An Announcement & News of the Week

An Announcement & News of the Week

Announcement; Netflix; Bank of America, American Express & Discover; Tesla; Intuitive Surgical; Meta; SoFi; Amazon; Market Headlines; Macro; My Portfolio

To Stock Market Nerd Readers & Friends -- A Major Announcement:

After thousands of pages of regular, rational, reliable, in-depth & free stock analysis, Stock Market Nerd newsletter will be going to a paid subscription model on June 1. I have spent the last four years building a record of high quality research, strong performance, blunt honesty & hard work. I have loved every minute of it and I truly appreciate the passionate interest from each and every one of you.

I have 2 things to say to all of you:

Thank you.

Keep reading & subscribe.

Here's how things will work:

You will no longer see any ads starting June 1st. News of the Week will continue to be published every Saturday, with a change that I think you’ll all love. News of the Week is going to become “Remaining News of the Week.” More high-profile earnings reviews will be sent mid-week. Major news coverage for investor days, fed press conferences, M&A etc. will also be sent mid-week more frequently. Remaining News of the Week will feature everything not yet covered.

The first section of each weekly article will often be entirely free to give new readers a sense of what they can consistently expect. Additionally, short pieces of some of the other sections explaining the "what happened" will be free. Full analysis will be placed behind a paywall. Working through implications, context and opinions (so the majority of the newsletter) will be pay-walled. The occasional earnings review for immensely popular firms like Tesla or Microsoft will also be free; Twitter, Threads, Instagram and other similar content will always be free. I will no longer share holdings and transactions on social media.

Subscription Tiers:

Tier one ($25/month) - This includes all of my articles: the weekly news pieces, deep dives, earnings reviews, & a new quarterly portfolio outlook article concept. Paid subscribers will get all Stock Market Nerd content sent to their inboxes.

Tier two ($20/month) - This will include contextualized transactions (& my updated portfolio plus performance vs. benchmarks) sent in real-time. I will field comments, questions and concerns from paid subs on transactions in a timely fashion.

These can be bundled for $35/month.

I'm deeply excited by this opportunity and to keep delivering in-depth research for many more years to come. The next 6 weeks will be spent putting the systems in place to ensure this transition is smooth. I’ll also be switching to Beehiiv as part of this process. No action is needed on your end, as you’ll be automatically moved over to the new email list. Cheers to continuing to work my butt off for you. Onwards & upwards.

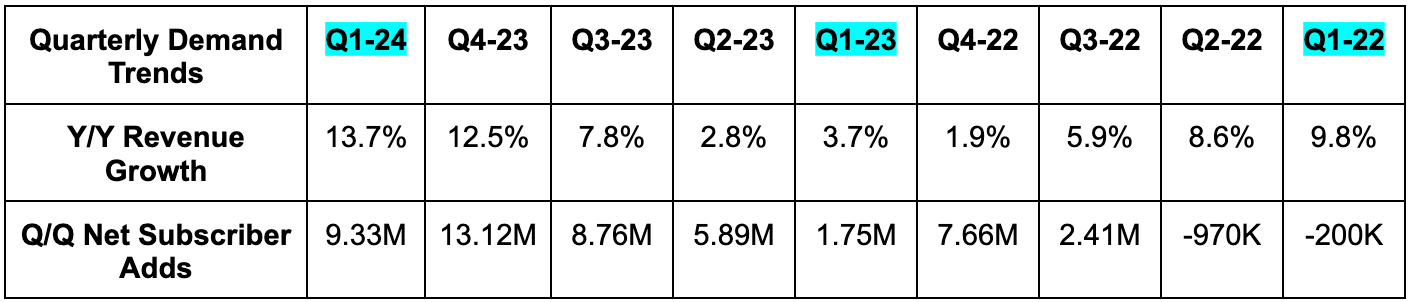

1. Netflix (NFLX) – Earnings Review

a. Demand

Beat revenue estimates by 1.0% & beat guidance by 1.4%.

Revenue growth was 18% Y/Y on an FX neutral (FXN) basis. The large gap between actual growth and FXN growth is related to a 75% devaluing of the Argentine Peso.

Crushed subscriber estimates by 94% or 4.5 million. This was also “better than expected” according to leadership. It no longer offers specific guidance on that metric.

Average revenue per member (ARM) rose 1% Y/Y & 4% Y/Y on an FXN basis.

