Quarterly Portfolio Summary

Quarterly Portfolio Summary

An Update on My Holdings, Process & Plans

Today’s article is powered by Savvy Trader, the company allowing me to offer free text message transaction alerts. To sign up, click here.

1. My Holdings — September 2022

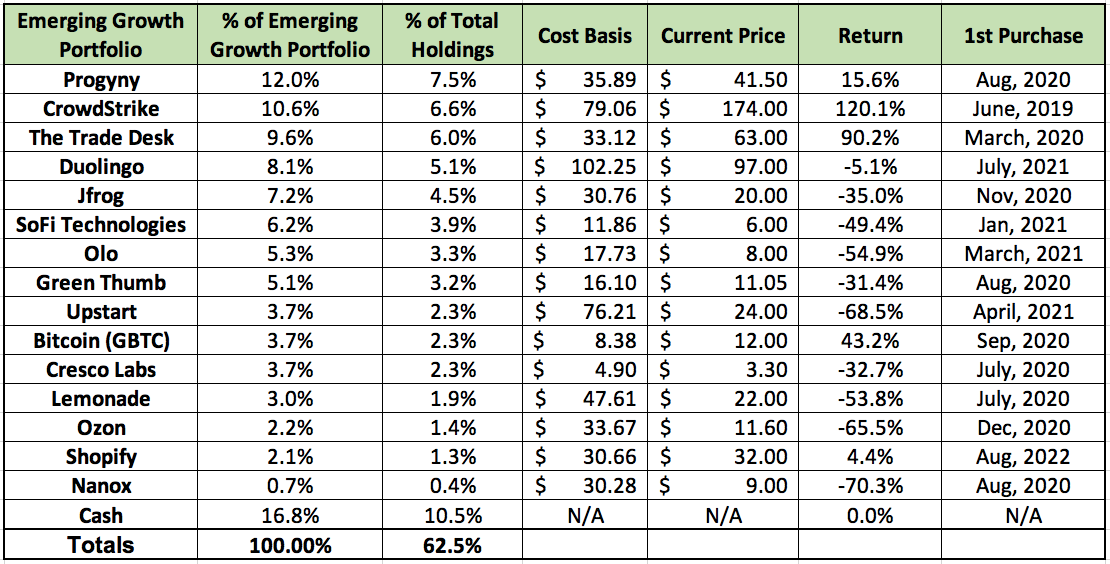

a) Emerging Growth Portfolio

Please note that I do not include exited positions like FedEx, Royal Caribbean, Planet Fitness, Goldman Sachs, Microsoft, Viacom etc. which have represented my best investments to date.

I exited GoodRx this quarter and initiated a new position in Shopify.

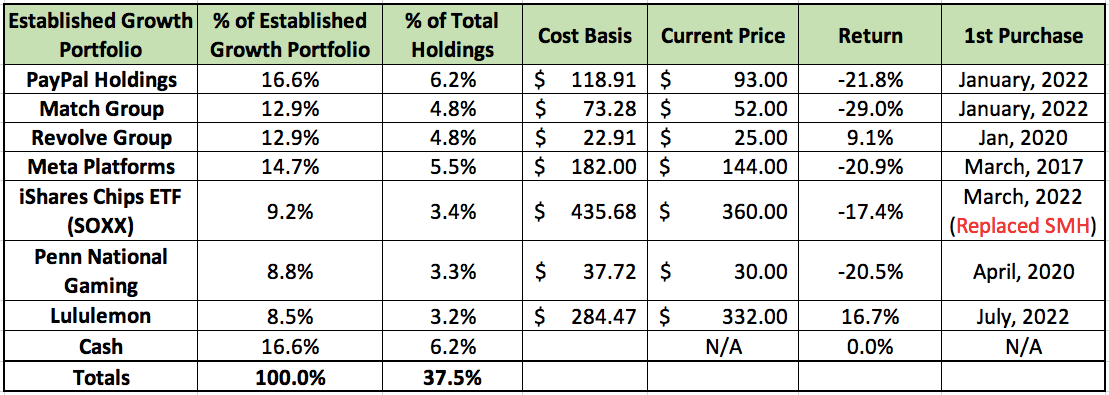

b) Established Growth Portfolio

c) Watch List

Chipotle

Airbnb

Adyen

Google

Sprout Social

Planet Fitness

FedEx

Wingstop

2. Summing Up Another Earnings Season

a) The Stand-Outs

Lululemon:

2022 has been a year to forget for the consumer discretionary category. Even for more affluent-focused brands like Revolve, times became abruptly more difficult while demand and margins grew more challenging. Lululemon did not get the memo.

