News of the Week (July 10 - 14)

News of the Week (July 10 - 14)

When to Sell; Meta; SoFi; Uber; Shopify; Microsoft; JP Morgan; UnitedHealth Group; Pepsi; Amazon; Upstart; Macro; Portfolio

Today’s Article is Powered by Savvy Trader:

1. When to Sell?

We constantly discuss fundamental research as the basis for justifying an investment. But when is it time to sell? While the answer to this question is highly subjective, we do have our opinions which we will briefly share in our typical long-term investing point of view.

a) When I Exit a Position

The decision to continue holding a company and allocating time, energy and money to the business must be emotionless and rational. Investments do not deserve our loyalty and certainly don’t deserve our unconditional love. They don’t care about you or me. Falling in love with a stock is a great way to let bias interfere with a calculated sell or hold decision.

So what’s involved in cool, calm and collected decision making? It all starts with identifying a stock with a solid bull case and learning it. Knowing the prospects, performance, and execution is the only way to judge a stock. It’s how I can know when an investment case is deteriorating or if things like sentiment are simply turning irrationally negative. So? It’s the only way I know if overly negative price action is to be approached with greed or caution. If we are relying on an incomplete argument to support a buy or hold decision, we leave ourselves extremely vulnerable to approaching alpha-fostering price action with anxiety rather than opportunism. In sum, determining when to sell is as simple as identifying if there is a broken stock, or a broken company.

What are some good reasons to exit a holding? Here’s an incomplete list:

Sharply slowing revenue growth over a string of several quarters.

Margin or market share deterioration over a string of several quarters.

An increasingly fragile balance sheet with shrinking liquidity and/or skyrocketing debt.

Egregious stock-based compensation and maligned leadership compensation incentives.

C-suites serving as a revolving door of entrants and exits.

Signs of a toxic work environment (like high employee churn).

Here’s an incomplete list of bad reasons:

A new competitor just entered the large, fragmented market.

The CEO sold some shares.

This person was elected President of the USA instead of this person.

The CPI print was a little too high this month.

The stock sold off after a strong earnings report.

This person on social media says it’s a bad investment in all capital letters.

A sell side analyst downgraded the name.

You’ll notice that poor financial performance over a “string of several quarters” is generally required to manifest an exit decision for me personally. Businesses are not perfect, hiccups are somewhat inevitable and a “one strike you’re out policy” is too harsh and premature. Iconic companies throughout their histories have ALL had missteps and exogenous factors or mistakes weigh on performance from time to time. Microsoft messed up Windows 8 and Zune, iPhone 6 dealt with bending issues and Amazon has flopped on several product releases. These 3 companies are 3 of the most successful in the history of humanity. It’s when missteps become more consistent that they become more concerning.

b) When I Trim a Position

The section above intentionally ignores valuation, but valuation is a highly important part of investing -- especially now that real rates are not negative and stimulus is not being pumped into the economy. To me, valuation is never a reason to completely exit a fundamentally thriving company. Why? Because profit estimates forming presumed valuations are routinely wrong. And furthermore, stock prices are living, breathing entities that go from expensive to cheap with no notice. We have no crystal ball. If valuations become stretched to the upside but the company continues to perform, we maintain a smaller position because of our belief that the company will grow into the stock price.

With that being said, valuation and multiple expansion is THE MAIN reason for personal decisions to trim holdings. Investing is all about seeking out compelling risk/reward. As multiples expand, that risk/reward naturally becomes less favorable. That doesn’t mean capital appreciation based on more multiple expansion can’t happen, but it does make that source of future profit less likely.

In terms of rules, I am deeply in the Peter Lynch camp of utilizing PEG ratios to judge valuations. A PEG ratio takes the P/E ratio and divides it by rate of earnings growth. For the sake of smoothness, I use 2 or 3 year earnings compounded annual growth rates (CAGRs) for the denominator. Again, this is just how I do things and many other bright individuals will invariably have a related, yet different process. As an overgeneralized rule of thumb, as holdings cross a PEG ratio of 2x or greater, I often will elect to trim 5%-10% of a position. As PEGs expand further beyond 2x in increments of 25-50 basis points (bps), I elect to make similarly sized trims. Why is there a bps range rather than a preset number?

It goes back to financial estimates sometimes being wrong. For holdings like Uber and Amazon, I don’t think analyst expectations have come remotely close to modeling the incremental efficiency and cost cuts that have been built into the models. Other reasons for the range include:

For some companies like the Trade Desk, we have a several years-long track record of constant beats and raises vs. consensus estimates. In this case, PEG ratios formed with forward estimates probably are unfairly high.

The highest quality growth companies in the world deserve premiums vs. everything else in the market. From my portfolio, I put Meta, Amazon and CrowdStrike (1 out of 1 in terms of scale, margins and growth) in this bucket.

When using a P/E ratio in isolation, we can be tempted to call a 10x earnings firm cheap and a 50x earnings firm expensive with no other context. But what if the first company compounds earnings at 2% annually and the second at 50% annually? The PEG will allow us to credit this growth with the first company sporting a hefty 5x PEG and the other 1x. This is why I prefer PEGs. If there is no net income to value, I use EBIT. If there’s no EBIT, I begrudgingly use gross profit. Revenue should never be used for valuation multiples as the quality of $1 in revenue differs massively between companies. Some can spend $1 on $10 in revenue. Some can spend $20 on $10 in revenue. Both have $10 in revenue.

c) Euphoria Creeping Back In

Euphoria seems to be creeping back into the market sentiment fold. This is not a repeat of the Fed Bubble, but fear is briskly being replaced with greed. Fundamentally broken companies like Nikola -- just a couple years removed from being caught pushing their semi truck down a hill in a demo video -- are jumping 60% in a single session. Coinbase has doubled in the blink of an eye and the most speculative holdings in my portfolio are the ones rising the most.

