Nvidia & Snowflake Earnings Reviews

Nvidia & Snowflake Earnings Reviews

Digesting the results of these two important technology companies.

1. Nvidia (NVDA) – Earnings Review

a) Results vs. Expectations

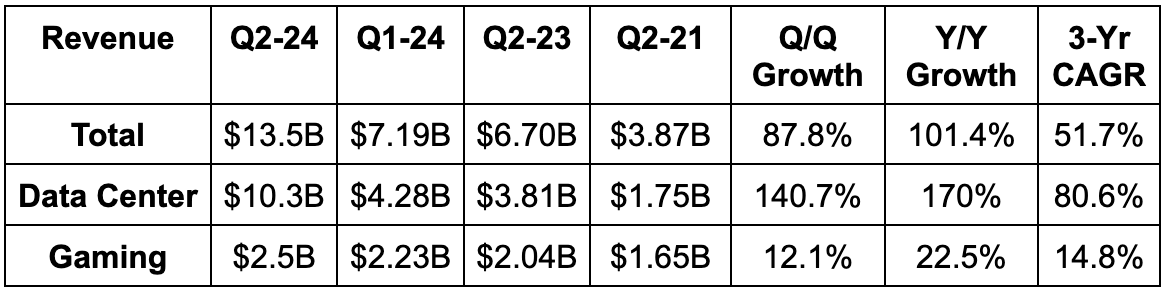

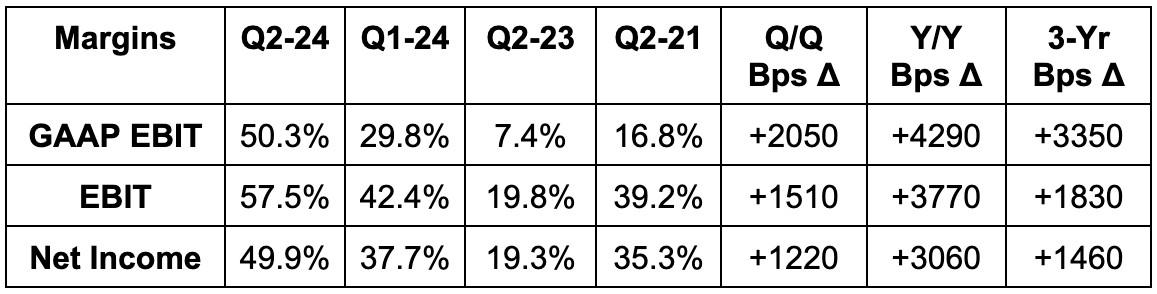

Beat revenue estimates by 22% & beat guidance by 22.7%.

Beat EBIT estimates by 31% & beat guidance by 34.1%.

Beat EPS estimates by $0.39 & beat guidance by $0.44.

b) Next Quarter Guidance

Beat revenue estimates by 29%.

Beat EBIT estimates by 39.7%.

It has “strong demand visibility” well into calendar 2024.

c) Balance Sheet

$5.8 billion in cash & equivalents.

$9.7 billion in total debt with $1.2 billion current (due within 12 months).

Share count fell 1% Y/Y as it bought back $3.1 billion in stock vs. $3.3 billion Y/Y.

Announced a new $25 billion buyback program to bring its total current buyback capacity to $29 billion.

Dividends are flat Y/Y.

d) Call & Release Highlights

The Generative AI Wave:

The transformation of general compute usage within data centers to accelerated compute and AI is in full swing; Nvidia is best positioned to capitalize. This newer approach effectively frees up a large chunk of central processing unit (CPU) needs to make these CPUs more efficient and slightly less needed. That means cost savings. Furthermore, Cloud service providers, large internet players and enterprises from all industries are racing to rip and replace their old infrastructure with Nvidia’s Hopper 100 (H100) graphics processing units (GPUs). This is thanks to the vast cost and efficiency edges it brings to the table. These edges allow Amazon to cut costs while enhancing service quality and diminishing carbon footprint and allow Meta’s Reels algorithm to power more than 20% growth in engagement.

Nvidia’s lead in efficiently training models and use cases is simply unmatched… and nobody comes close. Its inference technology is also considered in the lead, but the gap is less drastic vs. competition. Training allows models to more precisely query and provide information via better algorithm seasoning. Inference allows these trained models to predict and generate new information based on learning from old patterns. Training happens at the beginning… then inference takes over. Both are vital to effectively extract value from AI apps and large language models (LLMs).

Along the same AI theme, its networking revenue also doubled Y/Y thanks to its own “InfiniBand” platform for high performance computing. This product doubles performance vs. legacy ethernet alternatives with that edge being worth “hundreds of millions” to its large clients. If you’re noticing a theme of Nvidia delivering both cost and performance edges, you’re right. The platform is the “only infrastructure within networking that can scale to hundreds of thousands of GPUs making it the “network of choice” in AI.