This company posted a masterpiece quarter in every sense of the imagination. Demand remains incredibly robust with up-beat forward expectations as well. International growth recovered ahead of schedule, and it took more category marketshare than any other competitor during the quarter at 1.4% incremental gains. New categories are working. Legacy categories are working. It’s all working.

From a margin standpoint, things were equally positive. Gross margin held up admirably (regardless of large freight and FX headwinds not impacting it as materially last year).

“We are pleased to see some promising signs of supply chain improvement yet recognize further normalization will take time.” -- CEO Calvin McDonald

Operating and net margins both materially expanded, and the firm crushed profit per share estimates with guidance well ahead of forecasts as well. The company has been obsessively monitoring macro trends to seek out the weakness that its competition has cited — but it has seen no deterioration to date. This continued healthy traffic is also not being created via promotional activity, but largely at full price.

The ONLY slight negative from the report was the 85% YoY rise in inventory levels. But the reasoning eased that concern for me entirely. First — and most importantly — demand remains very strong and it feels like it’s “better positioned for the fall season” than it had been a year ago. Recall that 2021 was a period when Lulu was dealing with frequent supply outages and “leaving demand on the table.” The spike is its response to ensure that issue doesn’t recur. It anticipates zero pricing promotion to work through the new inventory — meaning it won’t weigh on margins.

Times are getting tough, but Lululemon seems to be tougher.

Duolingo:

Duolingo is quickly establishing itself as a quarterly stand-out. Countless app-based businesses have struggled with the post-pandemic hangover paired with macro pain in 2022; results have suffered as a result. Duolingo has managed to side-step all of this. How? Perhaps it’s the company’s prominent position in nearly half of American classrooms… maybe it’s the habitual split testing and core focus on product enhancement over marketing… or maybe it’s the robust word-of-mouth growth it gets because of that. Whatever the cause is, it’s working.

Bookings beat estimates by 11%, conversion from free to paid users materially accelerated and users overall continued to easily set company records. Again, this is not a Pinterest or a Snapchat — its model is proving to be far more durable across economic cycling.

“Subscribers as a percent of MAUs has outperformed what I thought would happen... I don’t see a reason why this can’t get to the mid-teens.” — Co-Founder/CEO Luis von Ahn

The company earned a slight EBITDA profit with expectations to be EBITDA negative, its gross margin continued to expand to an even more robust 73% and it exponentially (small base) raised its EBITDA guide for the rest of the year. Not bad.

The app is again live in China, finding rapid growth in India and quickly establishing itself as a digital education juggernaut.

“The macro environment is pretty crazy, but so far we have seen no weakness in our numbers whatsoever. We expect strong numbers… no layoffs are coming and we continue to hire.” — Co-Founder/CEO Luis von Ahn

b) The Good

The following companies materially exceeded expectations while offering up-beat guidance:

CrowdStrike

The Trade Desk

Progyny

JFrog

SoFi Technologies

Lemonade

Penn Entertainment

c) The “Meh”

The following companies reported roughly in-line results and guidance with perhaps a bit of downside amid chaotic macro:

Nanox

PayPal Holdings

Green Thumb (no guide like always)

Cresco (no guide like always)

Shopify

d) The Underwhelming

The following companies reported results that I found disappointing:

Olo

Upstart (accumulation paused for now)

Thanks to the Savvy Trader app, I can share my real-time portfolio with readers, offer text/email transaction alerts and publicly compare my performance to benchmarks -- all for free. Alerts include position added to/trimmed, percent change, and also a brief explanation from me on the reasoning behind the move.

If you’d like to make your own portfolio to publicly share, you can do so here.

If you’d like to sign up for my free portfolio alerts, you can do so here. (note that “MSOS” is a placeholder for “CRLBF” and “GTBIF” while those are added to the platform)

3. About my Investing Mindset

This section serves as an evolving explanation of my investing approach. For those who have read previous quarterly updates, it will look very familiar.

a) Stock Picking

I approach investing with a unique set of life circumstances that shape my risk posture and investment horizon. Personal considerations (a child-free millennial) account for this. As a result, I have a strong stomach for prudent, diversified risk. Your different circumstances could call for a different approach. Based on my own circumstances and preferences, my objective is to seek out two different types of companies:

Young, emerging disruptors with the potential to deliver life-changing returns while being accompanied by immense downside risk.

Established growers with long track records of effective compounding, the ability to continue growing 5%+ per year, strong cash flows and expanding or durable margin profiles. I often look for operational hiccups here (among a sea of consistent execution) to start positions.

