Introduction:

Fertility treatment coverage in the USA is broken. Sky-high costs, little guidance and poor outcomes are just a few of the realities plaguing this portion of healthcare. Progyny (PGNY) is a fertility benefits company born to remedy this stubbornly undesirable situation.

The organization began its journey in 2008 as “Fertility Authority” when it was founded by Gina Bartasi. 7 years later, Fertility Authority merged with Auxogyn (a fertility technology company) to create Progyny. Following the complete integration of the two companies, Bartasi stepped down with David Schlanger — the current CEO — replacing her.

Today, the company serves as the fertility benefits manager for large enterprises across the United States and has found notable success in doing so. This article will offer a detailed overview of Progyny’s industry, operations and prospects including:

- The Issues with Fertility Treatment

- Progyny’s Solutions

- Quantifying Progyny’s Impact

- Progyny’s Pre-Tax Edge

- Progyny’s Reach and Market

- The Business Model and Sales Cycle

- What’s Next? (Optionality)

- Management and Ownership

- Financial Performance and Outlook

- Balance Sheet

- Risks

- The Competitive Landscape

- Valuation Table

- My Approach

I also interviewed a Progyny Vice President as part of my research. The conversation was fascinating and quotes and insight from the talk are incorporated throughout the piece.

1.The Issues with Fertility Treatment

a. Fertility Coverage Issues

Despite infertility impacting 1 out of 8 couples in the United States today, the American Medical Association did not recognize it as a disease until 4 years ago. As a result, infertility insurance is extremely sporadic throughout the USA. Just 19 states have infertility insurance laws requiring some form of coverage, with 5 states having specific legislation pertaining to in vitro fertilization (IVF).

When private insurers do provide some form of fertility coverage, it’s usually inadequate, outdated and incomplete. How so?

Health insurance carriers (also known as managed care providers) commonly use “limited lifetime dollar maximums” which place a ceiling on how much fertility treatment coverage an insured individual has. This approach designed to cut cost by limiting utilization is embraced — in some form — by 88% of managed care providers according to survey data recently published by Mercer. The philosophy innately places cost over safety and outcome on the list of carrier priorities.

Furthermore, the maximums philosophy also leads to insurers fundamentally handcuffing fertility specialists via mandating step-therapy protocols to try and limit cost. No two people are identical — and their fertility treatment plans shouldn’t be either. This objective often precludes specialists from using the best treatment methods and technologies.

The median coverage of these maximums is $16,250 — roughly 25% of the average cost of a complete round of fertility treatment according to the Journal of American Medical Association (JAMA). The effect is that fertility programs are often halted in the middle of a course of treatment. This means that the $16,250 in cost is wasted for employers while employees realize poor outcomes.

- Common mandated step-therapy protocol example: Insurers often require a member to undergo multiple cycles of intrauterine insemination (IUI). This comes with a 5-15% success rate and costs $4,000 each time (with a $16,250 average budget). There is rarely genetic testing done to determine if this is the correct course of action. IUIs also must be spaced out over several months and these protocols do not take into account a women’s biological clock. This resembles a guessing game and wastes precious time for many.

The pressure that maximums place on a mother needing to get pregnant on time and on budget inherently fosters poor choices. For example, IVF treatments are often selected without any preimplantation genetic testing conducted. The result of this is a sky-high miscarriage rate and therefore longer workplace absences, distressed employees, and a larger economic burden on the employer and insurer.

Another common problem stemming from dollar maximums is that patients often elect for multiple embryo transfers when undergoing an IVF treatment — thinking this boosts their odds of pregnancy. This has little impact on pregnancy odds and instead often leads to mothers who do get pregnant having twins, triplets and/or pre-term births. The increased odds of both multiple births and early births greatly raises the probability of health complications for the mother and the child and is a leading cause of neonatal intensive care unit (NICU) costs.

For context, according to the American Journal of Obstetrics and Gynecology, the mean cost of a single birth over the last 5 years was $36,000 compared to $153,000 for twins and $577,000 for triplets. Furthermore, pre-term births ALONE cost the United States $40 billion per year. Private employers often bear the bulk of these expenses in the form of higher employee coverage costs.

