Apple (AAPL) & Cloudflare (NET) Earnings Reviews

Apple (AAPL) & Cloudflare (NET) Earnings Reviews

Analyzing the data and commentary from these two earnings reports.

1. Apple (AAPL) – Earnings Review

Apple needs no introduction.

a. Demand

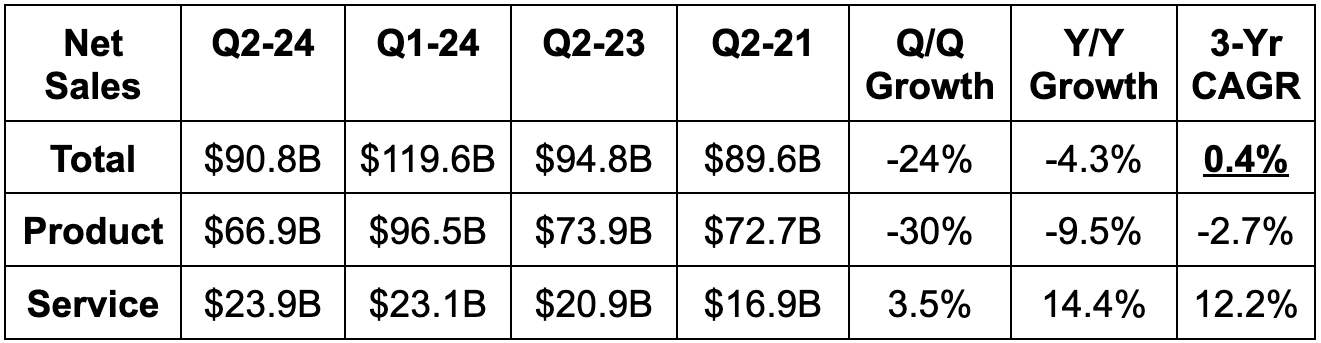

Beat revenue estimates by 0.2% & missed guidance by 1.6%.

Services growth of 14% Y/Y was much better than its 11% Y/Y guide.

Product revenue was light.

b. Profitability & Margins

Slightly beat GAAP gross profit margin (GPM) estimates & slightly beat identical guidance

Beat EBIT estimates by 0.7% & missed guidance by 1.8%. EBIT fell slightly Y/Y.

Beat $1.51 GAAP EPS estimates by $0.02. GAAP EPS was flat Y/Y.

Operating cash flow generation was $22.7 billion vs. $28.6 billion Y/Y.

c. Balance Sheet

$67B in cash & equivalents; $95B in non-current cash equivalents.

$105B in total debt.

Dividends were roughly flat Y/Y, but Apple just approved a 4% boost.

Share count fell 2.4% Y/Y. It added another $110 billion to its buyback program. This is worth about 4% of its gigantic market cap and represents a dollar figure larger than Bulgaria’s GDP. Casual.

d. Guidance & Valuation

Apple guided to low single digit revenue growth for next quarter. Sell-side was expecting 1.2% Y/Y growth, so I think we can call this a small beat. To me, “low single digit” means 1%-3% and so 2% growth at the midpoint (4.5% Y/Y growth on an FX neutral basis). It sees services growth remaining in the low double digits. Guidance implies that iPhone revenue will again decline Y/Y next quarter. Its gross margin guidance was 46% and in line with expectations, which means implied gross profit guidance was slightly ahead. GPM guidance assumes some memory input cost inflation. Taken together, and assuming the revenue guide means 2% Y/Y growth, EBIT guidance of $24 billion was in line. The guide assumes no change in macroeconomic dynamics.

Apple trades for about 24x-25x next 12 month (NTM) earnings with low single digit earnings growth expected over that time period.

e. Call & Release Highlights

Demand Overall:

Apple set a new revenue record in 12 countries this quarter. That list includes important growth markets like Spain, Mexico, India and multiple Middle Eastern nations. For product revenue specifically, the weakness needs more context. Apple is lapping a Q2 2023 period in which supply chain recovery unleashed pent-up demand. That unleashing added $5 billion to Q2 2023 iPhone revenue results. Last year’s pull-forward means this year’s tough comp. This is why iPhone sales fell 10% Y/Y. Excluding this atypical comp item, iPhone revenue fell by 0.7% Y/Y. iPhone revenue did grow in Mainland China, as it enjoyed the top two selling smartphones in that country (per Kantar research). Surprising, after all of the negative alt data we’ve seen. But? Alt-data is usually anecdotal and noisy. Outside of China, iPhone was the top seller in the U.K., France, Australia, Germany, Japan and (obviously) the USA. Per 451 research, this product maintained its 99% customer satisfaction rate.

