Table of Contents

a. Key Points

- Cloud growth was a bit lighter than expected.

- Reiterated 2027 guidance.

- Gross margin pressure being offset by operating expense discipline to enable operating margin expansion.

- Reiterated multi-year guidance under the new CFO.

b. Demand

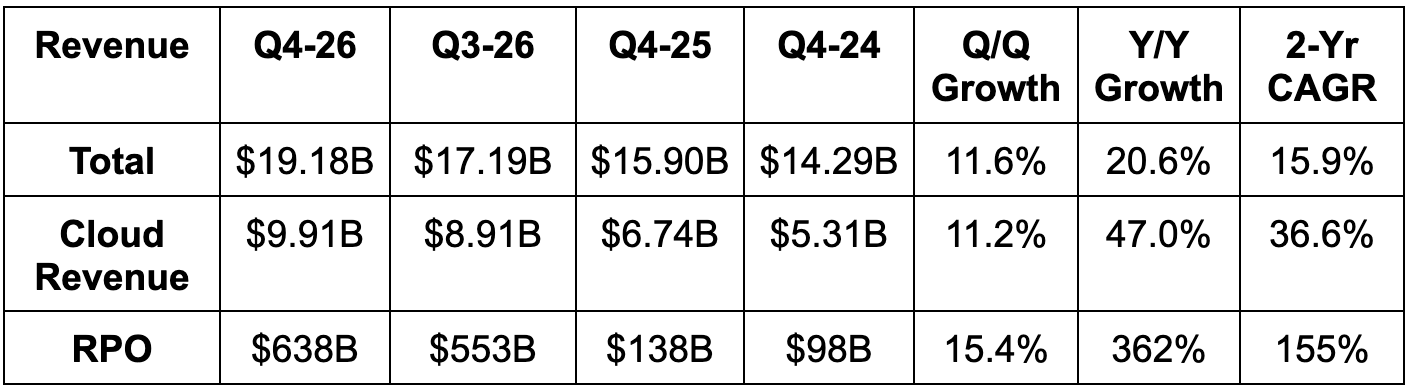

- Beat revenue estimate & guide by 0.5% each.

- Software revenue fell by 2% Y/Y due to ongoing customer migrations to cloud-based deployments.

- Cloud revenue missed estimates by 0.9%. 46% constant currency (CC) cloud growth missed 48% growth guidance.

- Beat remaining performance obligation (RPO) estimate by 8%.

