News of the Week (April 8 - 12)

News of the Week (April 8 - 12)

Amazon; Google, Nvidia & Intel; Meta; Lulu; Piper Sandler Teen Survey; SoFi; J.P. Morgan; Lemonade; Uber; Apple; Market Headlines; Macro; Portfolio

1. Amazon (AMZN) – Shareholder Letter, India & Piper Sandler

a. CEO Andy Jassy Shareholder Letter:

Amazon CEO Andy Jassy published his latest shareholder letter this past week. It dove into how Amazon thinks and how it has configured its business to drive historic success. It was a lengthy, yet valuable piece for understanding why you own what you own. Here are the highlights:

On Primitive Services:

The main theme of this letter revisits a 20-year-old Amazon idea about “Primitive Services.” In the firm’s mind, these are “discrete foundational building blocks woven together in whatever combination desired.” It famously introduced this idea in 2003 in its AWS vision letter. These services fixate on unbundling use cases to perfect them one at a time. The roadmap of development is guided solely by customer pain-points, and each service is beautifully tied together via slick application programming interfaces (APIs) to ensure the pieces are cohesively, not disparately, conjoined. This allows Amazon to emulate service customization without needing to build from scratch each time a merchant wants something slightly different. It creates a la carte style client purchasing. Why is this important? Because merchants are all unique, as are their needs. Think of primitive services like atoms. They’re indivisible, but can be combined in nearly-endless ways into different molecules to create a plethora of end products.

Jassy took us through how Amazon created this approach and how it’s implemented. Looking backwards, Amazon’s fulfillment network was the example used. The firm first built a primitive service to perfectly handle and distribute inventory for Amazon only. It then leveraged this service and opened it up to 3rd party merchants. This created operating leverage on existing capital infrastructure while giving its marketplace a broader array of inventory. He spoke about how Amazon applied the exact same idea to its payments, search, and other microservices like last-mile delivery. These needed to exist separately from one another, rather than being inherently stapled together, which Amazon learned the hard way through early failure. At the very beginning, it let Target.com use its tech to power their storefront and “jumbled” services together with some customization built-in. Instead, that design required partitioning of products into primitive services, which eventually laid the groundwork for AWS.

This idea seems to stand in stark contrast to the “vendor consolidation” and “platformization” software themes of 2023 where combining products is preferred… but it doesn’t. Amazon is still offering an overarching platform, just a malleable platform that looks different for different clients. This ensures that every single ingredient in the overall platform is best-in-class and used only when needed. Primitive services can be enjoyed by Amazon, leveraged by clients in isolation (like with Amazon Shipping for last-mile delivery for example), or weaved together to create something commonly needed by client needs like Buy with Prime (BwP) or Fulfillment by Amazon (FBA). Per Jassy, building with this mindset amplifies “freedom” of creation and fosters many more ways to drive profitable growth. Jassy discussed how Amazon failed early on in healthcare and robotics. It didn’t begin to succeed until it began to embrace this exact same philosophy of building one hyper-localized service at a time to solve one, specific pain-point.

The Next Primitive Service Focus Areas:

Generative AI (GenAI) is the next pillar of primitive services for Amazon. I’ve previously shared the three layers of GenAI. Layer one encompasses foundational models (FMs) and involves the chip and hardware infrastructure that goes into creating them. Jassy talked about how Nvidia’s graphics processing units (GPUs) have been used to create most FMs to date. However, advancements in Amazon’s Trainium (for model training) and Inferentia (for model inference/prediction) chipsets are powering new models of best-in-breed players like Anthropic and Hugging Face. He mentioned significant performance, cost and memory bandwidth upgrades for the new versions of these chips, as well as its Graviton central processing units (CPUs) for general compute. Amazon’s SageMaker is its managed means of guiding developers through the model creation journey in a more intuitive manner. It’s sort of like an instruction template. SageMaker is helping Perplexity AI train models 40% faster and Workday reduce inference latency by 80%.

