News of the Week (December 11 - 15)

News of the Week (December 11 - 15)

Quick Service Restaurant Intro; Adobe; SoFi; Disney; Amazon; Uber; Meta; Ad Market; PayPal; Match; Earnings Roundup; Macro; Portfolio

Today’s Article is Powered by my Favorite Brians Over at Long Term Mindset:

1. Quick Service Food & Beverage Intro

a. Setup

Over the next quarter or so, I will be publishing investment case articles on companies in the quick service restaurant (QSR) industry. To avoid sending a 100-page article, I’m going to send out mini dives into two companies from the landscape at a time. The first piece will be published later this month and will cover Cava and Sweetgreen.

I think this is a better format than the prior deep dives. It will be 90% as detailed as those were, with 100% of the important detail, and I’ll be able to send them out more frequently. This way, the information will be more current and more digestible. Furthermore, I think this approach will give you a better view of my investment thought process. It will also allow you to learn more about the sector overall and compare similar business models. As generalists, it is easier to build conviction by studying multiple companies in a sector rather than a single company in isolation. This tweak is my way of pulling back the curtain on how I dissect a new sector.

b. Sector Demand Intro

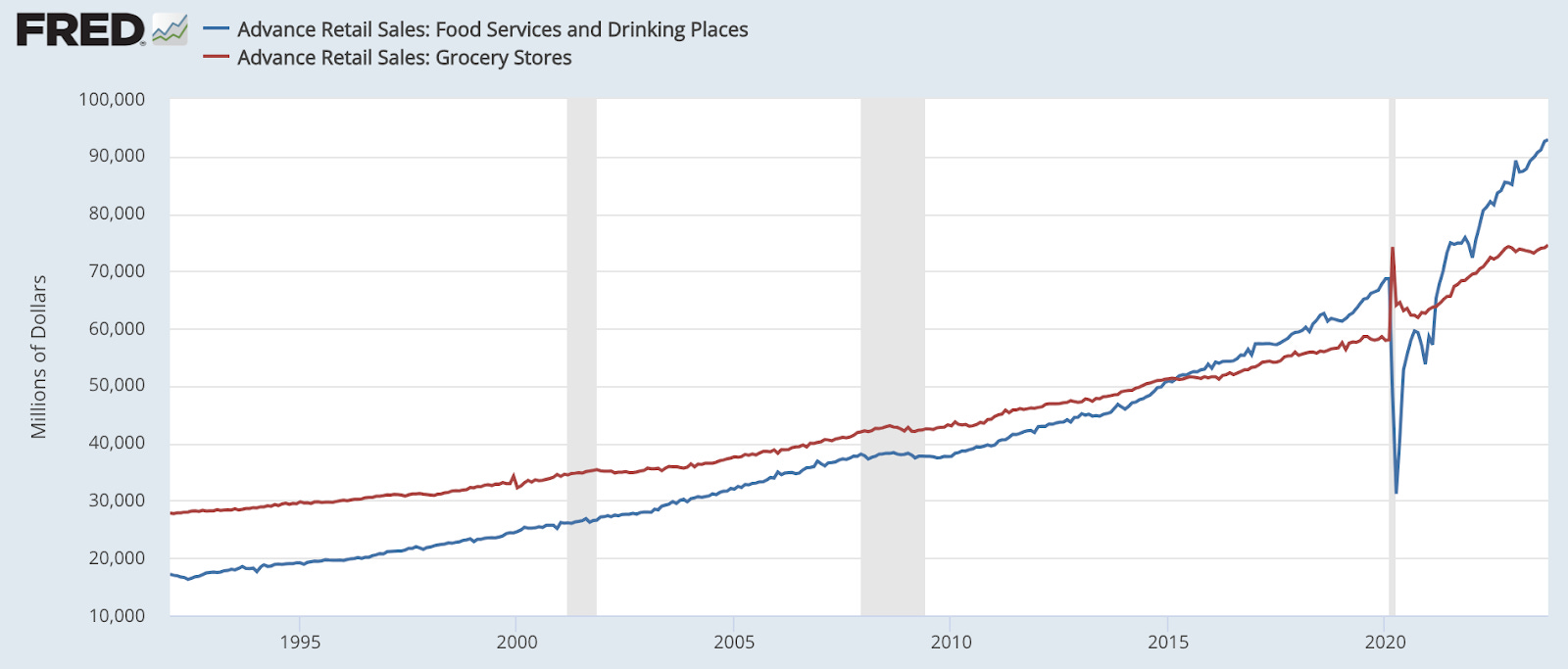

Quick service is a wonderfully stable secular growth story. Around 1992, per FRED, monthly grocery sales of roughly $28 billion were 63% larger than total restaurant service volume. Today, that has entirely flipped with $93 billion in monthly restaurant volume. That’s 25% larger than the grocery space as a whole. The 5.6% compounded annual growth rate (CAGR) for restaurants leaves a compelling opportunity for share takers in the sector. Depending on which research vendor we trust, forward CAGR expectations range from 6%-10% over the next several years. There’s no slowdown in sight.

