Amazon (AMZN) & PayPal (PYPL) -- Q1 2024 Earnings Reviews

Amazon (AMZN) & PayPal (PYPL) -- Q1 2024 Earnings Reviews

Digesting the Q1 2024 results of these two companies.

1. Amazon (AMZN) – Earnings Review

Amazon needs no introduction.

a. Demand

Beat revenue estimates by 0.5% & beat guidance by 1.8%.

AWS revenue beat estimates by 3.7%.

Advertising revenue met estimates.

Revenue growth ex-leap year would have been 11.3% Y/Y instead of 12.5% Y/Y. AWS growth ex-leap year would have been 16%. Unexpected foreign exchange (FX) headwinds reduced revenue by $700 million, which is why Amazon did not exceed the high end of its outlook (exceeded the all-important midpoint).

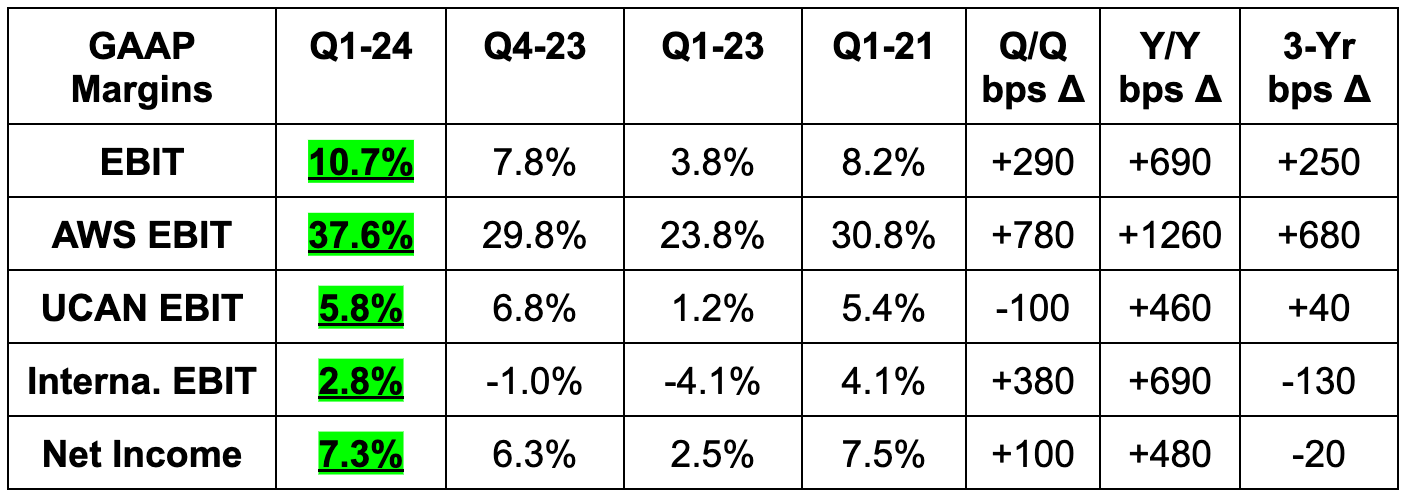

b. Margins & Profitability

Beat EBIT estimates by 38.5% & beat guidance by 53.0%.

Beat $0.83 GAAP EPS guide by $0.15.

c. Balance Sheet

$87B in cash & equivalents.

$58B in debt.

Basic shares +1.4%; diluted shares +3% Y/Y.

Amazon plans to pay down about $25 billion in debt by the end of the year. That juices EPS via reducing interest expense.

d. Q2 Guidance & Valuation

Revenue missed by 2.3%, which was partially related to incremental FX headwinds.

EBIT missed by 4.2%.

Europe was called weaker than the rest of the world.

e. Call & Press Release

GenAI:

In the last few Amazon earnings reviews, I’ve introduced the three layers of GenAI: hardware to support training and inference, models and consumer apps. To avoid redundancy for consistent readers, I’d point folks interested in reading that explanation to this article. Here, I’ll simply update Amazon’s progress across these layers. On the hardware front, it continues to work very closely with Nvidia; that won’t change. Still, Amazon is hard at work on building out its own custom silicon. Graviton is its basic computing chip, while (as we frequently discuss) Trainium and Inferentia are its training and inference GenAI semiconductors. Airbnb, Databricks and Meta’s Llama 3 are early customers here.