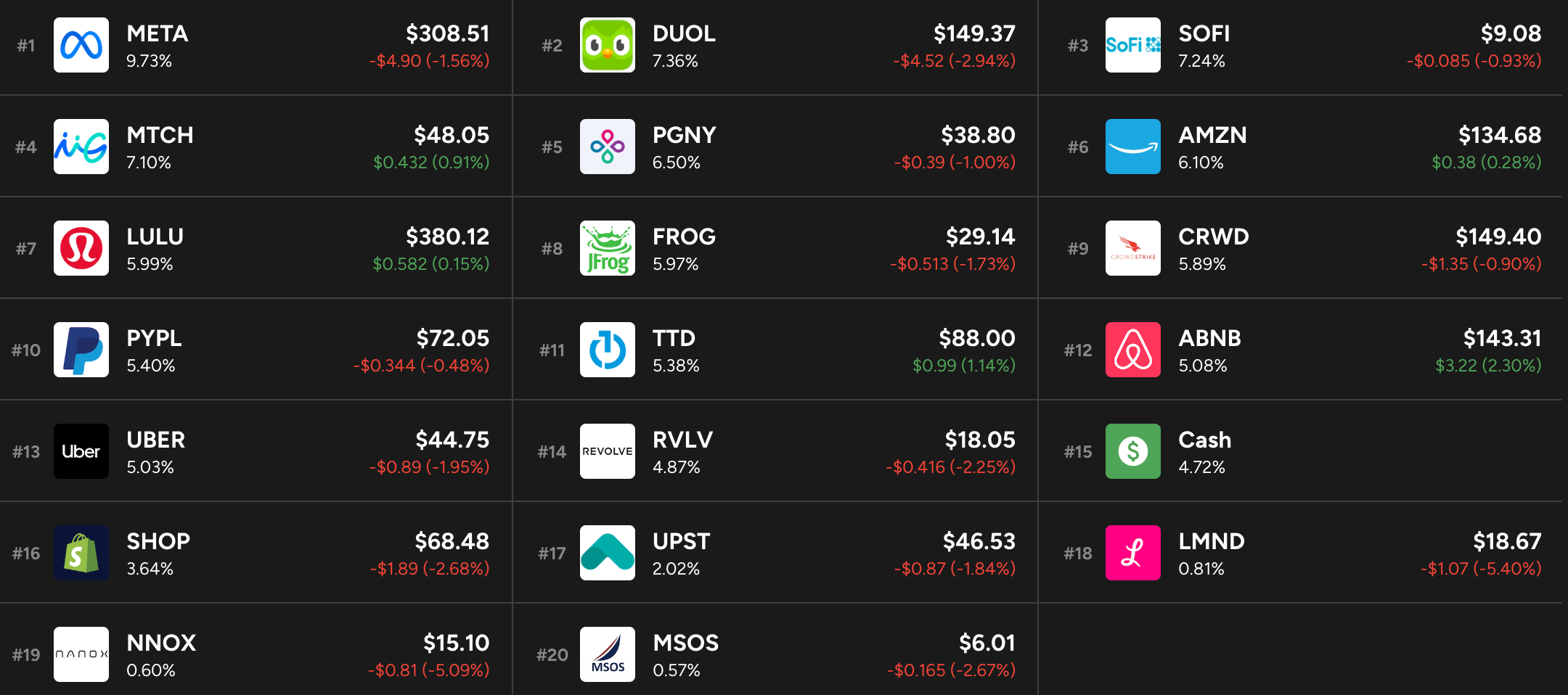

I will always be predominately invested. But in a world where I embrace “greedy when fearful and fearful when greedy” it is time to shift away from the greed I’ve been exercising for the last year + and to take a more balanced market view. Some valuations are getting nutty, I’m again hearing that “fundamentals and valuations don’t matter” way too often, and macro (despite a great looking CPI and PPI this week) still has significant challenges. So? All of this is to say that I have entered trim mode (with the exception of a couple holdings) and will likely push my cash position from the current 4.72% level to somewhere closer to 10% if things stay this fun. Nothing major, just some gradual cash building and preparation for the next dip.

