Table of Contents

1. Nu (NU) – Detailed Earnings Review

Read my Nu Deep Dive here to learn about the company in detail.

a. Key Points

- 2026 will be an “investment year.”

- They plan to accelerate global expansion in the next 4-6 quarters.

- Now the largest financial institution in Brazil by customer count.

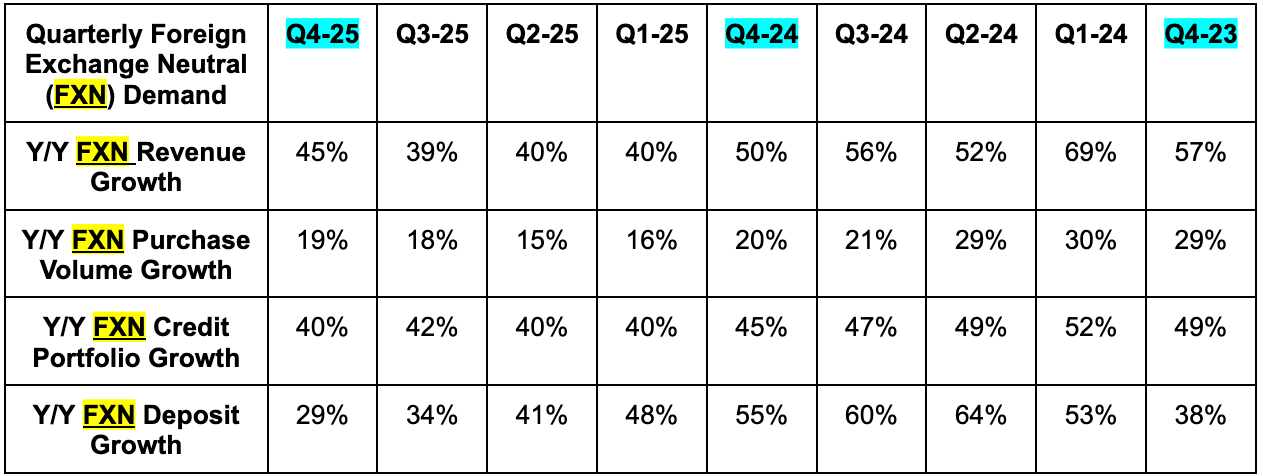

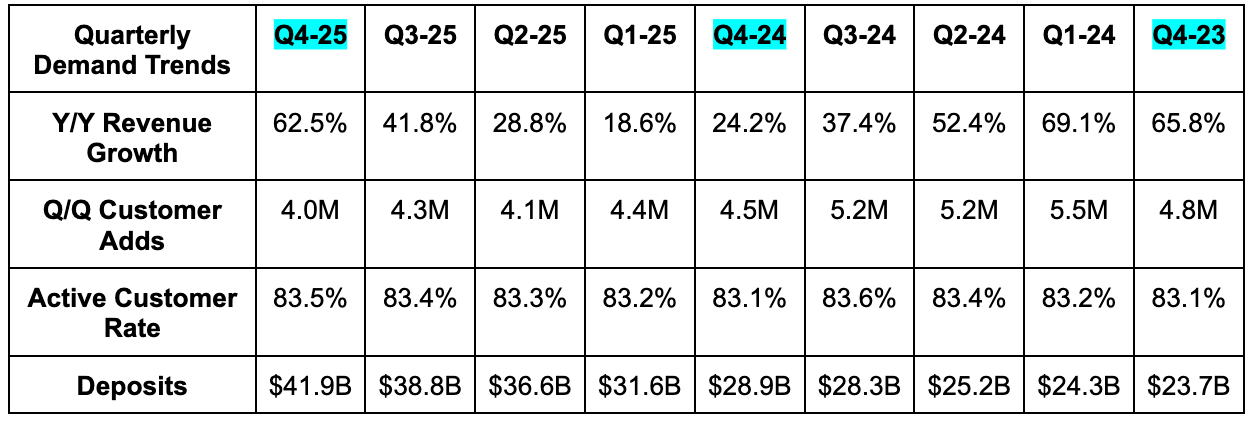

- Nice acceleration in Y/Y foreign exchange neutral (FXN) growth compared to Q3.