For models, Bedrock continues to resonate with developers for its broad lineup of partners like Anthropic, Mistral AI, Cohere and Meta. Tools like Model Evaluation (to pick the best one for you), question-answering guardrails and multi-step tasks are helping too. Leadership is especially optimistic about a new Bedrock tool called Custom Model Import. It’s a one-of-a-kind product that makes onboarding custom models more intuitive and rapid. This way, customers can use all of the compliance, security, hosting and other tools AWS provides before delivering a model or software package to runtime. This tool has become very popular to use alongside AWS SageMaker. SageMaker is its environment to build custom models on top of Bedrock. It’s similar to Microsoft’s Copilot Studio. Perplexity AI, trains models 40% faster with SageMaker vs. alternatives. Workday uses it to reduce inference latency by a full 80%. Overall, SageMaker Inferencing reduces foundational model costs by 50% and latency by 20%. These edges within inference matter as this area will eventually become the main part of the GenAI opportunity. After models are trained, they’re generally asked to constantly infer new insights (and only periodically re-train with new data).

Amazon Q was broadly released today. While Codewhisperer is its GenAI tool for general code writing, Q is purpose-built for AWS. Amazon thinks this is the best software assistant out there to generate, debug, and translate code. Q also offers a tool called “Agents,” which can perform a step-series of tasks like refactoring code and updating software. A developer conversationally asks it to perform a function, Q “analyzes existing code,” creates a plan and, upon approval, implements it. Pretty cool. Q Apps is another product to help developers build apps in the secure AWS environment — with more access to their data. Data is king for all cloud and customer applications… that may be even truer in the realm of GenAI. Models need to be trained; the best way to do that is with massive sums of relevant data. Enter Q Apps. Datadog, GitLab and the National Australia Bank are early users.

Amazon now has a few billion in annual GenAI revenue. This is a tiny part of its gigantic revenue base, but should be a high margin segment.

AWS:

We heard more of the same on AWS this quarter. Cost optimization trends have continued to fade and stabilize. It’s signing larger deals more quickly as migration appetite re-accelerates. Demand across all cloud apps for AWS was called very strong. And just like every other mega-cap, Amazon will invest into that strength. Being a global GenAI player requires massive infrastructure to ensure a lack of bottlenecks as use cases scale. Infrastructure is expensive. Considering this, Amazon said CapEx would materially grow in 2024 and called the $14 billion Q1 level a low point. This implies at least 15% Y/Y CapEx growth (likely faster). As a reminder, CapEx is expensed on the income statement as depreciation over the useful life of assets created. That is an EBIT and net income drag, which will greatly ramp up for Amazon in 2024. It added some needed detail here.

Leadership told investors that Amazon is at a point where it can balance growth and profits better than it was able to in the past. This ramping CapEx will not be Amazon throwing margin preservation out the window and accepting another long period of cash burn. This is it taking advantage of the far healthier position it finds its margins and balance sheet in to both walk and chew gum. There are margin tailwinds to offset this headwind, which we’ll dig into shortly. It didn’t say the tailwinds would make up for the added depreciation (like Alphabet did), but did assure us that it would keep a heavy focus on efficiency.

“We don’t spend capital without very clear signals that we can monetize it.” – CEO Andy Jassy

Customer wins and expansions included:

Siemens is using Amazon Bedrock.

Philips is using AWS Health Imaging and Bedrock.

New Anthropic collaboration to help highly regulated sectors comply with and adapt to GenAI regulation and trends.

PT Group is using Amazon Q to automate 12% of a software engineer’s job.

Audi is using SageMaker to build a GenAI customer service app.

