Table of Contents

It was a very slow week of news. Wall Street analysts and executives are fully in summer vacation mode, and news flow was light. Things will pick back up in a couple of weeks when Q3 earnings season commences (can’t wait). But there were still some meaningful fundamental developments that crossed the tape during this generally sleepy period.

1. Nike (NKE) – Earnings Data & Some Thoughts on Apparel

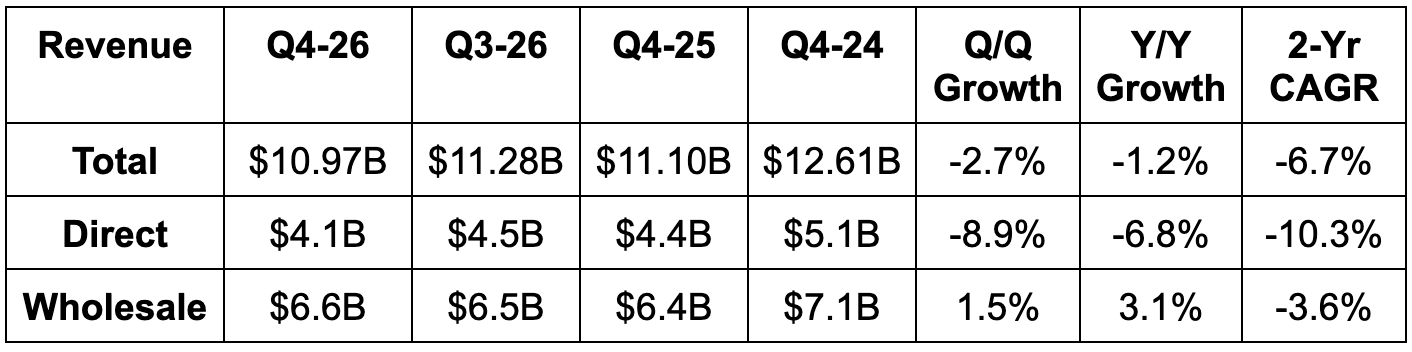

a. Earnings Data

- Beat revenue estimates by 1.2%. Y/Y comps got much easier, yet growth still meaningfully decelerated.

- Slightly missed North American revenue estimates.

- Slightly beat Europe, the Middle East and Africa revenue estimates.

- Beat China revenue estimates by 7.6%.

- Beat Asia Pacific + Latin America revenue estimates by 2.2%.

- Wholesale revenue beat by 1.8%. Direct-to-consumer revenue missed by 1.1%.

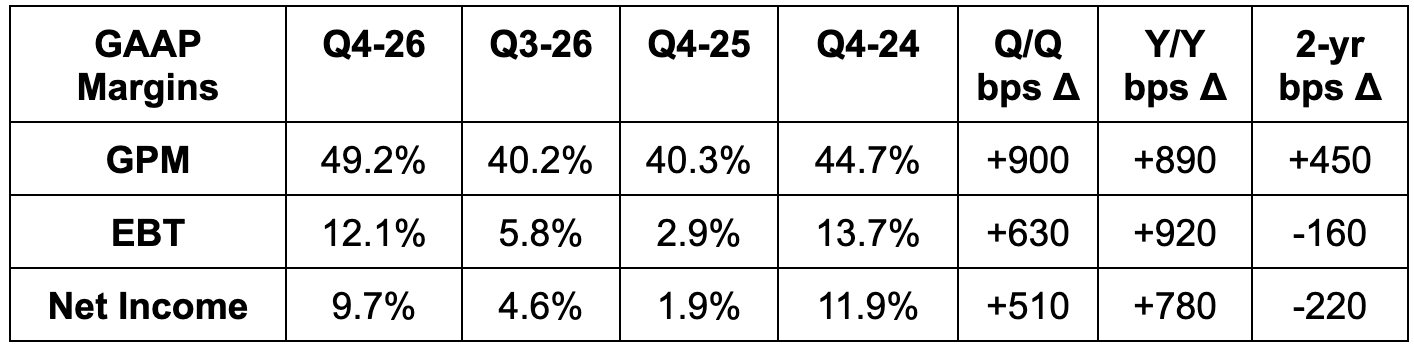

- Beat 40% GPM estimates by 20 basis points (bps; 1 basis point = 0.01%).