Apple was asked about the China opportunity over and over again during the Q&A. Leadership remains confident in the opportunity and has several initiatives in place to improve performance in what it calls its most competitive market.

Outside of the iPhone, Mac and iPad both maintained 96% customer satisfaction rates; Mac revenue rose 4% Y/Y and iPad fell 17% Y/Y. Declines in iPad were due to comping over strong product launches. Wearables, Home and Accessories fell 10% Y/Y due to successful launches in the Y/Y period (just like with iPad). Active Install bases for ALL hardware products in ALL geographies set new records.

I get that many think hardware growth is going to be hard to find for Apple in the future. I don’t really agree as an innocent bystander. 50% of iPad buyers and 67% of Apple Watch buyers this quarter were brand new to the products. There is still a runway here to complement faster, higher-margin services growth. And hardware comps will get easier.

From a services point of view, the 14% Y/Y revenue growth metric was excellent. Apple Pay, streaming, brisk paid account growth and overall engagement strength all helped drive this outperformance. It expects this momentum to remain strong.

Year to date, revenue is roughly flat. This is being hurt by foreign exchange (FX) headwinds and one less week of sales vs. the Y/Y period. Apple could really use a growth re-acceleration in the coming quarters to make the growth multiples look a bit less steep vs. others. Fortunately, that acceleration is expected. Sell-siders see Apple exiting the year at +5% Y/Y revenue growth — with more acceleration thereafter.

By Geography:

The Americas revenue fell slightly.

Europe revenue rose slightly.

Greater China fell 9% Y/Y.

Japan fell 13% Y/Y.

Vision Pro:

Apple remained steadfast in its optimism surrounding this product. I’ve seen multiple 3rd party reports saying it’s cutting production targets due to underwhelming demand and high return rates. While that’s not ideal, it’s also not surprising considering this is the very first iteration of a new computing form factor. Building product-market fit will take time for Apple… just like it has for Meta. I envision headsets being mocked, criticized and disregarded until the technology is miniaturized enough to drive ubiquity. I demoed the Vision Pro, and it’s just not comfortable to wear for long periods of time. That will change as Apple and Meta make these headsets look more and more like a pair of glasses over time. When that happens (I think it will), the mocking will quickly shift to rapid adoption. Give it time.

50% of the Fortune 100 is now exploring how to build apps on this hardware.

Capital Expenditures (CapEx):

As is usually the case, we got a lot less color on CapEx plans compared to every other mega-cap. Apple can get away with this (Wall Street darling as it should be) and it makes sense to avoid oversharing when it can. It did remind investors that its broad supply chain does allow it to share some CapEx intensity with 3rd parties. This includes data center CapEx, and could help curb growth in this expense compared to others.

Margins:

Product GPM’s sequential decline was as expected. This is typical seasonality and mix shift-related. Favorable input cost dynamics helped to offset these headwinds. That’s encouraging to hear from such a giant corporation, given how important inflation dynamics are for today’s markets. Services GPM, conversely, benefitted from favorable mix shift and outperforming growth.

Other News:

CEO Tim Cook teased a product launch coming next week.

The Worldwide Developer Conference this year is when it plans to finally offer a little detail on its GenAI plans. It sees its ecosystem and silicon innovation setting it up for high probability success here.

f. Take

This quarter was somewhat underwhelming, with the iPhone guidance being the notable lowlight. It just goes back to the idea of expectations, sentiment and positioning mattering dearly for short term reactions. For traders, this is important. For long term investors like yours truly, it isn’t. This setup resembled Tesla’s more closely than Meta’s. “Better than feared” seems to be the early takeaway.

With that said, Apple is still king. It still has one of the most compelling ecosystems and moats on the planet. It still has an absurd amount of cash. It still has a long global runway. It’s still Apple. The buyback engine will manufacture a powerful earnings tailwind with no end in sight.

I will say that I really think the innovation engine here needs to pick up the pace to drive more decades of profitable compounding. Continued services growth will rely on continued hardware growth to create more active devices to up-sell. The new buyer dynamics and continued growth in overall install bases both point to that needed goal being attainable. Its fortress balance sheet also gives it the flexibility it needs to invest in that innovation. This was not close to its best quarter and was never going to be. What matters is a top line acceleration being delivered throughout the year. That’s what sell-side expects; that’s what I expect. We shall see.