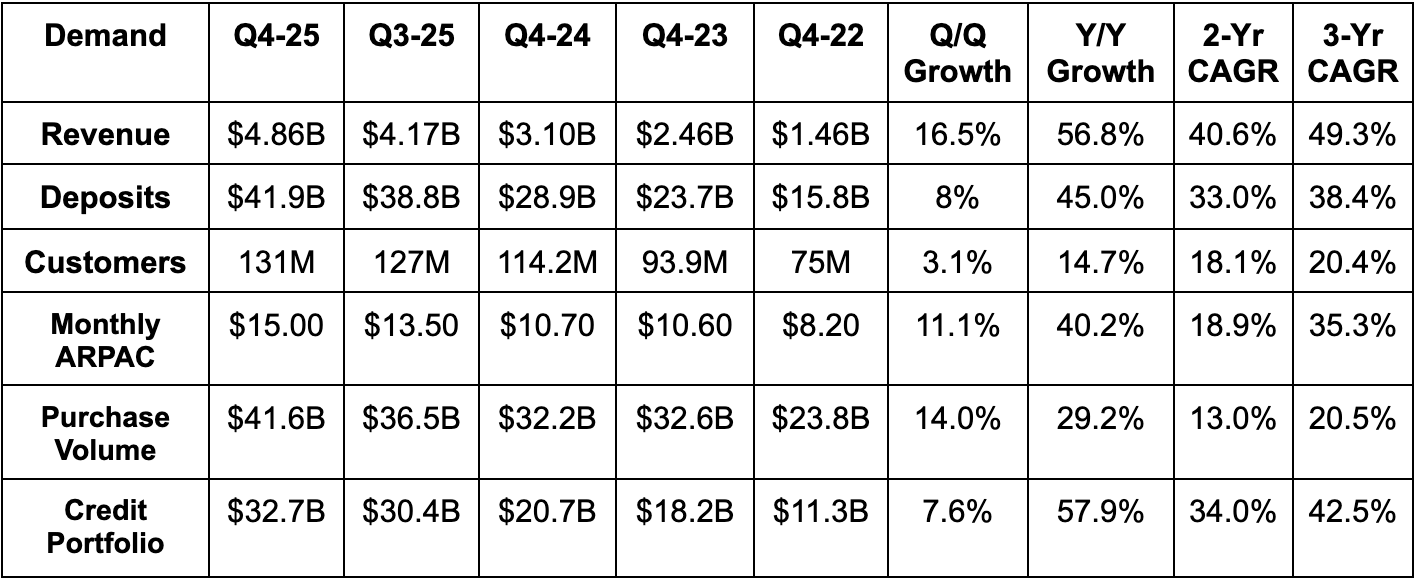

b. Demand

- Beat revenue estimate by 6.8%.

- 45% Y/Y foreign exchange neutral (FXN) growth was well ahead of 41% growth expectations.

- Met customer estimates.

- Met deposit estimates.

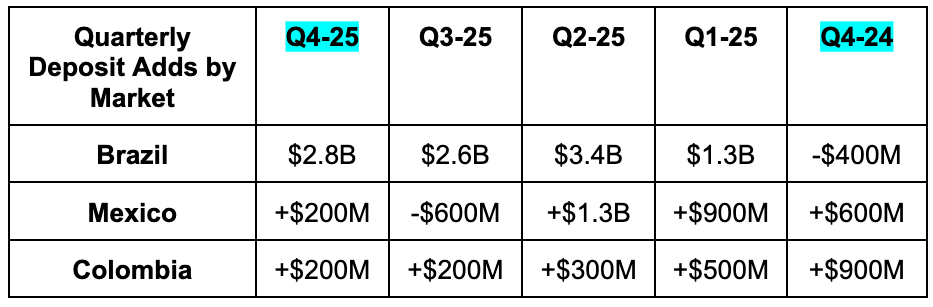

It was good to see deposit growth in Mexico turn positive once more. As a reminder, last quarter, they cut deposit yields paid to focus on monetization and margin a bit more than solely pursuing growth. They built a large base of customers and deposits and felt they were in a strong position to shift the prioritization slightly to profitability.

NU is now the largest private financial institution by customer count in Brazil. And despite ongoing rapid growth in that country, its active customer rate remains at a best-in-class 86%. It already has 62% of the adult population in its customer base in that market and doesn't think it's close to realizing its ceiling. At the same time, growth there will be more and more dominated by cross-selling and average revenue per active customer (ARPAC) gains rather than new customer growth. Speaking of ARPAC, there continue to be clear reasons to believe $15 is just the beginning. NU's most mature cohorts are well over $20 in ARPAC, and incumbents are at $40. All it needs to do is keep introducing more products and successfully scaling them, like it has consistently done over the last several years. This is not a matter of customers not wanting to use NU for more things. It's a matter of NU, not yet having everything people want. They're getting closer every single quarter.

In Mexico, NU now serves 15% of the population, while they crossed 11% of the population in Colombia, thanks to 70% year-over-year customer growth in that market. Colombian credit card approvals also spiked higher during the quarter thanks to success within its subscription-based credit card offering.

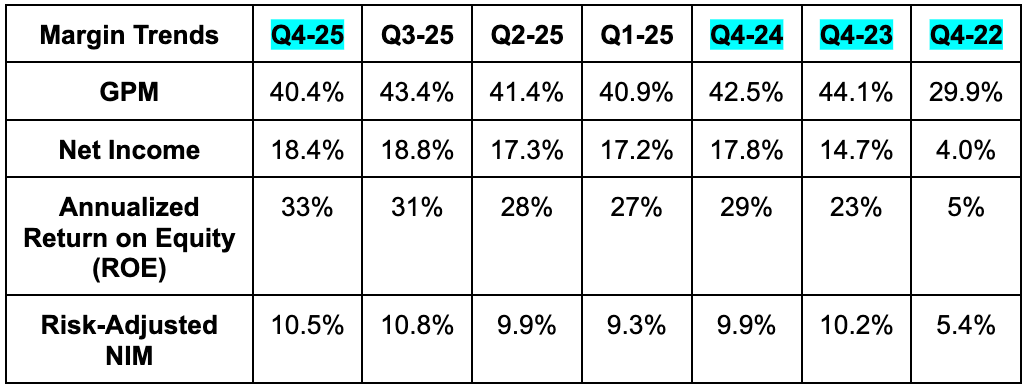

c. Profits & Margins

- Missed 43% GPM estimate.

- Missed net income estimate by 4%. Net income rose by more than 60% Y/Y.

- The tax rate was lower than expected due to a re-measurement in deferred tax assets, stemming from a change in policy in Brazil.

- Beat 10% risk-adjusted NIM estimate by 50 bps.