News of the Week (November 20 - 24)

News of the Week (November 20 - 24)

Nvidia; Amazon; CrowdStrike; Uber; SoFi; Autodesk; Market Headlines; Macro; My Portfolio

Today’s Article is Powered by my Favorite Brians Over at Long Term Mindset:

1. Nvidia (NVDA) – Earnings Review

a. Demand

Beat revenue estimates by 12.3% and beat its guidance by 13.1%.

The firm’s 56.4% 3-year compounded annual growth rate (CAGR) compares to 51.7% as of last quarter and 32.7% as of 2 quarters ago.

Data Center is the revenue bucket that Gen AI’s proliferation supports.

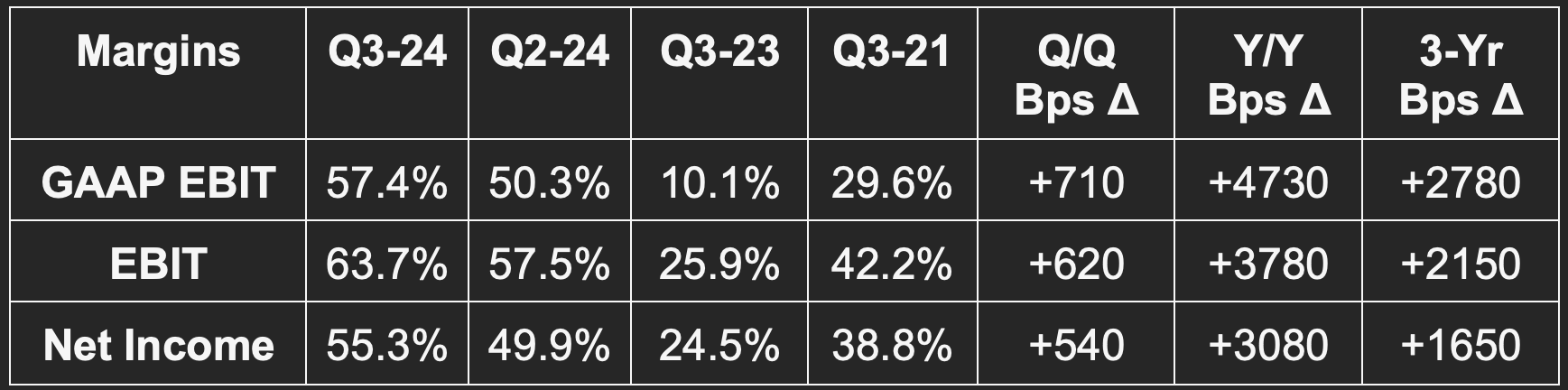

b. Profitability

Beat EBIT estimates by 18.7% & beat guidance by 20.4%.

Beat GAAP EBIT guidance by 22.7%.

Beat $3.40 earnings per share (EPS) estimates by $0.61 & beat guidance by $0.70.

Beat 71.5% GAAP gross profit margin (GPM) guide by 250 basis points (bps; 1 bps = 0.01%).

Beat 72.5% GPM guide by 250 bps.

c. Fiscal Q4 2024 Guidance

Beat revenue estimate by 12.4%.

Beat non-GAAP EBIT estimate by 19.4%.

Beat non-GAAP net income estimate by 19.3%.

Beat 74.7% non-GAAP GPM estimate by 80 bps.

d. Balance Sheet

$18.3 billion in cash & equivalents. Strong cash collections led to a decline in accounts receivable.

$9.7 billion in debt with $1.25 billion being current (due in the next 12 months).

$4.78 billion in inventory with purchase commitments for $17.1 billion.

$6.87 billion in year-to-date buybacks vs. $8.83 billion Y/Y.

Share count fell slightly Y/Y. It’s still hiring aggressively to meet demand and that means more stock comp. Considering these results, that’s something I think shareholders (which I am not) should be entirely fine with.

e. Call & Release Highlights

Important Definitions & Acronyms:

GPU: Graphics Processing Unit. This is an electronic circuit to display screen images.

CPU: Central Processing Unit. This is a different type of electronic circuit that carries out tasks/assignments and data processing from applications.

DGX: Nvidia’s full stack platform combining its chipsets and software services.

Hopper: Nvidia’s new GPU architecture designed for accelerated compute and Generative AI use cases. Key piece of the DGX platform.

H100: Its Hopper 100 Chip.