Going forward, Netflix will no longer disclose total subscribers on a quarterly basis; it will instead disclose concrete annual revenue expectations, like it did this quarter. Per the team, its new add-an-extra-member feature and advertising growth levers are making subscribers a less important indicator for revenue growth. It was highly important at the beginning of the Netflix journey when subscribers served as a leading indicator for future financial success. Now, as a more mature company increasingly focused on optimizing monetization of current members through maximizing engagement, it’s not as valuable of an indicator. That’s how Netflix explained the change during the call and in the letter.

That’s what the team says, but I am certain there will be skeptics saying this is due to expectations of slowing member growth. While I always prefer more disclosures, and while total subscriber count is a great metric to track overall engagement potential, I really don’t think anything nefarious is going on here. Netflix has a stellar team with a fantastic track record and it does a better job of sharing engagement progress throughout the year than most. It will also still update us on subscribers when it reaches major milestones.

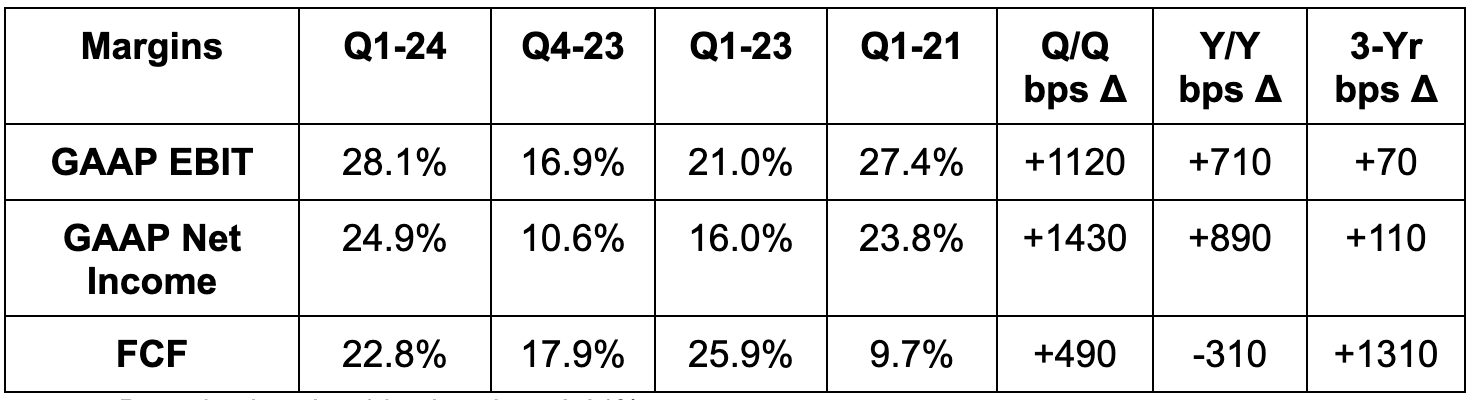

b. Profitability

Beat GAAP EBIT estimates by 8.5% & beat guidance by 8.7%.

Beat $4.52 GAAP earnings per share (EPS) estimates by $0.76.

Beat free cash flow (FCF) estimates by 16.3%.

Aside from outperforming subscriber growth, timing of content spend aided the profit beats this quarter. For GAAP EPS, $131 million in foreign exchange (FX) re-measurement helped by about $0.30. Still a strong beat excluding this non-operating boost.

c. Balance Sheet

$9.9 billion in cash & equivalents.

$14 billion in debt ($800 million current).

Basic shares fell 2.4% Y/Y.

Diluted shares fell 2.9% Y/Y.

There’s an update to the Netflix capital allocation philosophy. It’s removing the requirement to hold more than two months of cash on the balance sheet as a prerequisite for repurchasing shares. This is in response to its now comfortably investment-grade credit status. It also backed off from the $10-$15 billion in gross debt commitment and flexed an existing credit revolver from $1 billion to $3 billion.

“This will bolster our access to liquidity, and enable us to improve our cash efficiency, over time. We also expect to refinance our upcoming debt maturities and we don’t currently have plans to lever up to buy back stock as we value balance sheet flexibility.” – Shareholder Letter

d. Guidance & Valuation

For the second quarter, revenue guidance was missed by a modest 0.4%. Growth for the quarter is expected to be 16% Y/Y and 21% Y/Y on an FX neutral (FXN) basis (again due to Argentina). The firm’s EBIT guide was 3.3% better than expected, while its $4.55 GAAP EPS guide was $0.13 better than expected. It also guided to adding fewer subscribers Q/Q and modest FXN revenue per member growth. Most of the Q2 and 2024 growth for Netflix will be driven by more members, with little impact from price hikes.