Notably, food and drink service growth did flatline during the great financial crisis and did tank during the pandemic. Still, the sector has shown impressive resilience in its ability to recapture solid, run-rate growth in excess of U.S. GDP growth. Consumers, more and more, are leaning on restaurants for consumption as younger generations flock to services over goods. That reality has been turbo-charged by the proliferation of convenient delivery options. That is the growth setup for the sector.

c. Sector Margin Intro

Aggressive, macro-based margin headwinds are easing. Input cost inflation of raw ingredients continues to tumble, which helps all QSR margins (assuming at least constant menu pricing). It’s much harder to maintain traffic and profitability with a CPI at 8%. Few companies have the ability to hike menu prices at that clip to hold margins steady. It’s a lot easier to maintain or even grow margin with a CPI falling towards 2%.

A more gradual pace of input cost inflation allows chains to avoid sticker shock in their quest for margin preservation and makes traffic easier to maintain. In some cases, as we’ll see in the deep dives, price growth for some input costs like salmon has actually turned negative for players like Sweetgreen.

Further, in terms of expansion, the falling cost of capital should accelerate the pace and profitability of new restaurant chain openings as expansion becomes cheaper. Sky-high rates have weighed heavily on fixed business investments. Now, they appear to have peaked. That is the simplistic set-up. Using this as the 30,000 foot view, we are set to explore specific company investment cases. Expect the first part of this sector dive to be published this month.

2. Adobe (ADBE) – Earnings Review

Adobe is a software giant. It provides programs to create and imagine, handle customer interactions and process documents. Revenue is split into two main buckets: Digital Media and Digital Experiences. Digital Media is made up of its “Creative Cloud” and “Document Cloud.” The Creative Cloud includes Photoshop and Illustrator. It’s what empowers creation, iteration and perfection of digital design. The Document Cloud, including the ubiquitous Adobe Acrobat, allows for secure PDF management and collaboration – among other things.

Finally, its Experience Cloud includes Adobe Analytics and other products like “Campaign.” Campaign is its intuitively-named marketing campaign tool. Experience Cloud covers end-to-end customer interactions with a real-time customer data platform (CDP) to ensure those interactions are optimized. It also publishes some great macro data on overall commerce spend.

a. Demand

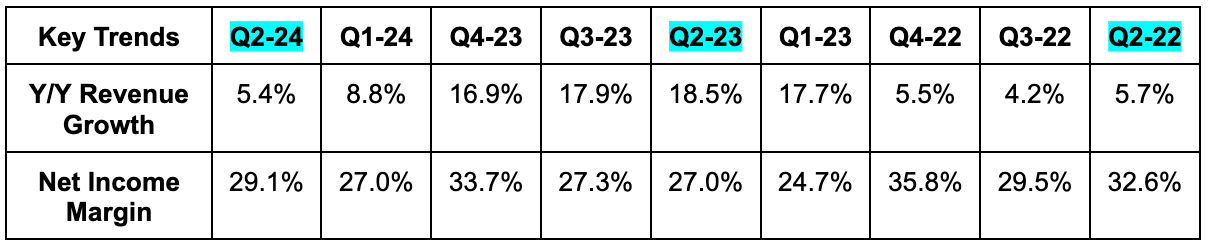

Beat revenue estimates by 0.6% and beat its guide by 1.0%.

Its 13.9% 3-yr revenue compounded annual growth rate compares to 14.8% as of last quarter & 15.5% 2 quarters ago.

Beat Digital Media revenue guidance by 0.9%.

Beat Digital Experience revenue guidance by

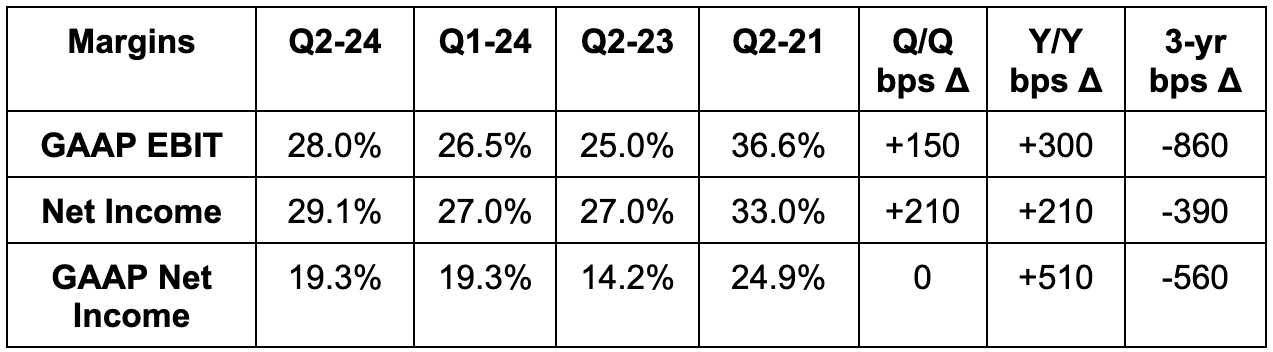

b. Margins

Beat $3.11 GAAP earnings per share (EPS) estimates by $0.12 & beat guidance by $0.10.

