Introduction:

Duolingo (Ticker: DUOL) is an online language learning platform offering content to nearly 40 million monthly active users (MAUs) globally. The main product is its gamified mobile language learning app built for smartphones, but the company also offers a desktop version of its software for consumers and teachers. It was founded a decade ago in Pittsburgh by Luis von Ahn and Severin Hacker and has already eclipsed 500 million total downloads while employing 400 Duolingo team members. Today, the company offers lessons in 40 different languages.

Here I will present the investment case for Duolingo (Note: I intend to purchase shares of the IPO) and the available, pertinent information regarding this unique organization including:

- The Issue with Education

- Duolingo’s Solution

- Power in Scale

- The Market

- More Duolingo Products and Optionality

- Demand Growth

- The Margin Profile and Upside

- Balance Sheet Pre-IPO

- Leadership and Ownership

- Competition and Risks

- The Deal, Valuation and My Plan

- Citations

1. The Issue with Education

Education is systematically unequal, far too expensive, and somewhat ineffective -- not the greatest combination. According to the Economic Policy Institute, years of extensive research revealed what we all intuitively know: a person’s social class and wealth are the strongest indicators of their educational success. Because of this, the vast majority of the world is at a distinct disadvantage when it comes to accessing top quality education: some are swimming with the current, and some are swimming against it.

And in a world where educational success powers economic mobility, one could argue that this is the single most pressing obstacle that equal access to economic opportunity faces. James E. Ryan -- The Dean of Harvard’s Graduate School of Education -- describes this frustrating reality perfectly:

“Right now, there exists an almost ironclad link between a child’s ZIP code and her chances of success,” said Ryan. “Our education system, traditionally thought of as the chief mechanism to address the opportunity gap, instead too often reflects and entrenches existing societal inequities.” (Ryan)

Let’s put some numbers behind this. In developed nations students receive on average 12 years of schooling vs. 6.5 years in developing regions, and the effect of this is dramatic. North America and Western Europe boast math and reading proficiency scores of 97% and 100% respectively. These scores are more than double the scores of Southern and Western Asia with regions like the Middle East and Sub-Saharan Africa also lagging far behind. As a whole, developed regions have a 33% lead in math proficiency and a 16% lead in reading proficiency. And this shouldn't surprise us: If there is no equal access to education then of course this frustrating learning gap will persist.

2. Duolingo’s Solution

Duolingo’s app attacks education’s problems from 3 separate angles within language learning specifically. First, is affordability. None of Duolingo’s content is paywall protected; anyone with a smartphone or a computer can access the product. Its business model is obsessed with broad access. The cost of the free product version is defrayed by advertising, but that’s a small price to pay compared to some less effective, legacy alternatives. Specifically, ad-sales made up 17% of the company’s overall revenues for 2020.

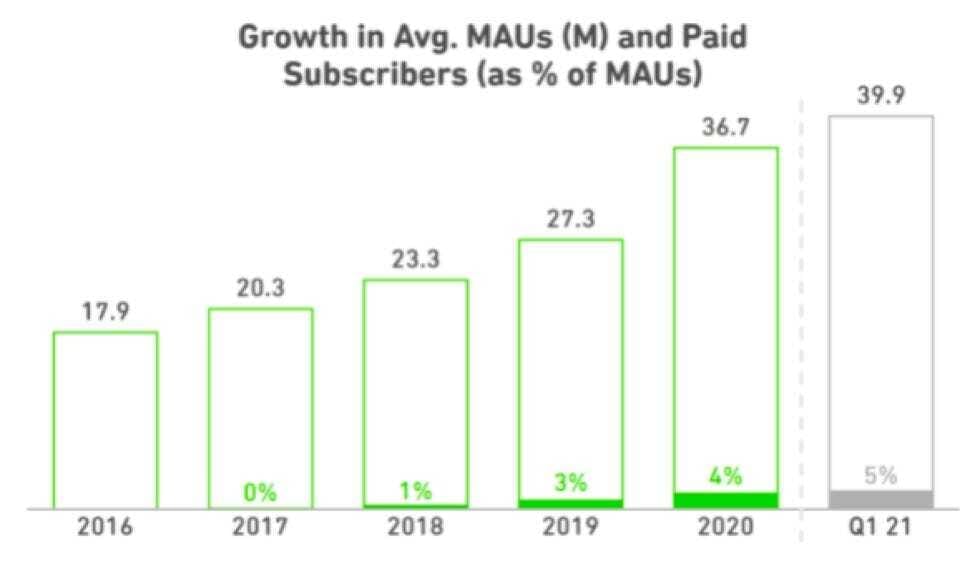

The flagship app also has an affordable paid-version called “Duolingo Plus” with monthly costs of $12.99 (or as little as $6.99 a month with an annual subscription). With these plans, paid users skip advertisements, can move through content at their own discretion and are able to track personal progress more closely. Today, 5% of Duolingo’s MAUs are paid subscribers vs. 4% in 2020 and 0% as of 2017; these subscribers contributed 72% of the company’s total 2020 revenues. Leadership believes that Duolingo is in the early stages of free-user conversion and the trend is positive and quite strong.

The second key differentiator Duolingo offers is an educational product that’s actually enjoyable. The company “believes that the hardest part of learning is motivation and engagement so it built gamification features into the platform” to keep users engaged. Things such as leaderboards, levels, points, crowns and streaks are just a few examples of how this company has designed an educational product that sometimes feels more like a video game or social media platform. Another example: Instead of learning a “chapter” users learn a new “skill” with the Duolingo app. Ask yourself how great it would be if the most addictive video game in the world taught you a new language while you played? This is the essence of Duolingo.

We’ve seen the gamification of other things like options-trading by Robinhood being met with harsh criticism and rightfully so. When people are investing it doesn’t seem like gamification is at all appropriate because of the incredible risk of loss. In education, however, it is more palatable because there is no risk of loss and because the goal is individual development. The concrete effect of gamifying a product like this is simply that users actually learn a language. This is something everyone can understand and embrace.

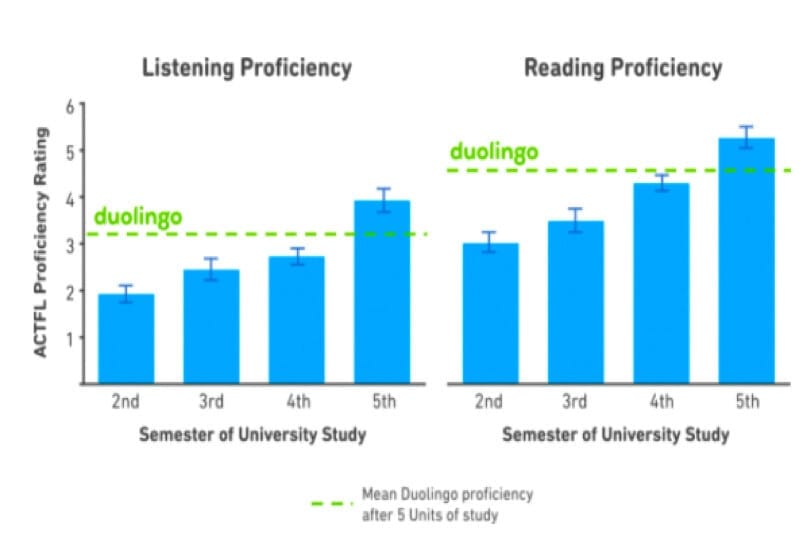

Third and finally, Duolingo built a language learning product that is more effective than legacy alternatives. It calls itself “the fastest way to learn a new language” and proudly proclaims that its users reach Spanish and French listening and reading proficiency equal to University students in their 4th semester and in just half the time. Quite the impact. This data is internally sourced form Duolingo (not an independent 3rd party) but it did carefully eliminate confounding variables to ensure accuracy. In the study, all users sampled were brand new to the subject, had only completed 5 units of a Duolingo course and were not using any other materials.

It is not that Duolingo’s product is teaching a brand-new curriculum. Its content is strictly aligned with the Common European Framework of Reference which is an international language proficiency standard. Instead, Duolingo crafts beautiful products in a way that keeps users more engaged, motivated, excited, and disciplined about learning. It also splits lessons into tiny, “bite-sized” pieces so that even the busiest of people can make progress. To ensure efficacy remains elevated, users are continuously monitored with checkpoint quizzes.

So how are consumers responding to these three supposed differentiators? Today, Duolingo is the top grossing education app on both Google and Apple thanks to a mind-boggling 500 million total downloads, as mentioned previously. It has nearly 40 million MAUs and now sports 1.8 million total subscribers while also featuring a leading brand awareness position within language learning. To offer some real-world context, there are more people in the U.S. learning a language through Duolingo than in all U.S. High Schools combined.

