GoodRx Deep Dive

GoodRx Deep Dive

A detailed exploration into this fascinating innovator.

Introduction:

Healthcare is one of the largest and most frustratingly opaque industries in the United States. Whether it’s the incredible pricing disparities or the labyrinth of rules that health insurers feature — nothing makes sense. At this point, transparency is an unrealistic expectation and consumers are left to largely seek out answers and information for themselves.

Doug Hirsch discovered this more than a decade ago. Even with health insurance, Hirsch was charged $450 for a medication at the counter. When he declined to pay and sought out another pharmacy in the same town, the second price was just $200. There was no explanation, just sympathy on the ridiculousness of U.S. Healthcare.

Ten years later, Hirsch’s realization has now blossomed into GoodRx — a company determined to optimize the American Healthcare system for access and low cost rather than confusion. The journey started with prescriptions but GoodRx has since addressed several other industry pain points to transform into so much more.

1. Understanding Pharmacy Issues

The viability of GoodRx’s core prescription business is rooted in the complexity of drug pricing. To understand this system is to understand the vast utility that the company features. Pharmaceutical reimbursement in the United States is byzantine and I will take the next section to fully describe it. If you don’t require those details, skip to section 2 or the summary chart at the end of section 1.

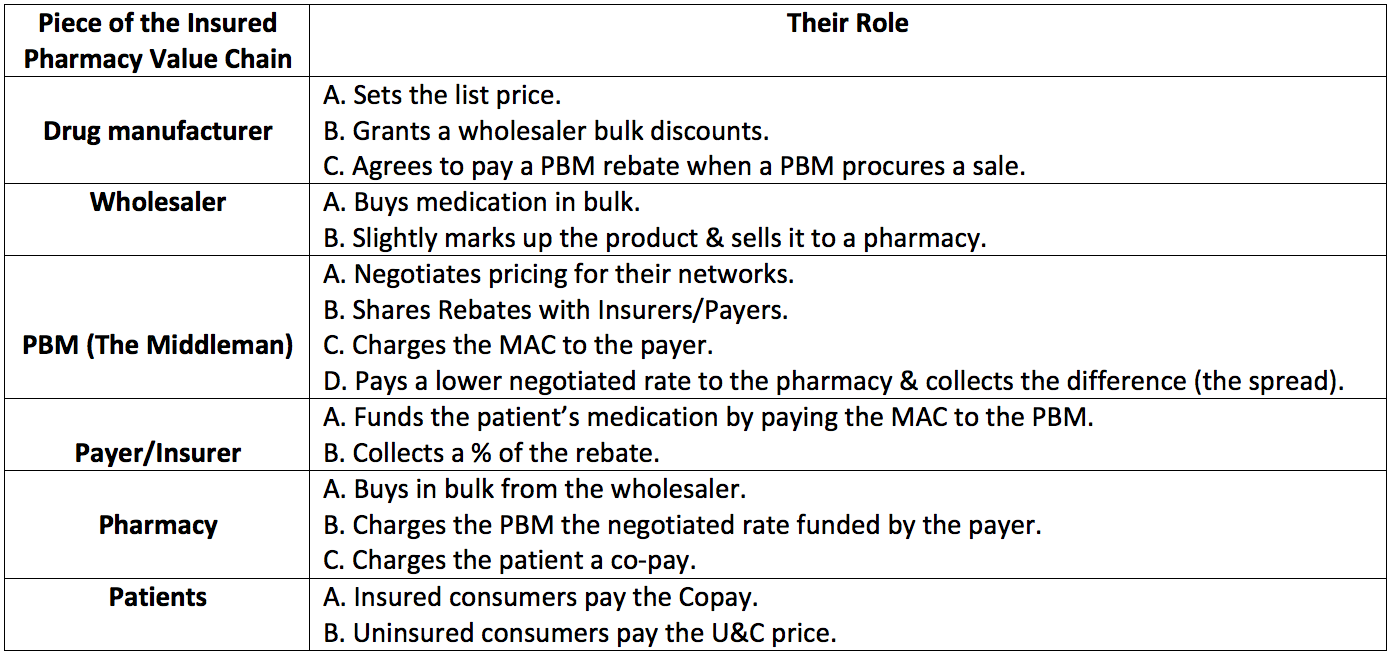

a. The Manufacturer’s and Wholesaler’s Roles:

Drug manufacturers set the initial price in the prescription work flow which is referred to as the list price. This list price is what a consumer would pay without any insurance or other discount programs.

A manufacturer conducts business with two types of entities: wholesalers and Pharmaceutical Benefits Managers (PBMs). Manufacturers are typically paid by wholesalers serving as a supply-side middleman between these producers and the actual pharmacy. 3 wholesalers account for 90% of the U.S. market today and so pharmacy chains benefit from maintaining fewer relationships with wholesalers vs. hundreds with different manufacturers.

Wholesalers use their immense scale to purchase large quantities of product at a time, thus granting them bargaining power to buy the medicines at a slightly discounted price. The price that a manufacturer charges the wholesaler is referred to as the average manufacturer price (AMP). The wholesaler will then sell the drug to pharmacies at a slightly marked-up rate.

When working with PBMs, manufacturers pay a rebate whenever a PBM creates incremental demand. This essentially functions as a hidden commission for access to the PBM’s membership network.

b. The Pharmacy Benefit Manager’s Role:

A PBM mainly works on behalf of insurance companies and large employers to negotiate pricing concessions with pharmacies. Generally speaking, they manage the drug perks an insurer can offer to their members — hence the title Benefits Manager.

These PBMs create value by aggregating all available insurer networks to create leverage with pharmacies and thus to lower prices. The pharmacies enjoy juiced demand (albeit with lower margins) via PBM-sponsored copays being lower than the Usual and Customary (U&C) price (also referred to as the “cash price”). Pharmacies also benefit from the inherent cross-selling that the added foot traffic brings.

Usual and Customary (U&C) price defined: The price that a consumer with no insurance or other discount program is charged at the pharmacy counter. This is also referred to as the “cash price.”

When a PBM fosters a pharmacy sale, it charges the associated insurer what is called the Maximum Allowable Cost (MAC) — this is merely the term for the highest drug price allowed by the PBM. The PBM — acting as a middleman — then uses these funds to compensate the pharmacy for dispensing the drug — but not by the same amount. Instead, PBMs will pay the pharmacy the lower negotiated rate and pocket the spread.

The spread defined: Funds collected by a PBM from an insurer - proceeds paid to the pharmacy for dispensing a drug

To give an idea of how crazy this pricing process truly is, PBMs often charge payers 5-20x more than what they’re paying the pharmacy for dispensing. There are even frequent instances when the PBM is paid a large fee by an insurer without even having to pay the pharmacy a cent.

It’s good to be a benefits manager — and it gets even better:

PBMs grade pharmacies on outcome data and claw back a portion of reimbursements if those grades are not satisfactory. These are called renumeration fees. The issue here is that variables such as adherence are used in the grading process which pharmacies have 0 control over. An even more ironic piece of this equation is that adherence suffers from higher drug prices and PBMs are a root cause of these higher prices as we’ll see in section 1c below. The vast majority of pharmacies have reported having to pay back PBMs in the form of these remuneration fees.

The benefits managers also directly work with drug manufacturers. A drug manufacturer pays PBMs for two things: to recommend their medication vs. close substitutes and, secondly, to negotiate lower prescription copays to financially incentivize purchasing. Essentially, manufacturers pay PBMs a commission to create incremental demand. The commission payment is what I called the rebate above and is shared with the insurer.

This brings us to our first conflict of interest. PBMs are not encouraging their networks of insured lives to take the best, most affordable and more effective medications. PBMs are nudging consumers towards whichever drug has a manufacturer willing to pay the highest kick-back fees.

Outrage within drug price structuring is typically directed towards the pharmacy, but perhaps that should be refocused onto PBMs. Yes, these PBMs serve a positive role in lowering out-of-pocket costs for insured lives — but the negatives are bountiful as well.

c. The Pharmacy’s Role:

The pharmacy pays the wholesaler for prescription supply and gets compensation from the insurer (through the PBM) and the covered consumer. Together these two parties pay roughly the U&C price for the prescription. The insurer’s payment is called a “reimbursement” with the patient’s fee referred to as the “co-pay” or “co-insurance.” Pharmacies charge the full U&C price to uninsured patients.

The negotiated rate that an insured American will pay depends on the bargaining power of the PBM, the pharmacy chain and manufacturers. Because this power violently varies, so do drug prices for all Americans.

The maximum a PBM will ever reimburse a pharmacy for dispersal is the U&C (AKA cash) price. Because of this, a pharmacy will often set the cash price far above the estimated maximum reimbursement to ensure that the business is not missing out on any revenue. For example, if a pharmacy sets a U&C price of $5 but the PBMs maximum willingness to reimburse was $10, the pharmacy is only compensated $5. If the cash price is set at any number over $10.00 the pharmacy gets double the reimbursement.

In reality, the pharmacies do not know the maximum willingness to reimburse from PBMs so they are left to guess at which U&C price will be above that amount. The large chains that own a PBM (like CVS) have direct access to one PBM pricing point — but just one of many.

Furthermore, rising negotiating power from consolidating PBMs has placed downward pressure on the portion of the total fee a that the pharmacy collects. Pharmacies have a fixed cost per medication dispersal of roughly $11 meaning any reimbursement below this amount results in a loss on the transaction. To compensate for the profit margin headwinds, pharmacies commonly inflate the U&C price even further and charge people without PBM representation even more.