L40S: Another, more barebones GPU chipset based on Ada Lovelace architecture. This works best for less complex needs.

Ampere: The GPU architecture that Hopper replaces for a 16x performance boost.

Grace: Nvidia’s new CPU architecture designed for accelerated compute and Generative AI use cases. Key piece of the DGX platform.

GH200: Its Grace Hopper 200 Superchip with Nvidia GPUs and ARM Holdings CPUs.

InfiniBand: Interconnect tech providing an ultra-low latency computing network.

NeMo: Guided step-functions to build granular Gen AI models for client-specific needs.

Generative AI Model Training: One of two key layers to model development. This seasons a model by feeding it specific data.

Generative AI Model Inference: The second key layer to model development. This pushes trained models to create new insights and uncover new, related patterns. It connects data dots that we didn’t realize were related. Training comes first. Inference comes second.

Data Center Going Gangbusters:

The Data Center explosion is being supported by H100 architecture and the coinciding Gen AI boom. Data center computing demand rose by a whopping 324% Y/Y powered by broad DGX growth. Demand was evenly split between cloud service providers (CSPs) and large consumer internet players like Meta.

H100 efficiently scales better than all competitors; this is key given the voracious data consumption of models and Gen AI apps. That claim is according to independent research benchmarks from MLPerf, not internal findings. Per leadership, the H100 “remains the top performing, most cost-effective and most versatile platform for AI training – by a wide margin.”

Newer Data Center Chips:

Nvidia is releasing the next iteration of its H100 chips (shockingly called H200) which doubles model inference performance – thus cutting costs in half (or doubling the value of each chip).

Tensor Runtime (TensorRT) is Nvidia’s software database with models and tools to optimize performance. It just released a new Large Language Model (LLM) which doubled inference performance (so cut cost in half). NVDA just continues to constantly iterate to drive better efficiency and that will not change.

Initial shipments of Nvidia’s GH200 chip are now underway. While H100 is perfect for most model training and inference, the GH200 allows this to be done on a larger scale for those with the heftiest needs. It also creates more real-time data visualization and analytics on a larger scale vs. H100. Both are rapidly ramping into multi-billion dollar product lines at unprecedented paces.

“We will also have a broader and faster product launch cadence to meet a growing and diverse set of AI opportunities.” – CFO Colette Kress

Data Center Networking Revenue:

Nvidia’s networking bucket is all revenue generated from technology allowing “products to communicate with one another.” It just crossed a $10 billion annual revenue run rate because its products are required for “gaining the performance needed to train models.” Azure uses 29,000 miles of NVDA InfiniBand connectivity cabling and virtually all other cloud service providers lean heavily on it as well. Networking revenue rose 155% Y/Y via strong InfiniBand infrastructure “to support data center demand.” Going forward, Nvidia plans to expand into Ethernet networking. It will release a new product (called Spectrum-X) next quarter with initial support from Dell, Hewlett-Packard and Lenovo. Spectrum-X delivers 60% better networking performance for AI communication vs. alternatives. This means lower cost. Better performance and lower cost is a consistent Nvidia product theme.

As an important aside, virtually every large cap tech consumer internet or cloud company uses Nvidia chips. Amazon, Microsoft, Google, Meta, Adobe, OpenAI, ServiceNow, Databricks, Snowflake. The list goes on, and on, and on. It powers ChatGPT, Microsoft CoPilot, Firefly, Now Assist, Meta AI etc. The company’s products are ubiquitous and virtually synonymous with AI.

Public Market Opportunity & Supercomputers:

Working in tandem with India’s government and tech giants there (Reliance, Tata, etc.) to “boost their sovereign AI infrastructure.”

The U.K. government will use 24,000 GH200 superchips to build a new supercomputer.

Initial chip shipments to The Swiss National Supercomputing Center started this quarter.

“National investment in computer capacity is a new economic imperative. Serving the sovereign AI infrastructure market represents a multibillion-dollar opportunity over the next few years.” – CFO Colette Kress

H100 Supply:

Supply bottlenecks remain in place. This is sort of ridiculous to think about given the insane growth this company continues to post. Imagine what it would look like if it could fulfill all orders today. Supply constraints are easing but will take a few more quarters to fully disappear (assuming demand doesn’t ramp beyond expectations).

China Export Restrictions:

The U.S. government will implement new export restrictions for chipsets that clear certain performance benchmarks. The countries involved include China, Saudi Arabia and a few others.

