News of the Week (March 4 - 8)

News of the Week (March 4 - 8)

MongoDB; Visa; SoFi; Disney; PayPal; Snowflake; Broadcom; GitLab; Alphabet; Zscaler & Cloudflare; Market Headlines; Macro; Portfolio

Today’s Piece is Powered By My Friends at BBAE:

1. MongoDB (MDB) – Earnings Review

MongoDB is a key player in data storage and analytics with a document-oriented setup. Last earnings review, I covered MongoDB’s niche and product suite overall. I think that’s an important read for folks wanting to understand this business. It defines key terms with needed context. That can be found in part 3, section e of this article.

Its most exciting product is called MongoDB Atlas. This is a cloud-native database service that implements a group of servers (or a cluster) used to actually store the data. The nature of MongoDB’s product allows clusters to be easily added to or subtracted from for easier flexing up & down as needs fluctuate. It also offers MongoDB Realm as a mobile environment for app creation, MongoDB Stitch to build apps without servers or any needed infrastructure maintenance and MongoDB Search for data querying. Finally, it offers MongoDB Data Lake specifically for unstructured data, which directly competes with players like Snowflake. There are more products, but these are the big ones with new releases discussed below.

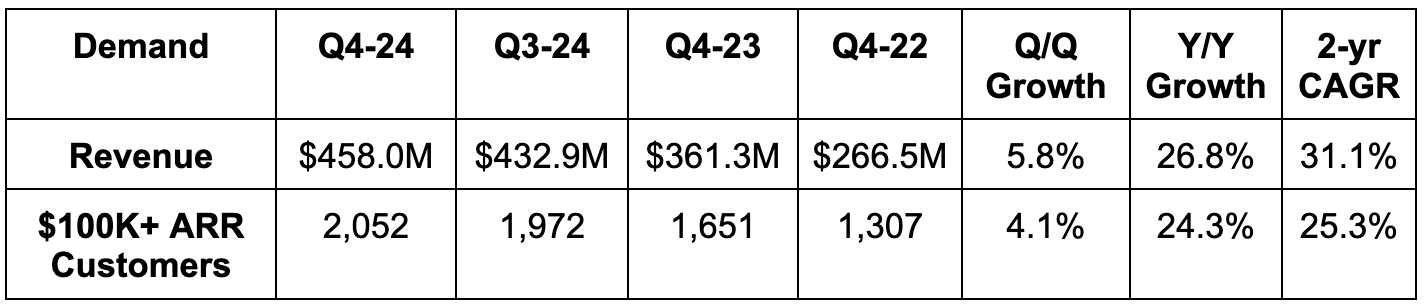

a. Results

Beat revenue estimates by 5.1% & beat guidance by 6.3%.

Net revenue retention was 120%.

Crushed EBIT estimates by 86% & Crushed guidance by 89%.

Beat $0.48 earnings per share (EPS) estimates by $0.38 & neat guidance by $0.41.

Met free cash flow (FCF) estimates.

Gross margin (GPM) of 77% worsened from 78% Y/Y. This is due to a 250 basis point (bps) boost to last year’s GPM due to “one-time cloud contract benefits.” It expanded by about 150 bps Y/Y without this headwind.

b. Annual Guidance & Valuation

Missed revenue estimates by 5.9%.

Sharply missed EBIT estimates by 34%.

Missed $3.22 EPS estimates by $0.84.

MDB trades for 163x next year’s earnings. Earnings are set to shrink Y/Y. Wait what? MongoDB’s guidance was shockingly poor, but there’s decent reasoning for this. The company pocketed $80 million in unused Atlas commitment revenue and multi-year licensing revenue (large Alibaba contract extension) last year. It expects that to fall to $0 this year, with non-Atlas revenue growth turning negative. This implies continued strong Atlas growth, which is by far its most important product. From a margin perspective, the $80 million in lost revenue was basically pure profit, which again won’t recur. These were the sources of the misses. (MDB’s team also loves to sandbag on their initial annual guides.)

The misses were not at all related to competition. Its win rates vs. all competitors rose Y/Y and its new product uptake is going very well. MongoDB is rapidly rounding out its product suite to consolidate vendors and cut costs within databases and app development. In a world obsessed with point solution displacement, this is a great focus area and is working. That’s likely why it now has 259 customers with over $1 million in annual business vs. 213 Y/Y.

c. Balance Sheet

$2 billion in cash & equivalents.

No traditional debt.

$1.1 billion in senior convertible notes.

Shares +4.1% Y/Y.

$109.9 million in FCF vs. -$24.7 million Y/Y.

d. Call & Release Highlights

Atlas:

Atlas’s new workload growth was strong while its retention and consumption trends were too. It sees consumption growth continuing throughout next year. This product had a great quarter despite tough comps related to lapping unused commitment revenue. It greatly changed its sales team incentives to minimize this stream of revenue and focus on consumption growth. 34% Y/Y Atlas growth would have been 36% Y/Y without this headwind.

GenAI:

MongoDB released a few GenAI products this year. Vector Search makes it easy to query needed data with slick integrations to plug that data into GenAI apps. GenAI apps and models insatiably consume data. The more data, the better; the more relevant that data is, the better. MongoDB provides data scale and secure access to a client’s first party insights. It pairs these data skills with ample programming language frameworks to free developers to bring their work to their data. This new tool offers Semantic Search, which allows clients to seamlessly scrape insight from data. It allows for theme-and-idea-based querying rather than just word-based. It also provides retrieval-augmented generation (RAG). This pushes semantic search results into associated large language models to uplift querying precision. It also debuted Stream Processing to utilize data as it is generated in real time. This will surely be a popular tool for GenAI app builders too.

While these products are compelling, they’re not really moving the financial needle just yet. Almost all GenAI spending is happening within model training and inference. Very little spend has happened to date within the app layer of GenAI, which is where MongoDB expects to carve its niche. It provides endless and cohesive access to data and tools to automate app creation from within its platform. It marries these strengths with powerful integrations to ensure a developer can easily deploy apps in runtime elsewhere. It sees strong evidence and early cases of its platform being used to build GenAI apps. Most of the demand tailwind from this, however, will take place in the future.

2024 Priorities:

Keep investing in the core platform and GenAI products like Vector Search.

Obsess over new workload growth.

Alter sales incentives to align go-to-market with workload growth maximization goal.

Accelerate sales team growth.

Relational Database Migration Opportunity:

As the MDB intro I linked to at the beginning of this spells out, displacing legacy relational databases is MDB’s biggest opportunity. It’s great at automating the preparation and data movement of these antiquated products. It’s not great at rewriting application code as that data enters its ecosystem. It plans to lean into GenAI products to internally automate that code writing process. It thinks this will significantly diminish migration friction for new customers. They’re probably right.

f. Take

Great quarter and an awful annual guide. If history is any indication, it will raise that guidance consistently throughout the year. It loves to under-promise when it offers initial annual guidance just like it should. Atlas revenue and guidance were strong, the margin trend excluding special items last year was very strong and commentary surrounding competition was encouraging too. Like with Snowflake, the multiple is simply far too lofty for me to start a position just because I think guidance is conservative. At 163x forward EPS, perfection is needed and I’m not willing to assume perfection at this stage. This was not perfect, but I do see why bulls defended the print.

2. Visa (V) – CEO Ryan Mclnerney Investor Conference Interview

Mclnerney talked about strong demand for services like cybersecurity and Visa’s work to drive productivity, diminish friction and lower fraud rates through GenAI. He spoke about Visa’s massive data set putting it in pole position to win in this new wave. It has firm-specific models now being built with partners. That was interesting, but all review.

What wasn’t review was his updated pulse on the health of the U.S. and global economies. Visa has arguably the best gauge of global economic health in the world. Their CEO is spending time to tell you how that economic health is shaping up. These are highly valuable insights to gather… so let’s gather them.

Mclnerney talked a lot about “stability as he looks around the world right now.” Nothing in their data is pointing to a recession. There’s some decelerating spend growth in the U.K. and Australia, but not in the USA and not across most regions. He called USA spending “as steady as she goes” with payment volume quarter-to-date in line with last quarter. There has been no further slowing. Content creators and social media experts sure do love to offer their macro opinions. I’d rather get those opinions from Visa’s CEO.

Looking for a better investment platform? Enter BBAE. The product speaks for itself. The Town Square copy trading tool allows you to emulate Wall Street’s finest. Its curated stock themes (under BBAE Discover) inspire new ideas, and its valuable technical and fundamental research tools guide you through key concepts.

BBAE is the broker dedicated to giving investors what matters to us. No gimmicks, no charms, no confetti, and never any pressure to trade. This is THE broker for long-term investors. Oh… and it’s offering generous deposit bonuses of up to $400. Check it out here. You’ll be glad you did.

3. SoFi (SOFI) – Complex Capital Maneuvers

The News:

SoFi announced two different pieces of complex capital structure news this past week. First, SoFi plans to raise $750 million in convertible senior notes maturing in 2029. Net proceeds will be about $845 million as options to purchase up to $112.5 million in additional notes were broadly exercised.

Secondly, it will exchange $600 million worth of its 0% convertible senior notes (maturing in 2026) for common stock. These two moves make it sound like SoFi is aggressively diluting shareholders, but much more context is needed.

I’m going to cover some complex accounting items in this section. This gets way more into the weeds than an investor needs to go, but I love to know everything about my investments. It’s how I am most comfortable with holding through turbulence. If you don’t need this level of detail, simply know the following things about these deals:

They boost net income and tangible book value.

They are neutral for net income and tangible book value per share.

They boost SoFi’s capital ratios significantly.

They will lead to at least 3% total dilution. If the stock goes above $14.54 before March 2027, there’s additional dilution risk.

2029 Notes Offering:

On the 2029 notes offering, some of the proceeds (and some cash on hand) will be used to retire $325 million in 12.5% preferred shares outstanding. These shares were set to see rates materially jump this spring. SoFi needed to redeem them before May to avoid paying the higher rate for the next 5 years. SoFi will only pay a 1.25% annual interest rate on the $750 million in fresh funding. This means it swapped out about $57 million in annual interest expense for $9 million in annual interest. But wait, there’s more. SoFi will use part of the remaining $425 million to refinance expensive debt, thus adding to the interest expense savings. This will be positive for net income, positive for retained earnings and so accretive to overall tangible book value.

The notes mature in March 2029. SoFi has the right to redeem these notes for cash if the stock price reaches $12.29 for a 30 day period (130% of $9.45 conversion price) at any point after March 2027. Note holders can convert the notes before September 2028.

2026 Convertible Notes Exchange:

Relatedly, SoFi will also exchange $600 million of its roughly $1.1 billion in 2026 convertible senior notes for roughly 61 million shares of its common stock. That news in isolation is a bit concerning and seems to indicate significant dilution. But again, more context is needed. Convertible notes are already part of fully diluted share count (which is what SoFi uses in its EPS guidance). So? While 61 million common shares are being created, $600 million from the 2026 convertible note balance is being retired. That $600 million represents about 54% of its 49.6 million share convertible note balance. 54% of 49.6 million is 26.8 million, which is deducted from 61 million shares. This leaves us with ~34.2 million shares being created for ~3% total dilution.

3% dilution is not crazy, but ideally we’d like no dilution. There are three explanations I see for why this second deal happened, which I'll cover in order of probability. First, it could have been a necessary amendment for buyers of the $750 million note offering to get that done at the terms SoFi wanted. Secondly, this may just be the company wanting excess capital ratio flexibility due to its pessimistic macro forecast. Finally, perhaps it’s seeing lending greenshoots and wanted extra balance sheet capacity to accelerate origination growth this year. That would be fantastic news, but also somewhat surprising considering Lapointe recently spoke of an overly cautious lending outlook.

These notes are trading at a more than 10% discount to par value. That means retiring them now allows SoFi to use about $60-$70 million less in stock vs. retiring at par. It also means capital ratio relief. Had this been done in Q4 2023, its total risk-based capital ratio would have been 17.3% instead of 15.3%. SoFi doesn’t plan to utilize excess capital ratio flexibility this year as Chris Lapointe told us in a recent investor conference. Still, it’s always nice to have for the future when macro does brighten and it leans back into origination growth. If it does use up this capacity down the road, it has more convertible bonds that it could potentially buy back at a discount for more capital ratio relief. That would also shrink fully diluted share count, effectively reversing some of the minor dilution from these moves. There are many, many levers this firm can pull under GAAP accounting to keep its balance sheet strong. Just keep growing profits & keep underwriting responsibly to maintain that flexibility.

SoFi Capped Call Transactions & Dilution:

Capped calls are option contracts that a convertible note issuer like SoFi will buy from financial institutions. SoFi pays a premium for this contract type up-front, which in this case will be $79 million. The counterparty will purchase some shares upon agreement to cover the potential obligation and shrink the tradable share float.

Why will SoFi and the option counterparty enter into an arrangement like this one? Firstly, Sofi enjoys dilution protection from the $9.45 conversion price up to the $14.54 cap price. It can avoid creating a large portion of the 78.6 million potential shares ($750,000,000 / $9.45 conversion price or 8% total dilution potential over 5 years) with this secondary transaction.

Instead of pulling entirely from treasury stock to dilute shareholders, SoFi can use the capped call seller’s shares from this in-the-money contract to help cover the liability. That’s why capped calls diminish dilution risk. Any price beyond $14.54 (the “cap price”) could lead to more dilution. That outcome would represent a minimum 24% return CAGR for SoFi shares from now to then and would be fine with me. Furthermore, SoFi is currently inflecting to profitability and enjoying strong capital market demand for its loans. If it owes more shares in the future, it’s rapidly becoming more capable of using profits to fund the liability rather than treasury stock. In this case, it would likely have the flexibility to purchase additional options with higher cap prices for more dilution protection. Think about it… if the stock price skyrockets, will that be because SoFi is struggling with liquidity and profit compounding. Probably not.

The point here is that it has options to make the dilution tied to this raise very modest. It’s all about profits continuing to ramp like they’re expected to.

If SoFI the stock struggles to get above the conversion price and starts to struggle with liquidity and profit compounding, there is a risk of it needing to raise cash to cover principal and interest payments. Note holders wouldn’t convert until the stock passes conversion levels as that would result in no capital gains and forgone interest expense. They can just hold the notes, collect interest, know they’ll get their principal back and partake in any potential stock upside as well. SoFi, in this case, would be at higher risk of covering liabilities with dilution. Its inflection to GAAP profitability diminishes this concern significantly and I consider this outcome to be highly unlikely.

This maneuver makes sense for SoFi, but why would the counterparty grant this option? Aside from the upfront premium collected, it provides a compelling profit structure for the capped call seller. If the stock does nothing, they keep their premium and nothing else happens. As the stock moves up to the $14.54 cap price, the shares they’re holding increase in value to offset the diminished value of the capped call contract that is sold. Beyond $14.54, losses are capped as the contract is settled. Downside risk protection paired with a large upfront premium makes it clear why the counterparty would do this deal.

And finally, for the buyers of the original convertibles, they don’t care about these secondary deals taking place. They solely care about their notes becoming more valuable over time and collecting that 1.25% annual yield. The buyers of the notes could easily be the same sellers of the capped call transactions (we won’t know for sure). Regardless, the point remains. Convertible note holders will still want more valuable notes regardless of whether they also sold the capped call to SoFi or not.

From this week’s news, there are a few capped call transaction items to note. SoFi will enter capped call arrangements that “initially cover the number of shares of common stock that initially underlie the notes.” Separately, it will amend the current capped call transaction connected to retiring 54% of its 2026 notes. While all of this is commencing, counterparty hedges will be built and unwound, which will likely create some incremental share volatility.

Eventual Dilution and Financial Impact of all items together:

We know there’s about 3% dilution from the $600 million 2026 note conversion. The eventual true dilution of the $750 million note raise is uncertain for SoFi. I’m still getting through the final 8K published last night and will include details about potential dilution outcomes from my learnings next week. What we do know is that all of these announcements taken together will boost net income, boost tangible book value and boost its capital ratios. For vitally needed context, per SoFi leadership, it will be neutral for profit per share. This means the earnings boost will roughly offset the dilutive impact on a 1-for-1 basis. The reason I can’t stand dilution is because it erodes earnings power. This context means that dilution in this case won’t. SoFi leadership knows its plans for handling these deals better than you or I ever could. It has earned my trust consistently since going public. I trust them here when they say this.

Stock Volatility Following the News:

On the stock’s volatility following the news, I think there’s actually a solid explanation aside from the 3% dilution with the 2026 note conversion. This news took me a few days to understand. I have a Master’s Degree in Finance. I have direct capital market and RIA experience and conduct fundamental stock research for a living. If I had trouble fully grasping this (I did), I’m confident that most other investors (including sell-side analysts) did too. I say it to explain that when headlines like this surface, people will assume liquidity issues, crippling dilution and sell. They’ll ask questions later. Further, convertible note holders had strong motivation to see the stock tank up to the closing of the offering yesterday. They want the conversion price to be as low as possible so they can make more if the stock price rises over the coming years.

4. Disney (DIS) – CEO Interview with Morgan Stanley

Financial News:

Iger did not hold back in updating shareholders on intra-quarter results. Sometimes these conferences are a waste of time. This specific interview was not. Iger reiterated Disney’s schedule to turn streaming EBIT positive. He said the Parks and Experiences business will enjoy roughly 15% Y/Y EBIT despite tough Walt Disney World 50th Anniversary comps. Finally, he told us that Disney would exceed its $8 billion annual free cash flow guidance. Mic drop.

As Iger told us last quarter, Disney is moving from a period of “fixing to building.” It has carved out unnecessary expenses, re-focused on making elite content and embraced optimal cost monetization once more.

Streaming & Films:

Disney grew Disney+ with too little focus and discipline before having the tech & marketing systems in place to support that growth. The result was higher marketing intensity, poor margins and higher churn than the Netflix “gold standard.” Iger thinks these systems, and their advertising stack, have now been put into place. That, paired with things like the Hulu bundle, is expected to greatly bolster retention and profits for the segment.

The Hulu and Disney+ bundle will fully launch in the coming weeks. Impressively, 50% of Disney’s new subscribers are going with this bundle despite it not yet being fully available. The churn benefits are clear and the subscriber growth impact is too as hit shows like Shogun build bundling demand.

The structure of this bundle is important. Disney intentionally placed Hulu in a separate channel within Disney+ with easy parental controls. This will eliminate the risk of children watching inappropriate content.

Another big piece of a healthy streaming business is simply making better films. Disney had lost its way over the last few years in terms of too much quantity, too little quality and too much focus on influencing culture. It’s back to its roots of “placing creativity at the center of its business” and holding content creators accountable for their blunders/successes. Iger sees the tide turning. He has thrown out low-quality projects in the pipeline and leaned into Disney’s most iconic IP. He thinks the slate through 2026 (including Mufassa, Star Wars, Deadpool & Wolverine, Toy Story, Inside Out 2 & Moana) is poised for great success. We’ll see. The Moana item is an interesting one to note. The original Moana film, which is now 8 years old, was the most streamed film in the USA across all platforms. Consequently, Disney redeveloped its planned Moana TV series as a movie. Great films are fantastic for streaming engagement.

Parks & Experiences:

Disney has the vacant acreage to build 7 new lands and significantly more “IP left to mine” or activate at these parks. It also has a thriving cruise business, which is in growth mode and poised for Asia expansion. Investment returns within these businesses are excellent and Disney is leaning in.

5. PayPal (PYPL) – CEO Interview

Alex Chriss talked with Morgan Stanley’s analyst this past week. The chat was quite reserved and calm. While investors criticized him for being too excited and optimistic at the beginning, they have since shifted to being critical of the exact opposite. Ironic. To me, this is a byproduct of poor stock performance, which I blame on the old team and not Chriss. Let’s see if he executes in 2024 and beyond rather than picking on every single word that comes out of his mouth.

On Transaction Margin Guidance for 2024 & Guidance Overall:

“I've been in the seat for 4 months. Most of my leadership team has been in less. So it was prudent for us as we get to our first guide of the year to be very thoughtful to give ourselves the flexibility that we need. That's just a smart way for us to think about it. I want to get points on the board before we get ahead of ourselves in terms of guidance.” – Alex Chriss

Guidance was probably sandbagged.

He spoke on the “combination of acquisitions that have been a drag to the business.” He’s addressing all of these areas (like with Happy Returns sold to UPS) with a goal to exit 2024 only with assets contributing to transaction margin dollar growth. As an aside, the 2024 guide assumes sector-wide e-commerce performance is similar to 2023.

On 3 areas of transformation:

“I know everyone is always impatient. I'm impatient as well. 4 months in, I think we actually have made a tremendous amount of change.” – CEO Alex Chriss

Chriss was asked about the clearest changes he has made to PayPal. He split the response into a couple buckets. First, he refreshed the entire c-suite level and most of the senior vice president (SVP) level as well. He brought in quality candidates with impressive resumes and a fixation on delivering great products. He also revamped the reporting structures for PayPal to be astronomically more transparent.

Chriss then shrunk the firm’s focus areas to branded PayPal checkout growth, profitable Braintree growth and Venmo monetization. He shared the learnings from his very first meeting at PayPal as product leaders talked through a couple hundred disparate offerings and progress reports on all of them. Halfway through the meeting, he paused the event to point out how PayPal’s suite was spread far too thinly; he challenged his team to prioritize focus areas. They closed or sold-off everything that didn’t perfectly fit into its renewed, tightened objectives. He condensed innovation and restructuring work set to take 2-3 years down to just 60 days. He moved with great urgency from day one, and while changes will take time to show progress, this urgency is well-placed.

Along the lines of product innovation, it launched Tap to Pay on iPhone for Venmo and Zettle users in the USA.

Fastlane & Branded Checkout:

Chriss reiterated that PayPal has fallen behind in removing friction from online branded checkout. He thinks this is especially true in mobile checkout, where PayPal has underinvested, per Chriss. Priority one is making PayPal’s checkout experience best-in-class once more. It has a brand trust, acceptance, privacy and security edge vs. everyone else. Chriss no longer thinks it has a checkout quality edge and aims to address that.

Fastlane is a material piece of this goal. As a reminder, Fastlane was one of the product launches from PayPal’s first look event. Merchants must be Braintree or PayPal Commerce Platform (PPCP) customers to use it. Fastlane allows merchants to tap into PayPal’s massive customer data vault to identify about 70% of consumers simply with an email. This morphs guest checkout from a manual, tedious process into something much easier and more delightful. With more than half of online checkout still being through guest checkout, PayPal thinks it just “leapfrogged” all competition in terms of the guest checkout utility it provides. Specifically with Fastlane, the 80% average conversion rate early on is an incredible 4000 basis points higher than normal guest checkout.

Once PayPal delivers a delightful experience, it can take advantage of post-purchase consumer touchpoints to educate customers on incremental savings to enjoy. It can leverage happy customers by telling them they’re happy because of PayPal….and by the way here are all of the other ways PayPal can make them even happier. It can also use these touchpoints to offer highly targeted promotions through smart receipts or its advanced offers program, which juice repeat purchase activity. Customers get unique value thanks to PayPal’s massive merchant base; merchants get precisely targeted customer acquisition sources thanks to PayPal’s massive scale. And these merchants only pay for that value upon actual sale conversions. That takes the guesswork out of customer acquisition cost (CAC).

This is a big piece of his vision to extend PayPal’s checkout presence to more pre and post purchase instances. This is PayPal leveraging the reality that it knows its customer better than the rest.

“Branded checkout volume is healthy and growing. Transaction margin dollars for branded checkout are growing well. I think there is more room to expand, but it’s doing well for us. We need to nail the experience.” – CEO Alex Chriss

Venmo & Braintree:

Venmo is a juggernaut within affluent GenZ and Millennial Americans. It has among the broadest reach of any fintech, yet has done an awful job of monetizing its passionate user base. Chriss hinted at Venmo realizing monetization through more banking services. He teased more ways to use Venmo funds once they’ve entered an account; he spoke about making routing numbers more easily available. That last note likely means it will dip its toe in direct deposits and high-yield savings accounts.

Aside from e-commerce checkout, Venmo will monetize its business profiles more powerfully with local customer targeting tools. Because of Venmo’s social payments feed, transactions can serve as stamps of approval from friends voting with their wallets instead of an influencer saying “trust me, try this.” That local flare for Venmo is a key separator from competition in my view. Unleashing and targeting the value from this feature can enhance merchant success while PayPal works to give Venmo users more financial service tools.

Not much new was shared about Braintree. Chriss simply reiterated that the company has been competing aggressively on price and will no longer do that as a critical mass of scale is now established. There’s a clear line of sight to driving profitable Braintree growth through expansion downstream, international growth and layering on value add services for clients like Meta.

A Quote to Leave you with:

“There have been different points throughout my career in which I've stood at a whiteboard and said, "Hey, does anyone know what to do?" That is not where we are right now. We know exactly what we need to do. This is all about execution, and it's about velocity. As a team, we’re working on making progress every single day and ensuring that our teams are just executing. That goes from innovation to go to market to customer service to OpEx. So velocity and execution. We know what to do. We just have to go do it.” – CEO Alex Chriss

6. Snowflake (SNOW) – CEO & CFO Interviews

CFO Michael Scarpelli & new CEO Sridhar Ramaswamy gave brief interviews with JMP Securities and Morgan Stanley this week. Here were the highlights:

Annual Guidance:

Snowflake’s recent annual guide rightfully spooked investors and sparked a new bull/bear debate. Bulls will tell you that the guide was sandbagged for the new CEO to come in and easily outperform during year one. Outgoing CEO Frank Slootman is a professional and that is what professionals do. Supporting this thinking, guidance assumes no improvement vs. somewhat weak 2023 consumption patterns. It also assumes no new products aside from Snowpark have any meaningful revenue contribution. That sounds like a classic case of under-promising to eventually over-deliver. As I always say, that is what an often shallow Wall Street cares about.

Bears will tell you not so fast. They’ll say that new open source storage options are eroding demand for keeping data within Snowflake. Storage revenue makes up about 10% of its entire business. Bears will tell you that competition like Databricks is impacting pricing power and that the degree of the guidance miss was too large to shrug off. It’s one thing to sandbag top line guidance by 1% or 2% for a new CEO. Snowflake missed on the top line by roughly 6%, which is a notably large miss. Its EBIT margin guidance of 6% also compared poorly to 9.2% margin expectations.

Who is right? I’m inclined to say the bulls, but next quarter’s results will likely make the answer much clearer. CFO Mike Scarpelli did tell us that revenue was shaping up about as expected this year, but we’re only a handful of days removed from their last guide. For now, there’s new uncertainty tied to Snowflake and it is still an expensive stock.

“We have a new CEO & so many new products that we won’t forecast until we see consumption history. I think there’s conservatism in our guidance… We would like to see Sridhar succeed as our new CEO." – CFO Michael Scarpelli

Potential Consumption Headwinds – Tiered Pricing, Iceberg Tables & Competition:

Snowflake will introduce tiered storage discounts for its highest volume customers. That’s already fully baked into annual guidance. Interestingly, Snowflake thinks the large customers eligible for these discounts will be the ones moving to Iceberg Tables for storage anyway. Iceberg Tables are open-sourced data storage offerings that are becoming popular due to lower storage costs, open-source integration flexibility and more data control. The new demand here is leading to data storage headwinds, with storage making up about 10% of Snowflake’s total business. It’s currently beta testing its own Iceberg Table product, but that won’t go live until June.

While this will be a FY 2025 headwind, it will be a long term positive in the eyes of leadership. How? It thinks the benefit of running queries across more open source data repositories will enhance the value of its product and generate more computing revenue over time.

From a competitive standpoint, Snowflake was directly asked about Databricks a few times. Snowflake thinks Databricks is ahead on its Notebooks product. Notebooks are collaborative and secure virtual environments for data science work. They allow for working on workflows remotely with colleagues in multiple source code languages. Snowflake is quickly working to catch up. For now, it partners with Databricks to combine this tool with its own compute and workload storage services in a “frenemy” type relationship. When this product goes live, that dynamic will surely become less friendly.

“We are behind on the notebook. We acknowledge that. There's a product in private preview. Just like with AI, where we went from not quite there to being world-class in 6 months, we will make sure that we ramp up with that much ferocity and velocity.” – CEO Sridhar Ramaswamy

The team pushed back on the notion that Databricks is cheaper. Its Snowpark product, for example, is “dramatically cheaper” than the Databricks alternative. Finally, it also pushed back on the idea that it was behind in unstructured data (which is wildly important for GenAI). It thinks its data lakes and coinciding services effectively compete against everyone.

Spending Environment:

Scarpelli called the spending environment quite good based on enhanced multi-year bookings appetite. How does that coincide with poor annual guidance? There’s still one pocket of weakness within venture-backed companies, which make up 10% of revenue. Those firms were the most aggressive consumption growers throughout 2021-2022 and have not yet normalized spending levels. For larger, more established customers, spending motivation is strong. These more mature customers are just slower and more intentional in growing their own Snowflake platform usage.

This lack of bounce-back for the VC consumption bucket is what led to Snowflake walking back its $10 billion in ARR guidance schedule. They still think there’s a chance to get there, but need to see a sharp acceleration in consumption, which they’re not counting on.

Why Ramaswamy as the new CEO & Why he Wanted the Job:

The interview made it crystal clear that Snowflake was not innovating and not shipping products quickly enough under Frank Slootman. It was not arming its go-to-market teams with the tooling needed to optimally capture robust demand. I talked about this innovation dawdling during the earnings review as personal speculation; this interview confirmed it.

Scarpelli alluded to Snowflake Unistore taking two years to develop and the delays that project has endured. He further told us about important integration capabilities missing from Snowpark that should have been addressed more expediently. He juxtaposed that with Ramaswamy spearheading the launch of Snowflake’s complex Cortex GenAI tool in just 7 months. Scarpelli even jokingly complained a bit about Slootman never being in the office. Perhaps he was somewhat checked out… and who could blame him after his decades-long masterpiece of a career. Go buy a big boat and enjoy life, Frank.

Slootman is a world-class operator, but he and the firm felt that operational skills paired with a “deep tech background” were required. Enter Ramaswamy, his PHD in Data from Brown, his building of Google ads into a massive business and his successful exit as CEO of Neeva. The succession plan was two years in the making, and this was Snowflake’s top choice by far.

He wanted the job as he sees Snowflake well positioned to capture a $100 billion revenue opportunity.. GenAI is a big reason for that. No company can effectively leverage GenAI without broad, overarching, organized access to all needed data. That’s what Snowflake provides. And it does so in a way that eliminates data replication risk thanks to its overarching view of every relevant public cloud.

New Products:

Aside from Snowpark, Cortex is the product that has Scarpelli most excited for 2024. Cortex is its “managed AI and search product” that integrates with its other AI tools as a “core AI layer shipped with every AI deployment.” It’s offered at the platform level and so is available to every Snowflake customer. This is what powers things like sentiment analysis in a no-code, easy-to-understand way. It also facilitates semantic index search to erode query friction and make Snowflake easy to use for everyone… not just developers. That will pair quite nicely with its planned Copilot assistant, making conversational querying wonderfully simple and powerful. It’s also hard at work on Copilot query response accuracy. The best models in the world still deliver wrong answers about 15% of the time and leadership believes that Copilot can shrink that substantially.

GenAI models brought in to fine-tune through Cortrex and the Data Cloud could offer a nice consumption tailwind. Aside from this, other new tools like Unistore won’t meaningfully contribute until 2025.

Do you love Twitter (sorry, not X) as much as I do? Do you only want investing-related content on that app? Do you get frustrated by all of the noisy content you scroll through to find the nuggets you actually care about? Same! Blossom is here to fix that. This is focused FinTwit meets serious investors meets portfolio tracking. It’s a thriving social media platform for us nerds and it just launched in the USA. It’s entirely free to use and something that I now post on daily. Check it out here and sign up. See ya there.

7. Earnings Round-Up

a. Broadcom (AVGO)

Results:

Beat revenue estimate by 2.0%.

Beat $10.42 EPS estimate by $0.57.

Guidance & Valuation:

All annual guidance was reiterated & roughly met estimates.

Balance Sheet:

$11.9 billion in cash & equivalents; $76B in total debt.

Rapid diluted share growth & infrastructure software growth via VMWare M&A.

Paid off $3 billion in debt calendar 2024 YTD.

b. GitLab (GTLB)

Results:

Beat revenue estimate by 3.5% & beat guide by 4.0%.

Beat $5.5M EBIT estimate by $7.3 million & beat guide by $7.7 million.

Beat $0.08 EPS estimate & beat same guide by $0.07 each.

Annual Guidance & Valuation:

Missed revenue estimates by 1.3%.

Sharply missed $31M EBIT estimates by $23 million.

Missed $0.37 EPS estimates by $0.21.

Balance Sheet:

$1 billion in cash & equivalents.

No debt.

Shares +4.3% Y/Y.

$33.4 million in 2023 FCF vs. -$83.5 million Y/Y.

8. Alphabet (Google; GOOGL) – Chief Business Officer Philipp Schindler Interview & Some Contemplation

Most of this interview was a review of recent earnings reports and press releases. It covered product innovation within cloud computing and advertising that I’ve already covered multiple times in detail.

The dialogue around search and GenAI disruption is the only item worth covering. There’s a class bull/bear debate forming around Google. Bulls say that Google seamlessly embraced previous search revolutions like mobile and social better than most expected at the time. They’ll tell you that Google’s unmatched search data set, world-class talent and fortress balance sheet put it in the best position to succeed amid the GenAI boom. They’ll say Google isn’t concerned with first mover advantage, but instead with model perfection for its generative search product in beta testing. The most powerful models still give wrong answers more than 10% of the time. Google is more fixated on eliminating that issue vs. rushing out upgrades to its search experience.

Bears will say that search drives Google’s entire business. If they lose even a few % in market share, that would be quite material to results. They’ll also say that generative search will never carry the margins that its current search product does, so succeeding here may be good for revenue, but not margins. Schindler expressed conviction in monetization for GenAI search eventually being strong. He discussed all of the new interactive advertising opportunities that it will have and how better targeting should improve impression value too.

This is hauntingly similar to what Meta was going through in 2021-2022. It needed to shift to Reels, but Reels didn’t monetize at a rate anywhere near its other content formats. Fast-forward to today and it’s a monetization and revenue growth tailwind for Meta overall. The first greenshoot for Reels was the engagement boost. The second was improving monetization. We’re already seeing engagement boosts from Google’s Generative Search (SGE) product in the markets where it’s testing.

One could also argue that OpenAI and Microsoft provide a newly intimidating competitive threat just like TikTok did for Meta. Despite the similarities, Google is still within sniffing distance of all- time highs while Meta plummeted by 70%+ from peak to trough. I think Google will figure things out just like Meta did. I think there will be growing pains just like there were for Meta. I think there could be some stock turbulence associated with those headaches. And I’d be eager to start a new position here if Mr. Market decided to give me an overly compelling deal. I am candidly concerned about Google’s profit and share position in search. Still, Google Cloud is a 20%+ grower, younger generations live on YouTube and its balance sheet provides significant opportunity for manufactured earnings growth.

Schindler called visual model bias Google has been criticized for “unacceptable.” It’s hard at work on fixing the issues and has already “made significant progress.”

9. Cloudflare (NET) & Zscaler (ZS) – Executive Interviews

While not much new was shared in either interview, we got further evidence that there is no “spending fatigue” within next-gen cybersecurity buckets. Cloudflare “had a great quarter and so did some of its peers.” Its ability to tie Zero Trust security into its content distribution network and distributed denial of service (DDoS). Its platform approach is working and its transformed go-to-market team is too. Zscaler basically said the exact same thing. It talked up its platform and ability to consolidate vendors. CEO Jay Chaudhry also said if you cannot deliver good products AND cut client costs, you’re likely struggling. If you can do both, like Zscaler can, you’re not struggling. Network security demand is rocking for next-generation disruptors displacing patched-together product suites and firewall hardware.

10. Market Headlines

Meta (META) – The House Energy and Commerce Committee unanimously voted to force Bytedance to sell TikTok or face a U.S. ban. TikTok’s plea to Congress seems to have failed as a consensus vote on something like this is not common.

Uber (UBER) – Uber will partner with Mastercard and Payfare on Mastercard’s Pro Card program in Canada. This will give drivers immediate access to earnings and will let them earn 4% cashback on gas and 8% cashback on EV charging.

11. Macro

Employment and Consumption Data:

JOLTS Job Openings for January were 8,863,000. This compares to 8,800,000 expected and 8,889,000 last month.

Initial Jobless Claims were 217,000 as expected.

Non-farm Payrolls for February were 275,000. This compares to 198,000 expected and 229,000 last month.

The Labor Force Participation Rate is unchanged at 62.5% for February.

The Unemployment rate is 3.9% for February. This compares to 3.7% expected and 3.7% last month. Closer to the first rate cut we come.

Output Data:

The Services Purchasing Managers Index (PMI) was 52.3 in February. This compares to 51.3 expected and 52.5 last month.

Factory Orders M/M for January fell 3.6%. This compares to -3.1% expected and -0.3% last month.

The Institute for Supply Management (ISM) Non-Manufacturing PMI for February was 52.6. This compares to 53 expected and 53.4 last month.

The ISM Non-Manufacturing Prices reading for February was 58.6. This compares to 62 expected and 64 last month.

Non-farm productivity rose 3.2% Q/Q in Q4. This compares to 3.1% expected and 4.7% last quarter.

Inflation Data:

Unit Labor Costs rose 0.4% Q/Q in Q4. This compares to 0.7% expected and 0.1% last quarter.

Average Hourly Earnings M/M for February rose by 0.1%. This compares to 0.2% expected and 0.5% last month.

12. Portfolio

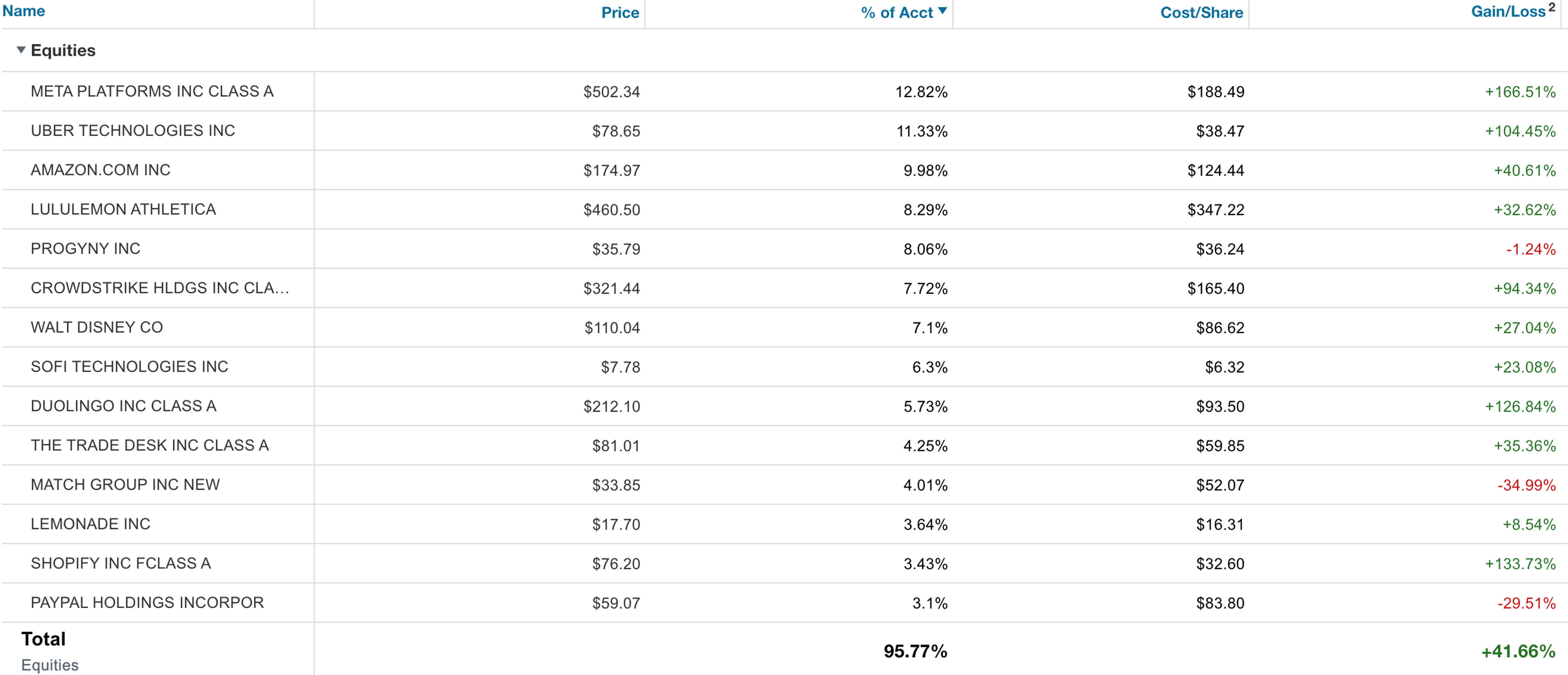

I boosted my Disney stake by 7.5%, my SoFi stake by 2%, my Lulu stake by 10% and my Progyny stake by 4%. I reduced my CrowdStrike stake the 11%.

Thanks for the great analysis and detailed report...

Excellent edition!