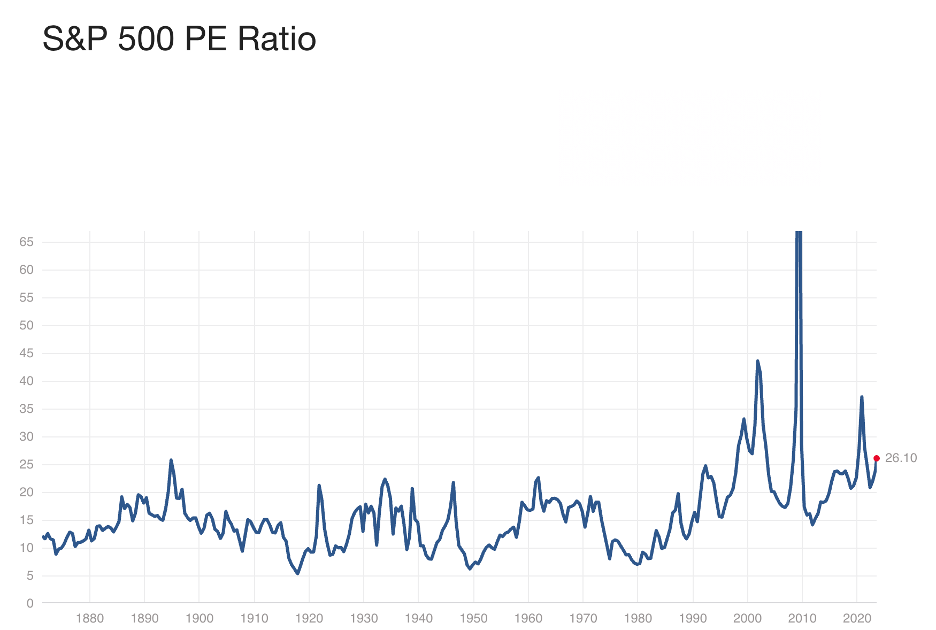

Raising a bit of dry powder for the market’s next inevitable fit seems prudent at this time as risk/reward deteriorates with steeper valuations. Many companies have set themselves up to demolish estimates this year, but that doesn’t change the fact that 26x earnings for the S&P 500 is somewhat stretched:

2. Meta (META) -- Roblox, Threads & More

a) Roblox

In the race for extended reality (XR) market share, content will be king. Both Apple and Meta will have to build ecosystems and incentives that win the hearts, minds and work of talented 3rd party developers. While that will be imperative, jumpstarting the content ecosystem with key partners will be another important piece of the puzzle. Apple has inked important deals with firms like Disney and Unity while Meta has its own relationships with entertainment juggernauts like Paramount. Now, according to a Roblox developer blog and confirmed by Zuck himself, Meta will add the immensely popular Roblox platform to Quest.

Not only will this be a vast injection of fresh, relevant content into Quest, but will mean a large ecosystem of Roblox developers more motivated and driven to build XR experiences for the Quest App store. Roblox developers, with very little XR-experience, will be able to easily use Meta’s tools and Roblox’s cross-channel presence to leverage their existing titles for use within the XR ecosystem. The direct relationship and integration should drive a larger proportion of Roblox’s 66 million DAUs to Quest. Roblox’s malleability will mean these gamers can play with Roblox users across devices including Xbox and Apple’s iOS.

To start, Roblox will beta test within Quest’s app incubator. That soft launch will allow Roblox and its 3rd party developers to A/B test in a low stakes environment and craft the best experiences before broadly rolling out. Roblox’s user base is gigantic, young, and now can play its beloved games directly on Quest. Great news… but for a revenue stream that will not be needle moving in the coming years.

b) Threads

Here’s a fun fact: Meta’s new Threads app reached 100 million users in less than a week. That represents 8% of the time ChatGPT took to reach that level and 2% of the time it took TikTok. Threads is thriving right out of the gate thanks to the unparalleled network that Meta’s Family of Apps provides. Some data is pointing to engagement peaking following the first few days, but Meta leadership continues to post mind-boggling stats on how quickly the service is proliferating.

What’s the monetization potential here? Evercore sees Threads reaching $8 billion in revenue by 2025. That’s just 5.2% of total projected 2025 sales, but should represent a larger proportion of annual EBIT as this app should boast margins closer to its other apps vs. Metaverse investments. The large caveat here is that we don’t know how much of this new Threads engagement is stealing time from Meta’s other apps. Is it incremental or cannibalistic? The reality is likely a combination of both as creators prompt their newsletter and Twitter followings to join the new community (like me 🙂). Some of the engagement growth, however, will inevitably cut into time spent on the other platforms.

Today, the app stinks. Meta rushed it out to launch as Twitter was dealing with its self-inflicted engagement limit drama and hesitant advertisers. The plan was to get something released and then to work on fine tuning and product tweaking from there. That’s now taking place as subtle new features pop up on the app daily. Will Twitter die? We hope not and don’t think so. Leadership there has even talked up record setting engagement in recent days. Still, will Threads likely win at least the occasional eyeballs from Twitter? Probably so. The master of copycatting strikes again. Whether it’s Stories, Reels or now Threads, Meta is the king of using social media competition for its own product R&D.

c) More Meta News

Meta continues to embrace open-sourced AI. It will release a commercial version of one of its latest models for developers to build on top of. These models allow for automated generation of images, code and more.

It’s new speech model can more accurately account for accents and impediments.

TD Cowen upgraded Meta to overweight due to expected estimate beats, Reels engagement strength, Threads potential and the ability to cut more costs. There was some other alt-data that surfaced this week on strong Reels monetization trends. As always with alt-data, this could just be noise. It’s either good news or irrelevant.

Savvy Trader is the only place where readers can view my current, complete holdings. It allows me to seamlessly re-create my portfolio, alert subscribers of transactions with real-time SMS and email notifications, include context-rich comments explaining why each transaction took place AND track my performance vs. benchmarks. Simply put: It elevates my transparency in a way that’s wildly convenient for me and you. What’s not to like?

Interested in building your own portfolio? You can do so for free here. Creators can charge a fee for subscriber access or offer it for free like I do. This is objectively a value-creating product, and I’m sure you’ll agree.

There’s a reason why my up-to-date portfolio is only visible through this link.

