News of the Week (August 22-26)

News of the Week (August 22-26)

SoFi; The Trade Desk; Duolingo; Penn Entertainment; PayPal; CrowdStrike; Upstart; Meta; Olo; Shopify; Match; Ozon; Macro; My Activity

To view my current portfolio, click here.

1. SoFi Technologies (SOFI) -- Student Loans

The Biden Administration offered some long-needed clarification on the student loan pay pause and possible forgiveness. I have no interest in commenting on the political viability of this move -- I solely care about how it affects SoFi. And in this case, the decision seems quite positive for the company.

The President announced that he would extend the payment pause one final time through the end of 2022. Furthermore, he declared that certain borrowers would be eligible for $10,000 in loan forgiveness (up to $20,000 for Pell Grant recipients) if their total income is below $125,000. How could that possibly be good news for a student loan originator like SoFI? Great question.

First, SoFi’s 2022 guidance assumes the moratorium will be in place through 2022 -- so the extension will not impact its 2022 forecasts negatively. Furthermore, SoFi’s average student loan balance is around $70,000, meaning eligible borrowers will only see a maximum of 28% forgiveness on their debt. The remaining payments will still be due to restart in 2023.

There has also been a quite large cohort of borrowers waiting to refinance loans until they knew if their debt would be forgiven entirely. Why refinance if you won’t owe the principal anyway? Now that these borrowers know the extent of the loan forgiveness & payment pause, they’ll be more motivated to refinance loans now. And with rates expected to continue rising throughout 2022, the urgency to refinance debt should be even more pressing for consumers.

Finally, SoFi’s average student loan borrower has an average income of more than 30% over the forgiveness cut-off. According the CEO Anthony Noto this week, the vast majority of its borrowers are not eligible for ANY forgiveness and virtually 0 are eligible for Pell Grant-level forgiveness.

After years of confusion, this moratorium seems to finally be resolved with a finite end in view. Considering student loans were SoFi’s largest and most profitable segment heading into the pause, I’m excited to see what results look like with it turned back on. Margins are already rapidly expanding and growth is already brisk without this large segment in full swing. Student loans will merely add gasoline to the momentum fire.

SoFi saw its student volume rapidly ramp into the last moratorium expiration until it was pushed out further. I expect that ramping to once again occur in a more sustainable and long-lasting manner this time around.

2. The Trade Desk (TTD) -- UID2 & Big Ten Football

a) Unified ID 2.0 (UID2)

Another demand side platform (DSP) -- MediaMath -- announced support for UID2. UID2 -- as a reminder -- is the open internet identifier that The Trade Desk built (but does not own) to replace and augment third party cookies across more channels. It’s good to see the demand side (direct TTD competition) leaning in and embracing this new open internet identifier. To me, it shows that The Trade Desk effectively removed potential conflicts of interest via vesting ownership of UID2. This allowed it to more seamlessly build adoption scale -- and it will still be a prime financial beneficiary. CEO Jeff Green is playing chess while the rest of the industry plays checkers.

“As the industry continues to innovate and work towards an alternative to the deprecation of third-party cookies, we believe it is vital that we partner with our peers and clients to enable their choice of scalable, privacy-conscious identity solutions.” -- MediaMath Chief Partnerships Officer Sylvain Le Borgne

b) Big Ten

The Big Ten Conference’s latest media deal includes a larger array of rights to Big Ten Football games for streaming platforms like Peacock. With live sports representing roughly 90% of the most watched shows in the United States, football dominating American culture and The Trade Desk being the largest demand side player in streaming, this is yet another material tailwind for the already thriving firm.

Click here for my TTD Deep Dive.

3. Duolingo (DUOL) -- Duocon 2022

a) Duocon

Notes from Senior Software Engineer Ananya Rajgarhia:

Rajgarhia went into more detail on the magic behind the newly formed home screen. As a reminder, this is the result of extensive split testing born from its leading market share. The main idea of the new screen is to create a more linear path to leaning. It consolidated features from across the app into this home screen to concoct a more centralized dashboard of progress. The path is constructed -- as always -- to maximize learning efficacy and efficiency. It features things like “spaced repetition” to intelligently source practice content needed by an individual (through its Bird Brain Algorithm) to achieve these objectives. Repetitions become increasingly difficult and also less frequent as a learner gets more comfortable. Other new tools from this upgrade include a guidebook with key grammar tips and concept explanations.