Supply:

Nvidia’s H100 chips are supply constrained. It praised its partners for “exceptional capacity ramps” but it’s still not able to meet 100% of its demand. Incredible to think about considering how mammoth of a quarter this still was. The company sees supply constraints easing throughout the year and into 2024 to allow it to better meet customer needs. Cycle times are shrinking and capacity partners are being added.

New Products:

Its new “enterprise ready servers” with its L40S GPU chip is expected to ease some of the supply scarcity for its accelerated computing demand.

Its next generation Grace Hopper 200 (GH200) Super Chip is in full production. This is 90% Nvidia GPUs and 10% ARM CPUs. The next generation of this next-gen chip is set to be available next spring. It’s always iterating.

Its DGX (the name of its full stack platform) GH200 supercomputer for AI models will be available in the next 5 months. This allows for the connection of 256 GH200 chips to be operated as a singular unit vs. previously only being able to connect 8 at a time. This drives cost and performance efficiencies.

China:

The team does not see export restrictions on its data center GPUs to China as immediately impacting results. This is thanks to the sheer magnitude of current global demand. Still, if further restrictions are actually implemented, that would shrink the opportunity to a certain extent and place a lower ceiling on where generative AI and accelerated computing can take Nvidia.

Partnerships:

Snowflake partnership will allow shared customers to create models and applications from within Snowflake’s environment. Nvidia’s NeMo platform (its software product to help build these models) will now be available from directly within Snowflake.

Now working with ServiceNow and Accenture on the “AI Lighthouse Program.” This will expedite AI app creation while using Accenture's deep selling channels to enhance go to market.

New Hugging Face collaboration to simplify model creation.

New VMware partnership that will “fully integrate” Nvidia’s technology into the newly formed “VMware Private AI Foundation with Nvidia” for VMware clients.

Gaming:

Nvidia thinks gaming growth for the industry as a whole has returned to positive territory.

It’s now working on its “Avatar Cloud Engine” (ACE) to infuse its gen-AI talents within gaming chip use cases.

e) Takeaway

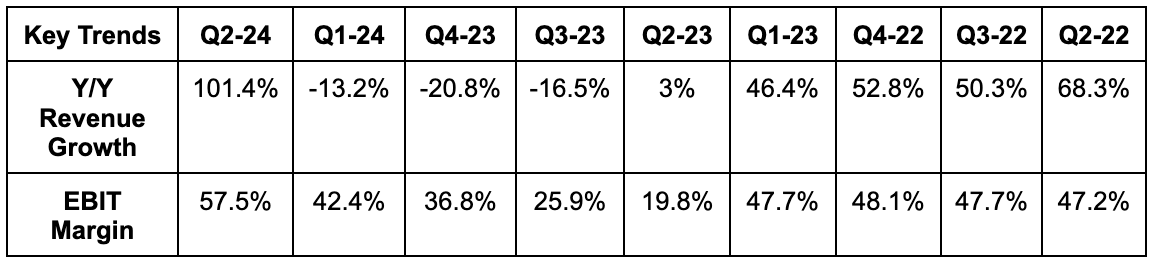

As an innocent bystander and someone who places this sector well outside of my circle of competence, all I can do is admire these numbers. This was the second best large cap quarter I’ve seen during this cycle with the best being Nvidia’s results 3 months ago. This company owns 90% market share of the AI chip sector which is set to explode in growth for the foreseeable future. Ideal. Experts will tell you that nobody comes close to the efficacy and value that Nvidia provides and these incredible numbers serve as evidence for that being the case. It’s very expensive… but how could it not be as it sets a multi-quarter trend of obliterating estimates by wild deltas. Elite quarter.

2. Snowflake (SNOW) – Earnings Review

Like Nvidia, this is not a personal holding. It’s just a company operating within the same themes that make up a large chunk of my portfolio… and I know many of you do own shares. It’s also simply a fascinating name to cover within data and AI as one of 2 companies in the world with its scale, growth, and free cash flow (FCF) margins. CrowdStrike is the other.

As a reminder, Snow is NOT a software as a service business… but a consumption based business. Flexing up or down data consumption is much easier to do in real-time vs. exiting multi-year contracts. For this reason, Snowflake is a wonderful gauge of how eager enterprises are to lean back into software spend growth.