The reality of this situation is frustratingly ironic. The insurance carriers and employers fixated on minimizing cost rather than maximizing utility end up with higher costs incurred anyway. Higher costs & poor outcomes — not great. When instead focusing on happier, healthier mothers experiencing safer pregnancies, the costs naturally fall anyway.

b. Fertility Medication Issues

Adhering to fertility medication schedules is a dauntingly complex process. The mandated step-therapy protocol philosophy means a one-sized-fits-all approach to fertility vitamins and other prescriptions when each person’s needs are intrinsically unique. There’s also a several step authorization process because these medications are administered via specialty pharmacies and involve numerous parties in the fulfillment process.

This red tape delays the delivery of a vital scripts by 1-2 weeks on average. The timing of consuming a pill could make all the difference in the world for a woman getting pregnant — time consuming authorization jeopardizes that imperative schedule.

The medication issues only continue. There is little to no reliable literature on how to actually store or consume a given prescription. Some of these medications require very specific storage temperatures with others being injectable and thus somewhat difficult to administer. Despite these being two vital variables in the pregnancy equation, women are often left alone with adhering to medication schedules.

c. Fertility Specialist Issues

Yet another issue with this field is the lack of uniform access to high quality fertility specialists. A large portion of treatment seekers are left mainly on their own to research and grade doctors. Virtually none of us are experts in this field, yet the we are often required to know how to qualitatively analyze one potential specialist vs. another. Good luck.

Furthermore, insurance plans come with pre-set networks of healthcare practitioners; these networks don’t always include the most-preferred option of an individual patient — even if they have one. Finally, in the field of fertility especially, the specialists perceived to be the best are globally coveted by perspective mothers. Hefty demand for a select group of professionals makes appointment availability a logistical nightmare.

We also have to remember that fertility specialists and clinics are judged on their track record of outcomes. Because the fertility treatment status-quo offers a damaging headwind for those outcomes, the shortcomings of legacy coverage has a profoundly negative influence on a specialist’s business.

The culmination of all of these issues is a lose-lose-lose situation. Employers spend more on NICU costs due to poor treatment plans while suffering from discouraged and absent employees. Mothers find less success (and more danger) on their fertility and family planning journey. Fertility specialists aren’t able to maximize their success rates and therefore the reputation of their practice.

If this sounds like a frustrating reality, that’s because it is. The common practices in fertility treatment are simply not good enough. Thankfully, Progyny brought a disruptive solution to the market to turn that lose-lose-lose into a win-win-win.

2. Progyny’s Solutions

Progyny’s fix to the plethora of issues that the fertility industry faces is inherently business to business (b2b) in nature. It contracts with large enterprises and integrates its benefits into their existing employee coverage plans. These employees are referred to as “Covered Lives”.

Progyny’s benefits take the form of 2 core product offerings:

a. Fertility Benefits Solution

Progyny’s fertility benefits solution was launched 6 years ago as its first commercial product. The offering was developed from listening to a network of large enterprises consistently voice complaints about the shortcomings of existing fertility solutions. Progyny made it its mission to solve those pain points, and this product is the result.

How Patients win:

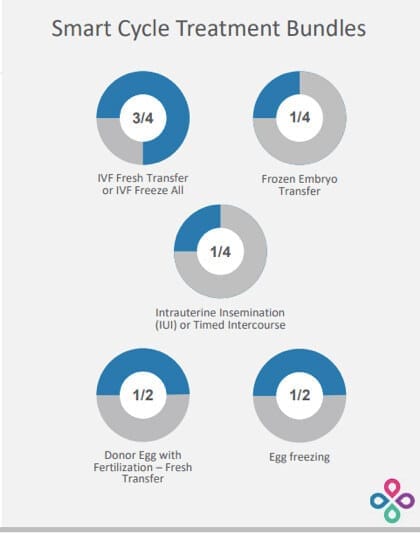

At the center of Progyny’s fertility benefits product is what it calls “Smart Cycles” — its take on assisted reproductive treatment (ART) cycles. Rather than mandating certain treatment practices be used, Progyny has created 19 different smart cycle bundles that can be mixed and matched to ensure the most customizable plans in the industry today. Progyny’s clients purchase 2-3 cycle units per employee on average.

