Alphabet (GOOGL) & Microsoft (MSFT) Earnings Reviews

Alphabet (GOOGL) & Microsoft (MSFT) Earnings Reviews

Exploring the results of two tech giants.

1. Alphabet (GOOGL) – Earnings Review

a. Demand

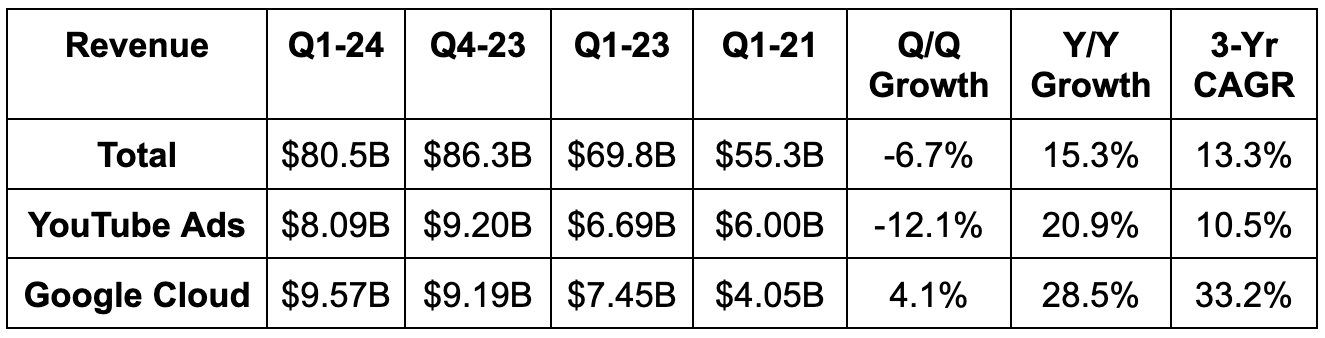

Beat revenue estimates by 2.3%. Its 13.3% 3-year revenue compounded annual growth rate (CAGR) compares to 14.9% last quarter and 18.4% 2 quarters ago.

Beat Google Cloud revenue estimates by 3.6%. Strong

Beat YouTube revenue estimates by 4.9%. Strong again.

b. Margins & Profits

Beat EBIT estimates by 15%. Rapid EBIT margin expansion was aided by lower severance and real estate charges vs. the Y/Y period. On an apples-to-apples basis, EBIT margin expanded by 390 basis points (bps; 1 bps = 0.01%) Y/Y.

Operating expenses (OpEx) fell by 2% Y/Y, but would have grown by a modest 5% Y/Y without this help.

Beat $1.51 GAAP EPS estimate by $0.38.

Missed free cash flow (FCF) estimates by 9.5% as capital expenditures (CapEx) continued to ramp to support GenAI and cloud infrastructure.

c. Balance Sheet

$107B in cash & equivalents.

$13.2B in longer term debt.

Share count fell by 2.3% Y/Y via continued stock repurchases. It added another $70 billion in buyback capacity this quarter.

Google also introduced its very first dividend. It’s a modest payout of $0.20 per share, but this does open the company up to more investment demand. Some investment vehicles exclusively invest in dividend-paying stocks.

d. Guidance & Valuation

Google told us that YouTube and Cloud will combine to exit 2024 with a $100 billion revenue run rate. Aside from that, all that Google offered was that CapEx would stay at or above the $12 billion Q1 2024 level. That’s nearly 100% higher than Q1 2023, as it invests aggressively in infrastructure (like everyone else).

Google trades for 24x 2024 earnings estimates. Earnings are expected to grow by 15% Y/Y for now, but I fully expect some modest upward revisions following the material EPS beat. Other commentary on offsetting rising depreciation expenses will help there too. More on that later.

e. Call & Release

CEO Sundar Pichai’s 6 Layers of the GenAI Opportunity:

Pichai spent the bulk of his talk diving through what he views as the 6 pieces of GenAI: leading in research, infrastructure and innovation are the first three pieces. Leveraging its global product footprint, execution and monetization areffrom the rest.

To drive faster, more impactful research (and to innovate faster), Google continues to consolidate teams under fewer leaders. It lumped all AI model-building teams into the DeepMind AI research branch. It also combined all machine learning teams and consolidated platform and device groups. The cost efficiency and communication from these moves early on are driving improved product development too. More with less.

Gemini is another instrumental piece in its aim to lead the innovation race. As a reminder, Gemini is Google’s series of foundational models used across its suite of products. The February update to Gemini yielded best-in-class “long context understanding” among other foundational model players. Leading in a key performance benchmark like this bodes well for confidence in Google’s ability to compete in GenAI. Gemini’s multi-modal (can process info from multiple modalities like images and text) models are already being used by several large customers to improve their own workflows and operations.