For the full year, revenue guidance also missed estimates by a modest 0.4%. Its guide represents 14% Y/Y growth at the midpoint. It raised its EBIT margin guidance from 24% to 25%, which implies an EBIT guide 4% ahead of expectations. It reiterated its $6 billion FCF guidance, which missed by 4.3%, as the sell-side was looking for a small raise. It continues to expect up to $17 billion in annual content spending.

Netflix trades for about 30x 2024 earnings with a ~30% forward 3-year earnings CAGR expected.

“We will work hard to sustain double digit growth over the long haul… we’re committed to growing margins every year. We see a lot of runway to continue to grow profits and margins over the long term.” – CFO Spencer Neumann

e. Call & Letter Highlights

2024 Priorities:

Netflix will continue to do whatever it can to drive engagement. It knows this means higher retention, more advertising revenue and more subscribers – and it’s delivering. This quarter, despite account sharing restrictions that reduced users per member, engagement per member was stable Y/Y. If you make great content, the people will come and they will stay. And so? When Netflix leads the world in Oscar nominations for yet another year while dominating leaderboards for streaming shows and films, it’s no wonder why engagement is so solid.

In 2024, that engagement push will increasingly feature live programming (including some sports), unscripted content, gaming and even a Stranger Things play. As Netflix loves to remind us, the “Netflix Effect” already leads to songs, books, fashion trends and travel destinations storming back onto the scene seemingly out of nowhere. It clearly has a massive base of fiercely loyal and passionate fans, and it’s planning to give these viewers even more to consume in 2024. The entertainment giant wants to capture more of the remaining 90% share of TV viewing hours that it does not yet possess. Creating broader value to accomplish that feat should mean more pricing power and continued best-in-class churn rates – while maintaining strong operating leverage. This company is executing on all fronts.

Advertising:

Netflix’s advertising tier maintained rapid expansion this quarter, with 65% Q/Q growth. That follows 70% Q/Q growth in each of the last two quarters. More than 40% of its new members are going with ads; that matters dearly considering ad buyers’ most frequent request is more scale to reach more eyeballs. Netflix is getting there quickly.

It also needs to build-out better targeting and measurement tools for these advertisers. It’s partnering with Kantar and Nielsen, among a few others, to achieve this. Regardless, there’s a long way to go in building out the services and capabilities needed to be best-in-class here. Disney and Hulu are considered best-in-class at the moment, and I think that has a lot to do with the Disney/Trade Desk partnership. In my view, a similar partnership to complement Netflix’s work with Microsoft Xandr makes all the sense in the world. Full disclosure: I am a shareholder of The Trade Desk.

The phasing out of its basic ad-free plan in Canada and the U.K. is going as planned. Netflix is pushing lower-priced, ad-free subscribers to either choose ad-supported or to pay more for an ad-free experience. With these changes, it can become indifferent to which tier a subscriber chooses as revenue contribution should be roughly the same over the long haul. For now, as Netflix continues to work on tooling and scales the offering, it is a small headwind for revenue per member.

Streaming Industry & Programmatic Advertising Hint:

Netflix included a great chart in its letter that shows a stable-to-rising share of TV viewing hours. But perhaps more interestingly, it shows the rising share of streaming as a percent of viewing hours from December to March. That’s fantastic news for all players in the programmatic advertising space; streaming is the largest, most broadly-enjoyed structural tailwind in that market.

f. Take

I thought this was a great quarter for Netflix. Conspiracy theories will arise on the disclosure changes, but if they keep compounding at a 10%+ clip with leverage, I don’t think shareholders should really care all that much. For now, we have a company that is successfully broadening its content offering and catering to more people while expanding margins. It’s growing Y/Y share of a fiercely competitive market and sees a long runway to keep doing so. Great company and a great quarter in my view… regardless of the stock’s reaction.

My friends at Savvy Trader have some great new tools to share. I may cover a lot of companies during earnings season, but I definitely don’t cover them all. If you’d like transcripts, estimates, breaking news & more, give it a look.

2. Bank of America (BAC), American Express (AXP), Discover Financial (DFS) – Bank & Credit Earnings

Two things are true about this week’s batch of key credit earnings. More lagging indicators are still showing signs of notable deterioration as Y/Y comps continue to be difficult amid worsening macro and normalizing credit metrics. Conversely, provisions and reserve commentary from ultra-prime underwriters and less prime underwriters was actually mainly encouraging.