3. SoFi Technologies (SOFI) -- Mortgages & a Noto Interview

a) Mortgages

Two weeks ago, we discussed the debut of SoFi’s first mortgage product following its acquisition of Wyndham Capital. Since then, all of our inboxes have been inundated with SoFi promotions showcasing unique mortgage offers. These two pieces of news indicate that the company is ready to push external marketing for home loan originations. The service and time-to-fund issues it was having with backend fulfillment partners appear to potentially be behind it, and the timing is perfect.

Mortgage rates are in the process of peaking right now. With rate cuts directly feeding mortgage demand, macro headwinds are turning to tailwinds right as SoFi is becoming aggressive. This should provide a great offset to cooling personal loan demand as variable to fixed personal loan refi demand wanes amid falling rates (less likely to want to lock in a rate if your rate is variable and yields are falling). Finally, SoFi has very little mortgage market share. It dominates in student refi, has rapidly built share in personal and thinks it now has the recipe to follow that path within home loans. Considering the gigantic size of this credit bucket, traction here would quickly become impactful to overall performance. We’re optimistic.

b) Interview

SoFi’s CEO Anthony Noto was interviewed on CNBC this week. He was immediately asked about Morgan Stanley raising its SoFi price target and downgrading it to underweight. There were three reasons behind the note. The first two were on valuation risks to its book of credit and student loan headwinds from the proposed payment on-ramp. We’ve extensively covered why the credit book is safe in previous articles. Here’s a summary of the main points:

Its credit niche is highly affluent with average income over $150,000 per year and an average FICO over 750.

It has a 3rd party conduct quarterly fair value markings, based on capital market demand and macro, that flow through its financial statements. This form of accounting vs. CECL makes the potential for misaligned valuations, unrealized losses and shady behavior even lower, not higher. These markings assume 2.5% GDP contraction this year which is pessimistic.

Its loss ratios are still 50% below 2019 levels as it continues to outperform peers and benchmarks.

It has done nothing but maintain or tighten credit standards throughout this cycle. It isn’t gaining volume by issuing riskier debt.

In terms of the former student loan on-ramp headwind, Noto seemed quite confident in the volume still coming and student loans still being a sharp tailwind for 2024. How? Interest will accrue under the proposed on-ramp and so borrowers will still be driven to seek lower rates. SoFi sees a large chunk of credit ripe for granting lower rates in today’s environment. That chunk will merely grow as we enter the rate cut phase of this cycle. It’s the people looking to extend term periods to lower principal payments who may take more time to refinance if the on-ramp is allowed. That’s a somewhat large if. It’s very unclear if this on-ramp proposal will even be allowed. The Supreme Court has struck down the administration’s ability to offer its relief plan, why would this next attempt be allowed? Expect more lawsuits and potentially another supreme court hearing.

The third reason behind Morgan Stanley’s bearish note was on it valuing SoFi as a bank rather than a tech firm. Noto welcomed this classification despite SoFi’s potentially promising tech branch, its more asset light, branchless model and its rapid growth and margin expansion. He indicated a clear path to 30% ROE for SoFi. Banks that fetch a 30% ROE typically have a tangible book value multiple of 4x-5x. SoFi’s is under 3x today. This leaves room for long term multiple expansion to feed capital appreciation while compounding should provide the largest part of this stock’s upside. Want to value it like a bank? No worries.

All in all, this was a mostly fair note. The repeated concerns around the credit business were a bit annoying, but when a stock doubles in 2 months, valuation concerns are warranted. Gains of that magnitude almost always need to be digested.

4. Uber Technologies (UBER) -- Domino’s & The Team

a) Domino’s

Domino’s is famously known for its pizza… and for making its customers have that pizza delivered directly through its app. That just changed. This week, UberEats (plus its Postmates brand) announced a new partnership with the largest pizza chain in the World. The new program will begin testing this fall with a full debut in 28 markets across North America by year’s end.

Why does this matter aside from it meaning another large, bellwether brand on UberEats? Glad you asked. There are a couple of reasons. First, this marks a sharp pivot in philosophy for the famous pizza chain. In the past, Domino’s has not only avoided support for 3rd party delivery fees, but it has allocated external marketing dollars to openly criticize the model and associated costs.

There are very few chains with Domino’s liquidity, slick app, resources and presence, yet it’s going with the unmatched power of Uber’s gigantic network. Massive partners continue to choose Uber out of respect for this verb-fueled ecosystem rather than trying to expensively build traffic on their own.

Google’s Waymo is now partnered with all Uber business segments for autonomous driving, Amazon partners with Uber for flexible fulfillment capacity and Prime member rewards, and large chain holdouts like Domino’s are accepting the need for Uber’s delivery demand augmentation as inevitable. Scale matters in the transportation of people and last mile goods. No company in the space comes close to Uber’s reach and capabilities which is likely why it was chosen as Domino’s exclusive 3rd party partner.

The argument against this upbeat takeaway would be that Domino’s is simply struggling to stay fully staffed and to preserve margins. The fact that Domino’s employee base will actually be making all deliveries on orders through UberEats puts that argument to bed. It truly is about reaching large incremental cohorts of potential customers and Uber provides that edge in unique fashion. Its client base alone is expected to be largely incremental and add a billion in sales to Domino’s business. That added billion would represent a 20%+ boost to current sales to give you an idea of how impactful this news can be. Nearly every other large pizza chain uses demand channels like UberEats… Domino’s is finally ready to follow suit.

