Table of Contents

- 1. Amazon (AMZN) – Healthcare & Conflicting Analys …

- 2. Alphabet (GOOGL) – More Regulatory Noise

- 3. Celsius (CELH) – Positive Developments

- 4. Tesla (TSLA), Uber (UBER) & Lyft (LYFT) – We Ro …

- 5. Piper Sandler Teen Survey Highlights

- 6. SoFi (SOFI) – Credit Cards

- 7. JP Morgan (JPM) – Earnings Snapshot

- 8. Cloudflare (NET) – M&A

- 9. Headlines

- 10. Macro

The SoFi Deep Dive will be published tomorrow morning at 6:00 AM. I plan to send a portfolio earnings preview article this week, along with a mid-week Netflix and Taiwan Semi earnings review article. Buckle up… earnings season is here (again).

1. Amazon (AMZN) – Healthcare & Conflicting Analyst Notes

a. Healthcare

Amazon is expanding its availability of same-day prescription deliveries next year. It’s opening 20 new “pharmacies” across the U.S., raising the portion of consumers with access to same-day deliveries to 45% by the end of 2025. Per the press release, most of that 45% will receive orders within 6 hours. These “pharmacies” are really just dedicated portions of existing same-day fulfillment centers, with all of the logistics automation and inventory routing know-how to power same-day fulfillment. Considering 50% of U.S. citizens live more than 10 miles from a pharmacy, this matters a lot.

In addition to shorter wait times, this expansion process will also facilitate lower costs for consumers. Amazon’s world-class inventory forecasting places goods closer to their final destinations, meaning lower cost to serve customers. All of this, paired with unmatched economies of scale, allows Amazon to pass savings onto customers, which it does through other tools like its $5/month Rx Pass and its deep discounts on popular drugs. Cost and access are the two most common reasons for consumers not taking medications as directed. This leads to soaring overall healthcare bills, which Amazon is alleviating.

Rapid, efficient delivery also unlocks more use cases in pharmacy. Just like faster deliveries opened up many more possibilities to sell everyday essentials, the exact same is true for same-day prescriptions. If I have the sniffles or need an antibiotic, rapid delivery enables Amazon to serve these use cases. Another tool making Amazon a deeper part of consumer lives; another tool creating real value for customers; another tool adding to Amazon Prime’s pricing power.

b. Analyst Notes

JP Morgan upgraded Amazon to overweight this week. The optimism was based on free cash flow expectations, as well as growth within its core e-commerce and AWS segments. It doesn’t think regulatory battles will hurt the company. They noted sports rights and CapEx as the risks to their optimistic view.

Mizuho channel checks revealed strong workload migration activity for AWS and raised its cloud spend forecast for 2025 from 22% to 25%. This also led to it raising 2024 AWS growth estimates to 20%, which is ahead of the street’s high-teens estimate. This meshes very well with the positive Yipit AWS data we got last month showing an acceleration towards 20% Y/Y growth. Mizuho is also optimistic about GenAI monetization. Interestingly, the firm thinks overly aggressive AWS EBIT forecasts from the Street and Kuiper profit headwinds could lead to disappointing results this quarter, but they’re positive on the next 12 months.

Scotiabank initiated Amazon with an outperform rating. They see AWS revenue growth “exceeding consensus estimates beyond 2025” and 15% annualized AWS growth beyond 2025. It sees strong traction for its GenAI solutions.

Wells Fargo, on the other hand, downgraded Amazon. It thinks upside to profit forecasts amid lofty investment levels are too rosy. It thinks EBIT in 2025 and 2026 will come in at a mid-single-digit percentage lower than the Street.

2. Alphabet (GOOGL) – More Regulatory Noise

Following an August ruling against Alphabet’s potentially monopolistic practices, the Department of Justice (DOJ) proposed a breakup as a “potential remedy” for the issues. The idea was to prevent Chrome, Play and Android from unfairly propping up Search. The DOJ also added the possibility of blocking certain partnerships and forcing the “Search King” to share its AI search model data and ad ranking algorithms. Forcing the sharing of proprietary data with the world would be severe, and is considered highly unlikely. In my view, that decision would be absurd and quite damaging to this firm.

The probable outcome is the mega-cap being forced to terminate default search engine agreements with Samsung and Apple. It pays both of them billions a year for these rights. No decisions have been made, there will be many more court hearings and appeals. and this will likely drag on for years.

This news comes as another judge this week made a ruling that would force the firm to add more Google Play app download options. The company will appeal this decision as well, and I’m pretty optimistic that they’ll win here. Android already allows for app store side-loading and claims this decision will lead to privacy and security issues from unvetted alternatives. It’s also dealing with a 3rd antitrust case in Europe pertaining to its ad tech business, which I wrote about previously. To me, this case has the most legitimate claims.

I still see all of the incessant regulatory noise for the stock as just that…. Noise. The only thing that would make me nervous is the forced sharing of proprietary data, which almost surely will not happen. I’ve said it before and I will say it again… this thing is easily worth more split up than all together. It is very intuitive to see how YouTube, Chrome, Play etc. would fetch a GAAP EBIT multiple in excess of 16x.

In terms of what I’d do with the equity going forward, I’d have to assess the competitive positioning and updated investment case of whatever newly formed companies I end up owning. It is true that this company leans on a powerful ecosystem that makes all of the pieces in it much stronger together. YouTube data enriches its ad targeting and marketplace inventory; Google Maps data is instrumental in Waymo’s development; Search and Chrome Data enrich Gemini’s utility; the list goes on & on. The splitting of this fortress may erode the competitive positioning of the newly formed companies by cutting off open access to some data, cash, talent etc.