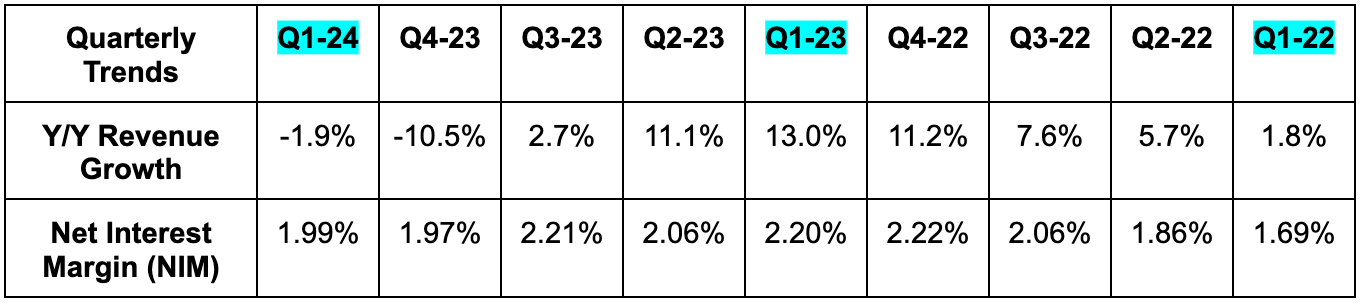

a. Bank of America

Results:

Beat revenue estimate by 1.6%.

Q4-23 revenue was hit by FDIC and Bloomberg Short Term Bank Yield (BSBY) index termination charges.

Slightly beat return on equity (ROE) estimates with a 9.40% ROE vs. 9.35% expected.

Slightly missed $0.76 GAAP EPS estimates by a penny.

Q4-23 profits were also hit by FDIC & BSBY charges.

Net Interest Margin (NIM) was expected to contract Q/Q with net interest income (NII) headwinds like seasonal income tax payments, but strong credit pricing discipline led to the positive surprise.

Balance Sheet:

$909 billion in average global liquidity sources vs. $854 billion Y/Y.

$296 billion in long term debt vs. $284 billion Y/Y.

$1.91 billion in average deposits rose 0.9% Y/Y. Internal expectations called for modest Y/Y declines in deposits.

$1.05 billion in average loans & leases rose 0.6% Y/Y.

Book value per share came in at $33.71 vs. $31.58 Y/Y. Tangible book value per share was $24.79 vs. $22.78 Y/Y.

Paid out $0.24/share in dividends vs. $0.22 Y/Y; diluted share count fell by 1.8% Y/Y.

Guidance:

BofA continues to expect Q2 to be its lowest quarter for NII generation. It’s still expecting three 2024 rate cuts and a 5.0% unemployment rate vs. 3.8% today. It sees expenses trending down throughout the year as well.

Credit Metrics:

Provision for credit losses came in at $1.3 billion vs. $1.1 billion Q/Q & $931 million Y/Y. The increase was driven by commercial real estate. Despite the rise, Bank of America released $179 million in credit reserves (meaning it thinks it needs fewer reserves to cover expected future losses) “due to a modestly improved macro outlook” per CFO Alastair Borthwick. Really good to hear.

But what was even better to hear? That the company expects a peak in net charge-offs for both its consumer and commercial businesses this quarter. That will further help with provisions for credit loss improvement, in addition to the reserve releases. Bank of America sees early-stage card delinquency trends improving on the consumer side. For commercial, more distance from front-loaded charge-offs within commercial real-estate is the biggest reason for optimism there. For now, total net charge-offs (the more lagging indicator piece of this equation) continue to rise and are $1.5 billion vs. $807 million Y/Y. About 2⁄3 of this is from consumer banking and higher credit card losses. This is due to more fragile macro and overall credit normalization. Credit card loss rate was 3.62% vs. 3.07% Y/Y. Commercial net-charge offs also rose due to commercial real estate office challenges. Overall net charge-off ratio was 0.58% vs. 0.45% Q/Q & 0.32% Y/Y.

Allowance for loan & lease loss ratio was 1.26% vs. 1.27% Q/Q & 1.20% Y/Y. This fell Q/Q as allowance for credit, loan and lease losses all modestly fell. Finally, non-performing loans and leases (NPL) ratio was 0.56% vs. 0.52% Q/Q and 0.38% Y/Y. This diluted the progress in allowance for loan and lease loss ratio, but only partially.