Layer two is where companies leverage FMs to create niche, localized, and customized models. Amazon Bedrock is its big product here, which already has tens of thousands of customers and a broad set of available foundational models to utilize.

Layer three is the consumer application layer, where its shopping assistant (Rufus), automated AWS coding (Amazon Q) and Alexa upgrades will come into play. The first spending wave has been within layer one as hyper scalers and consumer internet giants race to put infrastructure in place so they can enjoy monetization in the other two layers down the road.

On E-Commerce & Logistics:

Jassy essentially took a victory lap here on how rapidly Amazon has been able to optimize its supply chain via regionalization and same-day facility expansion. He reviewed how these factors have cut Amazon’s per unit costs, with improved delivery speed and customer service, for the first time in six years. The new layout and its last-mile delivery investments are also freeing Amazon to be a bigger player in perishable goods as well as everyday essentials. This category grew by 20% Y/Y in Q4 2023, which was a new disclosure and is encouraging. He also told investors that more reductions in per unit fulfillment costs were coming in 2024. Focus areas will evolve from localization and better supply chain monetization to inbound fulfillment optimization and inventory placement. Its newer same-day facilities and inventory algorithms are placing inventory closer to the final predicted destination more often. That drives down cost.

In other e-commerce news, Mexico became its latest country to turn profitable. It generally takes Amazon about a decade to deliver this inflection in new markets, and it remains confident that every single newer market is on that trajectory.

“There has never been a time in Amazon’s history where we’ve felt there is so much opportunity to make our customers’ lives better and easier. We’re incredibly excited about what’s possible, focused on inventing the future, and look forward to working together to make it so.” – CEO Andy Jassy

I was already a big fan of Jassy’s. The more I hear him talk and read his thoughts, the more I like him.

b. India

A few years ago, Amazon lost a bidding war to Walmart in its quest to buy a majority stake in Flipkart – the Indian e-commerce giant. Following that development, Amazon pushed aggressively into the market and claimed the top site traffic spot as of January 2024. Still, Flipkart leads in overall e-commerce market share… but Amazon has its ambitions set on a larger piece of the pie. This week, it announced “Bazaar” as a new, low-priced e-commerce site in that market. It will sell fashion and home goods for prices ranging from $2.39 to $7.21.

India is an incredibly compelling international growth market. Its population is young, giant and growing while its middle class continues to expand too. Its government is both business and US friendly; its economy is poised for 6.5% growth this year as it races to become the 3rd largest in the world. This news makes a ton of sense as Amazon gears up to invest $26 billion in India over the next 6 years.

c. Piper Sandler Data

Amazon remains the most widely used e-commerce site among teens. 61% of respondents surveyed by Piper Sandler use it vs. 57% Y/Y. This just keeps ticking higher & higher for every new survey released.

2. Alphabet (GOOG), Nvidia (NVDA) & Intel (INTC) – Semiconductor Market News

a. Alphabet’s Chip Announcement

This week, Google announced its latest chipset called Axion. Axion is based on Arm Holdings architecture and is a CPU product. Google has been hard at work on custom chipsets for about a decade, and Axion is the latest result of that work.

Importantly, Axion will be used for general compute (GP) purposes. This isn’t like Amazon’s Trainium and Inferentia chips that will be for high-performance compute (HPC) apps. That makes this new release more of a competitive threat for Intel and AMD than for Nvidia. HPC applications, powered largely by Nvidia’s GPUs today, have unlocked more data center flexibility, utility and potential. But? GP is not going to go away according to Google. Google sees it as “remaining a critical portion of cloud-based workloads” and Axion is meant to claim a piece of that specific market. Axion can greatly help with overall cloud cost optimization; HPC is very expensive and it doesn’t make sense to use it unless you need to.