Notes from Duolingo ABC’s General Manager Daniel Falabella:

Falabella elaborated on the structure of Duolingo ABC’s (its Children’s Literacy App). Like Duolingo’s other apps, the company fixated on “not creating a product that felt like taking medicine to a kid.” It wanted it to be fun, playful and -- as always -- effective. Considering a 2nd grader’s reading proficiency is directly correlated with long term quality of life, this is an important product extension to say the least… and it seems to be working.

Duolingo funded a 3rd party study of 105 children and their caregivers. The sample size was admittedly a bit small. Still, the students used Duolingo ABC’s for 9 weeks and saw a 28% boost to their literacy scores. Children also demonstrated a materially stronger motivation to learn. Mission accomplished.

Today, the app is entirely free to use and doesn’t feature advertisements. Duolingo takes its time with product monetization and this one is still too early-stage to extract revenue from. It will monetize eventually.

Notes from Duolingo Math Engineering Lead Sammi Siegel:

Why is Duolingo expanding into math? Similarly to literacy, income and health over the long term are strongly correlated to basic math skills.

This launch will come with the same guiding principal as the rest of Duolingo -- to enhance access to areas of education mattering the most. And with 50% of high schoolers reporting math-related anxiety, this ambition is quite relevant.

Duolingo’s Math App is now beta testing with select students. It offers immersive features like drag and rotate rulers to emulate the hands-on nature of in-person learning. All lessons are randomized so numbers are ALWAYS different and students can always practice with fresh material. The app comes with the same gamification ambitions as the language learning product and is mainly for children -- although it has a brain training function for adults as well. The official app launch will come later this year and the company will, again, take its time with monetization. This will not be a revenue contributor in 2023.

Notes from Co-Founder/CEO Luis von Ahn:

Duolingo recently partnered with the United Nations High Commissioner for Refugees. With just 3% of refugees going to college, Duolingo is fixated on enhancing access for this cohort of individuals. It’s waiving Duolingo English Test fees for these students AND hiring college counselors to consult on the best institutions for them.

In other news, Duolingo launched Cantonese for Mandarin Speakers and English for Bengali Speakers.

b) DET Milestone

Duolingo English Test crossed 4,000 institutions accepting it this past week. That makes it far and away the leader in digital english proficiency exams. And that lead is only growing with its acceptance by all 25 of the highest volume universities in the World. The test is far more convenient for prospective students across the globe vs. driving often several hours to take a test within a strict time slot. It’s also far cheaper than alternatives. Traction and success here is both encouraging and makes a lot of sense. This business is about 9% of total company sales and rising steadily. It now has its sights set on government organizations and has found some early success in Ireland.

Click here for my Duolingo Deep Dive.

4. Penn Entertainment (PENN) -- Rationalization… Finally

Finally, sports gambling app competition is pulling back on ridiculous promotional spend for market share. According to an article in the Wall Street Journal, both DraftKings and FanDuel are making this move to meet more pressing profitability targets. Growth at any cost is no longer in vogue with our tightening macro climate -- cash flow is.

To me, this is when Penn Entertainment and Barstool should start to dominate the industry and make meaningful incremental market share gains. Its Barstool brand has shown a unique ability -- thanks to its passionate 70 million+ cross-platform user base -- to rack up respectable 10%+ share while real rates were negative, cash was free and competitors spent like drunken pirates on promotions. That ability manifested in Barstool’s revenue market share in key states far outpacing its bet (also called handle) share. This was because more of its revenue came from genuine demand vs. free bets. It also manifested in Barstool Sportsbook being the closest among its peers to positive EBITDA. That is the impact of its brand power amid a sea of irrational spend.

Well, that irrational competitor spend is now winding down -- and right before Barstool’s bread & butter football season. That leaves branding within a commoditized space absolutely imperative -- and Barstool delivers that strength. It’s also nice that when it does spend on costly external marketing and promotion, it can do so by tapping into Penn’s $1.7 billion in cash and equivalents and its deeply profitable regional casino business.

Barstool… it’s time to shine.

5. PayPal (PYPL) -- Coinbase & Grants

a) Coinbase

PayPal became a member of the Coinbase Travel Rule Universal Solution Technology (TRUST) network to conjoin efforts on regulatory compliance within crypto. The network is looking to become an industry standard for best in class legal practices within the still nascent space. Other members include Gemini and Robinhood.