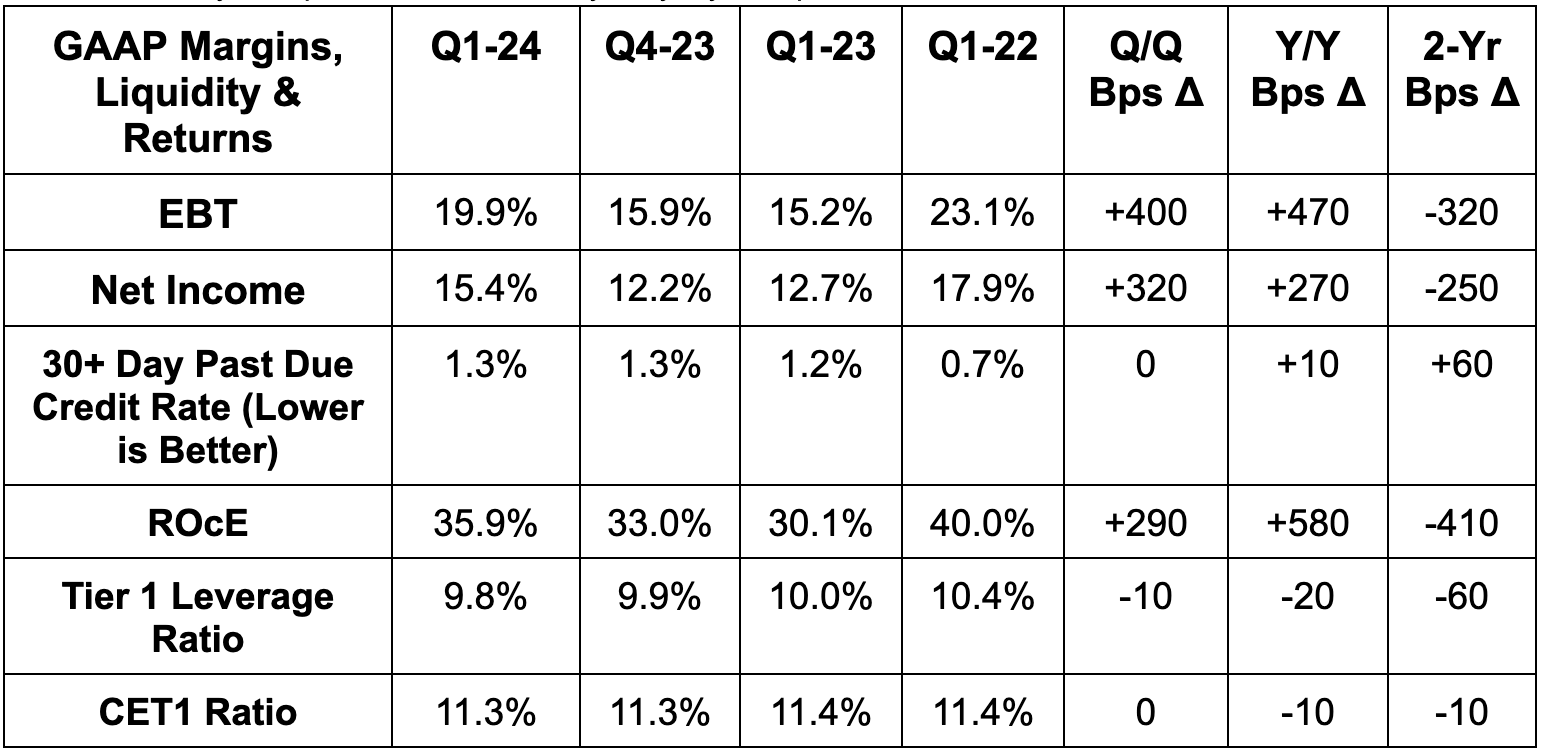

b. American Express (AXP)

Results:

AmEx barely beat revenue estimates by 0.1%.

Beat pre-tax (EBT) earnings estimates by 10.2%.

Beat $2.96 GAAP EPS estimate by $0.37.

Beat 30.9% return on equity (ROE) estimates by a robust 340 bps.

Balance Sheet:

$54 billion in cash & equivalents vs. $41 billion Y/Y.

$60 billion in card receivables minus reserves vs. $57 billion Y/Y.

$121 billion in loans minus reserves vs. $105 billion Y/Y.

$134 billion in customer deposits vs. $121 billion Y/Y.

$51 billion in total debt ($2 billion is current).

$37.79 in book value per share vs. $32.84 Y/Y.

Guidance & Valuation:

The company reiterated guidance of 10% Y/Y revenue growth and 15% Y/Y EPS growth. Both growth rates are about 1 point better than expectations. This doesn’t include an expected Accertify asset sale, which will likely prop up GAAP EPS due to the expected gain.

AmEx trades for 17x GAAP EPS with EPS set to grow by 14% Y/Y in 2024.

Credit Metrics:

American Express caters to a more affluent credit community than most. Due to this and its strong underwriting, it continues to enjoy strong credit health, with expectations of that remaining the case.