The new rules impact chipsets within its Ampere, Hopper (H100), Grace (GH200) and Ada LoveLace (L40S) architectures. Companies will be required to secure licensing before shipping these types of chips. The new rules are now in place and will start impacting Nvidia this quarter.

Over the last few quarters, China has represented 20%-25% of all data center revenue for Nvidia. It expects revenue from that nation to sharply drop going forward due to these rules. Fortunately, it believes that demand elsewhere will more than offset this blow. Remember, H100 remains materially supply constrained.

NVIDIA is working to procure the needed licensing to resume shipments but does not know when that will occur. Alternatively, it is working to ensure it has more supply of lower performance chips for these nations going forward. Notably, the rollout of one regulatory-compliant chipset for China has been delayed.

Gaming, Auto & Professional Visualization:

Growth for Gaming and Professional Visualization was helped by normalization of channel inventory gluts earlier in the year.

Gross Margins:

Gross margin was bolstered by a mix shift to data center revenue, outperforming revenue and lower inventory provisions Y/Y. Those provisions were from Ampere, not Grace or Hopper. Notably, provisions in last year’s quarter hit GPM by 1150 bps vs. just 240 bps this quarter. That was a material source of gross margin expansion. It wasn’t the only source as GPM expanded by 2040 bps Y/Y and this provisions comp tailwind only propped up GPM by 910 bps.

The explosion in revenue coincided with 16% Y/Y GAAP operating expense (OpEx) growth and 13% Y/Y OpEx growth. Crazy leverage.

Quick Notes on Software:

Nvidia’s software and services revenue bucket will soon cross $1 billion in annual revenue. This includes DGX cloud services and its AI enterprise software tools. Genentech was announced as a new customer. It will use Nvidia’s BioNeMo LLM framework to accelerate drug discovery. NeMo is its standardized framework for building LLMs with BioNeMo being more specific to biotech use cases.

Nvidia’s deepening Azure partnership will now allow custom Gen AI apps built through Nvidia to be seamlessly run on Azure. Customers will be able to access any needed Azure data to build models most specific to their needs.

f. My Take

This is one of the best large cap quarters I’ve ever covered. Nvidia’s last quarter was the second best with its performance 2 quarters ago being the third best. Incredible performance and incredible execution paired with a best-in-class value prop are paving the way for some historic results. I’m not a shareholder, just an admirer.

For the sake of balance, I’d like to provide the two biggest risks to the bull case that I see. Clearly, those risks aren’t impacting the company in the slightest today, but they’re still worth noting.

The first is cyclicality. We’ve had supercycles before. Supercycles have led to crazy spikes in demand growth for semiconductor firms. Never this crazy, but crazy. The risk here is that supply dynamics normalize, competition begins to catch up (long way to go) and that growth reverts back to the ~only~ roughly 25%-30% multi-year CAGR we’ve previously seen. 30x earnings (where Nvidia trades) is actually very cheap when you’re growing those earnings 50% annually. It’s less cheap if leverage slows and growth dips back to multi-year trends. That will certainly happen eventually. The risk is that it happens sooner than some expect. I have no opinion here as I don’t know enough about the industry to have an opinion. But it’s a risk.

Secondly is China. It’s easy to replace 25% of data center demand when supply constraints remain in place and demand is racing. It’s harder to plug that gap in more normal times like the scenario that I’m describing above.

What isn’t a pressing risk here? The claims of fraud that some seem to love to make on social media. I call these people conspiracy theorists… and the conspiracy is not compelling in this case. All in all, this has been a perfect year for Nvidia. Take a bow Jensen… then take another bow. You called out this super-cycle years before the rest.

Long-Term Mindset is a FREE weekly newsletter emailed each Wednesday. Each issue contains five pieces of timeless content to encourage you to think long-term. All issues can be read in less than 1 minute. There’s a reason why we are consistent readers and think you should be too. Subscribe here.

2. Amazon (AMZN) – AI & Black Friday

Amazon debuted free-to-use AI courses to train talent. The material will include eight courses as well as certifications. It will be offered to existing and prospective employees, as well as some students.

The Amazon distribution center in Swindon (England) is as “busy as ever” as it continues to see “more and more demand” per its manager Davad Tindal. He’s seeing no weakness which is especially (and pleasantly) surprising given that economic activity in EMEA has lagged North America a bit. Sporadic strikes across some fulfillment centers do not seem to be having any impact on this titan’s execution. Still, that is something to watch closely in case they become more broad-based in nature.