How am I so comfortable with occasionally making bad picks and incurring material losses? A few notes on this. First, the profit potential of public equities makes imperfection entirely okay. The sought “10 bagger” everyone seeks out can work wonders in more than making up for several losers. Finite downside and infinite upside is a wonderful combination. Similarly to private equity or venture capital, this approach -- especially with the emerging portfolio -- frees the overall portfolio to succeed while still being wrong quite a bit.

Secondly, you can’t win if you won’t accept the potential of a loss. That is the essence of risk. Index funds are a perfectly good option for those not wanting to try (no shame at all). Accepting some failure as inevitable is a large part of the psychological and financial battle. Humility goes a long way here and without it -- markets will humble us all in a hurry. When we expect perfection, we leave ourselves vulnerable to over-indulging or over-allocating into high conviction names. Over-allocation is the antithesis of good diversification and is a great way to get hurt. To combat this tendency, I've instituted a rule that I will never invest more than 6.6% of my wealth into any single name with a 4% max for cash burners. No matter how certain I am about a holding, I will try to avoid putting in more than that. Higher portfolio allocations can result from winners growing larger thereafter (see CrowdStrike) or portfolio values being cut as they were this last year. Again, that edge of finite downside only happens through diversification -- if I place all of my funds into one name, then the same finite downside still equates to a potential 100% loss of capital.

More rules I strictly adhere to:

No margin, ever. Debt is for reliable, cash flowing assets such as quality real estate. It's not for speculative assets.

No warrants, options, futures contracts or any other derivative instruments. Common equity only.

It's hard enough to be right about the long-term fundamental thesis of a firm. It's even harder to forecast the short-term timing of being right about that opinion and the coinciding stock move.

Common equity doesn't require me to express any vital opinion on timing, derivatives do.

Long only with cash position serving as my hedging mechanism.

Thematic ETFs for sectors I don’t understand well enough like semiconductors.

More general qualities I look for in a prospective position:

Sustainably brisk revenue growth with a long runway.

Generally 15%+ for the emerging portfolio & at least double run rate U.S. GDP (so roughly ~5%+) for the established growth portfolio.

Profitability and/or material margin expansion showing signs of getting there.

Management integrity (lack of red flags).

Public investors rely on honest disclosures from executives. If I’m not comfortable making that assumption, I avoid the company.

A tangible value proposition/competitive edge ("X% better than the competition at X").

Progyny’s 25% live birth rate edge over the competition is a great example.

Seamless optionality (product expansion without heavy spend or operational overhaul is preferred). Easy optionality examples:

Lemonade expanding from renters insurance to other verticals like car insurance using the same software base.

Progyny expanding into Canada where its employer clients have significant U.S. overlap.

Balance sheet health (especially for cash burners)

I will accept material dilution for newly public companies… but that allowance is finite and temporary.

b) Portfolio/Risk Management

Risk management and the Macro Bogeyman:

My cash position fluctuates between 5%-33% of total holdings as cycles of panic and mania play out in stock markets. I am always predominately invested in markets, but I do use macro signals and market sentiment/conditions to trim and add around my permanent positions. For example, hot inflationary readings and spiking corporate credit spreads this year have led me to exercise more accumulation caution. This has kept the cash position slightly elevated.

Macroeconomic events like supply chain chaos and monetary policy can work wonders to indiscriminately sweep up every public company via hefty stock pullbacks. It’s important to respect those events for stock-pickers like me, but also to be willing to patiently take advantage of them. I’m not waiting for macro signals to be 100% rosy and green. It would likely be too late to enthusiastically add at attractive multiples by then. Instead, I’m looking for the first derivative of macro signals to turn positive. In other words, for things like breakeven inflation rates and consumer confidence to start to suck a bit less. We’ve gotten that development in the last several weeks and I’ve recently (slightly) leaned in as a result. I’d like to see more trend confirmation before really getting excited.

As an aside, it feels like that excitement will come as we head into 2023 when the Fed Funds rate likely stops moving higher. But I’m not one to actionably predict macro patterns; instead I react to them. I'll remain data dependent and will keep my readers posted in the macro section of every single weekly article. I'm elated by the prospects of sinking my teeth into accumulating more shares of fundamentally thriving companies at much lower multiples (who doesn’t love buying on sale?). We are much closer to that point than 3 months ago in my opinion.

A major caveat is needed in the conversation around adding into share price reductions. It is vitally important -- as a stock picker during these times especially -- to be able to identify which companies deserve the selling and which are the babies being unfairly thrown out with the bath water. That’s where we create alpha.