- Beat $0.12 EPS estimates by $0.08.

b. Forward Guidance

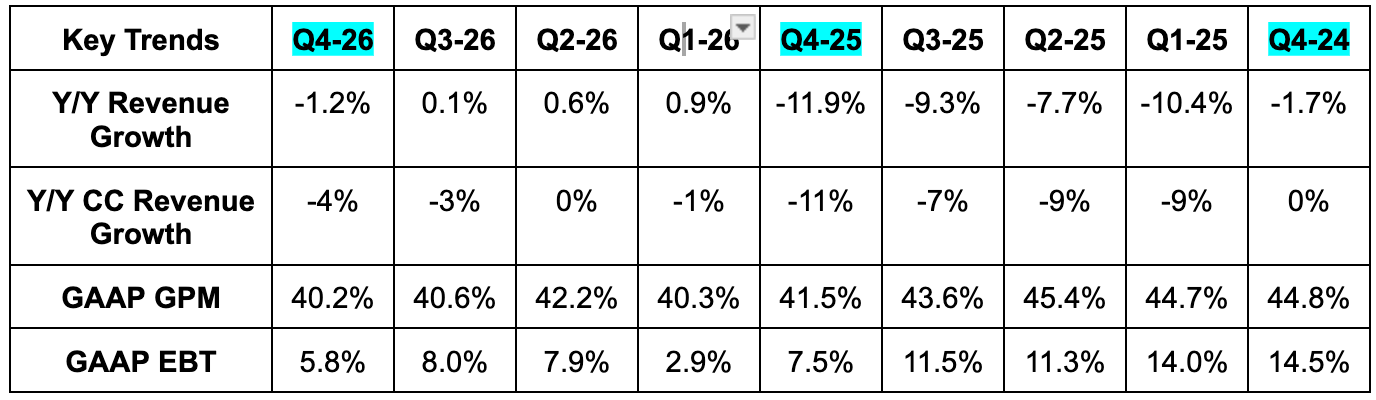

Three months ago, Nike guided to revenue for the first half of the year to be down about 5% Y/Y. They guided to 0% Y/Y EPS growth over that period and gross margin beginning to improve after Q2. Due to disappointing “recent sell-through trends” they’re moderating revenue growth expectations over the first half of the year. This is related to tighter inventory control, which will mean gross margin inflects a quarter earlier than expected. All of this led to next year revenue estimates falling by 2% and EPS estimates falling from $1.81 to $1.73.

c. Other News & Quick Thoughts

We’re now a couple years into the new team’s turnaround, with this news pointing to lack of progress on introducing fresh assortment, fixing inventory and reigniting Nike’s financial success. It feels like progress has stalled or even deteriorated over the last 2 quarterly reports.

Apparel is so hard. Changes in consumer taste & preferences are hard to model. They change on a whim. Missteps in evolving with the times can be the beginning of the end… even for the hottest & most beloved companies. Lululemon is learning that lesson right now. And even if you are killing it on assortment, this is not a structural growth sector. A new shirt is among the easiest things to cut first.

Simply put, this is a sector where hot brands come and go constantly, with the end of brand awareness and store growth runways generally meaning these companies become cyclical and unpredictable growers going forward. I’m not saying I’ll never own a company in this sector again. I just don’t anticipate doing so in the near future, even for the current hot brand darling (On Holdings) trading at a quite attractive valuation.

Finally, after 2 decades with the company, Nike CFO Matthew Friend will be replaced by David Denton (former CFO of Lowe’s and CVS).

2. Uber (UBER) – Waymo

Uber is winding down a 12 car Phoenix test with Waymo. It sounds like they’re replacing the partnership with others in that market and this was an “intentionally limited deployment” but I still don’t like hearing this. I want the signs of the Waymo partnership to be improving. This is a sign that the partnership may be softening, with Waymo positioning itself as more of a direct competitor like Tesla. I know they have many other capable partners to provide supply, but the ideal outcome here is Uber being the ubiquitous marketplace for all hardware vendors… including Waymo. Not good news in my mind. Certainly not a red flag or a deal breaker by any means. But a negative.