Beat $4.14 EPS estimates by $0.13 & beat guidance by $0.15.

Earnings per share rose by 17% Y/Y in 2023 as a whole.

It slightly missed EBIT estimates by a fraction of a percent. It doesn’t provide guidance for this metric.

Operating cash flow (OCF) margin was impacted by an $826 million U.S. tax payment that was deferred from Q2 and Q3. Without this one-time hit, OCF margin would have been 48.1%.

c. Guidance

Next quarter guidance missed slightly on revenue, but beat slightly on both GAAP and non-GAAP EPS.

For the full year guide, revenue was 1.4% light. GAAP EPS was $0.18 (or 1%) light vs. $17.98 expectations. Non-GAAP EPS was $0.37 (or 2.8%) ahead of $13.28 estimates. It generally likes to offer highly conservative preliminary annual guidance.

d. Balance Sheet

$7.84 billion in cash & equivalents.

$3.6 billion in debt.

Basic share count fell 2.2% Y/Y; diluted share count fell 1.5% Y/Y.

It has $3.15 billion in current buyback capacity.

e. Highlights

GenerativeAI:

Adobe plans to lean on what it sees as its two strengths to capitalize on the GenAI wave: Data and model-building. The data item is simple. Its scale is massive. Generative AI models need massive sums of data to be trained. The model building part is a bit more subjective. Adobe Firefly is its group of GenAI models. It enhances use cases among its current products, infuses new layers of automation into them and tears down the barriers to content creation.

Figma:

Figma is a platform for next-generation digital design. Adobe plans to purchase this company to introduce incremental value to its already broad toolkit. The European Commission has already pushed back on the deal for competitive concerns, but Adobe is responding to these concerns and pushing hard to close the deal. Ideally, that will happen some time next year.

Digital Media – Creative Cloud:

Creative Cloud had a strong quarter. The company did hike pricing here last month, but growth was driven by paid subscriptions. Most of the benefit from the hike has yet to be realized.

New GenAI product integrations are allowing clients to keep up with increased consumer demand for beloved brand content. These integrations are diminishing friction and vastly expediting content creation to meet enterprise needs. Across imaging, design, video and 3D, Creative Cloud + Firefly is leading to accelerating strength in mid and large client wins.

Along these lines of increased content demand, GenStudio is another key Adobe product. This is essentially an upgraded version of Adobe express – its end-to-end content creation product. GenStudio is GenAI-based and automates that creation from “ideation to delivery.” Automation unlocks a lot more capacity to create more content.

Deloitte and Pepsi were among highlighted wins for the quarter as the segment enjoyed a new record for net subscriber additions.

Firefly debuted 3 new models for Creative Cloud during the quarter including the Firefly Vector Model. Per investor materials, the Vector Model is the first GenAI model to transform text into “stunning vector artwork like icons and even entire scenes.” There are a lot of text to image models, but this supposedly goes a lot deeper. As an important aside, it’s adding GenAI credit packs to monetize this new usage growth.

While strength here was broad-based, emerging market strength was called out as a standout.

Frame.io (video-based creation and collaboration) enjoyed a record year in 2023 for net new ARR.

Digital Media – Document Cloud:

Adobe Acrobat for Web enjoyed 70% Y/Y growth in monthly active users. It also delivered a 400% Y/Y “surge” in link sharing for PDF collaboration. Thanks to Liquid Mode, Acrobat Mobile reached 100 million users. Liquid Mode is an AI powered tool to automatically retrofit web-based PDFs for mobile viewing.

Integrated Acrobat with all Adobe Express Workflows to pair powerfully artistic content creation with PDF formatting.

The segment won Bank of America, the Department of Veterans Affairs, Mastercard and State Farm as new customers during the quarter.

GenAI tools for the Document Cloud are in private beta.

Digital Experiences:

As we’ve already covered in previous articles, Adobe Analytics is a go-to provider for consumer spend data. It reported 7.5% Y/Y holiday weekend growth, which compares very well to expectations of 5.5% growth. This is where the Experiences Cloud thrives. If consumers want to spend more, brands will have more drive to optimize every interaction to maximize revenue per touchpoint. That’s what this suite does. Its real-time CDP gives companies a holistic, end-to-end control panel of individual customer interaction profiles at near-endless scale.