Amazon’s iRobot transaction looks like it will close at $1.4 billion without antitrust pushback from the EU.

3. CrowdStrike (CRWD) – AWS, Channel Checks & A Tougher Setup

a. AWS

It’s no secret that CrowdStrike and AWS work well together. Notably, CrowdStrike recently became the first independent software vendor within cybersecurity to cross $1 billion in AWS marketplace sales. Per Synergy Research Group, among the Big 3 public cloud vendors, AWS leads with small businesses. It has the largest market share of small and medium businesses (SMBs) at 31%, followed by Azure at 26% and Google at 19%.

b. Channel Checks & A Tougher Setup

All of this is to say that Amazon is the perfect channel partner for firms looking to expand their client bases downstream to smaller logos. That is a key growth vector for CrowdStrike, and one that should continue to bear significant fruit. Outperforming cost & efficacy for massive clients like Walmart, Accenture and Bank of America has a way of serving as key proof of concept for the little guys. CrowdStrike delivers that proof of concept in droves. Now CrowdStrike has combined these edges into the Falcon Go Bundle to cater directly to smaller players. Partnerships and product tiers like these should keep making that pursuit highly successful.

Promising Q3 channel checks from Morgan Stanley point to better-than-expected demand for CrowdStrike. The firm raised its price target based on this research. CrowdStrike’s stock has been soaring in recent months. It’s hard to imagine that it was in the $80s just a couple of quarters ago. Heading into earnings, I’m very optimistic about the actual numbers. I’m less optimistic about what the stock does in response to those strong numbers. It’s not nearly as expensive as a firm like The Trade Desk, but its roughly 40x free cash flow multiple still commands outperformance.

There are few companies that I’m more confident in outperforming than this one. Still, don’t be surprised if the stock shrugs off stellar numbers or responds poorly if there’s any negative surprise. I have no interest in selling shares despite having this view. I’ve owned CrowdStrike since the IPO; this share taking giant is one I want to own for many more years barring worsening execution. So? Either I’m wrong and the stock keeps moving higher, or it cools off a bit and I potentially get the chance to add more. We’ll see.

4. Uber Technologies (UBER) – Notes Offering

Uber announced a $1.2 billion convertible senior note offering. The notes carry a 0.875% interest rate and are due (mature) in 2028. Uber will use the proceeds to pay down existing debt including about $1 billion in 7.5% convertible senior notes due in 2025. This transaction offers more evidence of Uber’s strengthening liquidity, cash flows and coinciding credit ratings (which are now investment grade). More evidence came when the $1.2 billion deal was upsized to $1.5 billion – likely due to stronger demand or more favorable credit market conditions than anticipated.

This is the luxury of running a viable business, rather than one that chases growth at all costs. Now, the chase for growth will continue to become cheaper and more profitable thanks to the stronger footing Uber finds itself on. Nobody in the space can match its cost of capital strength, and that’s an edge it will fully leverage.

I’m expecting buybacks to start some time in the next quarter or two. Leadership has hinted at it a few times. Uber is set to generate $5+ billion in expected 2024 free cash. It also has $5.2 billion in cash and another $5.1 billion in investments that it will likely be partially liquidated. That leaves it well funded to continue expanding the product suite, keep investment and keep sharpening its customer acquisition cost lead – all while returning material cash to shareholders.

5. SoFi (SOFI) – Insider Buying

Anthony Noto made another small open market purchase of SoFi shares. I’ve spoken at length over the last few weeks on SoFi investment case risks and why I think those risks are being stretched and amplified based on price action rather than fundamental validity. I truly think recent price action all comes down to a skeptical Wall Street.

SoFi is a bank that uses accounting methods that most banks don’t use. These accounting methods are more transparent and more accurate in terms of diminished unrealized loss risk. Still, when you’re a bank and you do things differently… folks will ALWAYS assume you’re being shady. I expect 2024 to feature a tech segment re-acceleration, continued credit metric outperformance, easy access to capital markets and ramping GAAP profits. So? I expect 2024 to look like SoFi leadership thinks it will. I’m actually a tad more optimistic given the prudent guidance approach the team has used since going public.