Pichai is “pleased with Gemini and Gemini Advanced subscriptions” across app stores.

From a footprint point of view, Sundar sees Google as having the “best infrastructure for the AI era.” Its data centers are “some of the best performing and most secure and efficient in the world.” This architecture has been purpose-built for AI models since Google embraced being an AI first company in 2016. This is allowing it to rapidly debut AI models and algorithms that are enjoying 100x efficiency gains in just 1.5 years. It is committed to “making investments required to stay ahead” – just like we heard from Meta and just like you’ll hear from Microsoft in section 2 of this article. This means continued aggressive chip investments and CapEx staying at or above current levels for the rest of the year. For context, CapEx this quarter rose by 91% Y/Y. Google’s leadership explained this jump just like Meta’s did:

“So the increase in CapEx, as Sundar and I said, really reflects the opportunity we continue to see across the company.” – CFO Ruth Porat

Foundational models are quickly heading toward commoditization. The best way to compete in that future reality is to be the most efficient and lowest-cost provider out there — with the best first-party dataset. Google has the pre-existing scale and data to put it in a great position to lead. But? To keep leading, hefty upfront spend to support seamless and flexible capacity growth is vital. Bottlenecks will otherwise appear. It’s these investments that nurture economies (or queries) of scale and, for example, allow Google to cut search generative experience (SGE) query costs by 80% since inception. SGE directly pulls from Gemini to more conversationally surface answers to queries. Google is now implementing this (as many of you probably noticed) right in the core search process. For appropriate questions, with the help of Gemini, it is now populating answers above links in a conversational fashion. This is awesome for consumers and is already driving engagement and satisfaction gains. I wonder what kind of impact this will have on the media if consumers no longer need to click into other sites for answers to questions.

Circle to Search (circle a virtual item to essentially activate a direct link) was another example of how Google aims to lead in search.

Advertising (GenAI monetization):

There’s one more piece of Pichai’s GenAI vision to cover: monetization. That, for now, will happen within its advertising business as it improves targeting and campaign management/automation.

Performance Max (PMAX) is Google’s campaign creation service with aggregated impression access. This past February, Gemini was (shockingly) added to PMAX to automate campaign creation and sharpen conversion predictions. Advertisers using PMAX’s asset generation tool are 63% more likely to design a “good or excellent” ad strength campaign; this classification yields a 6% boost to conversions. And if advertisers simply elect to allow Google to deliver automatically created assets (ACA), they’re enjoying another 5% lift to conversion and stable cost per impression. There’s more. Its demand generation product (called Dimension) is being used to uplift customer targeting and retargeting across all Google properties. With this, Lionsgate enjoys a “96% more efficient cost per page view.” Another good example of advertising and GenAI colliding is “Broad Match.” This uses Google’s foundational models to sharpen ad matching. Generally speaking, AI is already directly impacting return on ad spend (ROAS) for Google’s buyers.

Separately, like Meta, Google is enjoying a material boost in advertising revenue from APAC advertisers. This almost surely means Temu. Comps will get tougher with this item in Q3.

“We’re very pleased with the momentum in our ads businesses.” – CFO Ruth Porat.

A Q&A Quote About Investor Doubt Over Google’s Position in GenAI Search:

“But if you were to step back at this moment, there were a lot of questions last year, and we always felt confident and comfortable that we would be able to improve the user experience. People question whether these things would be costly to serve, and we are very, very confident we can manage the cost of how to serve these queries. People worried about latency. We feel comfortable there too. There are questions about monetization. And based on our testing so far, I'm comfortable and confident that we'll be able to manage the monetization transition here as well. It will play out over time, but I feel we are well positioned. And more importantly, when I look at the innovation that's ahead and the way the teams are working hard on it, I am very excited about the future ahead.” – CEO Sundar Pichai

Commitment to Efficiency:

Despite plans to keep aggressively leaning into CapEx to support capacity needs, Google reiterated its commitment to efficiency and continuing to optimize its cost base. Combining teams, as already mentioned, is an important aspect of that. While elevated CapEx will mean ramping depreciation expense, CFO Ruth Porat committed to expense discipline offsetting that margin headwind. That was great to hear.

Google Cloud Tools, GenAI & Infrastructure:

The strong revenue result was modestly helped by a larger AI contribution as well as strong Google Workspace usage and revenue per seat growth.

90% of GenAI unicorns are now Google Cloud customers as it continues to resonate with that cohort of innovators.