“We’re excited to announce this unique partnership with Domino’s globally -- both starting as their exclusive third-party marketplace partner in the U.S. and making their menu available to our consumer base around the world. We look forward to bringing customers the convenience, tech & experience that are foundational to both of our brands.” -- Uber CEO Dara Khosrowshahi

b) The Team

CFO Nelson Chai is stepping down after more than 5 years with the company. While it’s never ideal to see a CFO leave, the lack of C-suite churn makes it less concerning. Before passing judgment, we’d like to see where he ends up next. If he gets a sizable promotion as, for example, the new CEO of PayPal or simply wants to retire, this news is irrelevant. If he makes a horizontal move which is followed by more leadership churn, then it becomes worrisome. For now, TBD.

More Uber News:

Evercore named Uber as its top pick amid an explosion in margins, steady demand growth and an expectation of a near future buyback with the building cash pile. Another firm turning bullish on the once polarizing name. Join the club.

UberEats is partnering with Waitrose in Great Britain to offer high end grocery delivery.

5. Shopify (SHOP) -- Batman Meet Robin, Roku & Lightening Up

a) Batman Meet Robin

If Batman were the Shopify product suite serving as the vital central operating system (or hero) of a merchant’s business, Batman just found his Robin. This week, Shopify announced “Sidekick” as its new chatbot purpose-built for actionable merchant use cases.

Sidekick will debut later this year as a conversational assistant to handle tedious merchant tasks. It can be prompted to add a new product and description to a page, can design marketing campaigns for a merchant and can run product promotions when asked to do so. This is not just a fancy piece of software for the sake of entering the field of Gen AI. This is a productivity enhancer and a success augmenter that allows merchants to focus on the most pressing pieces of their operations.

This is everyone’s “year of efficiency.” Meta said it first and virtually every other public company followed suit. Efficiency entails doing more with less, and this new tool should emulate the roles and functions of customer support, product and marketing teams for merchants with typically quite finite resources. Sidekick will make Shopify a better partner for manifesting that needed efficiency.

For Shopify, this should also be an efficiency boost. It’s easy to see how sidekick could handle onboarding issues or general functions. Theoretically, it will replace a lot of the nearly 1,000 customer support staff Shopify unfortunately laid off last year and allow it also to do more with less. With the more balanced focus on growth and profit and added emphasis on free cash flow generation under new CFO Jeff Hoffmeister, this product could help thread that needle.

b) Roku

Shopify added another external selling channel integration for its merchants this week. Now, merchant customers watching content on Roku will be able to directly buy products through linked advertisements. Shopify’s commitment is to ensure that its merchants are as successful as possible. Doing so requires channel omnipresence to guarantee products are wherever fans are spending their time. Whether its Meta, YouTube, TikTok, Pinterest, JD.com or Roku, Shopify is delivering on that need more completely than any other competitor. Moreover, multi-channel implies more complexity which works to tighten merchant relationships, retention and dependence on Shopify.

c) Lightening Up

I sold a quarter of my stake in Shopify this week. At about 25x 2023 gross profit, it trades for roughly triple the valuation of the S&P. It certainly deserves a hefty premium given the growth and margin potential, but that is pushing ridiculous in my view.

Shopify will probably beat the profit estimates that are supporting these valuation multiples. However, the beats will likely need to resemble Nvidia’s last quarter for this thing not to take a breather. As always, expensive could get more expensive, estimates could be even further off than we think they are, this could continue racing higher and we could be wrong. Data from Roth pointing to robust merchant growth this quarter makes that scenario a little more likely. But still, risk/reward has simply become less compelling since I started the position a few months (and a 100% gain ago) at a valuation I could just barely tolerate. As discussed in the “When to Sell” section above, I never liquidate fundamentally thriving firms with long runways that are ahead of themselves near term. I just trim. Shopify feels well ahead of itself, so the trim was larger than it normally is for me. Trimming is how I always have cash available when opportunities arise in the portfolio.

6. Microsoft (MSFT) -- Mega Cap M&A? and Network Security

a) Mega Cap M&A?

In May, the European Commission (EC) approved Microsoft’s proposed $69 billion acquisition of Activision Blizzard (ATVI). It required some concessions like licensing the gaming content to competition for a decade, but not much else. This week, a Federal Judge in North Carolina blocked an injunction from the Federal Trade Commission (FTC) to put the deal on pause in what was seen as a big win for the duo. The FTC appealed the decision which was denied last night.

When pairing those developments with FTC chain Lina Khan being chewed out and criticized for her decision-making by Congress this week, the mega cap M&A floodgates may be re-opening. For the last few years, large cap deals have been all but shuttered by strict FTC oversight; this marks encouraging signs that the oversight may be loosening. You best believe that every single mega-cap name has a long list of M&A targets on their wish lists. Those wish lists may actually be becoming realistic.

b) Network Security

Microsoft is debuting a new Secure Service Edge product. It announced the new offering this week as its entrance into network security to directly compete with Zscaler and Cloudflare among others. This is the last large opportunity in cybersecurity for Microsoft to pursue, and it will inevitably win some share. Its product offering will take time to get on par with established vendors in terms of cost and efficacy. Still, Microsoft will win share despite its product likely not immediately being best in class. Why? The enterprise bundle. That is a powerful selling point for clients yearning for vendor consolidation and simplicity.

Aries is a brokerage offering low cost tools like free option flow data and transactions to investors across the globe. It distanced itself entirely from a payment for order flow model to pave the way for operations in countries like the U.K. The interface is slick and intuitive and today, they’re looking for smaller investors to directly invest in their fund. If you’re interested in hearing more, you can pre-register to learn directly from the founding team here.

