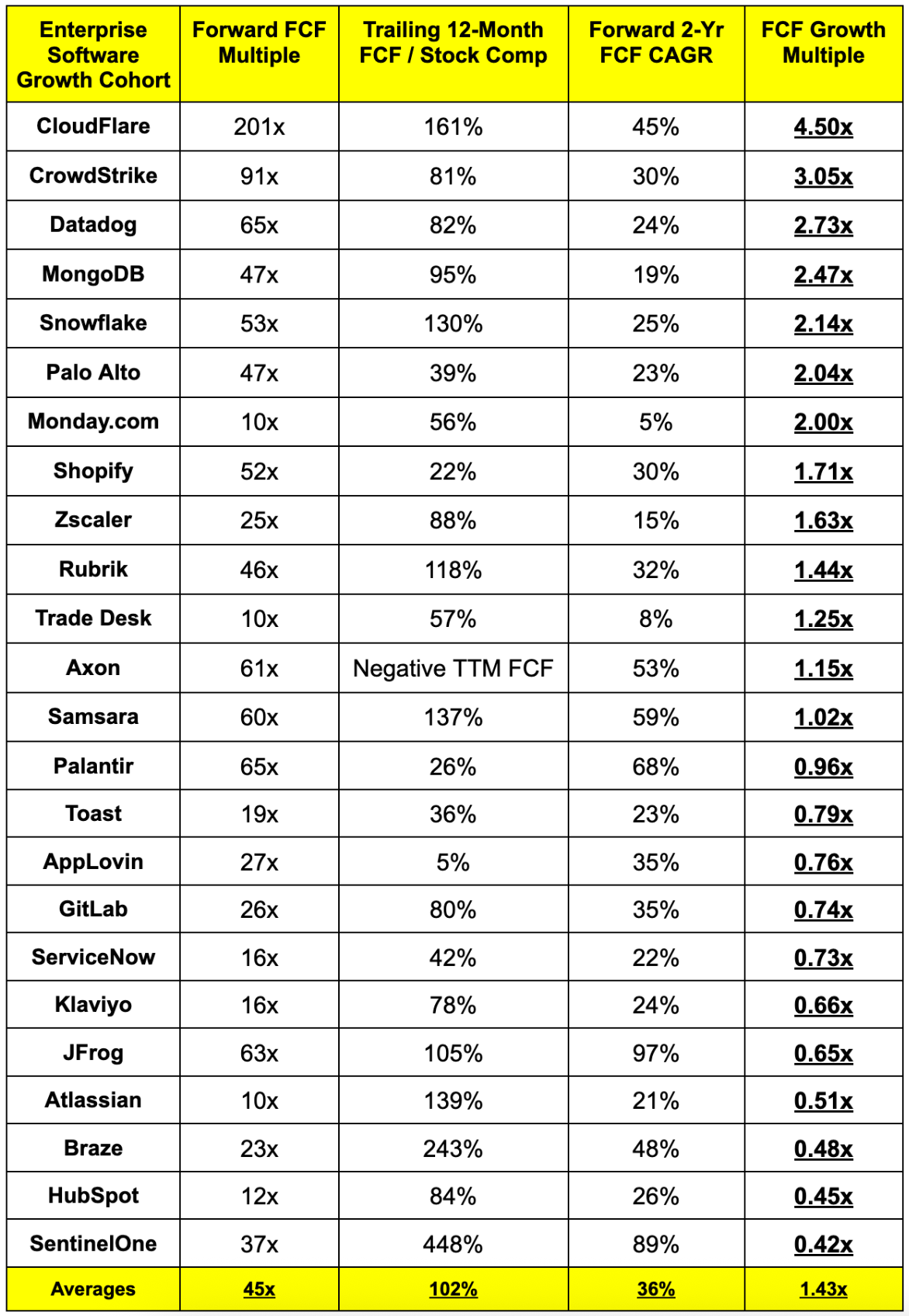

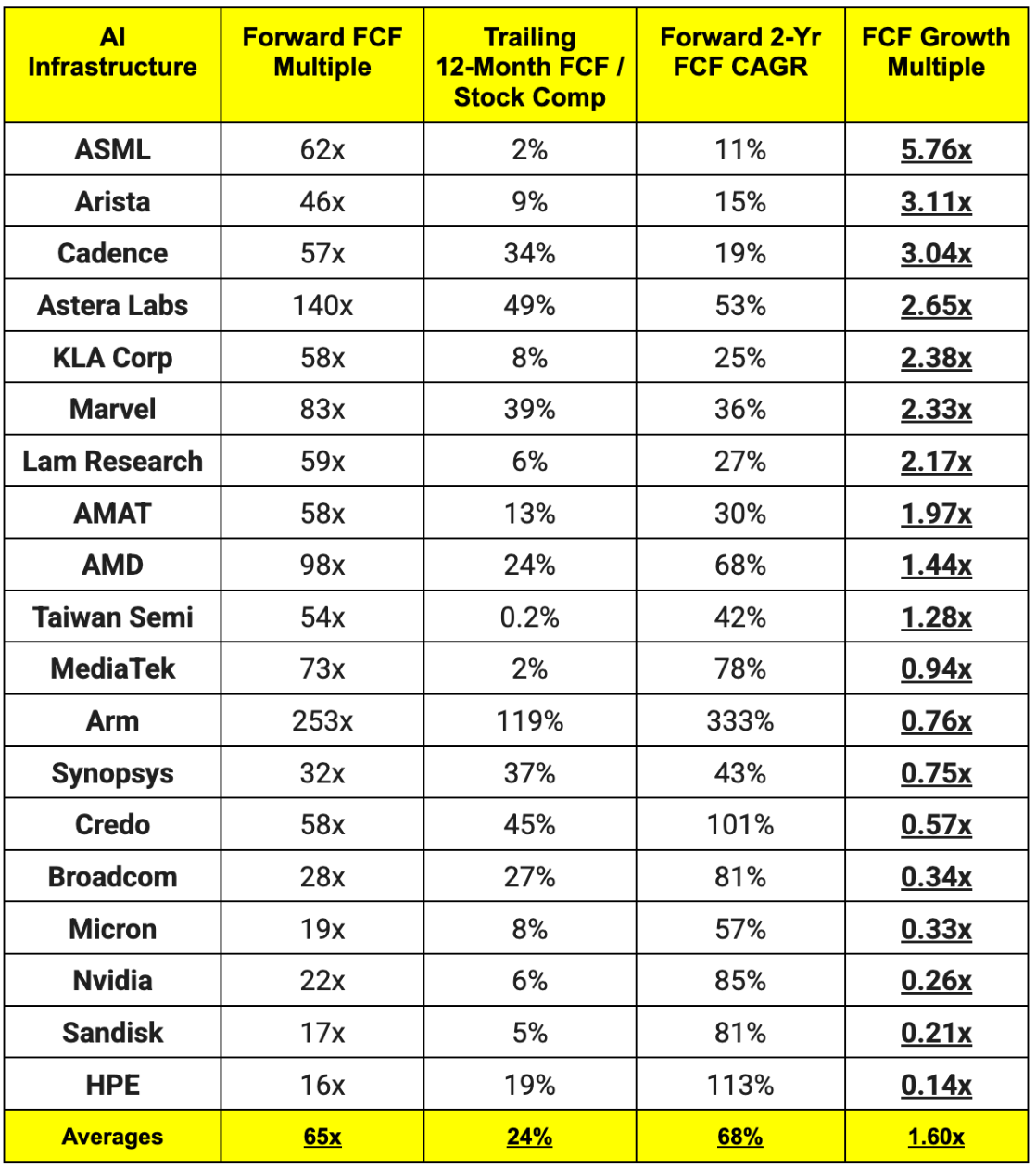

1. Free Cash Flow Growth Multiple Comp Sheets

A few notes on the data:

- FCF growth multiple is a variation of the PEG ratio that uses free cash instead of net income for calculation.

- Instead of using 1 year of profit growth to calculate the multiples on the right side of the images, I use 2-years of compounded annual profit growth.

- Oracle, Applied Optoelectronics, Lumentum and Intel are excluded due to lack of positive FCF for the given period. Qualcomm is excluded due to negative FCF growth over the given period.

- I skipped a year for Mediatek profit growth to avoid -45% Y/Y FCF growth and so I could include it in the chart. I also skipped a year for Micron/SanDisk profit growth to avoid 2 more extreme outliers.

a. Mature Growth Software

b. Fast Growth Software

c. AI Infrastructure

2. Lemonade (LMND) – Growth Financing Update

Lemonade added a new capital market partner this week in Hannover (one of the large reinsurance companies in the world based in Ireland). This will be for up to $250M in growth spend financing and begin January 2027. The most exciting part of this news is the interest rate on borrowed money vs. what they paid General Catalyst. At the current Fed funds rate, it would be about 6 points cheaper (little over 10% rate). A great sign of Lemonade’s maturation, rising underwriting reputation, growing brand awareness, & improving balance sheet. This will let them get even more aggressive on pursuing more growth, as the cost associated with doing so is now significantly lower.

3. Meta (META) – New Products & an Investment

a. New Products

Meta announced two interesting products this week. First, they're pushing into long-form video to attempt to capture some of the overall screen-time from Netflix and other streamers. Separately, they're also building a prediction market app internally, while exploring partnerships with Kalshi and Polymarket too. Both of these initiatives are attractive to me. This is Meta leveraging the immense value of the traffic it has already earned to make sure it's profiting from it in as many ways as possible.

I see each project as a very low risk way to test if new forms of engagement captivation work on their apps. If they do? Meta makes more money on the same massive base of people in its ecosystem. If they don't? It shutters the projects and moves onto the next ones without a material revenue hit or a risk to forward estimates. So either new legs of revenue to add to family of apps (FOA) or a blip on the radar and part of Meta's overall experimentation as it optimizes app experience and revenue per user.

b. New Investments

Meta is pushing more deeply into the highly attractive India opportunity. They're investing $900M in a fintech called CRED. Similarly to their ScaleAI investment, the founder (Kunal Shah) will join Meta as the new Head of WhatsApp and with ample payment infrastructure experience to guide this high potential product's future. For those of you who don't already know, WhatsApp is ubiquitous in India. And people use it for a lot more there too. Whether that's booking an Uber or other actionable in-app experiences, it's an especially prevalent part of day-to-day living there.