Debuted Imagen 2.0 — an AI text-to-image generator.

Debuted Google Vids as an app to easily create short-form video.

Continued driving advancements in its Axion Central Processing Units (CPUs) and Tensor Processing Units (TPUs) for machine learning.

YouTube:

YouTube Shorts monetization is a big focus area like Reels is for Meta. According to leadership, monetization levels for this content form doubled Y/Y. They also see no reason why it won’t eventually monetize just as well as traditional TV. That would be great news for all short-form video players.

YouTube debuted a “pause ad” format for YouTube TV. This shows brand and performance placements when a viewer pauses a show. So far, the performance of these ads is “commanding premium pricing.” Overall, YouTube TV now has 8 million paid subscribers and reached 1 billion watch hours per day this quarter. Watch time continues to rise for both YouTube TV and Shorts as it leads the streaming race over the past year (per Nielsen). It’s also very pleased with advertising demand momentum for these impressions. Great combination.

The Q/Q decline in YouTube revenue was due to 1 week of Sunday NFL ticket subscription revenue vs. 14 weeks in the Q/Q period.

YouTube TV will lap price hikes in May, which will make comps more difficult.

Final Notes:

Google One crossed 100 million subscribers.

Waymo is expanding into LA and Austin.

Google crossed 100 million music and YouTube premium subscribers.

f. Take

This was a strong quarter. The team is balancing hefty CapEx with strong income statement profit growth; the added context surrounding efficiency gains offsetting depreciation increases is important. The positive commentary on advertising demand bodes well for this company, and basically every other company left to report in the programmatic advertising space. It continues to turn Google Cloud into another quickly growing business with ample operating leverage. It continues to rapidly iterate in GenAI search. And? It continues to be one of the most iconic performers of the 21st century. Congratulations to shareholders on more profitable compounding.

2. Microsoft (MSFT) – Earnings Review

a. Demand

Beat revenue estimates by 1.6% & beat guidance by 2.3%. Its 14.1% 3-year revenue CAGR compares to 12.9% last quarter and 14.9% 2 quarters ago.

All three revenue segments were ahead of expectations.

Beat Azure FX neutral (FXN) growth estimate by 250 bps & beat guidance by 300 bps. Strong.

Commercial bookings rose by 29% Y/Y vs. 17% Y/Y last quarter and 14% Y/Y the quarter before that. This was much better than expected. Larger and longer Azure contracts were cited as the reason.

b. Profitability & Margins

Beat EBIT estimate by 4.9% & beat EBIT guide by 6.4%.

Activision Blizzard shaved 200 bps off of its EBIT margin. Operating expenses rose by 10% Y/Y or 1% Y/Y ex-Activision M&A.

Intelligent cloud EBIT margin was 46.8% vs. 42.9% Y/Y. Intelligent Cloud gross margin was 72% vs. 72% Q/Q & 72% Y/Y. It decreased ever so slightly (rounding error), but increased slightly when excluding a change in the estimate of the useful life of some infrastructure.

Productivity and Businesses EBIT margin was 51.8% vs. 49.3% Y/Y.

Beat $2.83 GAAP EPS estimate by $0.10.

Activision Blizzard reduced EPS by $0.04.

EPS rose by 20% Y/Y.

FCF rose by 18% Y/Y.

c. Balance Sheet

$80 billion in cash & equivalents.

$62.5 billion in total debt.

Dividends rose by 10.1% Y/Y.

Diluted shares rose slightly Y/Y.

d. Guidance & Valuation

Next quarter:

Revenue guidance missed by about 1%. This seemed to be entirely related to $700 million in incremental Q/Q FX headwinds. Without this headwind, revenue would have been slightly ahead.

Azure will maintain a 30%-31% FXN growth rate. This is despite some infrastructure capacity restraints that it’s currently dealing with.

Commercial bookings growth is expected to remain solid.

CapEx will again rise meaningfully Q/Q to support infrastructure investments. It’s getting aggressive here just like Alphabet and Meta are. For context, CapEx this quarter rose by 80% Y/Y to reach $14 billion.

Cloud gross margin should fall by 200 bps Y/Y and will fall slightly when excluding the tough comp impact from extending the useful life of some infrastructure.

EBIT was 1.1% better than expected, and Microsoft raised its annual EBIT margin expansion guidance from 150 bps to 200 bps.