These Smart Cycles include everything a perspective mother could possible want: diagnostic testing, access to the latest and greatest technologies, genetic testing for IVF and so much more. To ensure Progyny’s Smart Cycles are optimized for efficacy, the company’s advisory board — made up of world-renowned professionals in the industry — constantly reviews and upgrades the bundle options based on industry innovations.

No longer will a mother be required to go through IUIs or a blind IVF but instead will be able to select a personal plan from Progyny’s vast treatment options based on ideal timing and needs. Progyny does provide extensive educational resources to teach the patient and to steer them towards the best option. Ultimately however, it’s always up to that patient to decide which bundle to select.

Imperatively, there are also are no dollar maximums applied to these Smart Cycles. Instead, full unit values are assigned to complete treatment courses with a patient always covered for the entire unit’s cost. This means a person will not run out of funding in the middle of their treatment, but will instead be able to see it through to the end.

Below are some examples from Progyny’s most recent investor presentation of how its members can customize Smart Cycle units:

Progyny’s refreshing approach fosters superior outcomes as patient treatment paths are crafted for the best efficacy — not the remaining coverage availability. For evidence of this, Progyny’s treatment approach has all but eliminated the multiple birth scenario. It’s now clear that this former expectation stemmed from financial pressure forcing patients into less-than-ideal treatment plans. With Progyny, the treated multiple birth rate is roughly the same as it is with natural pregnancy.

- Multiple birth scenario/expectation: The previous assumption that fertility treatment heightens the odds of having multiple births.

Progyny collects all of the relevant data that its clinic network generates and the company then uses this data for its own constant improvement. A data driven approach vs. a guess and hope approach wins every time; according to CEO David Schlanger, no other competing program collects practice and outcome data in nearly as detailed a way as Progyny does. If its competitors are falling short (and they are), they likely don’t even know it.

Progyny does not expect consumers to be able to pick and adhere to the perfect fertility plan on their own. I already covered the educational resources it provides, but the company goes further in helping its patients. How? Progyny employs a team of Patient Care Advocates (PCAs) to provide administrative, strategic and emotional support every single step of the way. These PCAs communicate with each patient an average of 15 times per course of treatment which compares to 1 time per course of treatment for alternatives.

A PCA will help a member pick the best specialist, select the perfect Smart Cycle combination, schedule appointments, order prescriptions and answer any questions a person may have. With no dollar maximums to consider, these PCAs are free of any conflict of interest and can focus wholeheartedly on the best outcomes for their patients. It’s a true relationship and because PCAs are entrusted with so much responsibility, Progyny is quite selective in who it will hire to this position.

“We have babies named after our PCAs and you can’t find that elsewhere in our industry.” — CEO David Schlanger

Progyny’s PCAs come from fields like fertility, nursing, social work, psychology and endocrinology and boast years of relevant experience. Each PCA is also put through a training program before they can communicate with their first patient — all of this to guarantee Progyny’s consumers have the best experience possible. Generally speaking, the company’s hands-on, supportive approach also works to reduce the stress levels of hopeful mothers pursuing treatment. According to countless medical journals, there is a materially negative correlation between higher stress levels and higher rates of pregnancy.

How Participating Fertility Specialists Win:

Not only are the treatment plans superior and PCAs a wonderfully trusted ally, but Progyny also opens members up to its world-renowned network of fertility specialists. It calls this its “Center of Excellence.” The company’s network features 900 total specialists and 650 clinics across the United States including 46 out of the top 50 clinics in the nation. This makes confidently scheduling an appointment with an elite care provider an easier task — especially because a PCA does it for us.