7. Earnings Round-Up -- JP Morgan, United Health & Pepsi

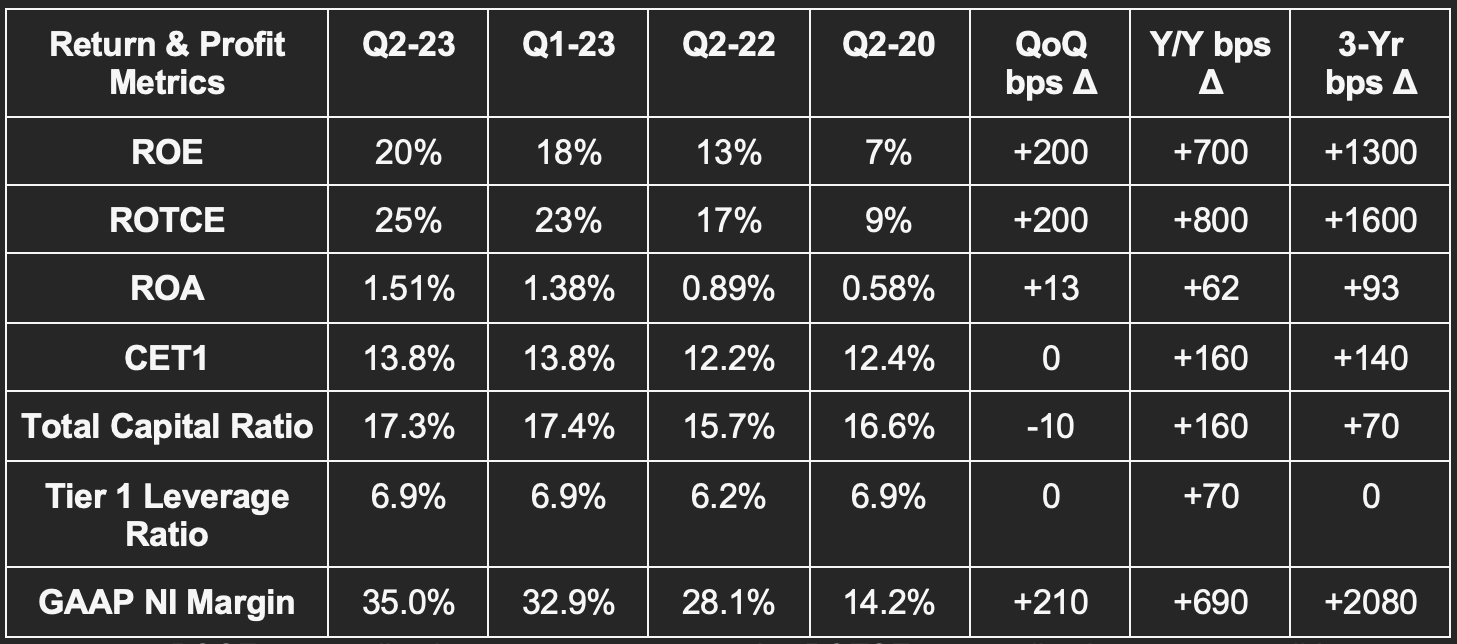

a) JP Morgan (JPM)

As arguably the premier financial institution in the World, JP Morgan offers a great view into the health of the consumer, fixed business investment and economic activity broadly speaking.

Results vs. Expectations:

Beat revenue estimates by 6.3%.

Beat/crushed $3.89 GAAP EPS estimates by $0.86.

Beat $96.96 book value per share estimates by 1.2%.

Beat Return on Equity (ROE) estimates of 16.1% by 390 bps.

Beat Return on Asset (ROA) estimates of 1.22% by 29 bps.

Forward Guidance:

JP Morgan raised its net interest income guide from $81 billion to $87 billion following its acquisition of First Republic. It also raised its adjusted expense guidance from $81 billion to $84.5 billion. This includes the FDIC’s planned systemic risk assessment. Finally, it continues to expect net charge-off rates on its book of credit of 2.6%. It sees delinquencies and charge-offs continuing to rise, but simply back to pre-pandemic levels.

Balance Sheet:

$1.4 trillion in cash & equivalents.

Dividend payments fell 3% Y/Y (still $1/share) while buybacks were $1.8 billion vs. $224 million Y/Y.

Report Highlights:

Notes from CEO Jamie Dimon:

Expects “material capital changes” from the finishing of Basel III CET1 updates and more changes in bank liquidity requirements stemming from this.

“The U.S. economy continues to be resilient. Consumer balance sheets remain healthy, and consumers are spending, albeit a little more slowly. Labor markets have softened somewhat, but job growth remains strong. That being said, there are still salient risks in the immediate view which I have written about over the past year. Consumers are slowly using up their cash buffers, core inflation has been stubbornly high, QT of this scale has never occurred, fiscal deficits are large, and the war in Ukraine continues. While we cannot predict with any certainty how these factors will play out, we are currently managing the Firm to reliably meet the needs of our customers and clients in all environments.” -- Dimon

Overall Results:

First Republic boosted earnings per share by a net of $0.38.

Organic Y/Y revenue growth was 21%.

Provisions for credit losses ex-FRC were $1.7 billion vs. $2.9 billion with it included.

CET1 and all of its capital ratios remain healthy and comfortably above regulatory minimums following the purchase of First Republic.

Built $1.5 billion in credit reserves in anticipation of deteriorating book health. This compares to a credit reserve build of $1.1 billion Q/Q and $428 million Y/Y.