I tweak the wildly cliché mantra from Warren Buffett when it comes to position management: "Be greedy when others are fearful, the company is healthy and macro is improving or easy.”

As a stock picker, I'd love to focus on microeconomics and what my holdings can control rather than fixating on what they can't. But the unspoken stock-picker’s truth is that most risk assets are correlated and that a dropping tide lowers all boats (& vice-versa). At this point in time, the uncontrollable is still negative for companies and the tide still needs to rise much more. Fellow stock pickers ignore that at their own peril, but to me, macroeconomic headwinds are to be deeply respected AND treated as longer-term opportunity. In my view, it’s a balancing act.

Non-Scheduled Turtle Mode:

I’ve had questions regarding my slow pace of position building, but it's a natural bi-product of the wildly volatile firms that I invest in. These innovators are inherent rollercoasters as stocks (see the last several months and also the last 100+ years). Considering this, I love the idea of always keeping some dry-powder available for when that rollercoaster dips down once more.

My style of accumulation is not dollar cost averaging as that approach allocates new funds on a pre-determined, scheduled basis. There's nothing scheduled about my accumulation path. Instead, it's purely a reaction to multiple compression, Mr. Market's madness and how the exogenous backdrop looks.

I'm not looking for technical strength -- although that frequently coincides with macroeconomic strength -- and I am never trying to perfectly time a bottom. I'm merely taking advantage of more favorable risk-reward as valuations shrink. Still, stock markets can be quite irrational in the short term as they're based on unpredictable human psychology; considering this, it makes the most sense to me to accumulate in very small pieces so that I have the flexibility to take advantage of more madness.

Not only do I benefit from future deals, but this also works wonders for my tranquility. There are two not-so-secret, secrets to my discipline amid hectic price action: First is developing a complete understanding of the firm (not the stock) so I can understand signs of execution or failure, and second is my cash management. A complete understanding of the firm and its value proposition is what allows me to have confidence to hold and accumulate when a stock is dropping. The cash position is what enables that.

The downside of this strategy vs. investing as cash becomes available is the potential of me holding a lofty cash position as markets rip higher -- but that's an opportunity cost I'm comfortable with. This works for me. My approach also undoubtedly means that I will occasionally underperform on a shorter-term basis like I have this year. Accepting that is important for me to limit portfolio churn which would otherwise work to erode long term alpha. I want to outperform on a multi-year basis -- I don't care about a quarter.

Valuation Starting Point Matters:

The idea of seeking out multiple compression within thriving firms to justify position-building requires more context. While I don’t automatically pass on a company due to a lofty valuation, I do start with much smaller purchases if I want to own it. Shopify is a great recent example for me.

The starting point of the actual valuation still does matter a lot. These past 2 years, we've seen countless firms publicly debut at 30X+ sales while 30X+ earnings or free cash flow used to be expensive. One great example of this was Olo. I invested in the IPO on day one -- although its 40X sales peak valuation kept the position initially tiny. Olo's sales multiple compressed to 35x, then 30x, then 20x and then below 10X -- but I did not start adding. I waited until the organization's forward EBITDA multiple fell below 100 (still expensive but far more reasonable) to begin building out the position.

Note: I’m going to be posting a Twitter thread on Sunday explaining the income statement, its acronyms and topics like valuation.

There's a benchmark of multiple compression that I require each healthy but expensive position to clear before my accumulation accelerates. It's not uniform as things like margin expansion and faster, more sustainable growth can make what's traditionally considered to be expensive far more tolerable. Again, this approach could have led to me owning a much smaller long term position in Olo than I wanted, but I was comfortable assuming 40X sales just would not last. See the last century+ of public market valuations.

No Shame in Trimming:

The flip side to multiple compression is multiple expansion. To have cash for future accumulation, I need to be willing to trim small pieces of positions as they get more and more expensive (and so as fellow investors get more and more excited). As a rough guideline -- and based on my cash position fluctuating between 5-33% -- I generally consider 67% of a current position to be permanent (as long as company performance remains strong) and the other 33% as more temporary and trade-able as valuations become loftier or more compelling. For example, when Lemonade soared from $50 per share to $180 per share on no profit inflection or outperforming demand, I sold roughly 40% of my original investment (10% of the position at that time). This is personally how I practice fear/caution when others are greedy.