As it proves itself year after year, skeptics will slowly turn into believers. I am optimistic that GAAP net income will be a key ingredient in turbocharging that process. The real bear case hangs on an unfounded belief that SoFi’s leadership team is not being truthful when they explain why its credit book and flexibility are in such good shape. Anthony Noto and Chris LaPointe have done absolutely nothing but build my trust since going public. They’ve exceeded financial targets year after year DESPITE long term projections being made BEFORE losing its largest student loan segment for 3 years. They’ve earned my confidence. Whether they’ve earned yours is, as always, entirely up to you. There are no certainties in stock market-land. Only risk/reward to be optimized.

6. Autodesk (ADSK) – Earnings Snapshot

a. Demand

Beat revenue estimate by 1.9% & beat similar guidance by 1.9%.

Please note that Autodesk is shifting from multi-year contracts to annual billings which is temporarily impacting growth for that metric.

b. Profitability

Beat $1.05 EPS estimates by $0.07.

Beat $2.00 non-GAAP EPS estimates by $0.08 and beat its guidance by $0.07.

c. Guidance

Autodesk roughly met Q4 revenue estimates. It missed $1.07 GAAP EPS estimates by $0.05 at the midpoint. It also missed $2.00 non-GAAP EPS estimates by $0.0.6.

For the full year, it raised its revenue growth guide from 8.5% to 9%. It reiterated flat GAAP & non-GAAP EBIT margins for the year. It raised its free cash flow guidance by 1.7%. Finally, it slightly raised GAAP & non-GAAP EPS estimates thanks to Q3’s outperformance.

d. Balance Sheet

$1.98 billion in cash & equivalents.

$220 million in long-term marketable securities.

Share count fell slightly Y/Y via $730 million in year-to-date buybacks vs. $897 million Y/Y.

7. Market Headlines:

Adobe (ADBE):

Adobe is a key source of aggregated consumer spending data for Black Friday-Cyber Monday. Its predicted $5.6 billion in 2023 Thanksgiving spending came precisely to fruition. This represents 5.5% Y/Y growth and points to enduring consumer resilience. For the holiday weekend overall, the firm is looking for 5.4% Y/Y growth with video games and Barbie products set to be two category standouts.

Palantir (PLTR):

The long anticipated $525 million National Health Service (NHS) contract in the UK for patient data management/analysis was awarded to Palantir.

OpenAI/Microsoft (MSFT):

If you missed it, the OpenAI saga was quite interesting this past week. Sam Altman was ousted as the CEO of the firm. Microsoft, despite its $10+ billion invested in the firm, does not have a board seat and so was caught off guard by the news. There are about a dozen different reasons to explain this firing depending on who you ask. Some say he was pushing new model cadence too aggressively, some say he was distracted from trying to fund another startup, others say different things entirely. Who knows. After the move, OpenAI’s board reportedly approached Anthropic about a merger. Anthropic’s CEO, Dario Amodei who came from OpenAI, would have led the combined firm. That didn’t pan out.

An arms race for OpenAI engineers then commenced. Microsoft offered Sam the opportunity to lead Microsoft AI; heavyweights like Salesforce CEO Marc Benioff offered to match compensation packages for any employee wanting to work there.

A letter was then sent from the majority of OpenAI’s employees to the board telling them to reinstate Sam, or they’d leave. That magically did the trick with Sam returning to lead the company. OpenAI is arguably the most valuable generative AI firm in private markets and this played out like a script in a tentpole.

8. Macro

Consumer and Employment Data:

Michigan Consumer Expectations for November came in at 56.8 vs. 56.9 expected and 56.9 last month.

Michigan Consumer Sentiment for November came in at 61.3 vs. 60.4 expected and 63.8 last month.

Output Data:

3.79 million existing home sales for October vs. 3.9 million expected and 3.95 million last month.

0% core durable goods orders M/M growth for October vs. 0.1% expected and 0.2% last month.

-5.4% durable goods orders M/M growth for October vs. -3.1% expected and 4.0% last month.

Inflation Data:

Michigan 1-year Inflation Expectations for November came in at 4.5% vs. 4.4% expected and 4.4% last month. 5-year inflation expectations remain at 3.2% as expected.

9. My Portfolio

I sold 10% of my Shopify stake during the week. I love the company's team, opportunity & path. The stock is just just very expensive. The price continues to fall right back into reasonable multiple territory... then rapidly rally 30%-40% thereafter to less reasonable territory where it is right now. This is what I do. Actively manage pieces of positions while keeping most of those positions intact as long as the fundamental investment case is solid. It’s entirely solid here in my view. Shopify's volatility & valuation continue to give me these opportunities more frequently than I usually get them. I'm taking advantage.