2. Cloudflare (NET) – Earnings Review

Here, I’ll introduce Cloudflare’s product suite and niche. This will be review for readers well-versed in its product suite.

In essence, Cloudflare makes the internet faster and more secure. They have a massive global Content Delivery Network (CDN) to move traffic closer to the end user, which cuts web latency. They actively assist clients in optimizing traffic speed and consistency as well. It also has a suite of security tools to protect customers from Distributed Denial of Service (DDoS) attacks. This form of hacking aims to inundate and overwhelm networks with traffic. NET doesn’t sell physical firewall hardware, but instead a virtual, cloud-native “Magic Firewall” to supplant these hardware needs. That’s deeply resonating in 2024. It offers web application firewalls too for app-level security, while Magic Firewall is for network-level security. The closest cybersecurity competitor in public markets is Zscaler.

A Few Key Products to Know Aside from Those Already Mentioned:

Workers Platform is its server-less (so fully managed by Cloudflare) product suite for developers to build, maintain, secure and deploy applications. This allows for caching of content and apps across Cloudflare’s global network for faster delivery. Its newer Workers AI product allows developers to access models and infuse GenAI tools (like sentiment analysis) into Cloudflare-hosted apps and networks. Workers AI pairs seamlessly with its “Vectorize.” Vectorize offers a style of data querying that allows for visualization of patterns. Another key example of Cloudflare’s GenAI tools is its R2 product. This allows cloud workloads and data to be freely moved among public clouds with no tax. Key in a multi-cloud world. This is popular for model building and implementation as models are voracious users of data and data is routinely hosted in many clouds.

Cloudflare Access is its Zero Trust Network Access (ZTNA) program. Zero trust means that a user or device must be constantly verified (or never trusted). Cloudflare does this in a seamless manner to minimize user friction. It considers device type, location, usage patterns (or signatures) and other contextual clues to better authorize permission requests. This way, it knows when to block those requests or when to require more information. It then deploys a minimal privilege approach to ensure only the necessary permissions are granted to workers. Nothing more, nothing less. Zero Trust ensures an adversary can’t breach the most vulnerable part of a tech stack and move freely throughout it thereafter.

Secure Access Service Edge (SASE) platform is a term for how Cloudflare conjoins web performance and security use cases. This drives vendor consolidation, controls costs and augments performance. Cloudflare One is its overarching product bundle subscription combining its suite.

a. Demand

Cloudflare beat revenue estimates & beat its same guidance by 1.5% each. Its 40% 3-year revenue compounded annual growth rate (CAGR) compares to 40.9% last quarter and 43.2% 2 quarters ago.

b. Profitability & Margins

Beat EBIT estimates & beat identical guidance by 22.5% each.

Delivered 1 point of Y/Y leverage across all three operating expense (OpEx) buckets.

Beat $0.13 EPS estimates & beat same guidance by $0.03 each.

Beat free cash flow (FCF) estimates by 75%.

Network CapEx was 8% of revenue, and will likely be about 11% of revenue for 2024.

c. Balance Sheet

$1.7B in cash & equivalents.

No debt.

$1.3B in convertible senior notes.

Diluted shares +2.5% Y/Y.

d. Annual Guidance & Valuation

Reiterated annual revenue guidance, which met estimates.

Raised EBIT guidance a bit and met estimates. Reiterated that FCF would = EBIT for the year, which means it raised its FCF guide slightly too.

Raised EPS guidance by $0.03, which beat estimates by $0.03.

Next quarter guidance was ever so slightly ahead of expectations across the board.

Cloudflare called its guide conservative, which was due to geopolitical chaos around the globe. In the short term, it remains highly cognizant of these potential risks, which is why the team beat revenue estimates this quarter, yet merely reiterated the full year revenue guide. To me, this simply lowers the bar for outperformance through the rest of 2024. They love to beat every single quarter.

e. Call & Release Highlights

Go-To-Market:

The bulk of this call was spent on Cloudflare’s go-to-market approach. Considering I’m a nerdy numbers guy with a financial background, I loved every minute of it. Over the last 14 years, Cloudflare has obsessed over building best-in-class products and operationalizing them with scale. It sees its suite of products, across network security, data protection, content delivery and more, as leading the pack by a material margin. It will remain focused on maintaining that lead while adding a new focus area. Cloudflare wants to complement its product suite with a go-to-market approach that is also world-class.

“Cloudflare has always been powered by our relentless innovation engine. I’m encouraged by our progress in building a go-to-market engine that will also be the envy of the industry.” – Founder/CEO Matthew Prince

The new President of Revenue (Mark Anderson) and other senior-level hires were recently brought in to deliver on that objective. Early signs are quite strong. In March vs. February (when Anderson took over), applicants rose 56% M/M. And while Anderson will surely leave his mark on this organization, it’s not like the situation he’s entering is at all bad. Quite the opposite:

Cloudflare set a new record for large deals signed in the quarter, while it enjoyed a double digit Y/Y improvement in sales productivity. It sees this trend continuing due to a robust pipeline and new talent. Continued productivity gains have eliminated the sales efficiency issues Cloudflare dealt with last year; that progress is emboldening it to lean in. The company will accelerate the pace of new hires this year to maximize its market presence. In today’s cost-focused world, this likely made some short term-minded folks a little nervous. But with an opportunity this large… with structural tailwinds this strong… and with its reputation of building elite products… leaning in makes all the sense in the world to me. There’s no reason why Cloudflare’s go-to-market can’t be as powerful as other stand-outs like CrowdStrike.

Sales cycle length was stable Q/Q.

New business pipeline creation outperformed expectations.

Large customers are 67% of total revenue vs 62% Y/Y.

The Platform Play:

Well… consistent readers knew this section was coming. 2023 was the year of tech platforms and vendor consolidators standing out from the pack. 2024 looks to be more of the same. While this firm was once mainly a CDN (already defined), that is no longer the case. It beautifully laces in a bevy of use cases through its overarching SASE platform. Some of these use cases include domain services, CDN, network security, data loss protection etc.

This company has morphed itself into a powerful driver of cost savings and outcome improvements. And? The wins this quarter are simply the byproduct of this development:

Signed the National Cybersecurity Center in the UK (cyber authority there) to a 3 year deal. This was a highly competitive bidding process.

The Accenture channel partnership helped it land a 3 year, $40 million deal with a “leading tech firm.” It opted into Cloudflare One and basically everything Cloudflare sells.

Completed 6 proof of concepts to land a Fortune 100 financial services company. The efficiency gains from operating through a single agent and interface (with unmatched data compliance) helped it beat out several other competitors. It sees this as a domino for winning more whales in that sector.

An international energy firm signed a 5 year, $4.5 million contract for Cloudflare’s overarching SASE platform. If the buzz-words and acronyms are confusing, they’re all simply defined in the intro of this review.

Won a Fortune 100 government-sponsored financial services firm due to NET’s better resilience, performance and architecture. The customer, with NET, enjoys overarching visibility of its network through a “single pane of glass.” I repeat… a platform play.

Product Innovation:

Product news took a back seat to go-to-market and platformization. Still, the Workers AI tool, which helps developers run models in the Workers Platform, went live. This AI tool has 2 million developer users, while NET added Python as an integrated language, Hugging Face’s roster of models and Meta’s Llama 3 too.

NET debuted a server-less standard query language (SQL) database to more easily access insights. Finally, it introduced “Hyperdrive” within Workers AI. This allows any legacy database to plug into NET’s global CDN. This should drive faster, cheaper data querying. It’s working on its next generation of servers, which should foster hefty inference improvements.

f. Take

This was a great quarter in a fluid environment. The ugly sell-off after-hours is, to me, driven by traders getting picky and expecting a larger raise to annual guidance. The reiteration of the annual guide implies a small miss for Q2-Q4 considering the Q1 beat. This is one of the most expensive names in the market at 125x 2024 earnings and 20% Y/Y earnings growth expected. A hefty premium raises the bar for what is considered a good quarter and can lead to seemingly positive prints getting punished.

With that said, this is a very special company. Its pace of compounding should remain lofty for as far as the eye can see, and operating leverage remains in its early innings. I just candidly see better risk/reward elsewhere… but Cloudflare has ALWAYS been among the most expensive names out there. If you’ve decided you can look past that premium (and investors so far have been rewarded handsomely for doing so), then this quarter is not something to panic about. To me, I’d love to see more earnings growth to justify paying up for this elite organization. It’s in the same bucket as Snowflake for me.

Without the buyback AAPL would have sold off on these numbers

Dear Brad, two errors in the Apple part.

Apple Mac revenue was positive 4 not negative.

Apple Vision Pro is not uncomfortable if you fit it right. heheh