Overall principal net charge-off rate was 2.1% vs. 2.0% Q/Q and 1.6% Y/Y. This is still below 2.2% pre-pandemic levels.

For the corporate portion of this metric, its charge-off rate is 0.5% vs. 0.8% pre-pandemic.

For loans specifically, principal net charge-off rate was 2.3% vs. 2.1% Q/Q and 1.5% Y/Y.

For card receivables principal net charge-off rate, AmEx reported 1.7% vs. 1.7% Q/Q and 1.9% Y/Y.

30+ days past due as a % of total loans rose from 1.1% to 1.4% Y/Y, but for card receivables, it fell from 1.4% to 1.1% Y/Y.

The net interest yield on its loans was 12.0% vs. 11.7% Q/Q and 11.3% Y/Y. While delinquencies continue to modestly rise as expected, AmEx continues to price risk effectively.

“We expect to see this delinquency and charge-off rates remain strong with some continued modest increases in 2024.” – CFO Christophe Le Caillec

Total provisions were $1.27 billion vs. $1.44 billion Q/Q and $1.06 billion Y/Y. The reserve build for AmEx was lower than in any of the previous 6 quarters, offering more signs of forward-looking credit expectations easing.

c. Discover Financial (DFS) Credit Metrics

Discover caters to broader credit bands (i.e. less credit worthy) vs. AmEx and Bank of America’s more affluent demographics. So we examine it to get the entire picture of the consumer from low to high credit scores.

Let’s start with the bad. Total net charge-off rate was 4.92% vs. about 2.70% Y/Y. Its recent vintages are showing higher delinquency levels as macro worsens and credit normalization plays out. Personal loan net charge-offs are also ticking briskly higher with that expected to continue near term.

The good news? Discover sees company-wide credit losses peaking in mid-to-late 2024. This compares to the commentary last quarter of losses peaking in the back-half of 2024. To me, that’s a reiteration, but you could make the argument that it’s a subtle upgrade to forecasts. It sees delinquency trends across the portfolio continuing to stabilize within its new cohorts. I’d still love to see the personal loan net charge-off rate peak, which did not happen this quarter as that rate rose by another 62 bps. This is more telling for players like Upstart, Pagaya and maybe Lending Club.

As a read through for SoFi specifically, this isn’t all that relevant considering SoFi’s affluent demographic. AmEx is the better hint.

Discover also saw provisions for credit losses rise by $395 million to $1.5 billion. This was due to rising net charge-offs, but that hit was encouragingly offset by a $410 million reduction in reserves built vs. the Y/Y period. Its expectations for credit performance are stabilizing.

3. Tesla (TSLA) – Some Thoughts

I don’t own Tesla shares. I would never even contemplate shorting Tesla shares. Tesla has been a hot topic in the news lately, and I wanted to offer my understanding of the current debate, without picking sides.

The margin trajectory from here is the most polarizing topic. First, there are some tailwinds it enjoys. Tesla continues to cut input costs per vehicle (by $3,000 Y/Y as of last quarter) & sees that trend continuing. Ramping up its new 4680 cell battery production will help a lot with scrap bills to cut costs too. Ramping capacity at newer gigafactories could be another boost depending on current demand levels. Its solar & especially its energy storage businesses also continue to find mainly consistent operating leverage.

But there are material margin headwinds to contemplate as well. Overall demand levels are currently challenged, which means less fixed cost leverage. Mix shift to lower-priced vehicles is a margin headwind today as well. Cybertruck costs are another issue as the production line hasn’t yet ramped (but costs have). That margin drag could also be more structural than some assumed, as early sales data from that model has not been stellar. Finally, Tesla continues to invest aggressively in AI and R&D to support its next-gen vehicle line-up. This, paired with weaker than normal sector demand, is hurting margins too.

The most controversial margin headwind, however, is the targeted price cuts across some models in some geographies. Tesla’s unmatched margin profile (both gross & net vs. all other EV programs) gives it the flexibility to profitably lean into consumer affordability. After all, higher rates mean higher interest payments and more expensive cars (all else equal). Optimists here will tell you Tesla is controlling its average selling price to counteract this reality for its consumers. They say that Tesla is willing to accept lower up-front margins today as it knows there are software up-sells coming in the future (like hopefully Full Self Driving (FSD)) to “harvest more profits” over time. Leadership has said the same thing. With tougher macro today, maintaining low sale prices makes finding demand amid the not-so-fun part of this auto cycle tougher for others. Tesla is using its competitive positioning to amplify this pain for its competition. That should mean stronger Tesla market share over time as headwinds abate & growth likely re-accelerates. That’s the bull case here.