c. Profits

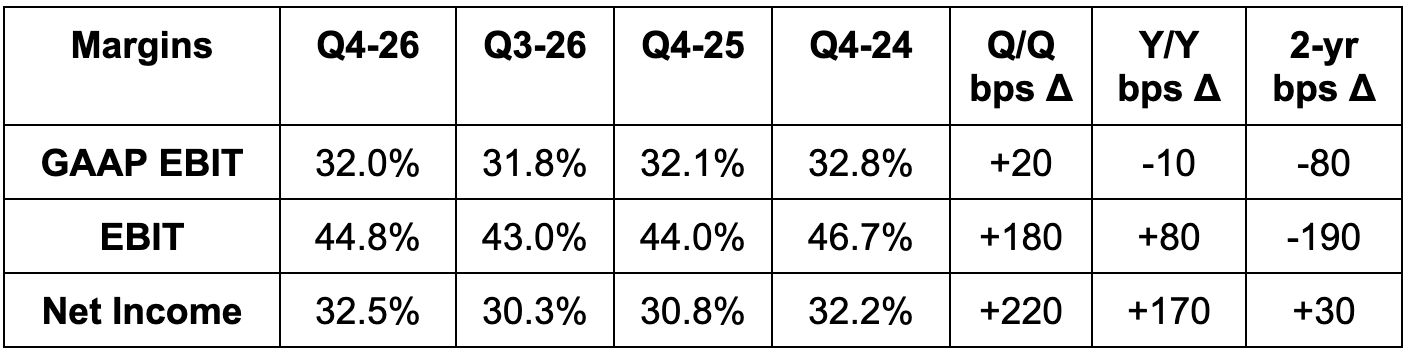

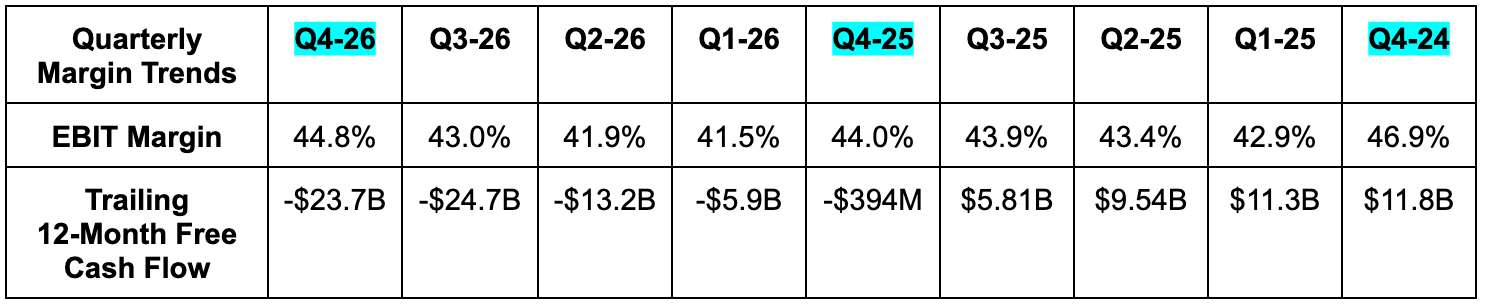

- Beat EBIT estimate by 4%. EBIT rose by 22% Y/Y.

- Beat $1.97 EPS estimate by $0.14 & beat guide by $0.13.

- EPS rose by 20% Y/Y excluding the impact of equity investment gains. It rose by 24% Y/Y when including this help.

- CapEx was $16.5B vs. $11.2B expected. FCF was -$1.9B vs. -$3.5B expected.

- GPM for the full year fell by 5 points due to ongoing infrastructure investments. EBIT margin was still able to expand Y/Y despite this challenge due to strong OpEx discipline.

d. Balance Sheet

- $32B in cash & equivalents.

- $130B in total borrowings.

- 1.5% Y/Y dilution.

- Oracle plans to raise $40B in a mixture of debt and equity for fiscal 2027 compared to $48B in 2026. This is to support their ballooning backlog and expectations for significant (and profitable) infrastructure growth ahead.

- CapEx for the year was $55.7B vs. $21.2B Y/Y. They expect that to rise to about $92.5B next year, which is far higher than ~$65B estimates. Notably, the massive $92.5B figure includes $22.5B in deals that involve prepaid contracts and bring your own hardware (BYOH) structures. These types of deals are becoming a much larger part of Oracle’s CapEx plans, as they move from 14% of total CapEx to 24% of total CapEx Y/Y. Importantly, this helps ease cash outlay requirements and improves cash collection cycles as well. This should continue, with the majority of their new backlog now coming from prepaid or BYOH formats.

e. Guidance & Valuation

- Reiterated 2027 $90B revenue guide, which beat estimates by 1.7%.

- This represents 34% constant currency growth.

- 2027 GPM will continue to decline due to all of the AI investments being made. They expect this pressure to dissipate when their large projects wrap up and start turning into more revenue.

- $8.05 2027 EPS guide met estimates.

- OpEx is actually expected to be down a bit Y/Y, which will allow EPS to grow by 18% Y/Y CC despite the material gross margin pressure.

- For Q1, 28% revenue growth guidance beat 27% growth estimates and $1.74 EPS guidance beat $1.69 estimates.