This brings us to our next innate conflict of interest. The scenario laid out above inherently incentivizes the rapid growth of U&C pricing, and the uninsured are the people actually paying this U&C number on their own. Translation? The most financially vulnerable population in our nation is footing the bill and this is exactly where the high-profile issue of lofty drug prices for the uninsured stems.

The effect is hauntingly negative. According to the American Journal of Health-System Pharmacy, every 4 minutes an American dies from not taking a medication as directed with nearly 30% of scripts left at the counter mainly due to cost. This is an urgent issue.

Regardless of widely-ranging, inflated costs, most medications are non-discretionary purchases. This means price elasticity of demand is extremely low and consumers have no alternative but to foot the bill. Even for insured individuals, the combination of sharply rising copays and deductibles as well as massive price ranges creates an environment of inefficient drug costs for most Americans.

d. The Insurance (Carrier/Provider/Payer) Company’s Role:

The actual insurance company is the primary payer when a medication is dispensed from a pharmacy to a covered individual. These insurance providers pay the PBM which will then pay the pharmacy a portion of the bill when an insured customer goes to buy a drug. A key question is, how can PBMs get away with charging the deep-pocketed insurers in excess of what these PBMs pay the pharmacy? How does the spread (defined above) exist?

A few things to consider. First, PBMs are not required to disclose the specific terms of their spread and rebate contracts. This reality has created an environment lacking any form of transparency and has allowed PBMs grow their profits precipitously over the decades at the expense of other parties.

Insurance companies also have other priorities beyond prescriptions. PBMs eliminate a great deal of administrative headache by handling the reimbursement of dispensed drugs — this frees insurers to focus elsewhere on higher return on investment (ROI) endeavors. Insurance companies once did all of this pricing negotiation and reimbursement directly. In recent decades — however — the ambition to expand medication coverage proved to be too overwhelming to handle internally for most carriers.

The providers benefit from the superior bargaining power that a PBM’s larger overall network brings. PBMs are simply in an ideal position to focus here and negotiate better pricing as the top 3 — Caremark, Express Scripts and OptomRx — control 75%+ of the overall market. Without PBMs, payers lose this valuable, membership-boosting ally as virtually no insurance company can match the aggregated scale that benefits managers provide.

Don’t feel bad for insurance companies. Carriers benefit from rebate sharing and the largest 3 PBMs are also all owned by large public insurers. These providers are actively choosing to pay their integrated PBMs the maximum allowable cost (MAC) rather than the negotiated pharmacy price because it’s a good business decision.

The PBM business model is inherently more profitable than insurance payers — it’s not even close either. PBM spreads have only grown further with this vertical integration, and that is because favoring PBM operations at the expense of insurance profits is a net positive for payers. Insurers are not incentivized to fix some of the root causes of sky-high prices, but are instead encouraged (somewhat forced, really) to add gasoline to this fire.

f. Summary of the Value Chain and Role of Each Party:

2. More Problems with Healthcare

a. Higher Costs Yet Worse Outcomes:

Intense cost pressures and poor outcomes in American Healthcare are not unique to the pharmacy value chain — far from it. GoodRx’s product suite is not merely focused on prescription discounts, but on healthcare overall — and for very good reason.

Americans rank last in life expectancy, obesity and chronic disease among nations within the Organization for Economic Cooperation and Development (OECD). Despite this grave reality, the United States spends roughly 2X per capita on healthcare compared to these same OECD nations according to Lancet. This is not a matter of resources, it’s a matter of allocation, incentives and organization.

Despite Americans having on average just $1,000 in savings, health insurance premiums and co-pays cost the average family $5,000 annually per the Bureau of Labor Statistics. That number is just for insured Americans — the uninsured have it far worse.

We also have to consider the current challenge of U.S. insurers and employers pushing more and more of the financial healthcare cost burden onto members and employees. Trends such as higher deductibles and larger co-pays are creating a new class of “underinsured” individuals who still can’t afford quality healthcare despite having coverage.

Per the Kaiser Family Foundation, the average deductible for covered Americans rose 36% to $1,655 from 2014 to the beginning of the pandemic. This means individuals are responsible for 36% more cost before the insurer will step in to help. Rising deductibles have paved the way for a new type of insurance called “high deductible health plans” (HDHP) with 30% of insured employees enrolled in this type of coverage as of last year vs. 8% in 2009.

Other sources like Health System Tracker have data pointing to average deductibles quadrupling to $1,2000 from 2006 to 2016. The exact growth in out-of-pocket costs varies by data source but the idea that these costs are growing is uncontested. As we will see later, this change has vastly grown GoodRx’s targetable market.

While there are affordability options out there for consumers, these options (other than GoodRx’s) are difficult to find and even more difficult to navigate. Fragmented pricing silos and restrictive regulation across healthcare lead to massive cost variances that consumers should be able to take advantage of. In reality, most aren’t able to do so thanks to the sheer complexity and inaccessibility of the industry.

I can go online to find the best deal on a concert ticket, but I can’t do so when trying to access life-altering care. With no context on pricing or service scores, it becomes impossible to judge one option vs. another and leads Americas to have to accept whatever their reality may be. That’s an issue.

b. Access and Inefficiency

While cost and complexity are severe hurdles for consumers navigating American Healthcare, access is as well. Shockingly, 25% of Americans do not have a primary care physician and 64% of Americans have delayed care due to affordable access. Furthermore — via data published by Teladoc Health — 80% of working age adults lack a strong relationship with a primary care physician. Bringing this 80% down to 0% would cut overall U.S. Healthcare costs by 20-25% (or over $800 billion) — but this is difficult to do. Why?

Our nation has a real doctor shortage with average wait time for a new appointment in the USA of 56 days in some markets according to Merritt Hawkins. Early detection is our specie’s best way to fight disease — these long waits preclude that early detection from taking place.

The results? 30% of emergency room (ER) visits in the United States can be avoided with better access to primary care in non-emergency settings. Based on UnitedHealthcare data stating that the average ER visit costs $2,200 in America, this is a pressing issue. In total, unnecessary ER visits cost the United States $300 billion per year according to the New England Journal of Medicine. These expenses are often born by U.S. health systems as well with 66% of all personal bankruptcies being healthcare related per the American Journal of Public Health.

Better access can work wonders in fighting these battles, but our nation has been struggling to improve healthcare outcomes for generations. As I will explain in detail, GoodRx’s product suite is uniquely and perfectly tailored to combat this harsh reality.

This isn’t just an issue for patients, but doctors as well. We have to remember that physicians are mainly graded on their track records of outcomes and efficacy. All of these issues prevent many Americans from pursuing the best healthcare options — that serves as a tangible headwind in the way of physicians enjoying successful careers.

The issues for doctors continue. Legacy electronic health record (EHR) and filing systems do not offer healthcare professionals with specific information of individual patient costs. This means physicians often prescribe medications and services without being able to understand patient affordability. This reality innately lowers adherence overall.

U.S. Healthcare has left countless people behind with that actuality only becoming more true in recent decades. That’s exactly where GoodRx helps. The company’s north star is to provide actionable healthcare solutions for the rapidly growing cohort of underserved Americans and it’s finding admirable success in doing so.

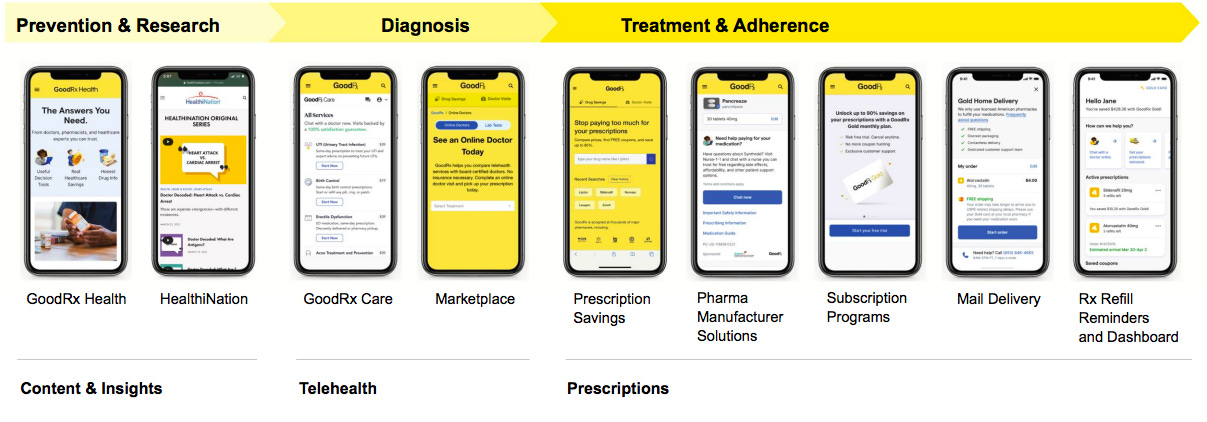

3. GoodRx Product Primer (The Philosophy)

GoodRx aims to aggregate all of the healthcare pain points we’ve covered to generate less frustration, better outcomes, healthier lives and more successful doctors. It works to uplift every stakeholder in the healthcare journey through an inherently direct-to-consumer (DTC) approach. This ambitious vision started with a price comparison tool for mainly generic drugs but has since blossomed into so much more.