In the release, Google wrote about GP CPU innovation slowing and falling too far behind HPC. If the gap widens too much, GP becomes a performance and efficiency bottleneck and cannot be effectively utilized. Axion is Google’s strategy for ensuring that the gap doesn’t widen too much, while also creating new revenue opportunities.

Per Google’s internal data, Axion delivers 30% better performance than the next-best Arm-based GPU workloads and 50% better performance than other current generation competition. It’s also 60% more energy efficient than those competitors. Amazon says similar things about its Graviton CPUs. Meta, which delivered more AI semiconductor releases covered the next section, and other chipmakers do too. As these claims are largely internally-derived, take them with a grain of salt.

Axion was built to work seamlessly with Arm’s infrastructure and workloads. This will make it easier for Arm’s “tens of thousands of cloud customers” to deploy their assets in Google Cloud. Early on, CrowdStrike, Datadog and Elastic have been named as early users.

b. Competition Heating Up

Intel released its latest AI chip called Gaudi 3. It will directly compete with Nvidia’s Hopper, Grace and Blackwell systems. Per Intel, it’s 2x more energy efficient and can run models 50% faster than the Hopper 100 (H1000) GPU. Nvidia has already released two higher-performing chips for these use cases since the H100, but this is still considered a large leap forward for Intel.

3. Meta Platforms (META) – More Semiconductor News & Piper Sandler Survey Data

a. More Semiconductor News

While Nvidia’s chipsets will power a large chunk of Meta’s next-gen data center and GenAI infrastructure, Meta’s Meta Training & Inference Accelerator (MTIA) AI will help vertically integrate semiconductor creation for certain use cases. Just like Amazon… just like Google… just like Apple. These use cases for Meta include its advertising and discovery algorithms, which are quite unique workloads. That uniqueness makes internal design and manufacturing a more rational move, given Meta can create them precisely for the unique features it needs. Per the team, the process is more efficient than delegating to a 3rd party.

The potential use cases are expanding with the second version of MTIA AI chips announced this past week. The new chipset can handle more advanced recommendation and targeting workloads, along with unlocking “new experiences,” with better efficiency and performance (so lower cost). It plans to continue investing more aggressively here in the coming years to optimize efficiency of its tech stack and enable more seamless, flexible scaling. Early success is emboldening its approach despite Meta’s massive orders for Nvidia’s advanced chips. MTIA version 2 is now live in Meta’s data centers and is being used by developers to build new models and applications with the firm.

b. Piper Sandler Data

So teens in the U.S. don’t use Facebook anymore, right? Right? Not so fast. Facebook monthly usage among teens rose to 32% and set a 4 year high in Piper’s data release from this week. It attributes this to improving advertising products and discovery algorithms.

Instagram saw its largest rise in favorite app preference since TikTok debuted with 7 points of additional share Y/Y. It’s now the 2nd favorite teen app behind TikTok as it passed a struggling Snapchat. Piper called time spent trends there “encouraging.” It remains the most used app in the U.S. with its lead growing from 5 pts to 8 pts Y/Y.

In other Meta news, Piper Sandler’s advertising channel checks were quite positive and led to it raising estimates from Q2-Q4 by about 1%.

