Table of Contents

a. Key Points

- North America and the running category continue to be the highlights.

- Ongoing struggles in China and new challenges in Europe, the Middle East and Africa (EMEA).

- Margins continue to be very challenged by weak demand, turnaround investments and tariffs.

- Nike will host an investor day this fall to offer long-term investor targets.

b. Demand

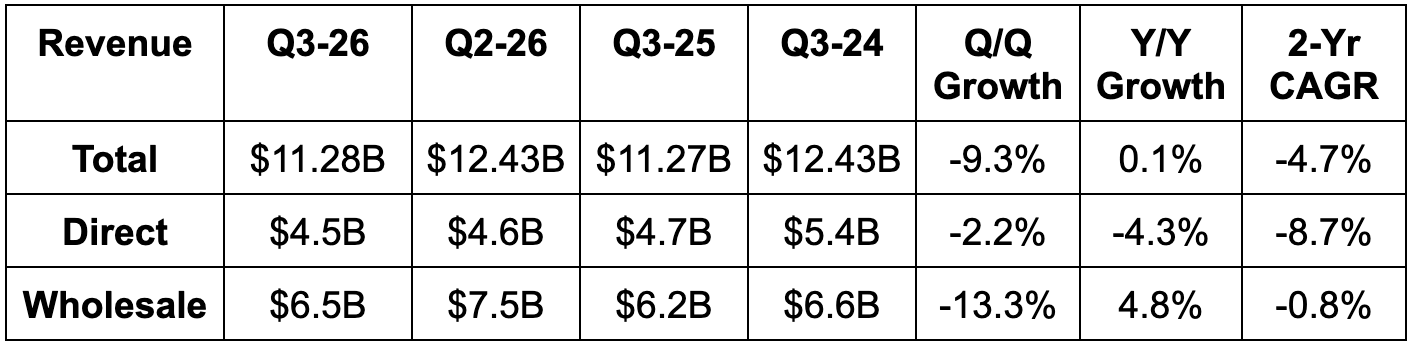

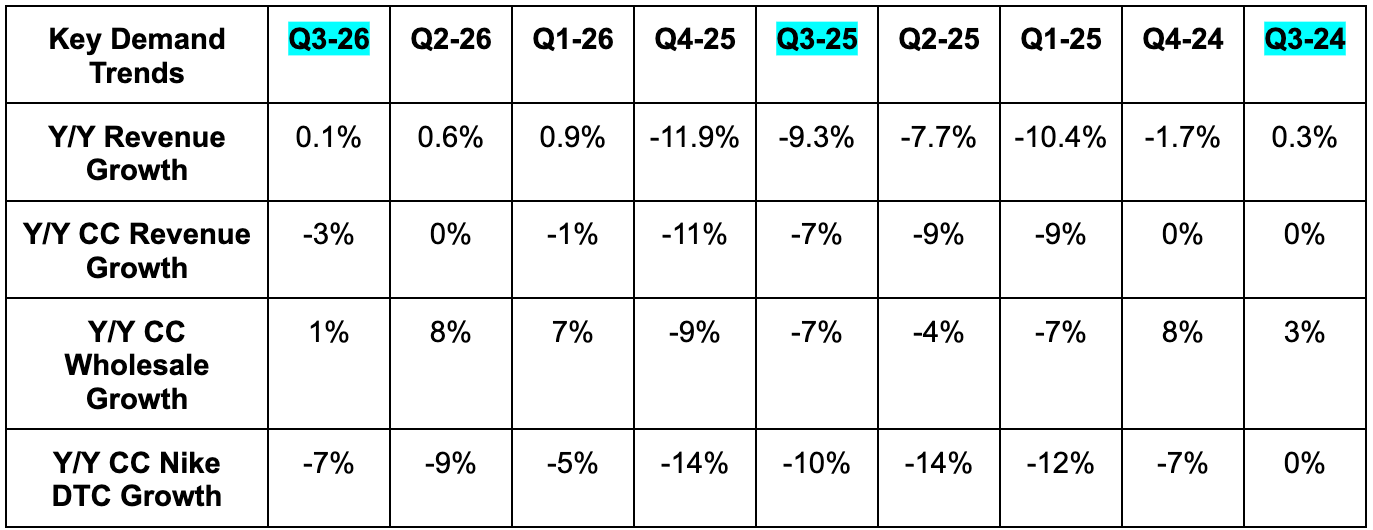

- Revenue beat estimates by 0.4% and beat negative low-single-digit growth guidance.