It fixates on rounding up the countless disparate data sources existing in healthcare and transforming these sources into easy-to-understand language and pricing. Its combination of fostering superior access to information and a focus on an intuitive user interface (UI) equips consumers with the power to effortlessly take healthcare into their own hands. That’s the essence of GoodRx.

The company’s goal is to be with the consumer for every step of their healthcare journey to build trust, delight and loyalty. This way, when an American decides that they need to seek care, they inherently think about doing so through GoodRx.

4. GoodRx’s Core Prescription Price Comparison Product

a. How This Works:

GoodRx’s largest (and first) product is its prescription price discounting tool. This product takes pricing information from across the industry — mainly from PBMs — and translates dozens of intricate cost-calculation methods to offer consumers a centralized location for prescription deal comparison. Like most cutting edge companies, GoodRX leans on machine learning (ML) to minimize clicks and confusion per action and thus to reduce user friction whenever possible.

Users can access the GoodRx app, pick the best price and present the coinciding GoodRx pricing code at the participating pharmacy for deep discounts off of the original U&C price — no insurance necessary. Once a code is selected and used, it’s automatically stored in a pharmacy’s database for future medication fills. GoodRx collects a commission from the related PBM every time its code is used leading to high-margin, high-visibility revenues.

For the rare instance of a consumer being displeased with the service, the company’s patient advocacy team features a 99% satisfaction rate with average wait time to get a representative of 20 seconds.

GoodRx works with over a dozen PBMs in total and not one has ever left the company’s platform with more signing on virtually every quarter. That makes perfect sense when we look more closely:

PBMs aggregate most of their bargaining power and collect most of their revenue through relationships with insurers and employers. Virtually every PBM — however — also has a direct to consumer cash business operated independently from the insurance value chain. The deals offered through these consumer-facing businesses make up the majority of the prices GoodRx offers its consumers. Insurers play no part in the fulfillment process when GoodRx is involved. Instead, Pharmacies pay PBMs a fill fee whenever a PBM pricing point is used and when that pricing point is originally accessed through GoodRx’s platform the PBM and GoodRx split the fee.

“We believe that we maintain the largest database of aggregated pricing information across PBMs in the United States.” — CFO Karsten Voermann

Even if a PBM were to leave the platform, the value it provides its partners is so compelling that GoodRx’s contracts allow it to collect fees after contract termination if GoodRx was originally responsible for the sale. An unparalleled PBM network featuring 230 billion daily pricing points paired with GoodRx’s top of mind brand awareness foster the best discounts in the industry. Furthermore, it also gives GoodRx a large supply of first party data to drive more relevant product upgrades and utility enhancements.

GoodRx signs 2 types of contracts with PBMs. 93% of this segment’s revenue comes from contracts structured so that GoodRx collects a set percentage of the fill fee. This fee structure is generally tiered with more volume being rewarded with a higher take rate for GoodRx. The remaining 7% of this revenue comes from contracts calling for a fixed fee for each sale that the firm is responsible for procuring.

b. The Results and User Base:

As of GoodRx’s most recent quarter, this product’s average prescription savings rate rose from 79% to 80% off of U&C prices. This 80% compares to 71% at the time of its IPO last year and 56% in 2016. Virtually every single script in GoodRx’s database now yields at least 70% savings off of the U&C price. Overall, the product has saved Americans over $35 billion on their prescriptions vs. “over $20 billion” when GoodRx went public in 2020.

“We dominantly have better pricing that anyone else in the discount space and we are the largest player by single digit integers.” — CFO Karsten Voermann

Intuitively, this price advantage leads to GoodRx users being roughly 60% more likely to adhere to prescription schedules than the average American. Additionally, 81% of GoodRx consumers can afford all of their medications vs. just 23% without it and the company has allowed 18 million incremental Americans to afford their medications. Talk about a tangible impact. The platform is constantly adding new pricing points to its ecosystem to ensure continuously improving discounts for consumers.

That trend of improving pricing has continued as GoodRx grows its PBM scale and datapoint network. This pricing progress lends itself to a wildly compelling network effect. Better prices further juice volumes for GoodRx and its PBMs which attracts new PBMs. This process also allows existing benefits partners to negotiate better pricing with pharmacies thanks to the volume boost for their operations. Both of these factors place even more downward pressure on pricing to feed the GoodRx growth engine.

GoodRx’s app has been the most downloaded medical app on both Apple and Google for the last 3 years and sports a lofty 4.8 star mean rating with over 800,000 reviews. Repeat activity has been over 80% for the last 5 years and GoodRx’s net promoter score (NPS) for consumers sits at an elite +90 vs. +40 for United Health and +64 for a cult-brand like Netflix. Clearly consumers love the product.

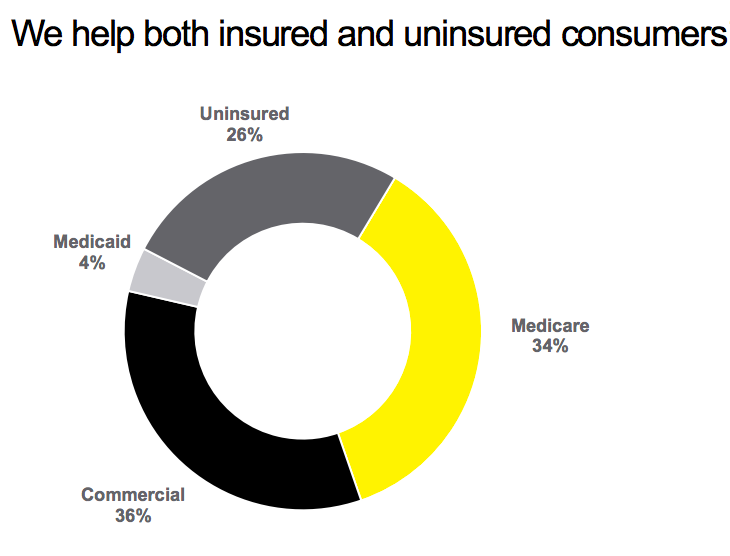

This tool is not just for the uninsured — far from it. The issues of rising out-of-pocket costs has created an environment where the prices GoodRx provides are often better than an insurance co-pay. Specifically, GoodRx is cheaper than insurance copays 55% the time with savings rates of 52% on average in those instances. As a result, 74% of this product’s monthly active consumers (MACs) have insurance; it’s safe to say the target market is most Americans.

c. Why PBMs Choose to Integrate with GoodRx:

PBMs do not collect manufacturer rebates when conducting a sale through cash networks — but the unit economics here are still outrageously compelling. As briefly mentioned, the PBM collects a fulfillment fee from the involved pharmacy in exchange for procuring new cash-pay demand. This fee is then shared with GoodRx. This transaction coincides with virtually zero costs for PBMs as the cash businesses are merely a leveraging of the existing networks that these benefits managers have built through insurers. This means the sales here are almost pure margin and the volume that GoodRx provides is nearly all incremental.

Considering this, PBMs are happy to list their prices on the platform in exchange for paying GoodRx a commission when it generates a sale for the PBM and pharmacy. GoodRx features tens of millions of highly relevant consumers and offering lower prices to far more consumers simply means more volume and more cash flow for PBMs. PBM success doesn’t depend on the price of a sale but instead on more transactions taking place to collect as many low-cost fill fees as possible.

We also have to consider that the more volume a PBM is responsible for, the more power it has to negotiate lower rates with pharmacies to drive more success for its entire business. This added negotiation power doesn’t just help PBMs within the cash business but ALL pieces of their operations by becoming bigger and more influential. GoodRx accelerates and enhances PBM aggregation efforts thanks to the massive volume boost it fosters.

Perhaps as a result, its PBM take rate continues to rise. Today, GoodRx’s mean take rate sits at roughly 15.5% of its transaction volume. This has grown from around 13.5% over the last few years while its competition has actually seen their take rates shrink. That divergence is a clear sign of the superior value GoodRx is generating vs. its substitutes — and it’s doing so while concurrently raising consumer savings rate by 20% in the same period.

d. Why Physicians Refer Patients to GoodRx’s Price Comparison Tool:

Physicians spend 14.6 hours per week on prescription administrative and adherence work with 90% of them saying this burden has risen in the last 5 years.

“Physicians have, for many years, expected to face prior-authorization (PA) hurdles… more recently, insurers have rapidly added PA requirements to more and more treatments… In my own practice, I now get insurer rejections or PA demands for a majority of the prescriptions I write each day.” — Jack Resneck President of the American Medical Association

Without GoodRx, the logistical prescription headache is simply a nightmare with offices hiring teams solely dedicated to handling the volume.

GoodRx’s price comparison tool plugs directly into essentially all physician workflows via deep EHR integrations. This way, the doctor is able to more easily consider cost in their prescribing decisions by accessing GoodRx price codes during a patient’s visit. GoodRx even provides an iteration of its app for physicians called GoodRx Pro to make using pricing codes as easy as possible. This interface cuts through red tape to help reduce time spent in this tedious area.

All of this convenience has led to GoodRx’s presence in 400,000+ doctor offices around the nation where trusted doctors promote GoodRx’s brand for free. Additionally, more than 2 million prescribers have a patient using the price comparison service and the GoodRx brand as a whole enjoys a gaudy 88% brand awareness among healthcare professionals.