4. Lululemon (LULU) – Valuable Brand & Company Data

a. Store Traffic Before & After Alo Store Openings

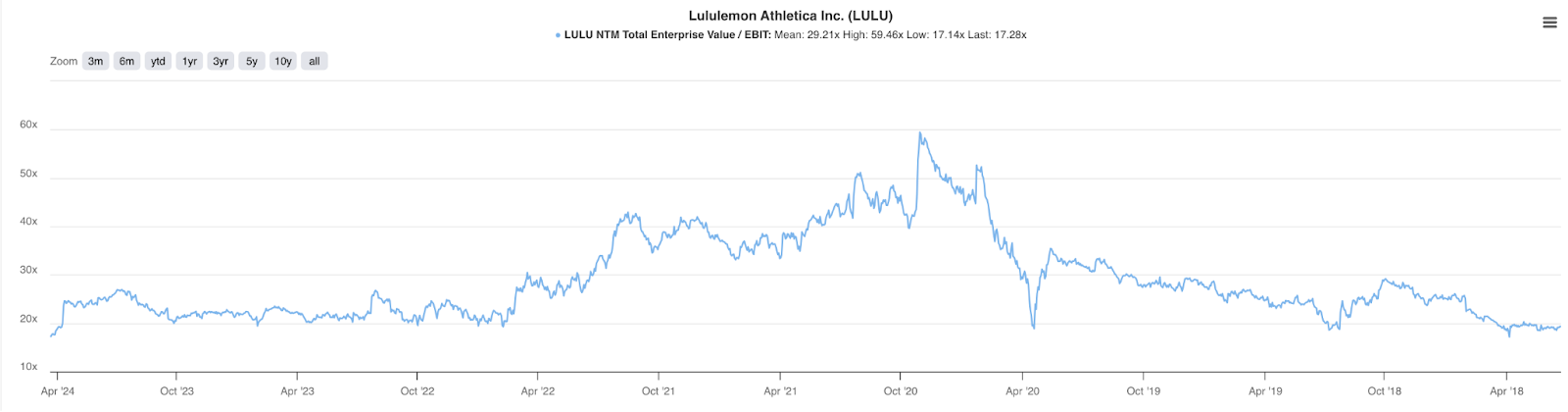

Morgan Stanley published research this week on same-store traffic trends for Lulu stores. It covered 5 markets and measured traffic changes for Lulu stores where a nearby Alo store opening occurred. The takeaway is positive. 6 months before and after an Alo opening, Lulu’s average store traffic actually accelerated by 2 points. How can this be? While Alo (and Vuori) continue to grow in popularity, so does Athleisure as a percent of total apparel spend. So while these two brands are succeeding, that is in no way preventing Lululemon from finding more of its own success. It was never going to own an entire $350 billion market, and perhaps these two budding brands are raising awareness and purchase intent for the category overall. That’s good for the king of this space, and that king is clearly Lululemon. And? The king is trading near 6-year EBIT multiple lows (thanks for the chart, Tikr.)

Piper Sandler Teen Survey for Lulu Specifically

Overall, Lululemon maintained the #3 spot in apparel (#3 for woman and #5 for men), but mindshare fell by a point Y/Y.

Among upper-income individuals for apparel overall, it gained 0.5 points of share Y/Y with women and lost 0.35 points with men.

It remains the top overall brand for affluent women and #3 for men.

Among average-income individuals for apparel overall, it lost 1.20 points of share. Piper attributes this to its premium pricing point and fragile macro.

I agree, and also think Q4-2023-Q1 2024 inventory issues at some of its stores amplified this result.

#1 in brands starting to be worn for females and #4 for men. It is not in the brands no longer worn section.

For athletic apparel, it stayed #1 overall among affluent females and took a whopping 2.75 points of incremental share Y/Y. It’s #4 for affluent men and #2 overall behind Nike.

Alo rose to #7 for athletic apparel brands among affluent females.

Vuori reached #10 for favorite athletic brands among affluent males.

Within handbags & accessories, this company continues to kill it. It moved from #6 to #5 for handbags with 6% favorite brand market share (vs. 2% just 2 years ago). It gained 2.25 points of additional share here Y/Y.

Piper Sandler maintained its overweight rating on Lulu and a $470 price target following the release of this new data.

This data isn’t uniformly positive, but it is predominantly positive and more upbeat for Lulu than most of the other brands mentioned. I think improving the inventory situation this quarter, easier comps through the year and hopefully improving consumer confidence as icing on the cake will make the negative sentiment here prove short-lived. The company has been a stellar performer for multiple decades and across cycles. One very small annual guidance miss is not going to chase me out of this one. I’d need to see much more evidence of brand deterioration, which I don’t expect to come. We shall see.