- Importantly, new CFO Hilary Maxson reiterated Oracle’s 31% 2026-2030 revenue CAGR expectation and the 28% 2026-2030 EPS CAGR expectation. There will be no changes to the operating plan or strategic priorities. More of the same under Maxson.

f. Call & Release

Capacity:

After adding 1.2 gigawatts in 2026 capacity, Oracle is expected to add close to 1.0 gigawatts in Q1 2027 as well. They’re sharply accelerating the pace of new supply coming online while still operating in an environment where demand is greatly exceeding supply. That’s why they have a 97.5% AI infrastructure utilization rate, as 92% of GPU contracts are being renewed (I thought it would be a tad higher) and the remaining capacity is getting quickly scooped up by other companies. That utilization rate should remain among the best-in-class, as 98% of their incremental data center capacity currently being built is already under contract. As mentioned, CapEx was nearly 50% higher than expected. This was not related to component inflation, but timing instead.

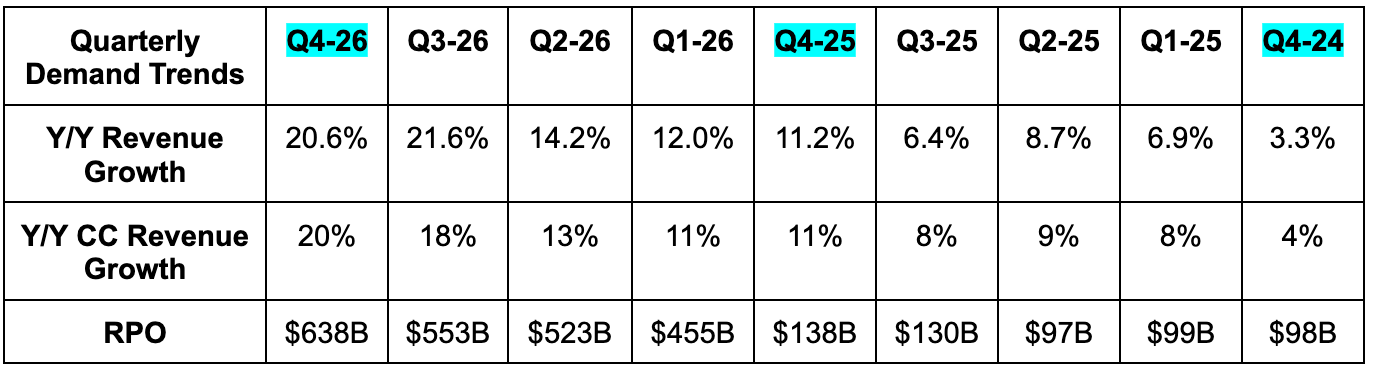

We got a slew of other important disclosures on the quality of the backlog during the quarter. Margins on new deals are stable or improving and customer diversification is also intensifying. During the quarter, they had 4 different customers contribute $8B in backlog. Finally, of the $638B, about $80B is expected to be recognized over the next 12 months, making up the vast majority of their $90B 2027 revenue target.

The Data Business:

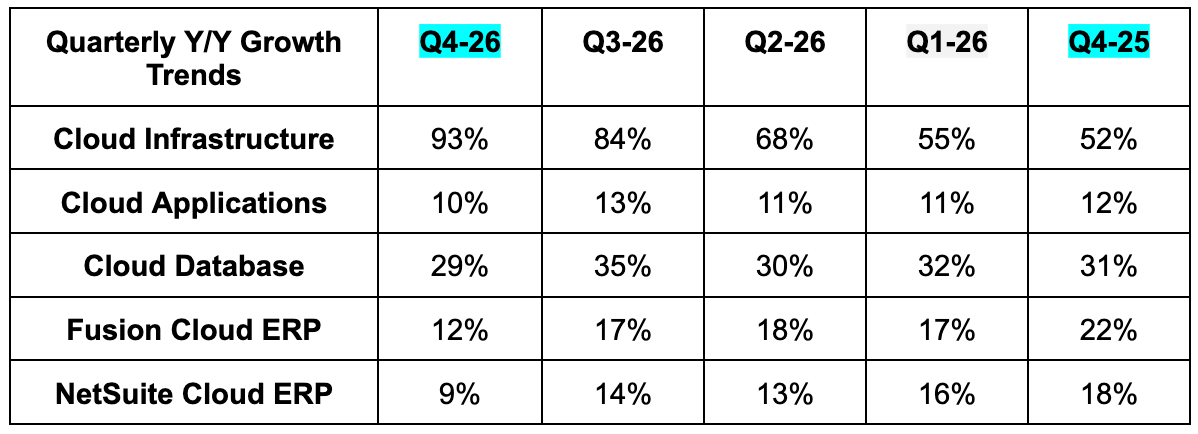

Within Oracle’s 29% cloud data business growth, multicloud revenue rose by a whopping 404% Y/Y, as this piece becomes a more important part of the segment and its “fastest-growing business ever.” Bookings for this also rose by 325% Y/Y, pointing to excellent momentum continuing. Innovation was cited as a big reason for this success, with newer launches like Oracle AI Agent Memory and Oracle Deep Data Security offered as two examples during the call. The first equips enterprise agents with needed data and context, which Oracle obviously has quite a bit of. The second creates well-defined and reliably enforceable database access rules for agents.

The Apps Business:

Existing stewardship over enterprise data makes Oracle a great enterprise software vendor for its customers as well. Everyone wants fewer vendors, lower data transfer costs and stronger interoperability. Oracle providing all database needs, applications and infrastructure in one place accomplishes this in ways that are similar to Microsoft.

One app segment where Oracle is particularly excited is healthcare. They are upgrading their Cerner software and patient care management system with AI features they expect to accelerate product growth back above 10% Y/Y for fiscal year 2027. Whether it’s improving patient service, expediting drug discovery or speeding up regulatory processes, Oracle is quite optimistic about where this business is heading, thanks to AI. More generally speaking, Oracle is seeing customers advance beyond AI app experimentation (for Oracle apps and apps built on Oracle) to commercial deployment, which is why deferred revenue rose by 16% Y/Y (6 points faster than overall app growth for this quarter). Interestingly, for the first time, leadership did talk about some contracts being delayed a few quarters ago by all of the “SaaSpocalypse” drama that has unfolded. On the other hand, that hesitant behavior has fully normalized and they think the overblown fears are gone.

Infrastructure:

The company remains confident in a 30%-40% AI infrastructure gross margin over the long haul as well as a return on invested capital (ROIC) in the “high-20s.” This expectation provides confidence in continuing to push ahead on aggressive fundraising and spending plans. Progress on its 5 large sites currently being built in the USA is all on or ahead of schedule. Importantly, the company utilizes variable component pricing contracts during times of uncertainty like we’re currently in. This is helping them maintain the margin trajectory in the infrastructure business despite soaring memory prices.

- Vodafone consolidated operations on Oracle’s infrastructure during the quarter in part because of having all three pillars (apps, data, infrastructure) in one place. To illustrate the appeal of this in action, cost for some workloads has already declined by 60% following the migration.

An Evolving Business Model:

Oracle is expanding outcome-based pricing models from a select group of sectors to every sector. Instead of charging on a per-seat basis, they’ll switch to more frequently charging for things like successful customer service interactions. They expect this to concretely show return on investment (ROI) for customers, while enabling the company to more effectively monetize the boom in agent-based activity. They’re still offering most of their AI innovation within existing customer products at no additional cost, which is why they market being the “quickest and most affordable way for customers to consume AI.” Now, the company is offering packages with higher levels of more advanced model access, which it will charge for based on outcomes. This monetization approach is consumption-based in nature. It just relies on that consumption actually yielding value, which Oracle is confident in delivering. Over time, they think adoption of these models will yield an overall acceleration in the apps business.