Cost & Speed to Serve:

The fulfillment localization project through 2023 was the big cost to serve lever for Amazon. There’s still more to be done there, but most of the margin accretive work is complete. When combining this with more 3rd party fulfillment services, the flex driver program and 3rd party seller momentum, we are left with the exploding North American EBIT margin you can see above. Amazon thinks it can do much more to reduce cost to serve, and this is where the CapEx offset will mainly come from. Ads, i nternational market scaling and 3rd party seller momentum will help too.

In 2024, cost to serve improvements will come from a few increasingly important places. First, it’s time for the company to fully leverage its same day fulfillment warehouses around the U.S. It is investing meaningfully in sharpening inventory algorithms to better place demand closer to the end consumer. This means fewer miles to fulfill, lower cost, and happier customers as they get things faster. It’s a big part of 60% of Prime Member orders in Amazon’s 60 largest U.S. markets arriving same or next day (75% in Tokyo, Toronto and London). Another piece of this idea is combining fulfillment boxes when shipping multiple goods to single destinations.

Amazon also continues to quietly work on proprietary robotics hardware and software to automate and streamline in-factory tasks. Beyond these items, it is changing its seller fee structure to motivate usage of local facilities. This should raise the proportion of fulfillment handled by these more efficient warehouses.

Store Selection:

Amazon is pushing hard to make best-in-class selection even better. It added several popular brands like Sonos, Oura, Parade and a new luxury re-selling collaboration with “Hardly Ever Worn” in Europe. Adding items is one way to broaden selection, which makes it easier for 3rd party merchants to add product listings is another. This quarter, Amazon debuted a GenAI tool to make that listing process absurdly easy. Now, merchants copy and paste a URL to the website, upload it, and Amazon builds you a beautiful product description page. It already has 100,000 sellers using GenAI tools like these… and the opening pitch in the top of the first GenAI inning has not even been thrown.

Grocery:

A positive byproduct of shrinking delivery times is gaining customer purchase intent for daily essentials and groceries. If I can get a toothbrush or an apple from Amazon in an hour, why drive to CVS or Kroger? That’s the thinking here, and Amazon’s increasingly timely delivery capabilities are facilitating great perishable goods growth. It was always a decent player in non-perishable foods; now fresh food is on the table. Its formula of Whole Foods and Amazon Fresh stores (which are performing well per the team), plus world-class fulfillment could make Amazon a large grocery player down the road.

Debuted a newer $9.99 grocery subscription Prime benefit. This pays for itself after one use per month, which should fuel more momentum.

Will launch “Whole Foods Market Daily Shop” in Manhattan this year as a smaller Whole Foods store concept.

If you find this work valuable, I’d greatly appreciate you sharing it far and wide with your network. Spread the good word. It would mean a lot.

Advertising:

Advertising growth remained quite strong at 24% Y/Y on an FX neutral basis. This is still being driven mainly by sponsored listings, which have a long way to go in terms of growing ad load. Separately, streaming ad performance from the nascent Prime Video ad-tier is off to a great start. The added granularity of targeting and measurement available in the CTV world is driving strong ad demand early on.

This quarter, AWS debuted the Amazon Publisher Cloud. This uses AWS Clean Rooms to ensure an ad buyer can access all 1st party data (and Amazon’s) in a safe and secure environment. This, paired with enhanced audience segmentation and campaign planning, should continue to bolster targeting and returns.

International:

EBIT inflection reflects progress across mature and developing markets.

Remains highly confident in all new markets eventually becoming profitable.

New availability zones coming in Saudi Arabia, Mississippi and Mexico.

Other:

Kuiper is almost ready for a commercial beta test.

Added same-day prescription delivery in 2 cities with 10 more coming in 2024. Added more Eli Lilly drugs (including in obesity).

Prime Video will get its first NFL Wild Card game next January.

Launched Ring Battery Doorbell Pro.

Zoox, its self-driving robo-taxi, is expected to debut later this year. It just got a California Public Utilities Commission Driverless Autonomous Vehicle Pilot permit. Quite the mouthful. It will soon operate in Las Vegas too.

f. Take

The quarter was excellent. All of the AWS commentary was positive while pretty much everything else was too. Ramping FX headwinds powered the next quarter guidance miss, which is one of the least concerning reasons out there. Additionally, the aggressive CapEx guide was all but inevitable.