5. More from the Piper Sandler Teen Survey – Nike(NKE); Chipotle (CMG) McDonald’s (MCD); Starbucks (SBUX) & Many More

Overall, self-reported teen spending fell 6% Y/Y while beauty rose to its largest wallet share level since 2018.

Among Consumer Internet Brands Covered (Besides Meta & Amazon):

Pinterest is doing well with monthly usage rate rising from 35% to 36% Y/Y.

Snap is struggling. Piper saw a “sharp engagement drop, which is one of the worst sequential results” it has ever seen.

Roku remains the top CTV operating system and Spotify the top music streaming app. Trends are pretty stable for Roku, but share fell from 70% to 67% Y/Y for Spotify.

Among Apparel & Athletic Brands Covered (Besides Lulu):

Nike is #1 for apparel, athletic apparel, footwear and athletic footwear, but is losing share across the board. In athletic footwear specifically, it lost a full 3.3 points of share since the fall 2023 report, with On Running, Hoka and New Balance claiming that piece of the pie. Piper Sandler thinks this is due to Nike’s “lagging innovation.” Skechers was called out as another brand that is performing very well.

Under Armour, VF Corp (NorthFace and Vans) are struggling.

Foot Locker is struggling.

Among Food & Beverage Brands Covered:

Chipotle maintained its #3 overall restaurant spot, but lost more share to Chick-fil-A within the average income cohort.

McDonald’s is top 5 in both food (#2) and drinks (#3).

Texas Roadhouse cracked the top 5 for favorite restaurant brands as the only full-service player. It edged out Olive Garden and is top 5 for both upper and average income.

Raising Cane’s cracked the top 5.

Chick-fil-A (private) is tops across both genders and income brackets.

Dunkin Donuts fell out of the top 5 for upper income teens.

Starbucks is #1 across all income levels for beverages.

Celsius has a 17% mindshare vs. its 11.5% U.S. market share, which points to more gains ahead.

Clif Bar (owned by Mondelez) was the #1 brand overall in proportion of respondents planning to consume more of it.

Beyond Meat is struggling with 22% of people willing to try it vs. 40% 3 years ago. I guess fake meats with ingredient labels that resemble science experiments were a fad. Shocker.

6. SoFi (SOFI) – Shareholder Letter & a Channel Partner

a. Shareholder Letter

CEO Anthony Noto published a shareholder letter this past week. Most of it dug into the business model, which we cover in detail in this newsletter. Still, there were a few interesting notes. First, Noto reiterated his intention of turning SoFi into a top ten financial institution. He also reiterated that continued tangible book value and GAAP net income growth will come this year. Finally, for the tech segment, he called existing client adoption of its risk data pipeline and market “rapid.”

“The benefits of our strategy have only started to come to fruition thanks to a uniquely diversified business that is unmatched by any traditional or digital-only provider in our scale, capabilities and competitive advantage.” – CEO Anthony Noto

b. National Association of Realtors (NAR)

SoFi and the NAR announced a new mortgage partnership. Together, NAR members and clients will get preferred and discounted mortgage rates, as well as student loan refi and personal loan offers from SoFi. Mortgages are SoFi’s newest lending business. It’s only a few quarters removed from fixing back-end issues and getting the product ready for prime time. And since? Mortgage rates have skyrocketed to greatly hurt market demand. Those rates are likely near a cycle peak right now. As mortgage rates fall and mortgage demand accelerates, this is how SoFi can more easily gain traction. It’s much easier to use channel partners to grow brand and product awareness out of the gate vs. trying to do it all on your own.

SoFi will still conduct external marketing for this product, but the NAR channel is inherently more relevant, aggregated and targeted as a marketing channel partner to pursue. Like CrowdStrike uses AWS to accelerate growth… like Tesla uses Uber to sell more cars… like Progyny uses Blue Cross Blue Shield to add more clients… SoFi is using NAR to shorten the path to mortgages becoming a more material part of this business. As an important aside, that will make SoFi’s credit book more resilient across cycles as the potential shift from unsecured to secured debt unfolds. I’m a big fan of this news.