Adobe Experience Platform (AEP) is its product bundle that combines all of the Experiences Cloud. Like other platforms plays in software that can drive vendor consolidation and cost savings, this platform is thriving in today’s environment. AEP had its first $100 million net new business quarter. Its entire book of business sits at just $700 million, making that feat very notable. Overall, the AEP and native apps business rose 60% Y/Y. Coke, Vanguard, Marriott and Unilever are among large customer wins for this segment during the quarter.

f. My Take

This is one of those wonderfully boring and highly consistent performers. It’s a titan in creative software and a large player in customer relationship management as well. The underwhelming annual guide will likely be raised throughout 2024 if history is any indication. A fine quarter from an elite company. Enough said.

Long-Term Mindset is a FREE weekly newsletter emailed each Wednesday. Each issue contains five pieces of timeless content to encourage you to think long-term. All issues can be read in less than 1 minute. There’s a reason why we are consistent readers and think you should be too. Subscribe here.

3. SoFi (SOFI) – Expensive? Misunderstood?

2022 and most of 2023 have been periods of me consistently and aggressively defending what I see as a pristine SoFi bull case. We’ve gotten into fine detail on accounting practices, its loan book, its balance sheet and more. We’ve dissected and dismantled all of the risks that seem to magically become more pressing when the stock price falls for a few weeks. But it isn’t falling anymore.

With the stock price now responding positively to macro events, the conversation needs to shift. I wanted to unpack my thoughts on when SoFi the stock will become “expensive” if it continues to vertically and rapidly move higher. Further, I wanted to provide a feel for when I’d consider first trimming.

SoFi is a bank that doesn’t look like other banks. It owns its tech stack, it has no branches, it offers lower return products that most banks shy away from, and, most importantly, it has no GAAP net income. That last item has forced investors to value this bank disruptor based on an enterprise value (EV) to EBITDA multiple. Candidly, simply valuing a banking disruptor based on EBITDA makes me cringe. I do it by necessity here. Luckily, I won’t need to as it turns GAAP net income positive this quarter.

I think a lack of GAAP net income up until now is a large, large reason for why SoFi’s stock has been so unloved and misunderstood for most of its public life. Most investors (besides my readers) are somewhat lazy. They’ll go to Yahoo Finance, read a P/E ratio, see that it’s negative, and never give the company a second look. They won’t study margin inflection trends, unique accounting items below the EBIT line, incremental margins, margin catalysts or any other detail. If the P/E looks bad, they’re done.

Well? Again, SoFi’s earnings will turn positive next quarter, and the deal-breaker will go start to away. As of now, analysts expect the firm to earn $0.07 per share next year. Between its consistent shattering of profit estimates, its pessimistic guidance assumptions, easing macro headwinds and commentary on 2024 revenue splits, I think it will keep outperforming. Furthermore, 2024 analyst estimates have more than doubled year-to-date; I don’t think they’re done moving.

For simplicity, let’s assume that SoFi earns $0.10 per share based on a 4.0% GAAP net income margin. I truly think it will do even better (as incremental margins point to), but I could always be wrong. From that $0.10 2024 performance, earnings are expected to compound at a 2-year clip of 115%. At today’s price, SoFi would trade for 94x my 2024 estimates, 40x 2025 and 22x 2026.

As per one of the greatest investors of our age, Peter Lynch, a PEG ratio under 1x is considered cheap. PEG ratios take P/E ratios and divide by earnings growth. I use multi-year earnings growth to eliminate one-off events and reduce volatility. SoFi’s PEG, under this methodology, sits at 0.82. Anything under $11.50 for this stock, as we look ahead to 2024, is inexpensive in my mind. That also assumes no increases to 2025 or 2026 profit estimates, which is not likely. I’m not saying that SoFi will get to $11.50 tomorrow or even in 2024. This is just me saying that I’m not interested in trimming at this stage. It would likely need to get closer to a PEG of 1.4x-1.5x for me to consider doing so.

4. Walt Disney (DIS) – India

Walt Disney and Reliance Industries are reportedly wrapping up a merger agreement. Bloomberg says this could be announced next week; other outlets say it will be done by next month. Regardless, the negotiations are at a very late stage in what would create the largest media company in India.

Disney will sell at least 51% of its India media business and merge its Star India business with Reliance’s Viacom18. This would transform Reliance from a fierce foe in that important market into a tight ally. Reliance, in the past, has done things like outbid Disney for cricket rights. It even offered those rights for free in what makes Reliance nearly impossible to match in India. So? Disney won’t try to match them. It will join forces. As an aside, it eventually must do the same thing with ESPN and mega-cap tech… but I digress.

Rough estimates point to Disney’s India segment being worth about $10 billion. The companies will supposedly each infuse about $1.5 billion into the new business. Considering this, at the very least, the move should represent more than $4 billion in cash added to its balance sheet. The newly formed media group will then get exclusive streaming access to Disney+ for 5 years.

The deal also allows Disney to focus on its core markets and core intellectual property. India was causing a major cash burn with incremental revenue being a distant second outcome. This will tighten Disney’s focus to higher priority businesses. It will do so while freeing Disney to participate in India’s upside, without being in charge of steering that upside. Why not tap into Reliance’s unmatched market presence and distribution? That’s the plan.

5. Amazon (AMZN) – 2024

Both JP Morgan and Piper Sandler named Amazon as a top pick for 2024. They called out reasons that were identical to the investment case (LINK) that I shared earlier this year. The bullishness comes from a combination of marketplace and logistics operating leverage as well as Amazon Web Services (AWS) cloud growth bottoming. Piper Sandler shared a survey with some upbeat data. It depicted strong AWS spend intentions from CIOs in 2024. It also hinted at a growth acceleration for AWS in excess of the other public cloud providers. Finally, the survey pointed out an optimistic ad spend appetite, which should further feed marketplace margins.

Speaking of advertising tailwinds, Amazon inked a deal with Interpublic Group’s (IPG’s) IPG Mediabrands for its ad-based streaming product. IPG is the 5th largest advertising campaign manager in the USA and this is Amazon’s first large-scale ad agency contract of this nature. The deal is for 3 years and gives Amazon Prime a large base of high-quality brands to sell placements to. IPG gains preferred access to sponsorship and advertising opportunities on both Amazon’s streaming service and its marketplace. Pairing marketplace ad placements with the newer streaming service will allow Amazon to mightily bolster the reach that it can provide to advertisers and better compete with established streamers like Netflix.

Amazon has been hard at work on its programmatic advertising offering. Its investments in building out the tech stack combined with its unmatched database provide real value to advertisers in their quest to maximize returns. Per a MarketingDive article, Magna (part of IPG Mediabrands) calls Amazon’s talents in programmatic advertising “game changing.” We shall see how that translates into high margin revenue.

As a final 2024 note, Amazon is enhancing investments in China to better compete against Temu for sellers there. It will launch a new innovation center in the country to guide new sellers through onboarding and their growth journeys. While I don’t see Temu as an Amazon-killer, it is a strong competitor. Its quality lags Amazon’s, its fulfillment greatly lags Amazon’s in the Western World, its brand trust lags Amazon’s and it can’t compete with the Amazon Prime subscription here. With all of that said, it surely can steal a little share and be a formidable counterpart. While this isn’t another Amazon, it’s also not another throwaway like Wish.com.

6. Uber Technologies (UBER) – Miscellaneous

Uber was added to the S&P 500 on Friday.

Added Sprouts Farmers Market as a new Uber Eats grocery partner.

Uber Freight is partnering with Greenlane to turbocharge the creation of public semi-truck charging infrastructure. The release teased using Uber Freight in a Calendly-like fashion to book charging appointments.

7. Meta Platforms (META) – Threads (Twitter Copy Cat App)

Threads is getting updated to comply with European law and pave the way for its release there. That’s the Threads news, but I wanted to add a bit of insight on the app this week.

Threads stormed onto the scene upon launch and then quickly faded away. That momentum could be returning as Meta works to perfect the product interface. Per data.ai, downloads for October shot Threads up the app rankings from #40 to #20 in its category. Momentum picked up from there. Impressively, Threads is now #2 on Apple’s U.S. app store as of today and #1 in Social Networking. This isn’t due to the Europe launch as the data is U.S.-specific. That’s notable to say the least.

I’ve built a thriving business on Twitter (X) and I both thank them and love them. I want Twitter to succeed. With that out of the way, it’s undeniable that the bird app finds itself on more fragile footing than in previous years. Half of Twitter’s advertisers have vacated the platform and it has started to feel more niche than since I started using it. Polarizing is the word that comes to mind. Elon is a superstar, but his antics still open the door for something like Threads to win. It will need to win for a long time to become material to Meta’s results, but the path is there. Meta has insight-rich data from half of the planet on what works in social media apps. Meta is less controversial for advertisers to embrace. Meta has a massive cash pile to invest as aggressively into this opportunity as it needs to. The stage is set for Threads to be yet another smashing success for this firm. Twitter is doing its absolute best to make that happen.

8. Meta Platforms (META), Alphabet (GOOGL), The Trade Desk (TTD) & The Ad Sector – Advertising Tailwinds

Bank of America came out with some upbeat 2024 online media commentary. Short-form video, GenAI discovery enhancements and easing macro headwinds were all called out by the firm. Budget scrutiny and timid advertising appetite headwinds are both seemingly fading away. All of this led it to revise its sector growth expectations in 2024 from 5% to 11%.

I think the reason for optimism is well-placed. All of these tailwinds should be amplified by one more factor as well. The highest quality firms in the space have effectively addressed the signaling gap left by Apple’s data sharing policy changes. Cost per impression is recovering, returns are rising and engagement growth is fueling more impression growth. This momentum is most notable with Meta and Alphabet. And if you think about it, that makes sense. As macro chaos abates, advertisers will first seek out the most certain and most precisely targeted impressions. They’ll seek out the ubiquitous commodity. That’s what these two giants are. I expect the greenshoots to eventually trickle into the smaller, open internet players. The Trade Desk will be the first to capitalize on that newfound tailwind considering its best-in-class open internet return metrics. TTD’s cautious Q4 commentary paired with very optimistic 2024 commentary also now makes more sense given this context.

9. PayPal (PYPL) – Data, Regulation & Rule Breaking

a. Data

Morgan Stanley published some data on PayPal this past week. Acceptance among the top 500 U.S. merchants reached 83% this past quarter vs. 76% in 2019. Apple Pay is the 2nd closest at 48% with that number quickly rising. Klarna at 19%, Google at 16% and Affirm at 15% round out the top 5. It rightfully called out the slow pace of Venmo adoption for checkout. It’s only accepted by 7% of the 500 largest merchants vs. 3% in 2022. That progress needs to ramp and ending the Amazon relationship, though likely due to cash-burning incentives, does not help. It also pointed out that just 45% of Venmo’s users were between 18-24 in 2022 vs. 58% in 2019. It needs to better cater to younger generations if it wants to keep dominating in settings like college campuses.

It called out Braintree’s rapid growth and margin impact which we’ve documented in detail already. It shared data that points to PayPal Branded Checkout growth lagging e-commerce by 180 bps in 2022, matching the sector's growth in Q1 and Q3 2023 and lagging it by 120 bps in Q2 2023. This underperformance in 2022 basically means old CEO Dan Schulman was either misleading or just wrong when saying they were taking or holding branded share through 2022. There are many data sources on industry e-commerce growth, but this one doesn’t paint PayPal’s old team in a positive light.

b. Regulation

Apple is reportedly considering opening its near-field communication (NFC) technology to competition to avoid antitrust battles. This would be great news for everyone in the payment space including PayPal. It would drive down user friction, enhance interoperability and make all competitors more viable in the vital mobile format. It could open the door for PayPal and Venmo to offer mobile tap-to-pay without requiring users to link their cards to their Apple Wallets. This will free PayPal to compete for volume without directly supporting its fiercest North American competitor.

c. Rule Breaking

I broke a rule this week. I added a bit to my PayPal stake before the transaction margin trough. I said I would wait for it to come. I didn’t. What changed? The change in mindset is two-fold. First, I have really liked the new CEO’s tone and decisions thus far. His sale of Happy Returns and rumored sale of Xoom point to sharper focus on its massive core initiatives. Its rumored “quantum leap” initiative to rapidly modernize PayPal checkout is also dearly needed.

Schulman couldn’t deliver this and struggled to painfully migrate one large merchant at a time onto PayPal’s latest flow. That just doesn’t work in a world where Shopify can onboard merchants with the click of a button. As an aside, Schulman will leave PayPal’s board this year. He’s a very nice person, and this is a very needed change.

Chriss has direct experience with successful innovation and nurturing of relevant products at Intuit. I think he can match that success here. PayPal doesn’t even need to have a superior branded checkout product. It just needs to be on par with the rest. Why? Its brand consideration and trust levels are second to none. Product is the only thing holding this former disruptor back, yet consumers flock to it anyway. Per Builtwith, it’s #1 in Europe and Asia and #3 in North America. Per Pymnts, it was the top branded checkout option in the USA in 2023. Imagine what this special brand can do with a great product. It once did have a great product. It needs to recapture that. Chriss is the man to pull it off.

The second reason, and why the purchase happened Wednesday afternoon, was related to the Fed statement. It was the final piece of proof I needed to be confident in the Fed being 100% done with hikes and confident in QT ending in 2024. Easy monetary policy without a coinciding severe recession should be great for monetary velocity. This will surely benefit a company like this one doing well over a trillion in annual volume. This company’s footprint is macro in nature and macro headwinds are now set to fade.

This is why I broke my rule.

10. Match Group (MTCH) – Update and Investor Conference

a. Investor Conference

Top-of-Funnel at Tinder:

Swidler walked us through a marketing blunder from the Match team. Top-of-funnel trends were recovering directly based on its successful Tinder marketing campaign during the spring and summer. For whatever reason, it halted this spend later in the summer to focus on a different back to school campaign. I’m not sure what data the team was looking at to make this pivot away from what was working, but they made it none the less. Top-of-funnel momentum subsequently dried up and has since started to recover as it turned the national marketing engine back on. This lesson will lead Tinder to having an “always on” portion of its marketing budget to avoid repeating this frustrating mistake. It cost the team about 2 additional quarters on the path to recovery. Again, frustrating.

The main concern here is that the app just doesn’t appeal to GenZ or women. Well? The marketing campaign was explicitly leading to a spike in growth among GenZ women specifically. This team really just needs to execute better and my patience to wait for them doing so is dwindling. It continues to work on infusing more serious, intentional dating profile tools into Tinder as that is what GenZ clearly wants (see Hinge). I occasionally use Tinder to try to meet that special someone. The app doesn’t look much different to me aside from added dating filters, which are actually a welcomed change.

Overall, Tinder top-of-funnel has been down by mid-single digits Y/Y throughout 2023. CFO Gary Swidler told us that lapping price hikes in Q2 will lead to progress here throughout 2024. He thinks they’ll be in “a lot better shape” here in a year and growth should turn sequentially positive in Q2 or Q3 next year.

Subscription revenue for Tinder continues to perform well and a la carte revenue continues to struggle.

Student loan payment resumption has impacted Tinder and Match in line with leadership expectations.

It may look to hike prices on Tinder outside of the USA in 2024.

Hinge:

If only Hinge traded as its own public company (but with access to Match’s large database). This app is thriving. All of the work on debuting it across Western Europe in 2023 should lead to more explosive growth in 2024. It has its eyes on Asia and Latin America for 2025 expansion plans.

Match Group Asia:

Azar continues to grow quickly thanks to upgrading its AI matching algorithms. Hakuna and Pairs both continue to struggle. For Pairs specifically, some help may be on the way. Based on Japan’s very low birth rate, the government and Match are now partnering on go-to-market for the Pairs app. Between that and newly legalized TV marketing there, the uniquely elevated dating app stigma should slowly fade away. Pairs caters well to the 18% of Japanese people willing to use dating apps. It doesn’t do well with expanding that 18% as the rest are not as comfortable with using them. It’s addressing that now.

Final Key Notes:

Swidler called out a change in Apple’s 10K risk disclosures. It now calls app store regulation likely. This would be a margin boost for Match’s business.

It doesn't see anything that it wants to buy. So? More buybacks.

“We have strong margins, cash flow and returns. When I look at the stock, I struggle to understand where people’s heads are at. But that gives us the opportunity to buy back more stock. And I'm optimistic we'll look back in a few years and say, we should have bought even more than we were buying back in 2023.” – CFO Gary Swidler

b. Update

The Fed pause is good news for Match group specifically. Why? Two reasons. For one, its balance sheet carries quite a bit of debt. Leverage ratios are in good shape, but this could allow the firm to get aggressive on those ratios to buy back more shares at today’s depressed valuation. Secondly, it will likely lead to downward pressure on U.S. dollar currency swaps. With a whopping 50% of its revenue not being collected in dollars, FX headwinds should quickly turn to tailwinds to prop up its growth. In a perfect world, I would have added to this name like I did with PayPal and Lemonade following the Fed Statement. I didn’t.

Candidly, it’s not because I consider the position to be full. I’m willing to break that rule in some instances, just not in this one. This has been the black eye of my portfolio with part of Tinder’s struggles being micro-based and self-inflicted.

New leadership is about a year into their tenure. Revenue growth for Tinder has accelerated, partially thanks to much easier comps, and Hinge continues to dominate. Still, old excuses are being replaced with new excuses. Leadership last year rightfully called out poor product innovation and “not getting enough product shots on goal” as the reasons for slowing company momentum. It further called out old leadership almost being too proud to spend on external Tinder marketing when that was dearly needed. Fast forward to today, and the excuses have changed. Several quarters into ramping up product iterating, macro headwinds are being blamed on a recently lowered 2023 guide while other companies cite easing macro headwinds. Its continued weak top-of-funnel trends are being blamed on Tinder needing to better cater to GenZ. At some point, this becomes the new team’s fault and leaves me wondering if this app truly is a dinosaur.

With all of that said, online dating is a secular growth story and this is the clear share leader. The market resembles an oligopoly with Match commanding most of the power. For this reason, I’m not yet ready to let go. Figure your sh*t out, Match.

11. Earnings Roundup

a. Oracle (ORCL)

Results:

Missed revenue estimate by 0.8% & missed guide by 0.5%.

Cloud revenue growth was below guidance.

Barely beat $1.33 EPS estimate by a penny & beat its guide by $0.04.

Met $0.89 GAAP EPS estimate; Missed EBIT estimate by 0.6%.

Guidance:

7% Y/Y revenue growth guidance slightly missed expectations and led to modest downward demand revisions from analysts. EPS guidance was in line with estimates. The company also reiterated its 2026 financial targets.

Balance Sheet:

$10.1B in trailing 12-month FCF vs. $9.5B Q/Q and $8.4B Y/Y.

$8.2B in cash & equivalents.

$89B in debt ($6.3B is current).

Diluted share count rose 2.6% Y/Y; basic share count rose 1.9% Y/Y.

b. Costco Wholesale (COST)

Results:

Costco revenue barely beat estimates.

EBIT was 1.3% ahead of estimates.

Beat $3.42 GAAP EPS estimates by $0.16.

Balance Sheet:

$17.8 billion in cash & equivalents.

$5.9 billion in long term debt and another $1.1 billion in current debt.

Share count is roughly flat Y/Y.

Inventory rose by 8.1% sequentially.

Will pay out a special $15.00 cash dividend.

12. Macro

a. Fed Statement

Jerome Powell was more dovish in his statement and press conference this week than perhaps anyone hoped for. In the statement, the Fed described inflation as “easing” in what was the most positive language change we’ve seen in over a year. It added the word “any” to determine the extent of (any) additional targeting to hint at it being done with hikes. For more evidence, its mean 2024 rate projection plummeted from 5.1% to 4.6% (3.6% for 2025 vs. 3.9% previously; 2.9% for 2026 vs. 2.9% previously). 4.6% represents about 3 cuts expected for 2024.

Cut probabilities for March rose from 40% to 60% as a result. The Fed is seeing faster disinflationary progress than it expected, but again, with more progress needed. Powell even called out cooling inflation in the stickiest non-housing services bucket. Policy was called “at or near its peak” with the potential for data surprises to change that view. Finally, longer-term inflation expectations remain well-anchored.

The labor market remains strong. Labor supply imbalance is still there but recovering with better labor force participation and higher rates of immigration. Wage inflation, as a result, is meaningfully cooling. It sees unemployment rising from 3.8% this year to 4.1% next year.

Taking all of this together keeps the elusive soft-landing outcome firmly on the table. It points to a Fed being able to pause and cut rates while the economy reasonably chugs along. Notably, it has no plans to slow down the pace of balance sheet shrinkage (quantitative tightening), which is its other tool for controlling inflation. That monetary supply headwind will eventually fade likely at some point next year.

Economic growth considerably slowed from Q3 vs. Q4. GDP for 2024 is now expected to be 1.4%. Restrictive policy is weighing on fixed business investments, housing and other rate sensitive sectors.

While all of this is encouraging, stocks still won’t go up in a straight line. They never do, and this time won’t be different. The Fed will work to hawkishly jawbone to keep excitement in check. Non-voting member Bostic did that yesterday when we called for 2 rate cuts in 2024 over 2023. Regardless of this sentiment, we are clearly closer to the end of this hiking cycle and the end of speculative growth assets endlessly and aggressively cratering. The “brighter days ahead” seem to be arriving.

b. Macro Data

Inflation Data:

Consumer Price Index (CPI) Y/Y for November rose 3.1% as expected and vs. 3.2% last month.

CPI M/M for November rose 0.1% vs. 0.0% expected and 0.0% last month.

Core CPI Y/Y for November rose 4% as expected and vs. 4% last month.

Core CPI M/M for November rose 0.3% as expected and vs. 0.2% last month.

Producer Price Index (PPI) M/M for November rose 0% vs. 0.1% expected and -0.4% last month.

Core PPI M/M for November rose 0% vs. 0.2% expected and 0% last month.

Consumer inflation expectations fell from 3.6% to 3.4%.

3, 10 and 30 year note and bond auctions all closed at rates lower than previous auctions. 4.49% for 3-year, 4.296% for 10-year and 4.334% for 30-year.

Consumer and Employment Data:

Retail Sales M/M for November rose 0.3% vs. -0.1% expected and -0.2% last month.

Core Retail Sales M/M for November rose 0.2% vs. -0.1% expected and 0% last month.

Initial Jobless Claims rose 202,000 vs. 220,000 expected and 221,000 last report.

Output Data:

Atlanta Fed GDPNow reading for Q4 jumped from 1.2% to 2.6%.

New York Empire State Manufacturing Index for December was -14.5 vs. 2 expected and 9.1 last month.

Industrial Production M/M for November rose 0.2% vs. 0.3% expected and -0.9% last month.

Manufacturing Purchasing Managers Index for December was 48.2 vs. 49.3 expected and 49.4 last month.

Services PMI for December was 51.3 vs. 50.6 expected and 50.8 last month.

13. Portfolio

As mentioned, I added to PayPal this week. I also added to Lemonade following the dovish Fed statement.

Adbe is a great company. Unfortunately very fully valued.

Very nice read on your summary of macro information .

Appreciate your connected very informative.

I will look at your stocks picks and see if I can add few to my daughters long term portfolio - Thanks