Amazon is the king of e-commerce and the largest member of a three-headed cloud monster. Its leading position in two highly compelling structural growth markets shouldn’t be taken lightly. I expect far more profitable compounding in the years ahead; I expect Amazon to remain near the top of my portfolio for a long time. More of the same… solid print…. next.

2. PayPal (PYPL) — Earnings Review

PayPal is world-famous for its branded online checkout button. It enjoys dominant merchant adoption share and is actively expanding into commerce/discovery. It also offers the third largest white-label processing platform in the world (Braintree), and owns Venmo too.

a. Demand

Beat revenue estimates by 2.4% & beat revenue guidance by 2.7%.

Revenue growth on an FX neutral (FXN) basis was 10% Y/Y.

Beat total payment volume (TPV) estimates by 2.8%.

Demand growth enjoyed a 1 point boost from Leap Day, but that was surely already in consensus expectations.

Met active account estimates.

Mix shift to larger merchants and rapid Braintree growth continue to negatively impact take rate.

Beat roughly flat Y/Y transaction margin dollar growth guidance with 4% Y/Y growth delivered. Branded checkout growth, Venmo improvements, a smaller drag from non-core projects and strong interest income due to Y/Y rate volatility all helped. More sensible Braintree pricing and margin-accretive cross-selling have not yet begun to impact things.

b. Profitability and Margins

PayPal stopped excluding stock-based compensation from non-GAAP margins this quarter. The change makes non-GAAP income statement margin comps irrelevant. “Old net income” uses the company’s previous method of excluding stock comp (SBC). “New net income” includes the cost. GAAP EPS rose by 27% Y/Y. Non-GAAP EPS under the old method grew by 20% Y/Y to $1.40. As you can see below, new net income leverage is faster, so making the change sped up earnings growth a bit this quarter. More on that later.

Beat $0.78 GAAP EPS estimate by $0.05 & beat guidance by $0.13.

Beat $1.22 ex-SBC EPS estimates by $0.18 & beat ex-SBC guidance by $0.23. Estimates were based on the old net income methodology, as that’s how PayPal’s initial 2024 guidance was set up. It had always planned on changing the structure this quarter.

Non transaction-related operating expenses (OpEx) fell by 2% Y/Y. This was due to previous restructuring, expense discipline and marketing timing.

c. Balance Sheet

$17.7 billion in cash, equivalents & investments.

$11 billion in debt.

Share count fell 5.5% Y/Y.

d. Guidance & Valuation

Annual Guidance:

Raised annual $3.60 GAAP EPS guide by $0.05.

Raised annual non-GAAP EPS growth estimates from flat to mid-to-high single digit growth. Importantly, this includes 3 points of help from the SBC account change. This was still a material raise without that help, but more like 3 points of growth instead of 6 points.

Guidance technically fell from $5.12 to about $4, but this was solely due to the accounting change. It was an apples-to-apples raise.

Raised transaction margin dollar growth guide from 0% to slightly positive for the year.

Maintained annual free cash flow (FCF) guidance & maintained buyback guidance.

Branded growth should be consistent through the year. Take rate reductions will be less noticeable this year.

Transaction margin growth will be fastest in the first half of the year, as PayPal will lap revenue gains from interest rate volatility in the back half. This is also due to expectations of one-off loan loss benefits not recurring.

The guidance continues to assume that all new projects have “very limited” positive impact on results. Per Chriss, these projects are “not built into the rest of the year.”

Next quarter revenue guidance missed by 0.6%.

PayPal trades for about 16x non-GAAP earnings under its updated methodology (12x under old method). Earnings are expected to grow by about 6% this year.

e. Call, Presser & Presentation

Realigning Disclosures & Incentives — for the Better:

Last quarter, I praised the new earnings disclosure format for PayPal. It’s more transparent, gives me context and is more neatly organized. This quarter, we can turn our attention to another positive disclosure change. Again, PayPal is now including stock compensation as an expense in non-GAAP margins.