7. J.P. Morgan (JPM) – Earnings Summary

“Many economic indicators continue to be favorable. However, we remain alert to a number of significant uncertain forces. First, the global landscape is unsettling – terrible wars and violence continue to cause suffering, and geopolitical tensions are growing. Second, there seems to be a large number of persistent inflationary pressures, which may likely continue. And finally, we have never truly experienced the full effect of quantitative tightening on this scale. We do not know how these factors will play out, but we must prepare the firm for a wide range of potential environments to ensure that we can consistently be there for clients.” – CEO Jamie Dimon

Results:

Beat reported revenue estimate by 0.5%.

Beat $4.16 GAAP EPS estimate by $0.28. A $725 million boost to expected FDIC special assessment charges shaved $0.19 off of GAAP EPS.

Comfortably beat return on equity & asset (ROE & ROA) estimates.

Loans and deposits organically grew by 3% Y/Y and 0% Y/Y, respectively.

Net interest income rose 11% Y/Y (5% organic growth).

Please note that the First Republic acquisition propped up growth through most of 2023 and into this quarter. That deal closed on May 1st, 2023, meaning there will be more inorganic growth for one more partial quarter before things normalize. Separately, Q4 2023 profits were hard hit by an FDIC assessment.

Balance Sheet:

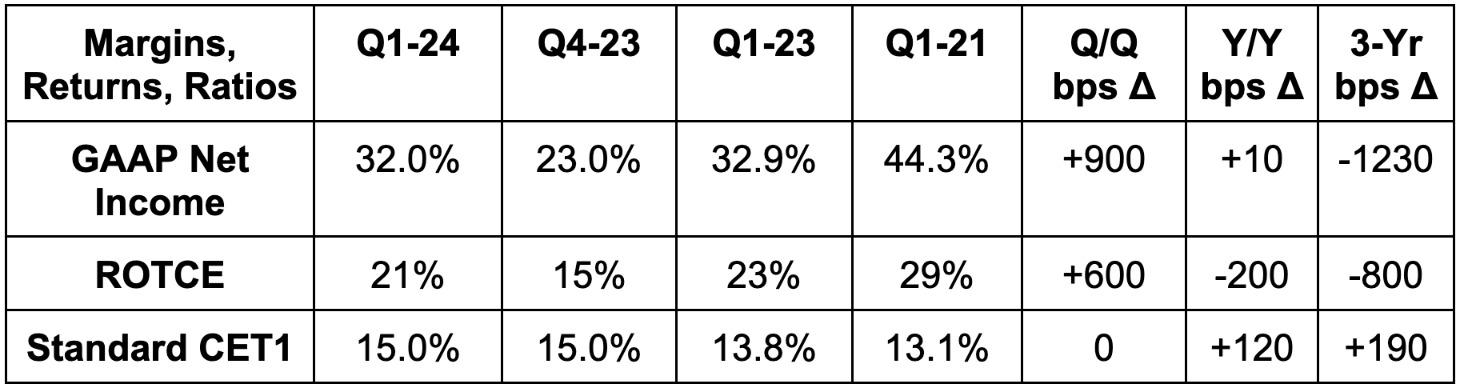

$1.88 billion credit loss provisions vs. $2.76 billion Q/Q & $2.28 billion Y/Y. This included $2 billion in net charge-offs, but a small $72 million reserve release. That hints at credit deterioration potentially moving into the rearview.

As you can see above, its 15.0% standard CET1 ratio is 200 bps above its 11.5% minimum.

Dividends rose 15% Y/Y to $1.15.

Diluted and basic share counts both modestly shrank Y/Y via buybacks.

Return on assets of 1.36% compares to 1.38% Y/Y.