To give an idea of how enthusiastic physicians are to recommend this price comparison service, 25% of GoodRx’s monthly visitors are physicians vs. 17% about a year ago. Impressively, over 80% of all physicians have now referred patients to GoodRx vs. 68% last year.

Some more highlights of GoodRx’s physician value proposition include:

93% of physicians believe GoodRx boosts medication access.

87% of physicians believe GoodRx helps patients stay on their medications.

To ensure the broadest and most relevant of EHR integrations for doctors, GoodRx recently signed a partnership with Surescripts. Surescripts is a leading health information network which facilitated the filling of 2 billion electronic prescriptions last year. It has 98% of the U.S. population is in its master index meaning this deal now makes GoodRx omnipresent at the point of prescribing for the vast majority of physicians — all seamlessly through their legacy EHRs.

Physicians will no longer have to independently seek out GoodRx but it will be a built-in piece of their workflow. This will remove more prescriber friction, reduce time spent on medication adherence and boost GoodRx’s doctor office traction further.

“This agreement with Surescripts strengthens our physician relationships by making it easier to use GoodRx. This allows us to go further up the prescription flow and grab more share.” — CFO Karsten Voermann

Similarly to GoodRx’s sky-high consumer NPS, its physician NPS also sits at an elite +90 vs. +86 when the company went public. This makes perfect sense considering the company is actively improving patient outcomes and therefore the reputations of associated physicians.

As an aside, I cannot send notes out about GoodRx without doctors openly sharing how readily they recommend it to their patients. The company sports a truly collaborative, win-win relationship with physicians.

e. Why Healthcare Embraces GoodRx:

GoodRx isn’t disrupting hospital systems, it’s merely supporting them by keeping patients healthier. There is no reason for healthcare not to embrace GoodRx as it helps to limit the current strain on our finite resources while manufacturing better results across the board. To put it plainly: GoodRx enables healthcare to do more with less. Today, that’s a requirement.

f. Why Pharmacists Accept GoodRx Price Codes:

In a perfect world for the pharmacy, it would collect the elevated U&C price as often as possible. GoodRx is directly preventing that goal from being realized, yet nearly all pharmacies accept these pricing codes and collect far lower total compensation anyway. Why?

First, some pharmacy chains like CVS directly own a PBM (and also an insurer) and so benefit from this profitable fixed cost business in an alternative way via the vertical integration.

Non-vertically integrated pharmacies rely on the incremental volumes that PBMs and their massive cohorts of members bring to the table. As I briefly mentioned, the proportion of total demand that PBMs represent allows them to negotiate increasingly favorable contracts with pharmacies. Common covenants in these contracts include mandating that GoodRx price codes be eligible for use at the pharmacy counter and preventing pharmacies from freely discounting on their own.

It’s not all bad news for the pharmacy. This added foot traffic means a more frequent opportunity to cross-sell other products that they stock. Specifically, Lab42 Research released data last year revealing 51% of consumers go to the pharmacy to make another purchase aside from prescriptions with half of that cohort spending an additional $11-$30 while there. GoodRx also more recently published data finding 25% of its users make additional trips to the pharmacy because of GoodRx with those consumers spending an average of $40 beyond the medication. This helps to make pharmacies more of an ally than an enemy.

PBMs are also very inconsistent in their price reporting which often leads to inaccuracies and angry patients at the pharmacy counter. GoodRx actively overrides these errors to ensure smoother transactions and more pleasant interactions for pharmacists. Furthermore, the organization is building new pharmacy workflow tools to help eliminate administrative redundancies and inefficiencies for this piece of the ecosystem and to boost collaboration further. Co-founder and Co-CEO Doug Hirsch has told us he expects “the fruits of our labor here very soon.”

The reliance on prescriptions to drive the bulk of a pharmacy’s success also continues to erode. For example, CVS’s Health Hubs place a greater emphasis on providing healthcare services rather than just pills and Walgreen’s is following suit. As pharmacies diversify their product offering, they should become more eager to relish the incremental traffic that GoodRx provides. But regardless of whether these chains like it or not, PBMs and GoodRx’s scale ensure the pricing codes are consistently usable at roughly 80% of pharmacies in the nation.

h. Why Bigger is Best Here:

According to CFO Karsten Voermann, GoodRx’s price comparison platform is several times larger than its closest competition. That size advantage fosters several competitive advantages beyond the aforementioned best-in-breed savings rates it offers and the compellingly unique network effect it enjoys.

Leading scale, especially when paired with elite NPS scores, generally translates into free, word-of-mouth marketing. And that’s the case for GoodRx with its largest customer acquisition channel (by far) being referrals and organic word-of-mouth. The company’s deep physician office presence is a leading source of this referral channel as product upgrades now allow these physicians to share a GoodRx price code through text or email right in the office. Consumers can also pick up a physical GoodRx card from tens of thousands of offices in the country. Other factors such as being cited 1800 times by major publications in 2019 and 4500 times by research organizations help as well — it does not pay for these placements.

Furthermore, familiarity makes GoodRx’s external marketing spend enticingly efficient. The name recognition has allowed this firm to rapidly grow its promotional activity while maintaining a payback period on that investment of 8 months during the last several years. Being the most well known in the space translates into more trust and — in this case — more appealing marketing conversions.

5. More GoodRx Products

GoodRx’s product mix is becoming increasingly diverse. In 2018, 97% of its sales came from the original price-comparison tool. This fell to 89% in 2020, 80% last quarter and is set to fall further to roughly 77% next quarter as new services gain lucrative traction.

The broadening mix lends itself to more cross-selling opportunities and therefore more lifetime value (LTV) with little added consumer acquisition cost (CAC). These enhanced unit economics justify more advertising spend to grab market share as customers become worth more to GoodRx.

To accomplish GoodRx’s ambitious objective of fixing American Healthcare wherever possible, it needed more products beyond discounted prescriptions. So it built more.

a. GoodRx Subscriptions:

Since 2017, GoodRx has offered a premium subscription offering called GoodRx Gold. This feature equips customers with options to bolster prescription savings rates. For $5.99 per month per person (or $9.99 for a family), subscribers gain frequent access to 90%+ savings off of cash prices and 1000+ medications for less than $1 at participating pharmacies. They also gain access to the mail delivery service that GoodRx added last year for no incremental cost. Other perks include discounted telehealth visits starting at $19 vs. $39 for non-subscribers (telehealth covered later) and refill pricing alerts.

“Our subscription program pays for itself for an individual with just a single prescription taken monthly.” — CFO Karsten Voermann

GoodRx is able to generate this added utility while also enjoying twice the LTV for a subscriber vs. a monthly active consumer (free user) thanks to subscription revenues being more recurring in nature. GoodRx does not have to spend a lot drive this conversion meaning it contributes to positive margin pressure.

In 2018, GoodRx launched a new co-branded subscription offering with Kroger — the 4th largest pharmacy chain in the United States. The program is called Kroger Rx Savings Club Powered by GoodRx. The subscription costs $36 per year per person (or $72 per family) and opens customers up to 1000+ generics for prices ranging from $0-$6. GoodRx manages the registration, promotional activity and transactions all on behalf of Kroger and shares this subscription fee with the chain. Kroger — and all pharmacy chains — are severely limited in what discounts they can directly provide; this relationship allows Kroger to sidestep some of those limitations.

Adoption for the product has been brisk. In a short period of time, GoodRx has already eclipsed 1.1 million subscribers (or roughly 1.6 million covered Americans) which is up 68% year over year and 7.4% sequentially. Last year, just 13.7% of GoodRx’s users were subscribers and that has now risen to 17.6% as of its most recent quarter. The company expects this percentage to rise as it adds more features like the recently introduced free delivery.

b. Pharmaceutical Manufacturer Solutions:

GoodRx’s main prescription price comparison tool does feature some branded medications but is predominately for generics. Roughly 74% of prescription spending in the U.S. being on branded medications (per IQVIA) and 20% of GoodRx searches are for branded drugs. Based on all of this, the reality of expensive branded medication prices rising 78% in since 2015 left a large gap in the company’s offering. GoodRx Pharmaceutical Manufacturer Solutions is the company’s answer to filling this void and morphing it into better consumer outcomes and more revenue.

Branded medications are generally far more expensive than generics due to stronger intellectual property (IP) protections and therefore less competition. Even for the insured, coverage is all-too-often inadequate with co-pays unaffordable. These manufacturers fund roughly $43 billion worth of annual patient affordability programs to boost adherence, improve outcomes and collect more revenue — but these affordability programs are only utilized by 3% of Americans who are eligible for them. Awareness levels are very low.

GoodRx offers and advertises these affordability solutions to the tens of millions of visitors on its core prescription app and collects a flat fee for doing so. This flat fee structure helps it to align its interests with consumers by ensuring there are no volume-based incentives leading drug recommendations astray — unlike within the PBM and manufacturer relationship. The product also automatically determines a consumer’s insurance eligibility for each manufacturer offering and allows patients to sign up for savings alerts to stay on top of the best deals.

Based on 25% of GoodRx’s total visitors being physicians and these physicians dictating most of the branded prescription activity in the U.S. — this serves as a fantastically targeted marketing vehicle for manufacturers. Specifically, GoodRx’s platform delivers 10X more traffic than any manufacturer’s drug savings page can provide on its own. This is what the consumer and physician trust that GoodRx has carefully built means. GoodRx consults with its manufacturing partners to understand what solutions they want so that value per user impression can be continuously optimized.