a) Results vs. Expectations

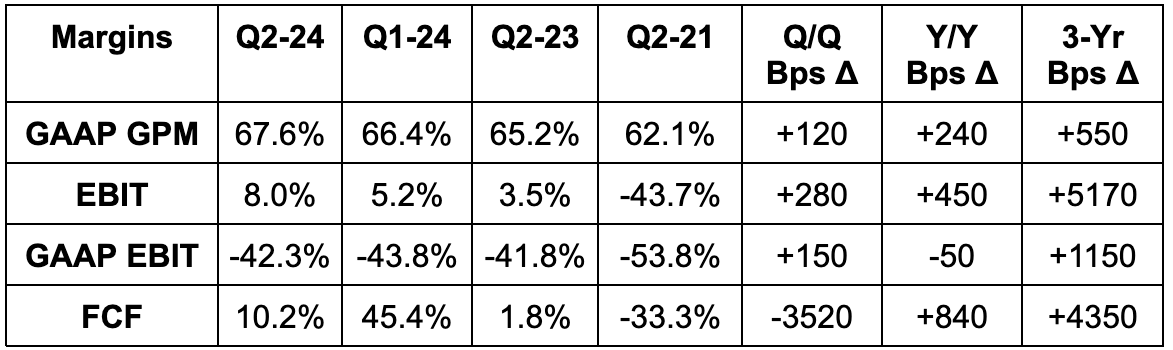

Beat revenue estimates by 1.8%. This represents a 3-year annually compounded growth rate of 71.7% vs. 79% Q/Q.

Annual recurring revenue (ARR) rose 69% Y/Y to reach $2.07 billion so far in 2023.

Beat product revenue estimates by 2.8%.

Beat EBIT estimates by 224% & beat EBIT margin guidance by 600 bps.

Beat $0.10 EPS estimate by $0.15.

Beat FCF estimates by 20%.

b) Annual Guidance

Snowflake reiterated its full year product revenue and margin guidance. This reiteration was also roughly in line with estimates. It does not guide to total revenue.

c) Balance Sheet

$3.7 billion in cash & equivalents with another $1.1 billion in long term investments.

No debt.

Share count rose 2.8% Y/Y as stock comp remains elevated. Share growth is a better gauge of dilution intensity vs. “stock comp as a % of some metric.”

Headcount rose 33% Y/Y.

No buybacks this quarter.

d) Call & Release Highlights

Macro:

The team spoke on stabilizing macro headwinds with weekly growth resuming in May and an “incremental improvement in sentiment and engagement.” It has not yet enjoyed a recovery in consumption and growth patterns… but things are no longer getting worse. As an important hint of future demand, bookings growth showed “promising signs with new bookings outperforming expectations.”

Data Salt to AI’s Pepper:

“Enterprises and institutions are all increasingly aware that they cannot have an AI strategy without a data strategy.” – CEO Frank Slootman

AI models must be seasoned to be worth anything and to create any kind of compelling app or use case. How are models seasoned? With Data. Who allows customers to conjoin their disjointed (multi-cloud) data sources under one roof, in one environment and with a plethora of actionable analytics tools? Snowflake does. For this reason, the team sees itself as having a “head start” in the generative AI race as model and app builders will inherently build through Snowflake data queries. As a sign of how tightly these two ingredients are connected, look no further than the new Nvidia partnership. Together, Nvidia’s software model building toolkit (NeMo) will be available for use directly in Snowflake’s environment… right where a customer’s organized data sources preside. Snowflake Container Services will be leaned on to ensure it can onboard products like this one safely with proper permissions and configurations.

“You heard in my conversation with Jensen [Huang], Snowflake is sitting on a gold mine of data. Together, we can help customers turn that gold mine into intelligence.” – CEO Frank Slootman

Data Network Effect:

26% of Snowflake customers are sharing data with the full customer base vs. 20% Y/Y. More data sharing means incremental insight to uplift the value a customer receives with Snowflake vs. what it can enjoy alone. As more customers share their data openly, this unique edge merely grows. A network effect is forming.

Demand:

Customers spending $1 million or more on the Snowflake platform continued to rapidly grow by 22% fiscal year to date. Along those same lines, its Forbes Global 2000 customer footprint rose by 17% Y/Y to reach 639. Both items helped its net revenue retention (NRR) rate reach 142% vs. 151% Q/Q and 172% Y/Y. 142% is still phenomenal and the dip goes back to that idea of data consumption being easier to tweak than longer turn subscriptions. A client of Snowflake’s can choose to move from 5 year data storage to 3 year data storage on a whim… which hits NRR. The same cannot be said for a business model like The Trade Desk for example.

Snowpark:

Snowpark is a newer Snowflake tool which frees developers to write and build within Snowflake and in a wide range of source code languages. This merges Snowflake’s data storage, querying, organization and leveraging prowess with an actionable ability to utilize this insight to create applications all in 1 place. This cuts down data transference costs while fostering cohesive simplicity and productivity. It also means developers can tap into data cleansing and quality issues in real-time while they build. Snowpark consumption growth remained rapid at 70% Y/Y this quarter as it added 400 new customers Q/Q.

e) Takeaway

There’s nothing to be alarmed by in this report. It was in-line across the board. Slowing growth will likely revert as macro improves and consumption appetite normalizes. It’s one of the most expensive names in public markets which means expectations are always sky-high heading into its reports. Perhaps some wanted more here, but again, this quarter was fine.

Great recap!

Fantastic Brad.