Its total capital ratio is 18.2% vs. 17.4% Y/Y.

Its tier 1 leverage ratio is 7.2% vs. 6.9% Y/Y.

Outlook & Valuation:

The firm raised its net interest income guidance by 2.2% and raised its total expense guidance due to FDIC assessments. It reiterated sub 3.5% card net charge-off rates. The company trades for 12x earnings, with earnings expected to grow by -2.1% Y/Y.

8. Lemonade (LMND) – CPI

As we frequently write about, inflation is especially tough for the insurance industry. Consumer claims rise freely with rising prices. The premiums collected from those plans cannot be adjusted in real-time to reflect that reality. These premium hikes must be approved by regulators, and those regulators are slow. Furthermore, there’s another time lag between when hikes are approved and when they can actually be implemented the following year. So? When we get sky-high inflation like we did in 2022-2023, profitability for the space is greatly pressured. We’ve seen large incumbents even pull out of some markets based on the harsh backdrop. Lemonade has also greatly pulled back on growth in many geographies and products as a result of this too.

The March consumer price index (CPI) certainly wasn’t the most encouraging report (producer price index (PPI) looked a lot better). But? A large portion of the hot reading came from sky-rocketing auto insurance rates. Auto insurance rates jumped by 22.2% while auto maintenance rose by just 8.2%.

To me, this is a clear sign that regulators are finally catching up. That will make all of these companies more profitable and will again embolden Lemonade to re-accelerate its growth spend, which tanked Y/Y in 2023. And we do have a bit of evidence for what this can look like. Europe has much more favorable regulation for insurers. They have more freedom to adjust rates on their own. And? Lemonade’s strongest geography right now is Europe. The macro-based weakness in the U.S. fading away would surely be great news for its largest market becoming healthier once more.

9. Uber (UBER) – More Ads

Uber is debuting a TikTok-like discovery feed to give restaurants another means of promoting their offerings. While the intent of this is better discovery, my mind immediately goes to more sponsored listing opportunities. Merchants will surely want to pay up for better placement within Uber’s gigantic consumer network. That advertising revenue will be among Uber’s highest margin revenue, and should be one of many pieces to deliver more operating leverage ahead.

10. Apple (AAPL) – Glowing Upgrade & More

Apple (AAPL) caught a glowing upgrade from Bank of America on what it sees as significant gross profit margin upside due to things like input cost levers and premium product mix shift. That will drive earnings growth, if accurate. It raised its 2026 gross margin estimate from 45.9% to 47.5%, which compares to 46.2% consensus. This meshes well with IQE news commentary on a strong 2024 orderbook. IQE is an Apple supplier.

And in more semiconductor-related news, Apple plans to release a new Mac line with its newest M4 processors. These are expected to drive significantly more GenAI utility.

Bloomberg reported that Apple’s iPhone production in India doubled Y/Y in 2023 as it tries to diminish Chinese manufacturing reliance.

Chinese iPhone demand remains challenging, per Wedbush channel checks.

11. Market Headlines

Microsoft will invest $2.9 billion in Japan for cloud computing. It is also building an AI Hub in London.

Taiwan Semi’s March revenue report implies Q1 revenue for the firm that is 1.7% ahead of consensus heading into the release.

Uber and Lyft have delayed plans to exit Minneapolis after the city pushed back implementation of new minimum wage laws. These laws would effectively make ride sharing companies pay workers a significantly higher minimum wage than everyone else is required to. Does that sound fair? No, no it does not.

12. Macro

Inflation Data:

The Consumer Price Index (CPI) rose by 3.5% Y/Y for March vs. 3.4% expected. This compares to 3.2% last month.

The Core CPI rose by 3.8% Y/Y for March vs. 3.7% expected. This compares to 3.8% last month.

The CPI rose by 0.4% M/M for March vs. 0.3% expected. This compares to 0.4% last month.