This surprised me a bit to be candid. I view PayPal as second to none in terms of regulatory relationships -- and so its partnering with these companies with less governmental clout is somewhat counterintuitive. Why share your advantage with the field? I suspect PayPal will approach this in a way to preserve that lucrative edge. And furthermore, it does fit hand in hand with its partner-first philosophy when it comes to commoditized products like digital currencies will become.

b) Grants

PayPal -- with Vanguard and the National Philanthropic Trust -- debuted a new grant product. The tool allows Grant-makers like donor-advised funds, sponsors and foundations to send expedient electronic grants to charities all from the PayPal digital wallet. 200,000 charities are now eligible to safely and securely receive payments from this tool. The vast majority of charitable giving is still done via paper check and PayPal is looking to change that.

Click here for my PayPal Deep Dive.

6. CrowdStrike (CRWD) -- Accolade

Another week, another research organization telling us that CrowdStrike is best in breed. SC Media -- for the 4th time -- named CrowdStrike the winner of its Best Security Company award. I am not a cybersecurity insider. My expertise is not within this highly complex space. So? I lean on things like market share data and 3rd party, unbiased research to form my opinions on the viability of a company’s tech. And that approach led me to CrowdStrike.

It has doubled its endpoint market share to 13%+ over the past couple years to pass Microsoft as the largest. It is the most independently tested security product in its space, AND it doesn’t pay for glowing reviews like some of its competition does. In the world of cybersecurity, I find this to be in a league of its own in terms of easy to own.

7. Upstart (UPST) -- Delinquencies & a Case Study

a) Delinquencies

Data from Jefferies indicated that Upstart’s delinquencies continued to rise into August to 5.44%. This isn’t entirely surprising, considering industry delinquency rates are ticking up and that Upstart’s borrower cohort is most vulnerable to macro issues. But still, it is undeniably a negative and worth noting.

Upstart’s guidance assumes macro conditions will be about as bad as they can possibly get through the rest of 2022. I expect negative data points like this to continue popping up over the next several months but I also think they’re baked into expectations at this point. I continue to think 2022 will stink for this company and 2023 -- or when macro becomes more inviting -- will look much, much better. If that doesn’t play out as expected, I’ll have to re-evaluate my position.

I’ve said it before and I’ll say it again: The company needs to continue rapidly building its partner list and shifting loan volume away from volatile and timid capital markets. That’s how it builds a more durably resistant business model in the face of future credit downturns. Otherwise, the next time monetary policy turns hawkish, its volumes will again aggressively crater. The partner add pace remains rapid today -- that must continue for this to be a long term winner. Bank partners do pull back to a certain extent on loan originations -- especially unsecured -- amid macro deterioration. But they do so FAR less abruptly than capital market participants like fast money hedge funds.

b) Case Study

Upstart released a case study with one of its smaller partners (Sharonview Credit Union). The overarching takeaways were:

Upstart greatly bolstered its origination volume without Sharonview needing to add staff.

Upstart delivered a large boost to proportion of loans fully automated.

Upstart fostered a boost to member growth.

Upstart facilitated a conversion rate edge as well via the soft credit pull & seamless application process.

Click here for my Upstart Deep Dive.

8. Meta Platforms (META) -- Miscellaneous

Meta is borrowing a feature from a smaller competitor -- “BeReal” -- for Instagram. The tool allows users to “be notified every day at a different time to capture and share a photo” per Bloomberg. The time limit makes these photos more candid and less rehearsed.

Meta settled with Facebook users on location tracking complaints for $37.5 million. Zuckerberg was dropped from an FTC lawsuit as a result.

Sony is debuting a new VR headset. With a potential opportunity as vast as this one is, Oculus will be far from alone in the VR market. To me, this is proof of concept and inevitable if these headsets actually have a strong future.

Facebook resolved an AI content sourcing issue that was showing users strange, irrelevant posts on their feeds. Meta is building a dedicated customer service team to help its users with issues they’re having with content creation and viewing.

9. Olo (OLO) -- New Brand & Danny Meyer

a) New Brand

Olo announced Razzoo’s Cajun Café and its 20+ locations as its newest brand client. Razzoo’s is implementing Olo’s Ordering, Rails and its newest Pay Module. While this past quarter was surely a disappointment, it’s good to see brands continuing to choose Olo for their enterprise technology needs. It’s also good to see continued Olo Pay adoption as that new product gains traction in a wildly competitive space.