Manufacturers accept lower prices on these specific sales and are more than happy to do so. Why? Because they run predominately fixed cost businesses.

Producing inventory costs manufacturers little in variable expenses and so the profit margin on these incremental sales is still compelling — even when considering the discounts they allow GoodRx to facilitate.

GoodRx’s primary objective for this segment today is to drive as much market share as possible. Thankfully, the company is merely leveraging its massive install-base to create a new revenue stream — it isn’t spending more money to enjoy these added sales. This means even the flat fee it collects comes with lucrative margins while it can bolster the appeal of the product for new manufacturers signing on. Furthermore, the flat fee has consistently risen as GoodRx demonstrates the compelling value that this product provides manufacturers.

While this all sounds nice, the benefits are translating into encouraging success to confirm the utility that GoodRx’s branded marketing solutions provide. The pure-margin revenues for this segment have more than tripled in every quarter since GoodRx has gone public. This is starting from a very small revenue base but is still notable.

GoodRx also now serves 19 of the 20 largest branded manufacturers in the nation which represent 50% of the total market spend here. It sells 3 marketing solutions per partner on average vs. just 1.5 year over year and offers 8 solutions in total vs. 5 last year.

All of this added traction translates into the segment boasting a net revenue retention (NRR) rate of over 150%. Impressively, a case study with a leading manufacturer migrating from traditional media marketing to this channel revealed that GoodRx delivered an 8X ROI increase across 5 drugs. This concrete evidence should push more and more manufacturers to sign on over time.

Net revenue retention (NRR): The amount of revenue being collected from an existing cohort of customers in the current year divided by that cohort’s revenue contribution last year.

The company also has ample opportunity for horizontal expansion within its current contracts thanks to GoodRx advertising just 4% of its partners’ medications — this is quickly rising according to Voermann. Based on this — and also GoodRx serving just 7% of the largest 500 manufacturers today — this business has a long growth runway to enjoy.

The pandemic did accelerate the shift to digital advertising in healthcare which certainly helped here — but that should be a permanent shift. Why?

Healthcare professionals do not generally enjoy pharma representatives physically coming to their offices to market drugs in the middle of the day. This distraction precludes physicians from wholeheartedly focusing on patient outcomes. GoodRx addresses that annoying issue AND delivers far better returns… So there’s really no reason to go back.

Specifically, digital branded drug advertising grew 43% year over year in 2020 to coincide with a 70% drop in, in-office medication pitches. There has been virtually zero reversion to pre-pandemic trends here to date.

In the near future, GoodRx plans to create new discount programs through its recently announced partnership with “CoverMyMeds.” These additional programs will include branded drug-integrated co-pay cards.

c. Multi-Pronged Telehealth Offering:

GoodRx offers 2 products within its telehealth segment: GoodRx Care and its Telehealth Marketplace. Both products are business to consumer (B2C) in nature.

GoodRx Care:

GoodRx Care is the company’s core telehealth offering resulting from its purchase of HeyDoctor last year. HeyDoctor had a perfect app score at the time of the acquisition making it the perfect culture fit in GoodRx’s mission to delight customers.

This business contracts with groups of physicians to offer virtual services through the GoodRx Care platform. Today, it can address 35 conditions — mainly associated with low cost prescriptions to optimize cross-selling capabilities — with visits starting at just $19 for Gold subscribers. GoodRx generates revenue here by taking a small portion of this visit fee as compensation.

Roughly 20% of GoodRx users searching for a drug through its main app do so without a prescription readily in hand. This telehealth offering allows GoodRx to more actionably serve those people while keeping them within its ecosystem to enjoy more cross-selling.

We also have to remember that our nation is currently dealing with a pressing doctor shortage. In 15 of our county’s largest cities — where access is supposed to be best — average wait time for new primary care appointments is 24 days. These delays contribute to the aforementioned added healthcare cost burdens that the United States endures on an annual basis.

GoodRx Care boosts and quickens access to care by connecting consumers with a physician in under an hour. This patient can then get a prescription filled if necessary. That outcome stands in stark contrast to the 80% of Americans with insufficient access to primary care.

More recently, GoodRx Care fully integrated GoodRx’s prescription pricing codes and a mail order feature to ensure its consumers can enjoy best-in-class access, convenience and affordability. To make the virtual consultation process as seamless as possible for participating doctors, GoodRx built its own EHR on top of Care. This EHR enables core functionality such as direct messaging, electronic prescriptions and mail delivery options.

All of this uniquely infused utility works to fight against commoditization in telehealth. Barriers to entry for standing up virtual point solutions are very low. By GoodRx incorporating all of the cost savings it can provide directly into its telehealth offering, it finds concrete differentiation in a sea of competition.

While there’s some concern about telehealth being a pandemic-induced fad, that does not at all appear to be the case as we exit Covid-19. GoodRx recently published a survey of 1600 patients and providers alongside the American Telemedicine Association on telehealth trends and satisfaction in a post pandemic world. The takeaways included 40% more face-time with physicians and easier appointment scheduling as well as 70% of providers confirming telehealth leads to better continuity of care.

Perhaps most encouragingly, 60% of Americans are planning to use telehealth vs. 17% pre-pandemic. As a negative, no-show rates were higher virtually than for in-office visits, but the conclusions were largely very positive. The U.S. Healthcare system needs to find ways to realize added efficiencies with finite resources — GoodRx is providing the tools to do just that.

Telehealth Marketplace:

35 conditions virtually covered is not all that many with behemoths like Teladoc Health serving exponentially more. To broaden the breadth of service that it can provide its users, GoodRx launched its Telehealth Marketplace.

This marketplace partners with 3rd party providers to raise its addressable conditions from 35 to 150 while also incorporating broad lab testing capabilities. It also expands the possible doctor selections for GoodRx’s users which innately fosters lower cost as well as allowing people to effectively compare service scores. GoodRx collects a commission for directing business to these 3rd party providers.

Telehealth margins:

GoodRx takes a unique approach to telehealth as it grows its addressable conditions and the geographic footprint. It sells these services roughly at cost to drive cross-selling and market share gains.

“We view our telehealth offering as cost neutral marketing.” — CFO Karsten Voermann

The company is able to price this product so aggressively thanks to all of the wonderful cross-selling opportunities form the rest of its product suite. It’s essentially another top-of-funnel marketing tool to boost LTV/CAC for the business as a whole. With Telehealth as competitive and commoditized as it already is, this approach is a very good one in my mind.

I was able to speak with a Vice President from GoodRx on this philosophy and here’s what they had to say:

“The margin profile and the competitive dynamics in the telehealth space — with many players willing to lose substantial amounts in aggregate and even per visit — means that we do not intend to become a telehealth-focused company. We believe these types of cross-platform integrated experiences will continue to enhance our ability to cross-sell going forward and will increase the stickiness of our users.” — GoodRx Vice President Whitney Notaro

Encouragingly, cross-sell activity from GoodRx’s telehealth visits rose from 10% last year to 30% earlier this year and to 60% as of two quarters ago. That momentum continued into its most recent quarter with the 60% metric rising to 65%. The at cost approach is working to feed the rest of its higher-margin businesses. Furthermore, since GoodRx started offering its Gold subscription at its telehealth checkout, 40% of visitors have already converted which offers us with more evidence of this approach working.

Today, margins for this segment are far worse than the rest of the business meaning as this telehealth operation grows, profitability worsens. The margins here will remain worse than the rest of GoodRx’s businesses but that gap could diminish somewhat in the coming years as the space matures.

d. GoodRx Health:

In recent months, GoodRx debuted GoodRx Health — its free healthcare information hub. This functions similarly to Google Scholar except with far more focus on healthcare knowledge and a stricter vetting and verification process to ensure the highest quality of information. There are 3.1 billion monthly healthcare-related searches in the United States and GoodRx wants that interest directed through its ecosystem as often as possible. The company employs a team of world renowned consultants to intricately and expertly curate the flow of information.

“I see this this as next generation healthcare content in a sea of noise. We give you one, concise answer written by a healthcare professional.” — Co-CEO Doug Hirsch

The new application features “Health Wizard Tools” to help Americans through sensitive and difficult decisions and offers a “Health Debunked” segment to inform the public on polarizing issues. Generally speaking, it focuses on outcome and financial guidance along with drug-specific inquiries. The product also allows users to customize their newsfeeds to ensure the most relevant and granular of information.

To bolster the service’s library of content, GoodRx purchased HealthiNation (a publisher of reliable healthcare information) for $75 million in an all cash deal earlier in the year; the product offers information spanning 350 health conditions.

“We’ve seen a 60% year over year increase in our content traffic.” — Co-CEO Doug Hirsch

Despite being free, GoodRx Health is expected to have 2 profoundly positive impacts on GoodRx’s business. First, it offers yet another vehicle for GoodRx to introduce more people to its services with very little customer acquisition cost. Secondly, this also provides another marketing tool (of highly relevant consumers) for its branded manufacturer partners to leverage and pay for.

6. The Market

Total healthcare spend in the United States was $4 trillion in 2020 and expected to grow to $6.2 trillion by 2028 per Centers for Medicare and Medicaid Services (CMS). GoodRx’s total addressable market (TAM) is nothing short of massive.

Its current prescription TAM sits at $360 billion and — according to CMS — this market will grow in excess of U.S. GDP through 2028 at a 5.7% compounded annual growth rate (CAGR). Here specifically, GoodRx is in the unique position of being the largest player with the most PBM relationships in the market by far — while also being less than 1% penetrated in this niche. This is a compelling combination: Being best-positioned to succeed and also having ample low hanging fruit to capitalize on.