3. Celsius (CELH) – Positive Developments

Celsius enjoyed a sorely-needed series of positive news developments this week. Pepsi’s CEO told shareholders that “distribution points are rising and that it remains optimistic in the partnership.” As a reminder, Celsius distributes its product through Pepsi in North America. Pepsi has been shrinking excess inventory for a few quarters, and that has materially weighed on CELH’s results. Celsius collects revenue when Pepsi orders product, not when a can sells in a Kwik Trip. While this quote is not a ringing endorsement of Celsius, it does avoid more negative sentiment over continued inventory reductions. And with the stock 70% off of previous highs, that’s really all it takes. The Pepsi CEO also attributed Celsius weakness to convenience store traffic declines. That should be temporary, but could last for now, as 7-11 alone is shuttering 3% of its stores and overall traffic trends remain poor.

Despite C-store fragility, we got some positive data from Nielsen this week. Through the 4 week period ending late September, Celsius volume rose by 13% with pricing falling by 6%. This is slower volume growth than previous periods, but also a much smaller price decline. Furthermore, energy drink volume overall rose by 1.3% over that same period with a 1.9% price increase. The category has been enduring negative overall growth. This is a good sign. Finally, and perhaps in response to all of this, Stifel issued a positive sell-side note for Celsius calling for accelerating growth and a $51 stock price target (closed at $32.80).

While all of these developments are encouraging, they change nothing about my view towards the position. I love it as a small holding. Consumer brands come and go so often it’s almost a cliché. Between negative Q/Q market share trends last quarter and the Pepsi uncertainty, I’m happy to own what I own and not interested in adding today.

4. Tesla (TSLA), Uber (UBER) & Lyft (LYFT) – We Robot Event

Elon Musk is highly polarizing and now a highly political figure. That is not what I am here to write about. This newsletter is not for politics; I don’t do politics. I do stocks. I frame this discussion, as always, exclusively from a Tesla business point of view. That’s what I care about and I know that’s what you care about.

a. The Product Announcements

There were four pieces of product news stemming from this highly anticipated event. Two were future launches and two were updates.

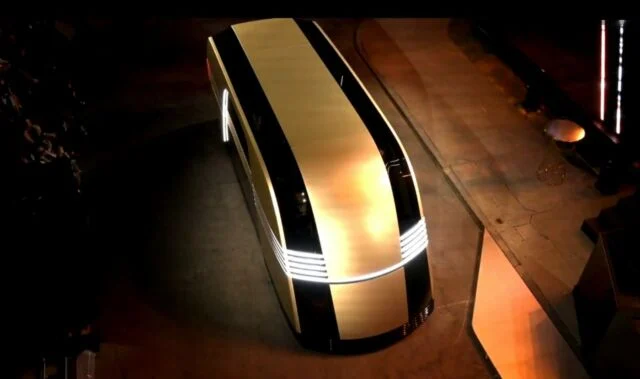

Cybercab:

Starting with the future launches, Elon unveiled a slick looking “Cybercab” robotaxi. It’s a very pretty car in my view. He rode around the Warner Brothers set in one of these concept Cybercabs before his presentation. 20 more of them were spread throughout the large building for use by attendees. The Cybercab has no steering wheel, no pedals and is expected to be in production “before 2027.” As we all know, and as Elon again explicitly said, his timelines for launches are always optimistic, so don’t be surprised if “after 2027” becomes a new target. It takes a lot of effort to jumpstart brand new product categories and Tesla is blazing that trail. I don’t think it would be wise for anyone, bears or bulls, to rely on these forecasts as gospel for their own investment cases.

The Cybercab, per Musk, could cut the cost of public transit from about $1 per mile on public buses to $0.30-$0.40 per mile with “individualized mass transit.” Furthermore, for the actual owners of these cars, the lower equipment requirements to foster unsupervised full self-driving (FSD) mean lower input costs and unique manufacturing efficiencies. That is a key ingredient in enabling Tesla to charge “less than $30,000” for this vehicle. Finally, as frequently cited, manned vehicles are only used for about 6% of the time in any given week. The remaining 94% is ripe for monetization for owners willing to make their vehicles available in off-hours. So, lower cost for fleet managers, lower cost for public transit and more monetization for owners. If it’s all delivered on, it's compelling. But, again this isn’t coming for at least 2 years and probably more.

Interestingly, Tesla plans to “overspec the Cybercab computer” with more capacity than it needs. Why? Because they believe that large fleets can essentially become massive, distributed swaths of inference compute. He doesn’t precisely share how this compute could be utilized, but it’s an interesting concept.

Finally, as an aside, Elon added a note about autonomous fleets removing the need for giant parking lots everywhere. It would be very cool for this revolution to result in converting acres of concrete jungle into greenery or affordable housing.

Robovan:

Robovan was perhaps the most interesting announcement from this week’s event. It’s “Tesla’s solution for high-density transit.” It can fit up to 20 people (or a lot of stuff for a merchant to transport) and cuts cost per mile down to as low as $0.05. I see this and immediately think “Iron Man” (or Iron Van, as a witty Tweeter put it).

Unsupervised Full Self Driving (FSD):

- Musk reiterated that Models 3, Y, S & X will all be capable of unsupervised FSD upon regulatory approval.

- Musk told investors that he expects regulatory approval for unsupervised FSD to come in California and Texas next year.

- Tesla remains adamant that FSD will be much safer than humans at some point. This software, as he put it, is like a person “living millions of lives and seeing every situation” so that it knows how to react. Unlike people, it “lives these lives” by seeing in all directions, and never texting.