The Core CPI M/M for March rose by 0.4% vs. 0.3% expected. This compares to 0.4% last month.

The Producer Price Index (PPI) rose by 0.2% M/M for March vs. 0.3% expected. This compares to 0.6% last month.

The Core PPI rose by 0.2% M/M for March vs. 0.2% expected. This compares to 0.3% last month.

The Export Price Index for March was 0.3% M/M as expected.

The Import Price Index for March was 0.4% M/M vs. 0.3% expected.

Michigan 1-year and 5-year Inflation Expectations for April both rose M/M and were hotter than expectations.

Consumer & Employment Data:

Michigan Consumer Sentiment and Expectations both missed expectations.

Initial Jobless Claims were 211,000 vs. 216,000 expected.

Inflation data continues to be less promising so far in 2024 vs. the latter end of last year. The PPI was certainly a needed cool-to-inline datapoint just like the March PCE was. All three Q1 CPI readings were notably hot and have made me a bit more cautious for the time being. I still expect disinflation to continue playing out in 2024 and I still expect 1-2 rate cuts. I would need more evidence of re-accelerating inflation to change my opinion and don’t see that coming. The GDP sugar high from recovering supply chains will be lapped in the 2nd half of the year, while housing inflation should begin to reflect the encouraging real-time data we’ve seen over the last several months. Red hot auto insurance inflation will also be very short-lived, and that drove the hot CPI this month.

Candidly, I don’t care about when the first cut comes. I care that the next move will be a cut and that we avoid hyperinflation and a severe recession. I still view doing so as the most likely outcome and will continue to absorb all incoming data to maintain or alter that view.

13. Portfolio

a. Management

As I said on X this week, I’m in wait-and-see mode in terms of cash and portfolio management. It has been a fantastic 7 months for equity markets. We are due for a pullback, and a few percent from all time highs is not something that I consider meaningful.

Still, I don’t see very many compelling discounts today and I don’t feel motivated to create extra liquidity to aggressively add to current stakes right now. I also don’t feel a sense of urgency when it comes to raising cash in the current portfolio. Either Mr. Market gives me a deal and that sense of urgency builds, or things keep ripping higher and I gradually re-enter trim into multiple expansion mode. For now, I’m doing very little. I did shift more Match equity into Lululemon this week as it hit my add target of $340. Last week, I said I would deposit instead of trimming Match to do this if I had the available funds. I have them, but I changed my mind as my confidence in Match dwindles further.

b. Housekeeping

A bit of housekeeping this week. I am changing the portfolio performance start date from July 1, 2022 to January 1, 2023. My portfolio size exponentially grew right up until 2023. That’s when the account became large enough so that deposits as a percentage of total size normalized from double or triple digits to single digits. I’m sure some of you have noticed the changes in holding percentages have greatly slowed over the last few quarters as this has unfolded. Including pre-2023 data distorts returns and makes anything I was holding when the account was tiny disproportionately important. And specifically, Meta was the vast majority of this account, while I didn’t hold any losers during that time period in it. That reality makes my returns since inception look unfairly phenomenal, when that’s really just because Meta performed well and I owned other stragglers in different accounts (mainly Robinhood). January of last year is when all of my holdings were officially in one place and when the return data starts to be accurate.

I would like to point out (as consistent readers already know) that the Stock Market Nerd portfolio is beating every single benchmark out there comfortably with the unchanged July 2022 start date. That was the case as of the last update I offered in the newsletter and it is the case now (note that my lead over the Nasdaq would have been about 0.61% lower had the Schwab data been updated before I scheduled this to publish).

I say this to make it painfully obvious that I’m not making this change to make my returns look good. If I were, I would have gone back to January 2020 or January 2019 to make the lead larger and far more permanent (longer time period), but I didn’t because (again) that was not my intention. I’m not going to go out of my way to look bad (or good!) when January 1, 2023 is the most intuitive start date here.

Have a great weekend!