Bears will say that Tesla is cutting costs and seeing margins tank due to intensifying competition across the sector (& poor macro). Especially in Europe and China, without the same tax benefits, skeptics simply think others are catching up, Tesla’s differentiation is shrinking and its pricing power is too. As of last quarter, market share trends were rising slightly in UCAN, flat in Europe and falling ever so slightly in China (where competition today is the most fierce). Most recently, ACEA reported the largest Y/Y decline in EU March sales in over a year.

And bears also have some new ammo with rumors of the postponed $25,000 mass market model plans. A shift in focus to robotaxi is far more speculative and will take far more time for potential revenues to ramp. If that's happening, investors believing in Tesla for its dominant EV share and margin profile may become a tad less bullish. Finally, some will say that Elon's antics and polarizing dialogue are turning some buyers off. These antics aren't anything new and I truly don't think that's a relevant factor here.

What do I think matters? It’s not Tesla suddenly finding a sharp recovery, more volume growth and a margin trough. That’s not realistic right now. What matters is where its current financial struggles are currently coming from. If this is macro-related, dip buyers right now could easily be handsomely rewarded over the coming years. If it’s more micro, and competition-based, they might be solely reliant on a distant future robotaxi to find capital gains. Which side is right? I will leave that for you to decide as this firm remains at the very top of my too hard pile.

4. Intuitive Surgical (ISRG) – Earnings Snapshot

ISRG makes robotic surgical systems to assist surgeons. It trains hospitals on the hardware itself, offers powerful data analytics on key performance indicators (like outcomes), and routinely allows for less invasive surgery overall. It dominates within this niche. Its largest revenue driver is the “da Vinci” system with “Ion” being its newer, faster growth hardware. It just got its latest da Vinci 5 system cleared, which unlocks many more minimally invasive procedures for usage.

Results:

Beat revenue estimates by 1.1%.

Beat EBIT estimates by 7.5%.

Beat $1.42 EPS estimates by $0.08.

Beat gross profit margin (GPM) estimates by 20 bps. Please note that mix shift to its Ion and new da Vinci hardware is a large gross margin drag. ISRG remains fully convinced that GPM will reach 70% in the future.

Balance Sheet:

$7.3B in cash & equivalents.

$1.3B in inventory & no debt.

Diluted shares +1.3% Y/Y; basic shares +0.9% Y/Y.

Annual Guidance & Valuation:

ISRG raised its annual procedure growth guidance from 13%-16% to 14%-17%. It reiterated GPM guidance of 67.5% and 13% Y/Y operating expense (OpEx) growth. More volume without more cost should lead to upward earnings revisions.

ISRG trades for 57x 2024 earnings and 63x 2024 free cash flow. Earnings are set to rise by 9.7% Y/Y with FCF expected to rise by 183% Y/Y following two consecutive years of deeply negative growth.

5. Meta Platforms (META) – Meta AI Release & WhatsApp

Meta debuted its latest version of Meta AI. This is its conversational GenAI assistant now built on Meta’s latest and greatest Llama 3 open-sourced foundational model. The assistant is infused directly into the search bar of Meta’s apps to give users more intuitive and powerful search and discovery tools. Queries are also sharpened by data sharing from both Google and Bing. Considering this could feasibly be used for commerce discovery and other traditional search use cases, that note was a bit surprising to me in a good way. The Meta AI assistant can now perform real-time content animation and image creation as well.

Meta AI is the “most intelligent free AI assistant” per Zuckerberg. It runs on Llama 3’s 8 billion and 70 billion parameter models, with the 70 billion parameter version already best in class in reasoning and math. Meta will continue to rapidly introduce new models and constantly improve its work here. For example, the 8 billion parameter Llama 3 model is already more powerful than the most dense Llama 2 model.

Meta is giving away Meta AI for free, so why is this relevant to its financial results? Better search means better content matching. Better content matching means more time spent on its apps. And? That means more advertising revenue. That doesn’t even consider the fact that this work will be a valuable piece of its chatbot customer service tools for paid business accounts within ecosystems like WhatsApp.

In other news, Apple removed WhatsApp from the Chinese app store. With Meta largely banned in that market, it is not material to its financial success.

6. SoFi (SOFI) – Miscellaneous

Galileo announced a new partnership with a business lender called Rapid Finance. Rapid did about $100 million in 2023 revenue, so it’s a very small company. Still, it is growing quickly and could maybe become more material for tech platform results down the road. For now, it won’t be material but offers good evidence of SoFi successfully expanding into business lending. It’s also great to see it as the Sponsor Bank for this new product. Together, the two will offer credit lines for merchant customers to draw at their discretion.