For 2025, it offered some preliminary guidance. It sees 10%+ revenue and EBIT growth for the year, which keeps 14% Y/Y growth estimates for both on the table. Conversely, it also sees 100 bps of EBIT margin contraction Y/Y due to rising investments and depreciation costs to support infrastructure. This is technically 100 bps worse than expected, but 2024 EBIT margin will be better than currently expected, so the true miss is smaller.

e. Call & Release Highlights

GenAI:

Microsoft has taken the most aggressive approach to monetizing GenAI in the cloud and software space. GenAI is already propping up Azure’s overall revenue growth by a full 7 points as its Copilot offering builds meaningful traction. Copilot is essentially Microsoft’s GenAI assistant that is used across products like GitHub (software development), Azure, Office 365 and basically everything else that it does. Copilot is even being used for dedicated sales and customer resource management (CRM) automation. Overall, it’s used by 60% of the Fortune 500 today.

Copilot is also a foundation for creating more local, custom assistants for customers. Copilot Studio is essentially its new playground for customers to integrate their own data to create more relevant assistants. Studio enjoyed 175% Q/Q growth — off of a small base.

Love this visual?

My good friend Carbon Finance sends out a weekly visual newsletter with the most important infographics, insights, and insider trades.

It’s completely free and only takes 5 minutes to read.

Join 10,000+ investors and subscribe here now.

Azure:

Azure Arc is its platform to access applications and data in a multi-cloud environment. This is a key tool in removing cloud migration friction for customers like Dick’s Sporting Goods as most companies don’t want to use a single public cloud. They want to use multiple; this makes that easier. So? Migration frequency for Azure is accelerating partially thanks to Arc. All in all, Arc grew its customer count by 100% Y/Y to reach 33,000.

Impressively, 65% of the Fortune 500 already uses Azure AI while spend per customer here just keeps rising. These Azure AI customers are also using its data and analytics tools at a 50% clip. Popular cross-selling products here so far include Cosmos Database (DB), which is Microsoft’s fully managed, multi-model database service. Multi-modal here means diverse querying structures. Its next-gen data analytics framework (Fabric) is another popular example. The point is that Azure AI is directly creating better, incremental use cases to make other products more compelling for clients. This is why Azure accelerated Q/Q yet again while the demand and cloud optimization environment remained steady. Large deals, partially due to this increasingly strong cross-sell lever, are facilitating acceleration… as are market share gains. While it’s not just AI driving Azure’s growth, AI is improving demand for all Azure cloud services.

$10 million deals more than doubled for Azure Y/Y.

Azure is enjoying an acceleration in multi-billion contracts secured.

Cloud usage optimizations are still happening, but the bulk of the optimization wave is behind us.

GitHub:

GitHub is killing it for Microsoft. 90% of the Fortune 100 are clients. GitHub Copilot (automated coding) subscriptions rose by 35% Q/Q and revenue overall accelerated yet again to 45% Y/Y. Copilot subscribers like AT&T are accelerating usage based on this assistant as Copilot “bends the productivity curve.” From coding experts to dummies, its wide set of source code tools is freeing developers to create powerful software packages in a more automated, managed fashion. It’s now to a point where, for simple code creation, users can just tell Copilot exactly what they want to be written.

Productivity & Business Processes (Microsoft Teams, Dynamic, LinkedIn & 365 etc.)

Microsoft is rolling out a new version of Teams that is 2x faster while using 50% less memory vs. the old version. Y/Y usage growth for this tool continued to be positive. Teams crossed 1 million rooms for the very first time.

Office Commercial Product and Cloud Service growth was 13% Y/Y, thanks to 15% Y/Y 365 Commercial growth (4% for Consumer). Office Commercial Products specifically saw revenue fall by 20% Y/Y as clients continued to migrate to the cloud.

LinkedIn grew by 10% Y/Y. This was its 7th straight quarter of LinkedIn hiring marketplace share gains. The muted job market is, for now, diminishing the positive impact of this progress.

Dynamics Products and Cloud Services revenue rose by 19% Y/Y.

The Office consumer suite reached 80.8 million subscribers vs. 70.8 million Y/Y.

Bing now has 140 million daily active users (DAUs); the team said they took more share of overall search during the quarter.

Personal Computing (PC):

The PC demand environment was better than expected.

Activision was the source of the 61% Y/Y Xbox revenue growth. Organic gaming growth was 0% Y/Y. Still, this gaming segment outperformed expectations as Call of Duty performed very well.

f. Take

Like Google, Microsoft is second to none in terms of consistent execution and drama-less profitable compounding. And like Google and Meta, CapEx will continue to soar to support GenAI infrastructure. Still, margin preservation is strong, shareholder returns are growing and this company just keeps executing… quarter after quarter. Another great report. Enough said.

We find your summaries excellent Brad! Even though we operate solely from a chart perspective, you provide valuable information.