Unsurprisingly, Progyny is extremely selective with the specialists it allows to enter its exclusive network. According to CEO David Schlanger, “providers consider it a privilege to be part of our network” which has allowed Progyny to aggregate a vast group of talented industry experts.

“When we started out 5 years ago, we had to beg doctors to be involved. Now doctors are begging us.” — CEO David Schlanger

Progyny boosts volumes for these participating clinics thanks to opening them up to its growing list of clients and members (covered below). It also improves its network’s overall treatment efficacy by providing the clinics with adequately covered patients. Because these patients can select the best treatment plan and always see it through to the end, Progyny frees its network of specialists to be at its best.

“Doctors don’t view us in the same boat that they view large commercial carriers and think working with us is easier and more beneficial to their practices.” — CEO David Schlanger

To add to the utility Progyny provides, the company eliminates administrative bloat and risk for its clinics and specialists. How? By paying them for the full value of the treatment directly. This means clinics have a far lower bad debt expense arising from consumers defaulting on expensive treatments.

Unlike its competition, Progyny requires its clinics to share any and all data they have on treatment selections and outcomes — as I briefly mentioned above. Each quarter, Progyny uses all of this feedback to send out report cards depicting each specialist’s results while also publishing the results of its top performing clinics. This not only creates a healthy sense of competition but allows Progyny to keep track of underperforming clinics and to remove those not meeting the company’s high standards. Inevitably, it leads to the sharing of best practices to raise the level of care across the entire network. All of this data aggregation and sharing is always done in a fully HIPPAA compliant manner.

The company signs 1-2 year contracts with each participating clinic and annual renewal contracts are signed thereafter.

How Employers win:

The better patient outcomes Progyny creates also lowers operating costs for employers. By offering more personalized, appropriate and effective treatment, employers are able to reduce the amount of fertility programs they will actually have to fund.

To begin to quantify this edge, Progyny’s pregnancy rate per IVF transfer is 61.4% vs. 53% for the national average. This translates into an average of 1.63 IVF treatments per Progyny member vs. 1.88 for the USA as a whole. Considering IVF costs roughly $12,000 per round, this leads to savings of $3,000 per employee electing to use IVF treatments. That $3,000 adds up very quickly for the large enterprises Progyny services.

Progyny patients also have multiple births at a rate of just 2.8% vs. 9.9% for the national treated average. Based on twins costing 5x that of a single birth (and triplets nearly 20x), this represents a substantial additional cost reduction as well. These are just two of many areas for cost savings that employers enjoy. Broadly speaking, these large enterprises save on a portion of the tens of billions of dollars spent on annual NICU costs.

Again, when employers focus on fertility coverage efficacy rather than cutting costs, the costs magically fall anyway. Based on the most common hesitation with adding fertility coverage being incremental costs, this is important.

Beyond cost savings, employers enjoy more productive and happy labor forces. Shorter time to pregnancy reduces the emotional burden this process inherently takes on parents and allows them to return to work much more expediently. Superior treatment plans serve as a powerful recruiting tool for employers trying to win over new talent. Based on our nation’s extremely tight labor force at the moment, this adds yet another layer of value for Progyny’s customers.

Along these lines, Progyny often cites a network effect emanating from its operations. Once one large player in a given sector purchases Progyny’s offerings, it generally puts pressure on competing employers to do so to most effectively compete for new hires.

More loyal, productive, healthy and talented labor forces plus lower expenses makes it increasingly difficult for clients not to go with Progyny’s offering.

b. Progyny Rx solution

Progyny also offers a prescription benefits plan — called Progyny Rx — for its members to save on drugs throughout their fertility treatment. This product blossomed from listening to frustrations expressed by enterprises such as difficulty with accessing fertility drugs in a timely manner for their employees. As a reminder, these drugs require a strict schedule and precise administering techniques based on a mother’s finite window of fertility. Perfect timing is of the essence.

So how does Progyny Rx help?

First — similarly to a traditional pharmacy benefits manager (PBM) — Progyny Rx leans on extensive drug manufacturer relationships to save users and employers 20% on fertility drug unit costs. It also generates another 8% in savings for employers from “waste management savings” via common overprescribing issues with legacy solutions.