Forbes ranked SoFi Bank as the 5th best in the nation. It’s only a couple years away from securing its charter, yet only ranks behind customer service titans like USAA, which only caters to families who have served in the military.

SoFi’s long requested dark mode is being rolled out alongside its Zelle integration.

Do you love Twitter (sorry, not X) as much as I do? Do you only want investing-related content on that app? Do you get frustrated by all of the noisy content you scroll through to find the nuggets you actually care about? Same! Blossom is here to fix that. This is focused FinTwit meets serious investors meets portfolio tracking. It’s a thriving social media platform for us nerds and it just launched in the USA. It’s entirely free to use and something that I now post on daily. Check it out here and sign up. See ya there.

7. Amazon (AMZN) – Prime Growth & Another Bullish Sell-Sider

Amazon Prime reached 180 million members in the USA with 8% Y/Y growth – per Consumer Intelligence Research Partners. Concerns were building around 2022 and early 2023 about slowing growth here. Many creative reasons were used to explain short-term declines in membership. But the only reason we needed was the historically aggressive pandemic pull-forward and relatedly tough comps. Those tough comps have now been lapped and growth is magically accelerating. What a concept.

In other Amazon news, more sell-siders (DA Davidson and Truist this week) lined up to publish bullish notes on the company. Like all of the other notes we’ve covered recently (and as my investment case spelled out before all of them), profit estimates have not caught up to reality and Amazon is poised to outperform. The only issue here is that every sell-sider is saying this and they are all raising estimates. That raises the bar for success heading into the current quarter. Not relevant for the long term investment case, but relevant for the set-up for those of you utilizing other approaches.

8. Market Headlines:

TD Cowen sees Datadog (DDOG) comfortably beating earnings expectations this quarter following a bullish CIO survey that it ran.

For Shopify (SHOP), RBC channel checks and Morgan Stanley’s confidence in 20% revenue compounding for the next 6 years led to two bullish notes released this week.

Duolingo (DUOL) will be added to the S&P MidCap 400 index this quarter.

MercadoLibre (MELI) will hire 6,500 people this year in Brazil. That represents nearly 30% Y/Y growth in pace of hiring as it leans into that market.

Lululemon (LULU) is shuttering smaller distribution centers to consolidate into larger facilities. About 100 people will be laid off as a result.

Disney (DIS) received approval for Disneyland expansion from Anaheim’s City Council.

UBS sees continued stabilization in cloud spending for Amazon, Microsoft and Google. It thinks the three will modestly outperform expectations this quarter. The EU also cleared Microsoft’s proposed $13 billion OpenAI investment.

9. Macro

Consumer & Employment Data:

Core retail sales M/M for March rose by 1.1% vs. 0.5% expected. This compares to 0.6% last month.

Retail sales M/M for March rose by 0.7% vs. 0.4% expected and 0.9% last month.

Housing Starts in March sharply missed estimates. Existing home sales slightly missed expectations.

Continuing and Initial Jobless claim data was slightly better than expected.

Output Data:

The New York Empire State Manufacturing Index for April was -14.2 vs. -5.2 expected. This compares to -20.9 last month.

Industrial Production M/M for March was 0.4% as expected. This compares to 0.4% last month.

The Philly Fed Manufacturing Index for April was 15.5 vs. 1.5 expected. This compares to 3.2 last month.

In a speech this week, Powell acknowledged the pause in disinflation progress we’ve seen – especially in the Consumer Price Index (CPI) since January. He basically told us that this has pushed out rate cut expectations by a few months. Nothing about my take on the macro environment has changed from the last few weekly issues. (LINK)

I also wanted to chat very briefly about war’s impact on markets. I’m not even remotely an expert on war or geopolitics and want to stick strictly to my lane of investment in stocks. That is how I will frame the discussion as that is how I frame every discussion. While war is awful for all of those involved, while it’s anxiety provoking, saddening and upsetting, it is not devastating for Mr. Market. The stock market has a way of apathetically and coldly shrugging off encounters like the ones we are seeing today – after the initial shock factor has worn off. And regardless, this conflict has zero material impact on the long term compounding of the companies you or I invest in. These flare ups will continue to get significant attention and press, but when strictly viewing things through an investment lens, it will likely be much bark and no bite.

10. Portfolio

No transactions to report this week. I’m very tempted to cut Match and add to other holdings, but I’m committed to giving them one more quarter to show real signs of progress with Tinder top-of-funnel.

Congratulations, Brad! Interesting to see where you go from here! Onwards and upwards!

Surprised it has taken so long... Good luck!