While Meta has made great progress on WhatsApp monetization, this remains the app with the biggest gap between potential and current financial contribution. This is why prioritizing a complementary payments platform to join the budding list of useful things to do on the app makes complete sense. It's how Meta not only can create good in-app experiences and consumer convenience, but also work to fetch a bigger piece of the overall profit per transaction. CRED has a strong presence within digital payments and lending, which should be a rapid accelerant to WhatsApp Pay's roadmap.

- Meta is hiring Virtue AI's co-founders to its Superintelligence teams. Virtue AI makes AI security and governance tools and should make Meta a better agent-based work and orchestration partner.

- Meta also debuted a company-branded pair of smartglasses for $299.

4. SoFi (SOFI) – Product Launch

SoFi is debuting a conversationally-powered AI investment strategy builder via its Composer Securities acquisition. If someone thinks rates are going way lower & the market is wrong? Or if they believe a new theme will take over investor attention? They can now describe it & the product will build a strategy to reliably reflect that view. Like WhatsApp for Meta, SoFi Invest is arguably SoFi's most under-monetized & highest potential tool. They can make a lot more money on existing users by adding proven features that others already have. They've made a lot of progress in that regard and are now taking advantage of their owned tech stack and modern infrastructure to create entirely new services that can help it accelerate market share gains. It's good to see them keep focusing here.

5. Headlines & Macro

Memory Inflation:

Consistent and massive price hikes from memory manufacturers are now creeping their way into overall inflation dynamics. Consumer hardware giants like Apple and Microsoft's Xbox are jacking up prices to account for rising component costs, and it sounds like those costs will just keep rising in the near term while shortages persist. If all of the new supply coming online next year doesn't take care of the scarcity issue, I think there's a small but growing chance that the federal government steps in to implement some kind of temporary regulation to cap pricing for the time being. That always creates inefficiency and deadweight loss, but it may be a necessary concession to accept if this is going to have a material impact on headline inflation numbers. That would quickly slow growth and gross margin expansion for all of these vendors, as both of those things are currently mostly powered by price raises. Not a prediction, but something to keep an eye on and something that my buy-side friends are also considering a rising possibility.

- Apple is also reportedly asking for permission to buy memory from a Chinese supplier currently on the military's blacklist.

More Macro Data:

The core personal consumption expenditures (PCE) was in line with expectations but still quite elevated. It rose by 0.3% month-over-month (M/M) and by 3.4% Y/Y due to hot services pricing and resilient consumer spending. That's not all bad news, but it does point to stickier and more structural inflation, which makes more hawkish fed policy a more likely outcome. That's especially true if war continues to rage in the Middle East, as energy pricing will indirectly impact core readings (even if directly excluded). Output data for the week was good across manufacturing indexes, while the latest Q1 GDP reading was 2.1% vs. 1.6% expected. Finally, initial jobless claims were slightly lower than expected.

Company Headlines:

- OpenAI is considering a 1 year IPO delay.

- Amazon is investing $13B in India cloud infrastructure through 2030, boosting its existing commitment from about $35B.

- Alphabet has lost a few key pieces of AI talent over the last couple weeks. Noam Shazeer (Gemini’s co-lead) leaving for OpenAI is the highest profile. Also lost a Google DeepMind VP to Anthropic and two other researchers to Anthropic (which it owns nearly 15% of). We continue to see AI companies steal talent from each other pretty consistently. I am not fretting. Google DeepMind is known for its deep bench of world-class talent, and this doesn't change that in the least. The company is also reorganizing some AI team talent.

- Zscaler is deepening its AWS partnership to include safe AI enablement and adoption for the public sector, hospitals and schools. AWS is a big, big part of those sectors. This allows customers to more safely embrace the technological change while more easily doing so with Zscaler’s products.

- Palantir & Zeta signed a new 7-year deal for Zeta to use Palantir as the foundation for their data platform. The two will also spearhead a "joint go to market" to help customers sharpen their advertising practices with better data and technology. This is probably a bigger positive for Zeta than Palantir in terms of potential financial impact. In other Palantir news, The U.S. Army’s Next Generation Command and Control (NGC2) platform, purpose-built to modernize battlefield analytics and decision-making, is using Palantir as a key cloud data partner to power its evolution. This will function as that product’s source of efficient and cohesive data ingestion, creating interoperable insight out of formerly disparate silos to use in a highly relevant and customized model. This means the U.S. Army can work in more informed, safe and effective manners.

- Uber added FedEx Office, Kiehl's, Choice Pet and a few other brick and mortar vendors to Uber Eats.

- The early part of Amazon's Prime Week went a bit better than Bloomberg consensus. We should get more news on this soon. You might see headlines about Y/Y declines, but it's important to keep in mind that Amazon keeps adding more days to these events, so it's not a fair comparison.