There's an important idea within that anecdote: Capital gains via multiple expansion are less appealing to me than capital gains via outperforming profit compounding. Within the famous price to earnings (P/E) multiple, I'd much rather see the "P" rising in tandem with the "E" vs. independently of it.

c) Quick notes on valuation and liquidity

I've used earnings/net income and cash flow multiples in my examples thus far, but that's not always appropriate. When a company is investing every single gross profit dollar it generates into more growth vs. letting that gross profit flow down to earnings, does it really make sense to still use a P/E multiple? Probably not. Of course when you're using a valuation ratio denominator that is intentionally near-zero, then the earnings multiple will be lofty.

As companies mature, I generally use denominators from further and further down the income statement and begin using the cash flow statement more readily as well. I start with gross profit multiples and transition to EBITDA, or operating cash flow multiples once a company has matured enough to be generating a material amount of either. As soon as there's a solid base of earnings and/or free cash flow, I transition to using those as denominators.

I prefer free cash flow vs. earnings if I had to pick one vs. another, but both are very useful. For example, a company purchasing loans to collect net interest income will be penalized via deducting that purchase from free cash flow -- but not net income -- when it was really just a change in balance sheet structure. Conversely, weird mark-to-market items within equity investment valuations can mess with net income while leaving free cash flow un-impacted. Again, both are important for completing the full picture of profitability.

Note that I never use sales multiples as this metric entirely ignores the quality of revenue growth. Any company with funding can invest $2 to create $1 in growth -- and while this will make revenue growth look more impressive, it is far from sustainable. If there's no gross profit to grade a company's valuation, I do not invest.

Balance sheet health also matters a lot when determining the appeal of company's valuation. One of my exits, CuriosityStream, now fetches a gross profit multiple of under 1X with 35% growth expected this year. While this seems compelling, we need to dig deeper. The company has just a few months of liquidity left on its balance sheet at the current, worsening burn rate. Expectations for inflecting to profitability are also being pushed out further which makes significant equity dilution and/or expensive credit deals all but inevitable. While the enterprise value at $1.60 per share is just $7 million today, it will likely be much higher at some point in the not-too-distant future. ALWAYS pay attention to shareholder dilution and capital leverage trends when judging the viability of an investment and also its current valuation.

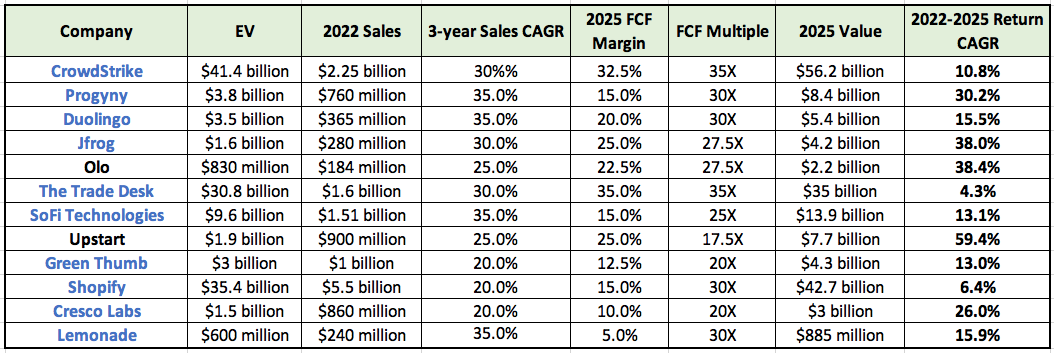

4. Forecasts

Below are my forecasted fair value and return estimates for all holdings (besides pre-revenue Nanox with its deep cash burn). I aggregated data from historical results, comparable firms and industry research to arrive at these values -- which should all be taken with a large grain of salt. The amount of assumptions that go into stock forecasting make the process inherently inaccurate -- actual results will surely differ from my projections. This merely paints a picture of where I think my holdings can be in five years if things don’t go poorly. I did try to lean slightly pessimistic whenever possible with growth, margin and multiple assumptions.

AGAIN, take these projections with a large grain of salt. Especially for the holdings with depressed enterprise values and sky-high 3-year forecasts, there is significant risk to that result coming to fruition!

One more item that's very important to note is stock based compensation. For companies with dilution expected over the next three years, I accounted for this by adjusting the current EV reading higher. For the companies that I did this with, the firm's name is colored in blue. For most, the adjustment was between 2% annually, although I made it 3% for SoFi, Cresco Labs, Green Thumb and Lemonade.

a) Emerging Growth Portfolio

hey Brad, saw your payPal update. Patience is the key in such cases. I have sometimes waited 3 years before fair value is reflected in a company. if you do this over many years, you will stop being frustrated!

Any updates to this holdings list?