Incurred $1.4 billion in net charge-offs. This compares to net charge-offs of $1.1 billion Q/Q and $657 million Y/Y. Pace of charge-offs continues to rise.

Commercial and Community Banking (38% ROE vs. 24% Y/Y):

37% Y/Y growth was 31% on an organic basis.

Net income was up 61% on an organic basis.

Average deposits fell 2% Y/Y while client investment assets rose 42% Y/Y.

Average loans rose 19% Y/Y.

Card services net charge-off rate was 2.41% vs. 2.07% Q/Q and 1.47% Y/Y.

Mobile customers up 10% Y/Y.

Provision for credit losses rose 145% Y/Y for the segment and 97% Y/Y on an organic basis.

Corporate and Investment Banking (15% ROE vs. 14% Y/Y):

Has a leading market share of Global Investment banking fees at 8.4% so far in 2023 vs. 8.1% at this time Y/Y.

Total market revenue fell 10% Y/Y with fixed income down 3% Y/Y and equity down 20% Y/Y. This should theoretically revert as appetite for things like IPOs improves.

Credit loss provisions here fell 36% Y/Y.

Commercial Banking (16% ROE vs. 15% Y/Y):

42% Y/Y organic revenue growth and 54% Y/Y organic net income growth.

Average loans rose 23% Y/Y while average deposits fell 8% Y/Y.

Credit loss provisions here rose 425% Y/Y and 134% Y/Y on an organic basis.

Asset and Wealth Management (29% ROE vs. 23% Y/Y):

8% Y/Y organic revenue growth and 10% Y/Y net income growth.

Inorganic contributions helped make this a record quarter for net asset inflows.

Assets under management rose 16% Y/Y to reach $3.2 trillion.

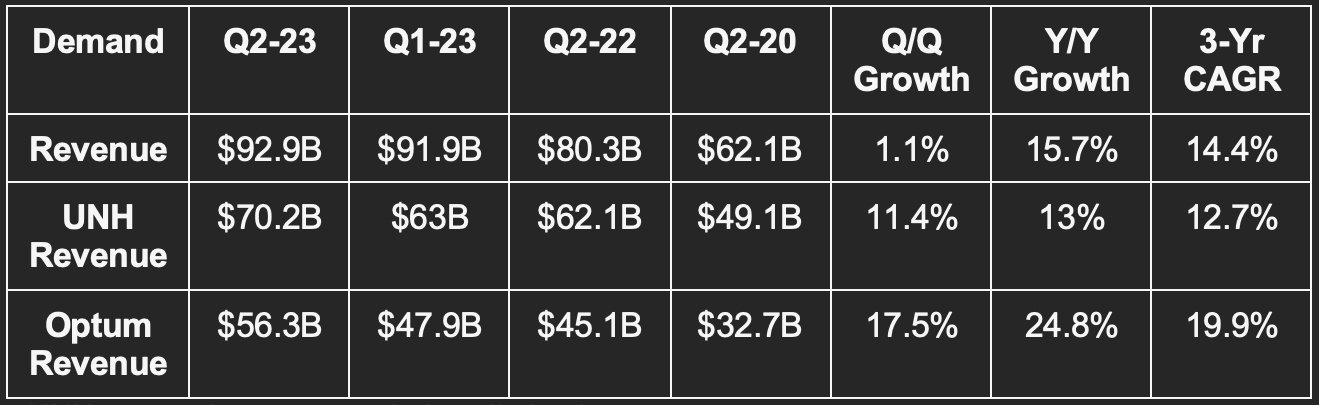

b) UnitedHealth Group (UNH)

Results vs. Expectations:

Beat revenue estimates by 2.1%.

Missed GAAP EBIT estimates by 0.4%.

Missed GAAP EPS estimates of $5.95 by $0.13.

Missed EPS estimates by $6.26 by $0.12.

The profit miss seems to be related to quarterly timing rather than operational efficiency as the full year profit guide was slightly raised by the firm.

Forward Guidance:

Now sees $23.60 in 2023 GAAP EPS vs. $23.50 previously.

Now sees $24.85 in 2023 EPS vs. $24.75 previously.

Balance Sheet:

Year to date, it has paid out $3.28 billion in dividends which rose by 13% Y/Y.

Year to date, it has bought back $5 billion vs. $5 billion Y/Y.

$46.3 billion in cash & equivalents.

$59.3 billion in long term debt; $6.3 billion in current debt (due in next 12 months).

Report Highlights:

Results:

Medical care (or loss) ratio rose from 81.5% to 83.2% Y/Y. This measures what proportion of premiums is being spent on care. UNH ideally wants this to be lower. This was driven by a mix shift to things like elderly outpatient care.

UNH Segment Context:

Features like less government reimbursement and healthcare service inflation are hitting UNH segment margins on a 3-year basis.

Year to date, it has added 1.1 million new customers to its medical benefits programs. This is nearly double the total additions it had at this time year to date in 2022.

Optum Health Segment:

Revenue per consumer rose 33% Y/Y as services offered grew.

Optum Insight’s revenue backlog rose from $23 billion to $31 billion Y/Y.

OptumRx revenue rose 15% Y/Y with adjusted scripts of 381 million vs. 357 million Y/Y.

c) Pepsi (PEP)

Pepsi is a key player in the consumer packaged goods (CPG) space. Its performance can be taken as a decent hint of pricing power within quality brands as inflation cools but remains elevated. Its largely upbeat results were credited to resilient consumer demand for its affordable goods. It is shifting some focus to “productivity initiatives” to fatten up margins and provide more liquidity to fuel growth.