Why do I love this? Because it hints at management seeing stock comp cuts as a real source of operating leverage. It gives them an easier profit starting point to grow from, along with another tool for accelerating that growth. And? PayPal plans to switch a large chunk of stock comp to cash comp this year, which confirms that idea. Finally, it’s also tweaking employee comp and incentive plans to better align with transaction margin dollar and EBIT growth. Love it.

Progress:

New CEO Alex Chriss inherited a mess at PayPal. Checkout flows were antiquated and stitched together with heavy, clunky integrations. The asset base was bloated, random and lacking focus. The employee and overall compensation incentives were not friendly to shareholders. Well? That’s all now changing. The company has rapidly accelerated the pace of product innovation and is quickly reorganizing its strategy to focus on core areas. The theme of this call was brisk progress, renewed energy and emboldened expectations… with several reminders that this will be a process that takes time to play out. Let’s unpack how they’re doing in each of the main areas mentioned.

“We see clear opportunities for operational improvements across our large enterprise, small business and consumer businesses, including Venmo, and in driving more efficiency across the organization. But it will take time to prudently drive a meaningful and sustainable transformation… we will leave no stone unturned.” — CEO Alex Chriss

Rapidly Accelerate Pace of Product Innovation:

First, PayPal Fastlane is showing obvious signs of being a high value product debut. Fastlane is effectively a single sign on (SSO) brought to guest checkout. With it, guests can easily speed through purchases if they’ve ever shopped at one of PayPal’s millions of merchant accounts. PayPal can also re-target relevant promotions and products towards Fastlane users without a PayPal or Venmo account. That should be a compelling top-of-funnel growth outlet.

For now, this is in beta testing with a sizable cohort of large merchants. So far, the launch is creating a low double digit lift in guest conversion rate with strong demand from the rest of its merchant base. This will be broadly released later in the year. Why does this matter? Fastlane is a clear example of PayPal better leveraging its databases to create better customer experiences. 60% of checkout online is still guest checkout. This allows those guests to be immediately recognized (thanks to PayPal’s scale) far more frequently to sidestep manual data entry and friction. It creates incremental delight in the checkout experience to increase brand and PayPal account consideration. PayPal has the first party data to uniquely add value to the checkout ecosystem. It’s finally doing so. It sees this as the best guest checkout on the market, and I agree. Considering that, it will aggressively price the product to drive more share in 2024 before normalizing its pricing approach thereafter.

In other checkout innovation news, it’s cutting out password requirements and will launch a brand new mobile checkout later this year in a push to juice conversion. It’s also currently in the process of modernizing its overarching tech stack. They’re currently taking “15 years of legacy integrations to build a more modern architecture for modern integration” and onboarding. That update won’t be as concretely visible from a user interface point of view as its back-end focused in nature. But it will be wonderfully impactful. Why?

This work will allow PayPal to cut steps and requirements for merchant onboarding. It will allow PayPal to expeditiously move its merchants to its latest product offering; the old team took weeks upon weeks at a time just to migrate a few of them. This will mean PayPal moves faster, iterates more constantly and has a far higher portion of its merchants on its latest checkout product. That change fosters easier Fastlane, Venmo and PayPal cross-selling for private label customers. The modernization will facilitate constant checkout updates, rather than some grand annual event. It will make PayPal far more competitive in the tough e-commerce checkout category. This is how PayPal will remove crippling operational bottlenecks to accelerate pace of progress.

Shifting Strategy & Focus — Braintree & PPCP:

Braintree was the main part of the conversation here. With the roughly 10% marketshare Braintree has built, Chriss and PayPal are confident they can begin to “price to value” rather than solely competing via undercutting competition. Per Chriss, PayPal’s auth rates and up-time are both best in class, and that would certainly command real pricing power in a commoditized space that usually lacks it. A lot of these merchants are currently attending a conference in California where PayPal is showcasing all of the incremental value it’s working on delivering there. It sees clear appetite for Braintree clients to purchase high margin software add-ons like Hyperwallet and other tools. For example, Draftkings added PayPal’s Fraud Protection Advanced (FPA) product this quarter.