Not only is the current prescription market massive, but it’s also wildly unserved. The roughly 30% of prescriptions left at the counter in the USA translates into another $164 billion in possible TAM for companies able to broaden access. That’s exactly what GoodRx does so well.

GoodRx’s Pharmaceutical Manufacturer Solutions TAM was calculated 5 years ago based on the total promotional spend for branded producers which sat at $30 billion. This $30 billion also does not count the $13 billion in discounts that manufacturers distribute annually which GoodRx is enabling them to do more efficiently. That brings this segment TAM up to at least $43 billion — and likely more today.

The telehealth market is also massive (and highly competitive). McKinsey projects the market to be $250 billion — but that should rapidly grow in the coming years. The $250 billion is cited as a fraction of the $1.25 trillion in outpatient and home visit spend in the United States. According to Teladoc Health, eventually 25%-50% of these visits will be virtual with that $250 billion only assuming 20% are addressable virtually.

In total, GoodRx’s TAMs sum up to a total of $817 billion. The growth runway for this company is as long as any other.

7. What’s Next (Optionality)?

a. More products:

GoodRx’s original generic prescriptions opportunity remains broadly untapped. 70% of consumers still don’t know that prices can vary by up to 100x on prescription prices and the vast majority of us are motivated mainly by cost.

Subscriptions, telehealth and branded manufacturer solutions are all young GoodRx endeavors and are all rapidly growing. The firm’s original price comparison business will continue to attract more MACs and subscribers while enhancing its cross-selling activity and therefore LTV/CAC ratio. Revenues here should continue to compound based on all of the opportunity GoodRx has to savor.

Still, developing existing channels won’t be the only focus — the product roadmap remains far from complete:

“What I spend most of my day on is additional healthcare pain points. There are so many exciting opportunities for us to help more Americans and to spawn new businesses.” — Co-CEO Doug Hirsch

GoodRx leadership has hinted at where it may debut new products. In the company’s prospectus, it highlighted common healthcare procedures and surgeries as other areas of healthcare lacking any means of price and service comparison or transparency. According to a study published by the Healthcare Cost Institute, prices for these services range by up to 39X to provide the same service in the same city — not great. GoodRx sees this as another problem to fix along with things like clinical trials and in-person doctor visits.

“Through the extension of our platform into many other areas of healthcare that lack price transparency and consumer empowerment, we believe we can address a larger portion of the American Healthcare market. The list of things we want to accomplish is getting longer.” — Co-CEO Doug Hirsch

The company rarely talks about its GoodRx for Pets product, but based on compelling macro-trends I think this could be an appealing vertical for it to find more growth. Younger generations are more likely to consider a pet as a member of the family and as a result have a higher propensity to spend on pet medical expenses. The pet meds space is poised to benefit from an 11.1% CAGR through 2026 and — as a trusted, established brand in healthcare — GoodRx can take piece of this pie if it wants to do so. Time will tell.

Leadership is also very open to more M&A activity to bolster its value proposition. With the team’s track record of successful integration of companies like HeyDoctor and RxNXT, I would welcome this:

“We build a lot of great products here but we are not going to build everything. There are a lot of great companies out there and when we find one that is complementary to our business and helps us accelerate our path we will take action.” — Co-CEO Doug Hirsch

b. Business to Business (B2B):

The company is at the beginning stages of its business to business (B2B) pursuit. Somewhat similarly to how a benefits manager functions, GoodRx is signing large deals with enterprises to expand its offering to large employers. GoodRx inked agreements with USAA and its 13 million members along with DoorDash to offer over 1000 medications for under $10 — alongside free delivery and discounted telehealth. Doug Hirsch sees carriers like USAA as some of the most capable aggregators of demand and therefore the best B2B partners — signing more insurers will be a key focus going forward.

“Employed Americans covered by health plans is one of the biggest areas to aggregate demand and we are moving very aggressively in that direction with some pilot programs going on right now.” — CFO Karsten Voermann

The organization recently signed a new agreement with Fetch Rewards and its 10 million active consumers. Fetch is a receipt refunding service with over 1.8 billion total receipts submitted. Now all of these users will be able to access GoodRx pricing codes directly in the Fetch app. We’ve been told by GoodRx leadership that these are merely the first dominos to fall in the company’s B2B endeavors; it expects many more agreements like these to come to fruition in the near future.

Furthermore, its recent acquisition of RxNXT allows employers to offer a free benefit in their health plans to automatically use GoodRx pricing codes whenever it beats an insurance co-pay. This will work to further reduce overall cost inefficiencies and to deepen the company’s B2B value proposition.

c. Medicare and Health Insurance:

With the majority of GoodRx consumers being insured, it saw a partnership with the Medicare player — GoHealth — as a natural expansion of its offering. With this partnership, eligible GoodRx users can find the best Medicare plan directly in the GoodRx app and GoHealth members gain access to its pricing codes. It’s still very early days for this project, but Co-CEO Trevor Bezdek told us on the last earnings call that traction and momentum here is ahead of expectations. We’ll see.

Interestingly, the company’s most recent earnings call indicated that GoodRx planned to further enter health insurance by “navigating customers through the process as their trusted advocate.” GoodRx will not become a licensed insurance vendor. It will likely create an insurance marketplace — like SelectQuote and others provide — to offer better information and more context on how to pick the best plan. The GoHealth partnership will be a big part of this.

d. Medicaid:

As a result of the pandemic, the federal government passed the Families First Coronavirus Response Act which prevents state-level Medicaid programs from removing any lives from eligibility lists. This resulted in soaring Medicaid enrollment — but this is temporary. When the temporary legislation wears off in a couple weeks, some predict that 15 million Americans could lose coverage. While this is a negative for those Americans, it will inject added demand into GoodRx’s affordability solutions and could provide a new lever of growth starting next year.

“As people end up losing Medicaid coverage and end up without solutions, that will drive more people to look for benefits with us. It’s an unfortunate positive for our business.” — Co-CEO Doug Hirsch

e. Hiring data:

As of the end of last year, GoodRx had 479 employees vs. 137 in 2018. It has continued to hire at a rapid pace according to data from LinkedIn with over 68% employee growth year over year and roughly 50 new hires just in the last 8 weeks.

8. Leadership, Culture & Ownership

a. Leadership

GoodRx is still led by its two co-founders who continue to share an office roughly a decade into their journey. Doug Hirsch is a Co-founder, Co-CEO and a member of the board. Before joining GoodRx, Hirsch was the CEO of DailyStrength which is a social network for support groups that was purchased by Sharecare. Beyond that experience, Hirsch also worked in senior roles with both Facebook and Yahoo. At Facebook specifically, Hirsch was the VP of Product and a co-creator of Facebook Photo-tagging.

Trevor Bezdek is the other Co-founder and Co-CEO and he too serves on the board of directors. Before starting GoodRx, Trevor was a managing partner at Tryarc which is a technology consulting firm and he also founded Bioware — a community for biologists and scientists.

Doug and Trevor showcase a perfect mix of talents. Doug found remarkable success in building consumer-facing technology met with broad adoption and Trevor is an expert on the ins-and-outs of healthcare regulation. Together they form a dynamic duo sporting an elite 98% approval rating on glassdoor. I don’t think I’ve ever seen a score so high to be candid.

Andrew Slutsky was the company’s 3rd employee and has been the President of Consumer with GoodRx since joining the team. His lengthy tenure offers more evidence of a strong workplace culture. Slutsky was formerly a senior marketing manager at RentTheRunway and a director at Loeb Enterprises.

Karsten Voermann has been the CFO since 2020 and most recently served as the CFO at Mercer Advisors and Ibotta. The company’s President of Healthcare — Bansi Nagii — boasts impressive experience as the former Chief Strategy and Business Development Officer at McKesson as well as a Principal at Deloitte.

Highlights from its board of directors include:

A former Tripadvisor CFO

A former CFO of Optum Rx (the PBM that UnitedHealth Group owns)

A former President of Operations for Express Scripts (another large PBM)

Silverlake Capital has multiple board seats in connection with a $100 million private placement at the completion of the IPO

b. Culture

GoodRx features a self-proclaimed “excellent employee track record” and is extremely selective in who it actually hires to the team; just 0.6% of applicants are brought on. The LA Business Journal named GoodRx a best place to work for the last 2 years while also naming Doug and Trevor as best CEOs and crowning GoodRx as a best company for women and diversity.

To build company relationships, the executive team hosts weekly happy hours and frequent game and movie nights. The headquarters is also a pet friendly office. GoodRx’s culture resembles a tightly-knit community rather than a publicly traded corporate giant. That’s a great sign.

c. Ownership

GoodRx features a dual class share structure. The vast majority of the executive team’s ownership is paid out via options and equity awards to keep incentives tightly aligned with company success. Uniquely, much of Andrew Slutsky’s ownership is expressed through his 5% class A common equity stake while Hirsch and Bezdek predominately hold future options and so aren’t expressed as large shareholders in the proxy statement (as of April 2021).

Four funds — Silver Lake, Francisco Partners, Idea Men LLC, and Spectrum — own 81.1% of the total, non-diluted shares overall.