Results vs. Expectations:

Revenue of $22.3 billion beat estimates by 2.8%. The revenue generation represents 10.4% Y/Y growth.

Gross margin dollars of $12.2 billion beat estimates by 5%. Gross margin of 54.7% beat estimates by 110 basis points (bps).

EBIT was roughly in line with estimates.

GAAP EPS either beat estimates by a penny or exactly met estimates depending on which data source you use.

Guidance:

Raised its annual organic revenue growth guide from 8% Y/Y to 10% Y/Y. This was VERY strong with consensus estimates looking for about 5% Y/Y growth.

It raised its EPS growth guide from 7% Y/Y to 10% Y/Y. This actually slightly missed EPS estimates calling for 11% Y/Y growth.

It continues to expect to return $7.7 billion to shareholders this year or 3% of its current market cap.

Balance Sheet:

$6.1 billion in cash & equivalents vs. $4.95 billion 6 months ago.

Inventories rose 14% vs. 6 months ago.

$36 billion in long term debt and $7.6 billion in current debt.

Share count shrank by less than 1% vs. 6 months ago.

8. Amazon (AMZN) -- Prime Day

Prime Day appears to have gone quite well. Per Adobe analytics and Numerator, volumes rose by 6% and 8% respectively on the first day. This growth compares to expectations of relatively flat Y/Y demand and put it on pace to surpass Bank of America’s $12 billion volume estimate by about 7%. We have not seen data from either firm or Amazon on the second day’s performance, but day one was a great start. Specifically, Amazon called day one the single largest sales volume day in its history with 375 million units sold.

A few pieces of needed context here. In terms of margins on these sales, Amazon reportedly deepened its discounts this year to cater to consumers struggling with inflation. While that could result in lower profits for the event, 3rd party sellers were also called out as a notable winner over the 48 hour window. 3rd party sales feature better margins than 1st party for Amazon. One margin headwind and one tailwind.

9. Upstart (UPST) -- Partner

Upstart announced a new partner this week in Arbor Credit Union. With $600 million in total assets under management at the financial institution, this will not be all that material to its funding supply. What is material is the $4 billion in committed funding Upstart secured earlier in the year. That will allow it to more flexibly fulfill strong demand without as glaring of a funding gap affecting originations. The committed capital was a great step in the right direction for Upstart, but we’d love to see actual deal terms and take rates associated with that fresh funding to turn more bullish. We’ll likely have to wait and see how those terms play out in the future margin profile.

Demand has been robust throughout the cycle, supply has been the issue. Partners are still extremely timid with funding appetite while capital market demand is still essentially gone. We do expect sub-prime partner funding to return as macro improves and as vintages for those partners outperformed across the nasty credit cycle. When that happens is a guessing game, but by the end of this year or early next year seems somewhat likely. Its performance amid turmoil should have built significant trust with origination partners. Conversely, some vintages for UPST capital market investors during 2022 did not meet expectations and it’s less clear when or if that supply channel will brighten.

For now, the committed capital is crucial to Upstart’s return to profitability and sequential revenue growth. Arbor Credit Union will not be the source of those positive inflections. My small position remains on the do not add list though the position continues to grow as the stock rises.

11. Final Market Headlines

The Trade Desk will be added to Nasdaq Indices next week.

Needham channel checks points to relative demand outperformance for Airbnb and Expedia.

India lowered its age of consent for data sharing which should be a small tailwind for tech giants as they try to gain traction in that demographically compelling country.

12. Macro Data from the Week

Consumer Price Index (CPI) data was encouraging:

CPI Y/Y rose 3% in June vs. 3.1% expected and 4% last month.

CPI M/M rose 0.2% in June vs. 0.3% expected and 0.1% last month.

Core CPI Y/Y (strips out food and energy) rose 4.8% Y/Y vs. 5% expected and 5.3% last month.

Core CPI M/M rose 0.2% vs. 0.3% expected and 0.4% last month.

Producer Price Index (PPI) data was encouraging:

PPI M/M in June rose 0.1% vs. 0.2% expected and -0.4% last month.

Core PPI M/M in June rose 0.1% vs. 0.2% expected and 0.1% last month.

More inflation data:

Export Price Index M/M in June fell -0.9% vs. -0.2% expected and -1.9% last month.

Import Price Index M/M in June fell -0.2% vs. -0.1% expected and -0.4% last month.

Michigan 5-year inflation expectations for July are steady at 3.1%.

More data:

Michigan Consumer Expectations for July came in at 69.4 vs. 61.8 expected and 61.5 last month.

Michigan Consumer Sentiment for July came in at 72.6 vs. 65.5 expected and 64.4 last month.

Initial jobless claims were 237,000 vs. 250,000 expected and 249,000 last report.

Inflation continues to cool faster than output or employment data deteriorate. This is a good sign for realizing the somewhat rare soft landing. At this point, a soft landing or a mild recession seem to be the only two probable options. Both should mean the end of rate hikes (recession making that happen more quickly) with that serving as a favorable risk asset setup alongside a still robust economy. Markets seem to be sniffing this out with speculative stock land racing higher.

13. My Portfolio

I moved 25% of my Shopify equity into Amazon and trimmed about 6% of my stake in The Trade Desk this week. Both moves were the result of stretched valuations.

In relation to Uber x Domino‘s: Domino’s has been on the Lieferando app for years. So, it’s not as uncommon for them to join such platforms and not an exclusive one.

Thanks for the weekly as always,