Olo’s transaction-based revenue stream directly correlates with consumer health and spending. As inflation raged and consumer confidence tanked, customers traded down in terms of restaurant purchases -- and that is weighing on its growth today. The other negative byproduct of that has been a lengthened sales cycle as enterprise chains focus on mission critical business preservation vs. streamlining operations or finding new growth. This has led to a build-up of brands that Olo is still in the process of fully deploying and revenue being delayed to 2023. Translation? 2022 will be underwhelming and I think results will look much better thereafter. We shall see.

b) Danny Meyer

Danny Meyer (Shake Shack founder & Olo Board Member) made a $250,000 purchase of Olo stock this week. This is a very small piece of his $400 million net worth, but it’s his 3rd buy of the last 18 months for a total of $850,000.

Click here for my Olo Deep Dive.

10. Shopify (SHOP) -- Australia

Shopify Capital -- its merchant credit product -- has expanded to Australia. It’s now offering up to $2.5 million AUD for eligible merchants in that nation. With inflation and macro headaches raging on, this is a timely product launch -- especially as we head into peak shopping season in Australia. This launch followed extensive Shopify market research and surveying revealing that 62% of its Australian merchants were motivated to borrow to fuel their business’s success. Furthermore, over half of the respondents were turned-off from the manual, dense application process.

A key part of this launch is the same seamless, automated application process that has worked so well for the firm in other geographies. Merchants can access these loans directly through their Shopify accounts, do not have to give up equity in their business, and don’t have participate in credit checks (makes me a bit nervous). As a merchant generates revenue, a fixed percent of those daily sales is automatically sent to repay principal. This makes credit quality/delinquencies and merchant liquidity less risky as re-payment cadence is defined. Shopify Capital is already live in the USA, UK and Canada and has seen its origination volume rise by 90% since Spring 2021. Perhaps the 36% sales spike the product delivers (on average) is the reason. This will be another compelling growth lever for the segment to pull.

Click here for my Shopify Introduction.

11. Match Group (MTCH) -- Apple

Match’s Tinder App filed an antitrust suit against Apple in India. The accusations center around forced payment provider usage for in-app purchases. It’s very similar to its battle with Google which resulted in the search giant allowing Match to plug into other payment providers. The regulatory sails are clearly at Match Group’s back with global governmental developments around app store practices gaining more and more steam. Any movement here would be a gross profit margin boost for the dating app organization. That boost also would likely flow down the income statement to bolster earnings growth.

Click here for my Match Group Introduction.

12. Ozon (OZON) -- Earnings

Results:

a) Demand

Orders rose 121% YoY to 90.2 million while active buyers rose 67% YoY to 30.7 million.

Merchants selling on the platform tripled to 150,000 YoY.

Revenue rose 58% YoY to $982.6 million. Gross Merchandise value rose 92% YoY. Marketplace commissions rose 179% YoY.

It continues to build out infrastructure in Belarus and Kazakhstan.

b) Margins

Gross margin improved to 56.8% from 32.1% YoY.

It barely turned adjusted EBITDA positive vs. a -24.3% margin YoY.

Operating margin improved to -13.7% from -33.2% YoY.

Free Cash Flow margin improved to -26.3% vs. -32.4% YoY.

Net income margin improved to -12.3% from -41% YoY.

My Take:

The company is thriving in every sense of the imagination. Malicious action from the Russian Government -- where Ozon presides -- has led to its continued freeze on American exchanges. I do not know when this situation will resolve itself. I do know that when it does, I will likely liquidate my very small stake in the firm. There are plenty of great companies in places like the U.S., Europe, Korea etc. to invest in. I’ll be avoiding Russia and China altogether going forward. Quite the frustrating lesson; I don’t plan to learn it again.

13. Macro

a) Key Data from the Busy Week in Macro:

The Core PCE Price Index came in below expectations at 0.1% vs. 0.3% expected and 0.6% last month.

Q2 GDP came in at -0.6% vs. -0.8% expected and -0.9% last quarter. Following final revisions, we’ll likely be in a recession.

Initial jobless claims came in slightly below expectations. This shows more slack in the labor force for the Fed to get more aggressive on taming inflation.

Purchasing Managers’ Index (PMI) Data:

The Manufacturing PMI came in below expectations at 51.3 vs. 52.0 expected and 52.2 last month. Anything above 50.0 still marks expansion.

The Service PMI came in well below expectations at 44.1 vs. 49.2 expected and 47.3 last month.

New home sales materially missed expectations. Pending Home Sales actually sharply beat expectations at -1.0% vs. -4.0% expected and -8.9% last month.

There was a 2-year note auction at 3.307% vs. 3.015% last month. Not great.

Core Durable Goods Orders beat expectations at 0.3% month over month growth vs. 0.2% expected.

Personal spending came in at 0.1% month over month growth vs. 0.4% expected.

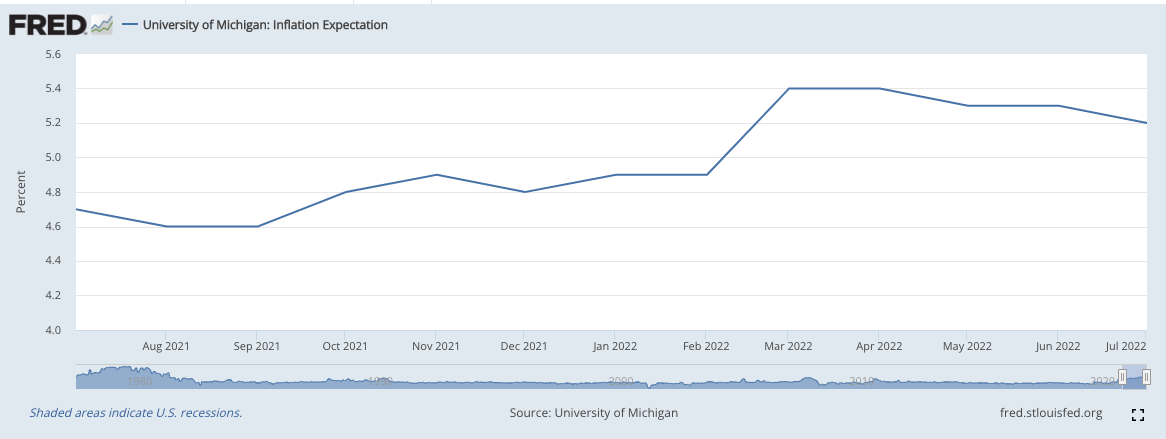

University of Michigan consumer expectations and sentiment both SHARPLY beat expectations at 58.0 and 58.2 respectively vs. 54.9 and 55.1 expected respectively.

UofM 1 year Inflation Expectations also continue to slowly tick down:

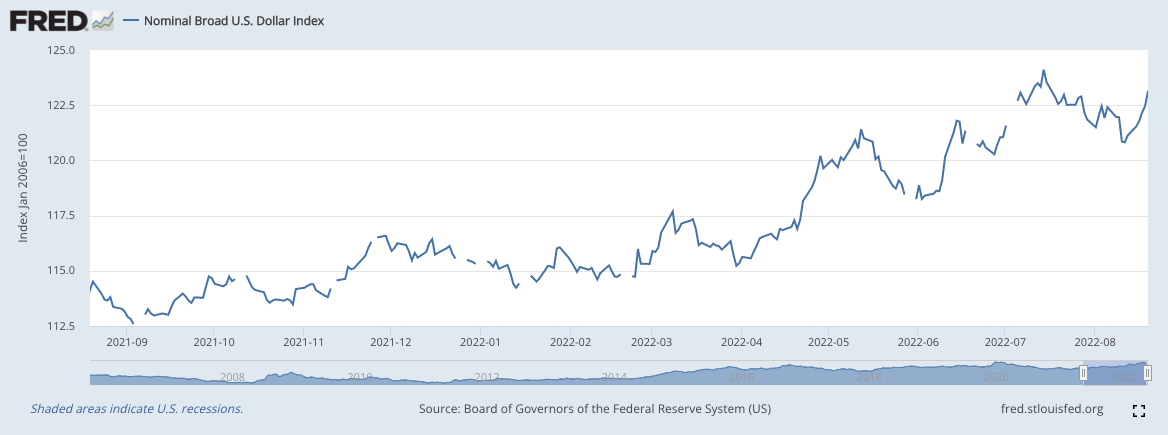

In more global news, the ECB finally seems committed to appropriately hawkish policy. It’s forecasting double or even triple rate hikes in the near future. That could be a much-needed headwind for U.S. Dollar strength. Good news, but the trend on the dollar today remains stubbornly higher:

Powell spoke for a few minutes at the Jackson Hole meeting this past week. He views the current Federal Funds Rate as neutral and is adamant it needs to enter restrictive territory for an extended period of time to combat inflation before rate cuts can happen. He used the word “pain” quite a bit in his speech. Metrics like sinking inflation across the CPI, PPI and PCE readings this month, a technical recession, and now underwhelming PMI readings point to economic cooling.

Conversely, durable consumer confidence and still too much slack in the work force via low jobless claims both give it incentive to keep hiking. And I (and everyone else) expect it will. The labor market remains somewhat strong (although multiple job rates are soaring) and so the main focus is rightfully on prices. While commodity prices continue to fall (Bloomberg’s commodity index is quickly 12% off of 2022 highs), stickier pieces of inflation like rent should last longer.

We’ll see how all of those pushes and pulls play out -- but my optimism is slowly growing.

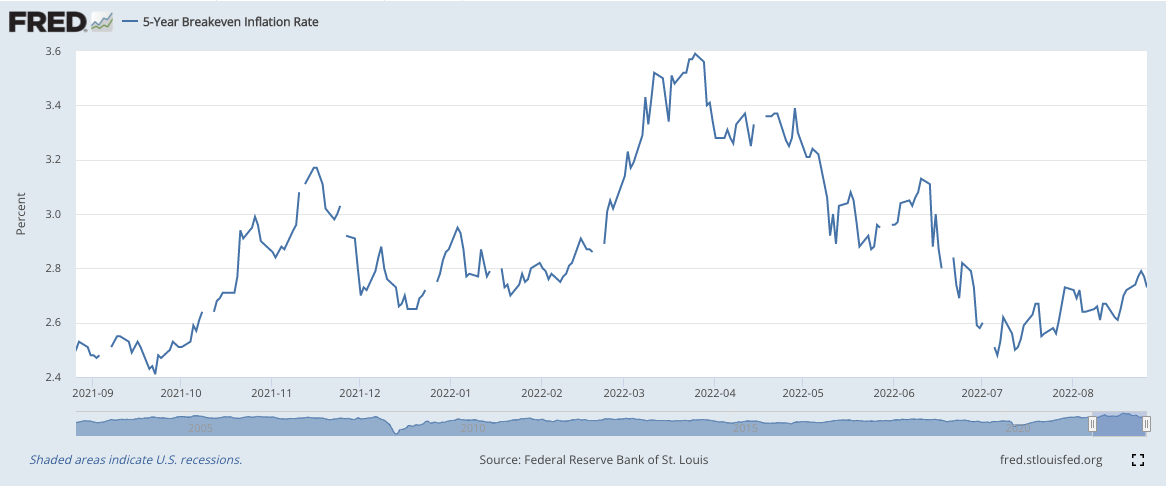

5-year Breakeven Inflation Expectations ticked down this week:

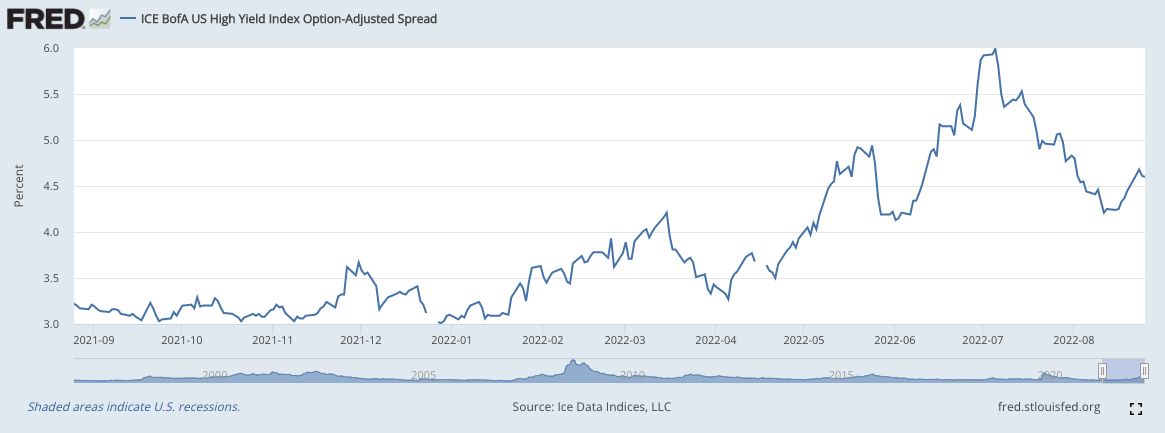

High Yield Option Adjusted Corporate Credit Spreads also encouragingly ticked down this week:

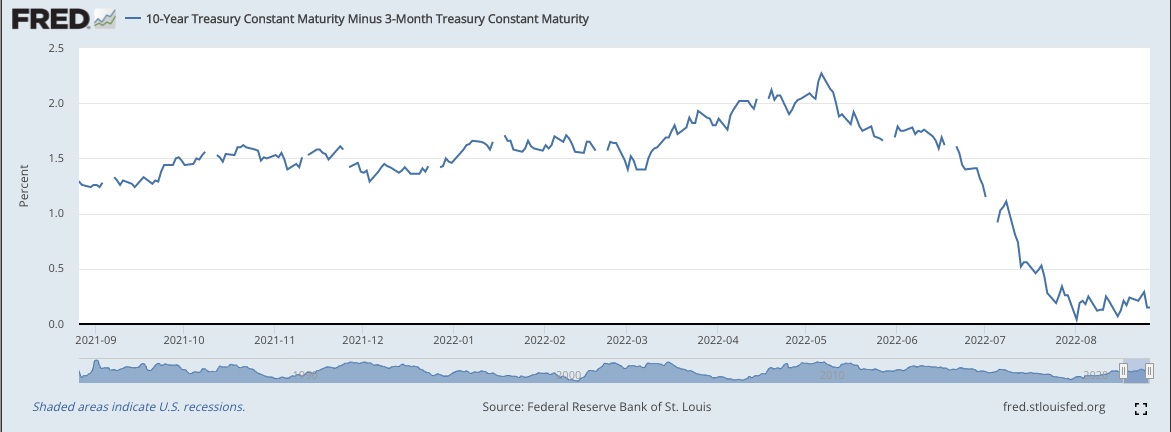

The 10 Year-3 Month Yield Curve continues to flirt with inversion (a strong recession indicator):

Please note that recessions are negative for just about everything except for discount rates on growth stocks. A recession would eventually force the Fed to turn dovish and make longer term, speculative cash flows worth more. It would also make growth more difficult to come by which would lead to structural compounders becoming more rare and coveted. I’m not saying us growth investors should root for a recession, but we shouldn’t fully loathe one either.

b) Level-Setting the Data

The economic cracks are becoming deeper and clearer as the Federal Reserve’s policy begins to work (takes several months for monetary policy to fully work). The Fed remains committed to eroding what it sees as still frothy demand… and hopes that demand destruction offers a positive byproduct of allowing supply chains to recalibrate. Commentary out of Cisco last week hints at that possibly being the case.

So? While I don’t agree with some bright people on a dovish pivot coming in the next few months, I also do not see continued hawkishness lasting that far into 2023. That opinion is supported by futures markets not really showing any incremental Fed hawkishness following the week and probabilities of smaller future rate hikes rising. But obviously I could always be wrong!

I can see the light at the end of this long, intimidating tunnel -- and it grows brighter as inflation readings abate. There were a few intimidating data points this past week, but the positives continue to outweigh the negatives in my view. That could always change, but it did not this week. I remain more eager to buy into multiple compression than I have been in months.

14. My Activity:

I added to SoFi and Revolve during the week. My cash position is currently 18.9% of my holdings.

If you’d like access to my real time portfolio and to sign up for text notifications when I transact, my friends at Savvy Trader now make that possible. It’s 100% free and can be accessed via the button below. Please note that the MSOS position is a placeholder for my positions in Green Thumb and Cresco Labs while OTC stocks are added to the platform. You can also re-create your very own portfolio through Savvy Trader.

If you or someone you know may be interested in sponsorship/advertising opportunities with Stock Market Nerd, please let us know! That is how we keep our content entirely free.

Love your weekly write-ups. Thanks!