9. Financials

a. Demand:

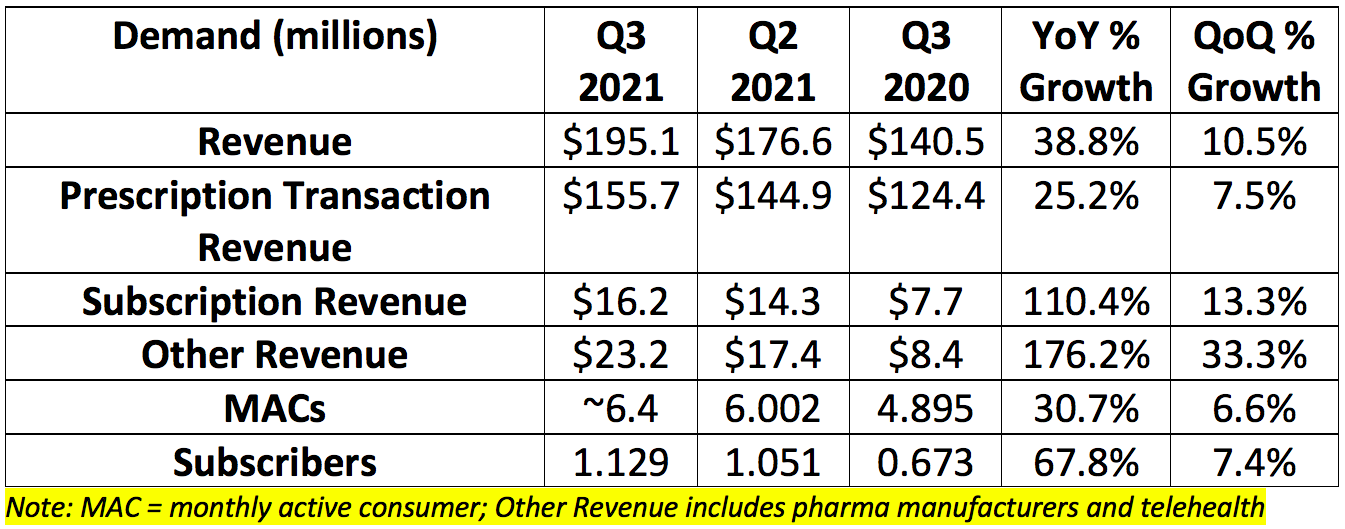

GoodRx’s demand metrics have been strong since the company went public despite the pandemic weighing on the largest piece of its business. The company’s prescription price comparison tool (its largest segment by far) is tightly correlated with total prescription volumes. The pandemic halted elective care and the spread of cold & flu so prescription volumes tanked as a result. Its most recent quarterly demand performance is depicted below:

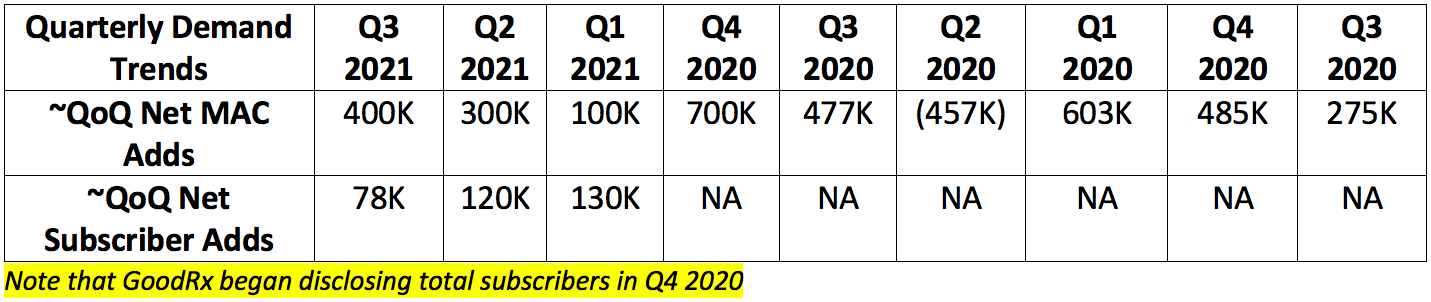

Traffic for the company depends on consistent subscriber and MAC additions. That trend is depicted below (Q2 2020 was severely impacted by Covid-19):

GoodRx has a long history of delivering lofty growth. That reliability is illustrated below:

b. Demand Guidance and Context:

GoodRx removed its 2021 annual guidance after the first quarter of this year due to volatile trends in healthcare utilization pertaining to the pandemic and subsequent variant outbreaks. It re-instated (and reiterated) this previous guidance despite the pandemic having a more durable impact on the company’s business than it originally anticipated. The original first quarter guidance assumed a return to normal by now and that has not come to fruition. Based on this, I found it impressive that the company was still able to maintain its original guidance from earlier this year.

This means the rest of the products in its suite are more than making up for the headwind and are fostering outsized growth. It’s exciting to think where this firm will be when prescription volumes do truly return to normal — GoodRx now believes this will be at some point next year.

While this is proving to be a stubborn headwind, it’s temporary. When the roughly 1 billion-visit-backlog in the United States begins to unwind, that will work to accelerate growth for its main prescription pricing business. That acceleration is entirely ahead of the company.

GoodRx’s most recent demand guidance is depicted below:

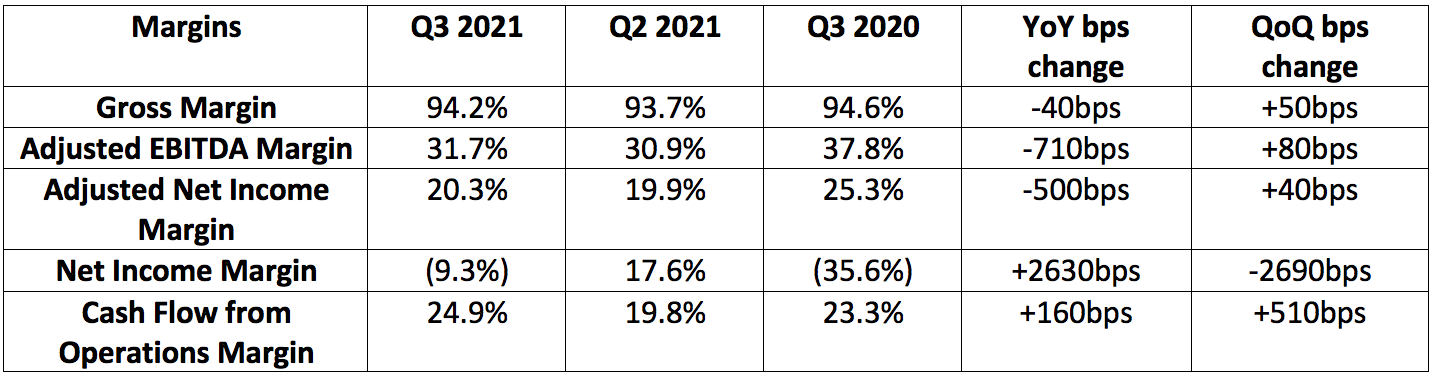

c. Margins:

GoodRx’s most recent quarterly margin performance is depicted below:

The lofty margins have allowed GoodRx to aggressively re-invest profits back into more scale and more value to maintain its industry-leading pricing.

Note that Q3 2021 net income margin was greatly impacted by a $55.5 million swing in tax benefits vs. Q2 2021 and $20.1 million in non-recurring stock-based compensation in connection with the IPO. Adjusted net income margin accounts for these impacts.

GoodRx’s at-cost telehealth approach and its aggressive spend on marketing, headcount and innovation all continue to weigh on the company’s margins — by design. CFO Karsten Voermann expects a 30% adjusted EBITDA margin to be the floor for GoodRx with that margin line expected to improve in the coming years:

GoodRx guided to a “roughly 31%” adjusted EBITDA margin for next quarter and for 2021 which was identical to the midpoint guidance of 30-32% that it offered in the first quarter.

d. Balance sheet:

GoodRx has $912 million in cash and equivalents plus roughly $140 million in net receivables and pre-paid expenses. Its balance sheet features a $100 million credit revolver as well as a $700 million 1st lien term loan facility. Just 1% of this debt is current (meaning due in the next 12 months).

It has $663 million in debt net of unamortized issuance costs and discounts. This debt carries an interest rate of roughly 2.6%-3.1% depending on GoodRx’s net leverage ratios at the time of the next interest payment.

The company did have a 2nd lien credit facility carrying a much higher interest rate but used an expansion of its 1st lien term loan facility to pay that off. Doing so helped lower its interest expense to roughly 3% of total sales in GoodRx’s most recent quarter vs. 4.5% in the same period last year.

As a note, stock-based compensation has been abundant for this company — like with many successful IPOs — since it went public. Encouragingly, all restricted stock units related to founder’s awards in connection with going public have now vested.

In GoodRx’s most recent quarter, stock-based compensation fell to roughly 20.5% of sales vs. 76% of revenue year over year and 23.0% sequentially as IPO bonuses continue to fade. Still, that 20.5% needs to continue to decline and it likely will with the bulk of these stock-based compensation charges being non-recurring. This only becomes alarming to me if it does not continue to precipitously fall as we move further from the IPO.

d. Valuation table & My Prospects:

The chart below is based on the following:

An enterprise valuation (EV) of $15.7 billion

A share price of $40.00

Mean analyst forecasts pulled from Koyfin (which have been quite stable)

A stable 95% gross profit margin.