The product has claimed a position on Fortune’s “Change the World” list, Time Magazine’s “Genius Company” list and CNBC’s Disruptor 50 list for 3 straight years as well. It even won Apple’s free app of the year award.

3. Power in Scale

Thanks to its already massive, unparalleled scale and data collection efforts, Duolingo rightfully calls itself the world’s largest learning dataset. This reality comes with some distinct advantages. The more data points Duolingo accumulates and ingests, the better they can make the experience for its users.

On a daily basis, it collects 2.3 billion tracking events to power 500 A/B tests (or split tests) every single quarter. These tests leverage internal artificial intelligence (AI) and machine learning (ML) algorithms to examine 2 different product versions and how the user base reacts to each. This way it can continuously improve the app by knowing what actually works rather than guessing thus boosting engagement and efficacy ratings further. The A/B test could compare something as subtle as a button having 2 different colors or as complex as introducing a brand-new feature.

This relentless trial and error approach has been incredibly effective. Today, 40% of Duolingo users return to the app after day 1 vs. just 12% at the company’s founding and it has a lofty 4.7 star Apple app store rating with 1.2 million reviews. When the company A/B tested a leaderboard feature its total user hours rose by 20% immediately. Not only has this method been effective, it’s also efficient as the company can simply abandon any change to the app that isn’t well-received.

It helps to have real, tangible examples of this AI in action and we have those here. “BirdBrain” is Duolingo’s personalized instruction algorithm that crafts individual course difficulty based on a user’s ability. It stores and analyzes every answer a user has ever given to predict the probability of a correct response to make sure that users aren’t getting frustrated with impossible questions or too bored with easy ones.

“Smart Tips” is another Duolingo-built algorithm actively improving the user experience. This program gauges common user errors and then interrupts an individual lesson in a timely manner to explain concepts that are eluding a student. Smart Tips can identify and target weak spots in understanding so that they can directly be addressed.

Data, AI & ML are all at the core of Duolingo’s ability to continue offering a superior product. Everyone likes to say they have a data/AI/ML/scale advantage. Duolingo actually does.

4. The Market

According to HolonIQ, there are 1.8 billion people in the world actively trying to learn a language in some capacity. The market is already large with a total addressable market (TAM) of $61 billion powered by the tremendous economic opportunity that comes with learning English and the unlocking of new connections/experiences.

The TAM is also growing quickly with language learning as a whole poised for an 11% compounded annual growth rate (CAGR) through the year 2025 to reach $115 billion. That CAGR includes both online and offline learning but Duolingo’s online niche specifically is set for a 26% CAGR during that same period. Somewhat unsurprisingly, online language learning penetration will jump from 19.6% of total spend today to 40.8% of total spend in 2025 to reach roughly $47 billion in market size.

The company also appears to be actively growing the language learning TAM on its own. Internal Duolingo data suggests that roughly 80% of its users are brand new to language learning, offering a powerful sign of how inclusive and expansionary the app truly is.

As we will touch on below, the organization is now expanding its model into new subjects beyond language to deepen its value proposition and engagement. Successfully converting from a language learning company to an online education platform would open Duolingo up to $6 trillion in annual global education spend; this will be extremely interesting to monitor.

This growth in online education as a whole (not just languages) also seems to be in the early innings. As of 2019, just 2.3% of total education spend was digital. This compares to 10% for restaurants and 50% for books according to Cowen research from Olo’s recent S-1. The market is large, quickly growing, and still comparatively untapped. It will be up to Duolingo to create products to capture this opportunity and so far, so good.

5. More Duolingo Products and Optionality

The organization continues to find success outside of its core language learning app which hints at strong optionality going forward. In 2017, it launched the Duolingo English proficiency test for people around the globe seeking everything from university admission to work visas.

Today, the main alternatives like TOEFL are administered in testing centers and typically cost several hundred dollars (even in developing nations). Conversely, Duolingo’s tests are growingly accepted substitutes and cost just $49. To differentiate further, grading is automated and exams can be taken remotely. The proficiency test product reached $15 million in sales in 2020 vs. just $1 million year over year and already contributes 9% to the company’s total revenues.