PayPal Complete Payments (PPCP) (basically Braintree for smaller merchants) is now in 34 countries. The low-and-no-code merchant tools it introduced this year to ease onboarding and PPCP go-to-market are working; 7% of PayPal’s total small merchant volume is now running through PPCP. And again, having merchants on its latest software (which PPCP is) means far easier software and branded checkout cross-selling. It’s absolutely vital; it’s now a reality. PPCP clients are using 4 products on average, churning at a lower clip and delivering a 100% revenue per account uplift vs. its sunsetted product. Per Chriss, the old team “took eyes off the ball and priced us out of competing” here. Despite that, PayPal commands a top share of global SMBs, and Chriss is determined to repair fragile relationships and extend that lead.

Shifting Strategy & Focus — Xoom and Venmo:

Xoom was interestingly another focus area. There were rumors that PayPal was looking to sell the asset, but that’s not the case. It thinks it can be a big piece of the international remittance market. Xoom has been stagnating for years due to lack of focus. It’s now re-aligning fee structure and using the newer PayPal Stable Coin (PYUSD) to offer customers fee-free transfers. That should be a very popular feature for users.

The consumer app interface also got a refresh to more obviously and intelligently surface products for users to enjoy. This should help the near-future mobile checkout upgrade realize its full potential. The new interface is making things like debit card usage more intuitive, which led to 38% Y/Y growth in first time debit card users in Q1. That is notable. The debit card is a 3% cash-back tool with strong PayPal unit economics. The value prop is there and the returns are there. Time to lean in. These users are delivering a 20% rise in revenue per account, yet just 4% of its base has them today. Chriss is determined to push that number higher and doing so could be quite material to results.

For Venmo, it’s focusing strongly on effective monetization. Just like for PayPal, it’s making the rest of its non-peer-to-peer (P2P) product suite more visible. This includes a debit card, which enjoyed 21% Y/Y new user growth this quarter. Debit card vs. P2P-only users deliver a 600% boost to revenue per account. Chriss spoke on the issue of 80% of Venmo funds leaving accounts within 10 days. That is a massive missed opportunity to collect more interest and more transaction revenue on the $18 billion in inflows in enjoys PER MONTH. Frustrating… but also exciting. The debit card is a big piece of fixing this issue, along with more checkout adoption, merchant profiles and marketing tools. Venmo leads the P2P market share race with users who have 22% more disposable income than the average American. The potential here is simply massive. Now go capture it.

Regulation:

Proposed late fee caps from the Consumer Financial Protection Bureau (CFPB) would have about a near-term 3% impact on PayPal’s earnings growth. This headwind is not currently baked into its annual guidance! PayPal sees several levers to pull to shrink that impact to 1.5% by the end of the year and further thereafter.

Demand Growth Metrics:

Credit revenue continues to fall due to business loan conservatism and loss rate normalization on the consumer lending side.

f. Take

This was a good quarter. As I’ve been saying, PayPal is not Meta. It cannot snap its fingers and turn things around on a whim. There was much more to fix here, longer time to value on the fixes and more uncertainty over how impactful the fixes could be. To me, this quarter delivered all of the subtle greenshoots that I wanted. A raise to transaction margin expectations with guidance still sounding quite conservative… obvious signs that Fastlane will be a great, differentiating PayPal product… robust volume growth… an important Braintree software cross-sell and talks of pricing to value… continued branded checkout stability… hints of strong pent-up demand for financial services…. fixing Xoom.

This is a beast of a turnaround project for Alex Chriss. PayPal’s product suite has been neglected for years, and competition has caught up. PayPal’s brand, data and trust edges were not being utilized, but now they are. While I expect it to take a few more quarters for investor optimism to see what I’m seeing, he’s doing all of the right things. He’s fixing PayPal a bit faster than I thought he could. And? I resumed adding to my stake on Tuesday, using Match Group as the source of funds.