Progyny Rx uses its broad relationships to cut through a large chunk of red tape and get prescriptions to patients more expediently. As a reminder, these fertility prescriptions are not fulfilled by typical pharmacies but specialty pharmacies which leads to complex authorization and people not getting medications for 1-2 weeks on average. Typical pharmacies are simply not designed to meet the time-sensitive needs of administering fertility medications.

Progyny leverages its industry relationships to cut that 1-2 weeks down to 2 days and even includes a delivery service for all members to boost convenience and thus adherence. The company also provides extensive educational resources (in addition to its PCAs) to ensure all questions about pharmaceutical usage are answered; Progyny Rx’s mission is to ensure medications are taken in the most effective way possible.

This program has only been around since 2018 yet has already been adopted by 73% of Progyny’s clients with 84% of new customers purchasing it in 2020. Just like the fertility benefits product, Progyny Rx is generating lower costs and better outcomes for all associated parties.

c. More Pieces of Progyny’s Value

Employers using Progyny’s services get a clear edge with regard to Environmental, Social and Governance (ESG) claims. While many legacy fertility coverage offerings prevent the LGBTQ+ and single mother by choice communities from accessing appropriate treatment, Progyny does not. It also offers a surrogacy and adoption reimbursement program to guarantee that future mothers needing alternative options have the financial backing to do so.

Finally, Progyny’s member portal functions as a centralized platform for patients to review coverage, study benefits options, track claim details and keep up on account balances. Transparency is of the utmost importance for Progyny. No matter who you are, where you come from or how you choose to live — Progyny has you covered.

This company is finally creating incremental flexibility, access and peace of mind in an antiquated space desperately needing a reset.

d. Summarizing the Triple-Pronged Value Proposition:

For Progyny’s Members:

- Safer, faster pregnancy.

- A dedicated PCA for emotional support.

- Vast educational resources.

- Less career disruption.

- Prescription savings.

For Progyny’s Network of Specialists:

- More volume.

- Better efficacy due to broad treatment flexibility and full coverage.

- An ability to measure results vs. other clinics.

For Progyny Clients:

- Less fertility treatment due to higher efficacy.

- Lower NICU costs powered by superior safety.

- Healthier, happier and more loyal workforces.

- Prescription savings.

- More competitive in recruiting new talent.

Healthier and happier mothers and children, more successful specialists, safer treatment, constant support and more successful client and specialist businesses. That’s Progyny.

3. Quantifying Progyny’s Impact

It’s nice to say Progyny does things better, but it’s really nice when that claim comes with 3rd party data to quantify its edge. Fortunately, we have it for this company.

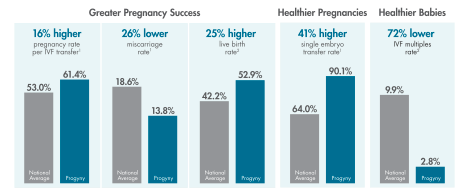

The Society for Assisted Reproductive Technology (SART) and the Center for Disease Control (CDC) recently released a report on the latest American fertility data. The results were wildly encouraging with Progyny delivering a 16% higher pregnancy rate and a 26% lower miscarriage rate both vs. the national average. Additionally, its IVF multiples rate is 72% lower than the national mean with its single embryo transfer rate 41% higher than the national mean.

The encouraging statistical leads continue. Progyny raised its live birth rate lead over the national mean from 23% higher to 25% higher year over year which feeds into a broader overall pattern. The company’s live birth rate has improved 14% since 2016 while the national average has stagnated. Progyny’s lead grows every single year.

The fertility disruptor now boasts a 52.9% live birth rate vs. just 42.2% for the national average which directly leads to lower costs incurred by all parties and happier patients.

Perhaps unsurprisingly, Progyny’s member support services boast an industry-leading net promoter score (NPS) of +79 with its integrated Progyny Rx offering carrying an even higher +81 NPS.