- North America revenue beat estimates by 0.6%.

- Europe, Middle East & Africa (EMEA) revenue missed estimates by 3.4%.

- China revenue beat estimates by 8.4%.

- Asia Pacific + Latin America revenue beat estimates by 1.7%.

- -3% constant currency (CC) growth compares to guidance calling for negative mid-single-digit growth.

- Wholesale revenue beat estimates by 1.3%.

- Direct to consumer (DTC) revenue missed estimates by 0.4%.

c. Profits & Margins

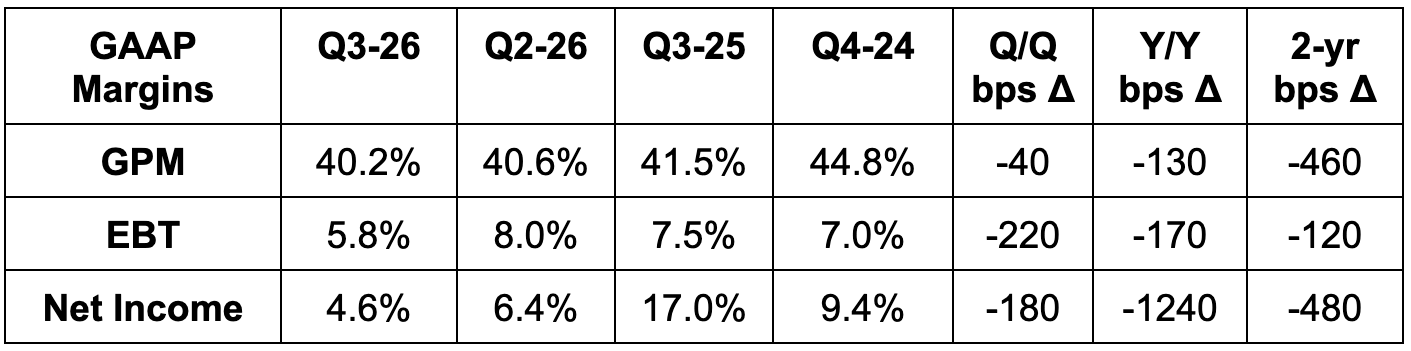

- Beat 39.7% GPM estimate by 50 basis points (bps; 1 basis point = 0.01%) & beat guidance by 70 bps.

- Tariffs powered the gross margin decline.

- Beat pre-tax (EBT) income estimate by 20%.

- SG&A rose 2% Y/Y. Demand creation expense was flat Y/Y, as more sport-level marketing was offset by lower brand marketing.

- Beat $0.28 EPS estimate by $0.07.

- EPS fell from $0.54 to $0.35 Y/Y. It's worth noting that Nike's effective tax rate was 20% vs. 5.9% last year. With a stable year-over-year tax rate, EPS would have been $0.41.

Operating overhead rose 3% Y/Y to $2.9 billion due to $230M in employee severance across supply chain and technology roles. Leadership says de-prioritization of direct-to-consumer sales and efficiency gains at all costs is leading to lower digital infrastructure needs for the company. That’s likely true, but I think over-hiring and spending throughout the pandemic likely is part of the reason too. In the coming years, they plan to shift a lot of the fixed costs in their supply chain to a variable cost structure that allows them to add and subtract capacity more easily and diminish the risk of gluts. Looking ahead, Nike sees more opportunities to optimize its supply chain, which could lead to more one-off charges, like we saw this quarter. At the same time, they expect the help from these decisions to materialize during fiscal year 2027 and accelerate thereafter.

d. Balance Sheet

- $8B in cash & equivalents.

- Inventory -1% Y/Y.

- $8B in debt; 2.5% Y/Y dividend growth.

- ~0% Y/Y share count growth.