In this scenario, GoodRx trades for the following multiples:

I believe a combination of GoodRx’s vast addressable market, untapped optionality, elite net promoter scores and unmatched scale will all translate into sustainably lofty revenue growth. With an assumed 27.5% CAGR through 2030 we get 2030 sales of roughly $6.68 billion. Assuming a stable EBITDA margin of 31%, GoodRx would then boast $2.07 billion in EBITDA.

With a multiple of 25X EBITDA, we would then be left with a $51.7 billion enterprise value for GoodRx or a 14.6% compounded return during that time. Growth will likely be above 27.5% for several years to come and EBITDA margin will likely expand from the short-term trough. This merely paints a picture of where I think the company can be (in a somewhat pessimistic outcome) and should be taken with a large grain of salt. Actual results will surely differ.

10. Risks to the Bull Case

a. Competition:

Prescription Price Comparison Competition:

Within this segment, GoodRx is several times larger than its next closest competitor SingleCare. Specifically, SingleCare does around $27.5 million in annual revenue with GoodRx’s competing segment generating roughly 20X that amount just during the first 9 months of 2021. Again, this large size advantage is the key contributor to GoodRx offering better discounts.

“Our competition is made up of small, fragmented competitors lacking the breadth and relationships that we have. We’ve seen other players in consumer brands, health plans and well-funded start-ups that have all tried to replicate our business. They haven’t had success.” — Co-CEO Doug Hirsch

Amazon is another competitor to consider. The consumer-technology giant recently announced a new product attempting to mirror some of the value that GoodRx’s price comparison tool provides. While deep-pocketed competitive entrants are always to be contemplated, they also serve as evidence of the opportunity being lucrative enough to pursue which I take as a positive. And for a much larger positive, Amazon has found virtually no success in this space to date.

In a recent investment banking interview, Co-CEO Doug Trevor Bezdek explicitly told us that GoodRx has seen no evidence from any 3rd party data of Amazon gaining any traction:

“There’s virtually no usage. 3rd party data shows they only have a few hundred users per month” —Co-CEO Trevor Bezdek

How could this be the case? There are two important factors to note. First, Amazon is predominately trying to build out a prescription delivery channel — and that’s a very tough business. Mail delivery as a percentage of total prescription volumes was just 5% during peak pandemic months and has now begun to shrink with our nation opening back up.

Americans use pharmacy trips for a bevy of use cases like routine medical services — you can’t get a flu shot on Amazon. Beyond that, expensive prescriptions must be signed for upon delivery meaning a patient is required be home whenever a script arrives — quite inconvenient.

GoodRx’s pricing is also better than Amazon’s — by a lot. Thanks to GoodRx working with well over a dozen PBMs vs. Amazon working with just 1 (that GoodRx also uses), Amazon is more expensive for consumers over 90% of the time by mail and 100% of the time for retail. GoodRx sees its core competition as the 70% of Americans not knowing that prescription prices vary — but it’s still encouraging to see the tangible and vast differentiators GoodRx enjoys over Amazon.

GoodRx believes that Amazon’s competing product — the Prime Rx card — was only launched to give it the legal right to display 3rd party pricing on its prescription price comparison website. It was not with the intention of having its consumers actually use the card in a brick and mortar pharmacy (where GoodRx does most of its business).

Pharmaceutical Manufacturer Solutions Competition:

GoodRx competes with alternative advertising methods for branded manufacturers like linear television and other health information platforms like WebMD. The $43 billion in TAM here is a zero sum game — as one organization claims a larger piece of this pie others will largely lose out. It’s up to GoodRx to continue making its platform the most efficient place for marketers to spend. So far, so good.

Telehealth Competition:

The telehealth competitive landscape is daunting. Business to business (B2B) players like Amwell do not directly compete with GoodRx’s consumer-facing product but still take a piece of the overall telehealth opportunity and therefore do compete in some capacity. Teladoc’s business represents both B2B and business to consumer (B2C) competition through its BetterHelp offering.

There are countless other consumer-facing services like ZocDoc for example that are all competing for the same business — although GoodRx does benefit from the broad range of its product offering. As I mentioned above, GoodRx is also selling this service at cost to accelerate cross-selling which is the most effective way to grow near-term market share in a commoditized sector. Still, there’s no guarantee that it will find pricing power in the future.

b. Politicians:

One of the primary risks associated with owning GoodRx is political risk — we have zero control over new laws being enacted. Investors must be comfortable with that lack of control possibly ending poorly in some regulatory scenarios.

Legislation such as the Affordable Care Act (ACA) forced drug manufacturers into price concessions in exchange for Medicare Part D participation and also raised the number of individuals with insurance coverage. While better coverage could have hurt GoodRx’s business, this legislation did not really accomplish that goal. Why? An unfortunate side-effect of it was soaring deductibles for newly insured lives. This created that new class of underinsured individuals where GoodRx price codes are still far more appealing than co-pays.

The Trump administration attempted to implement new transparency and price disclosure mandates within the industry and planned to spend $135 billion in 2021 to boost competition and lower costs. It also proposed a federal price ceiling on insulin and EpiPens but it was not able to pass this legislation through congress before the 2020 election.

More recently, President Biden’s proposed domestic spending package “abandoned every single policy idea aimed at lowering prescription drug prices” according to Stat News.

“Every administration has tried to fix the broken healthcare in this country and none have had an impact. Nothing we see right now — regardless of passing or not — has any material impact on our business.” — Co-CEO Doug Hirsch

GoodRx maintains a strong relationship with Capitol Hill and is even frequently cited in pilot programs that politicians propose based on the understanding of GoodRx now being a core piece of this industry. Still, anything forcing insurers to lower co-pays and deductibles, pharmacies to limit U&C prices or PBMs to disclose contracts more clearly could negatively impact GoodRx’s business.

An idea often floated around that could actually work is opening the Canadian border to drug imports but there’s currently little movement here. There have been countless attempts to try and accomplish healthcare affordability for Americans but the success of those attempts has been severely lacking until GoodRx arrived.

c. Covid-19:

The Covid-19 pandemic had quite the mixed impact on GoodRx’s business. A combination of less social interaction cutting into cold and flu season plus elective care being all but halted at the peak of the pandemic represented a large headwind for the price-comparison business. GoodRx’s monthly active consumers (MACs) even dropped during the second quarter of last year with all of these factors. The largest contributor to the company’s word-of-mouth growth is all of the free physician referrals that it gets. Less doctor visits meant less of these referrals.

As a result of Covid-19, the elective care backlog ballooned to 1 billion visits as Americans delayed consultation. As that backlog unwinds, prescription demand will accelerate. Translation? Covid-19 was a daunting short term headwind for GoodRx’s price comparison business but will turn into a lucrative tailwind before the backlog fully normalizes and growth reverts to historical trends.

Furthermore, the 2021 cold and flu season looks to be far more normal than last year:

“It looks like this season will not be great from a cold & flu perspective which will drive demand for us. We previously talked about how the light 2020 cold & flu season cost us about $5 million in revenue. A more normalized season this year contributes to potential revenues looking forward. Our anticipation right now is that this season will be more virulent than in the past unfortunately for Americans.” — CFO Karsten Voermann

Conversely, GoodRx’s telehealth business was greatly helped by the Covid-19 pandemic. According to data published by McKinsey, 46% of consumers had used telehealth services by the end of 2020 vs. just 11% in 2019 — the pace of that adoption curve is not normal. The pandemic invariably served as a tide that lifted all boats in this space and GoodRx surely benefited here as well.

It will be interesting to see how telehealth momentum continues in the coming years. It’s undeniable that virtual visits are more convenient and productive for certain use cases. Now that 46% of consumers have experienced this incremental utility, it’s hard for me to believe they’ll just go back to their old healthcare consumption pattern.

Finally, the pandemic represented a tailwind for its manufacturer solutions segment by forcing the industry to discover the added efficacy and convenience of digital marketing vs. in-office visits that I previously discussed.

D. Concentration risk:

When a few PBMs control such an overwhelming majority of the total market, there will naturally be revenue concentration risk for the price comparison tool and therefore GoodRx as a whole. Specifically, the 3 PBMs GoodRx does the most business with (MedImpact, Navitus and Express Scripts) accounted for 42% of 2020 sales. That fell from 61% in 2018 but is still a large number. It helps greatly to know how much value GoodRx is providing to these PBMs and that no PBM has ever ended an agreement with GoodRx. Regardless, this is something to keep in mind.

E. Walmart Generics:

Walmart runs a generics savings program that offers hundreds of prescriptions for a small fixed fee + cost of medication. It offers many prescriptions for under $4. This does diminish the value that GoodRx’s savings offerings has for consumers but based on the company working with 12+ PBMs vs. Walmart’s 1, it’s still usually cheaper.

If CVS and Walgreens were to follow suit, that could be a real headwind for the price comparison tool. Thankfully, this doesn’t appear to be all that likely. Walmart collects a far smaller portion of its sales from prescriptions vs. CVS and Walgreens and therefore gains more from discounting scripts and enjoying the coinciding added foot traffic.

CVS and Walgreens are not currently in a position to do so as their prescription businesses are relied on far more heavily to drive overall operations. That reliance is diminishing with initiatives like Health Hubs, but it’s still vast. For evidence, the Walmart generics program is already 15 years old and others have not followed suit.

Furthermore — per my discussion with Whitney Notaro (GoodRx VP) — there are significant regulatory and economic obstacles in the way of doing so: