Upstart Q1 2022 Earnings Review

Upstart Q1 2022 Earnings Review

Exploring the results of this young disruptor.

Today's piece is presented by Commonstock:

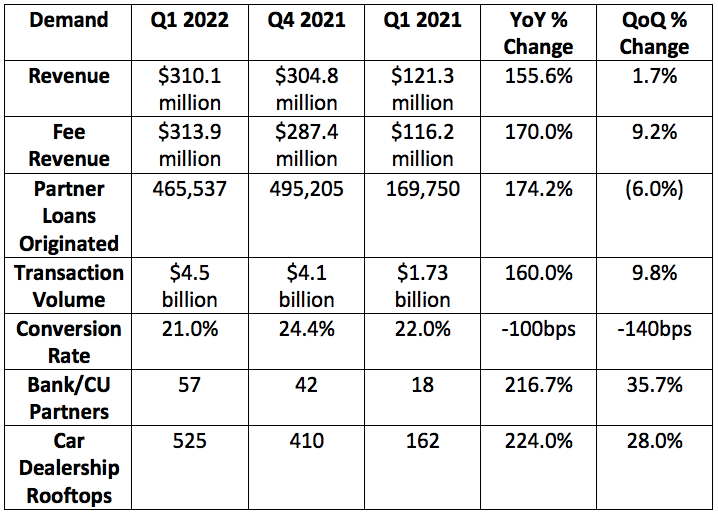

1. Upstart Demand

“We see a clear path to more than $10 billion in revenue in the coming years.” — Co-Founder/CEO Dave Girouard

Upstart guided to a midpoint of $300 million in quarterly revenue while analysts expected roughly the same. The company posted $310.1 million in sales, beating expectations by roughly 3.4%.

Upstart percent revenue beats by quarter:

3.4% beat in Q1 2022

17.2% beat in Q4 2021

8.8% beat in Q3 2021

22.9% beat in Q2 2021

4.3% beat in Q1 2021

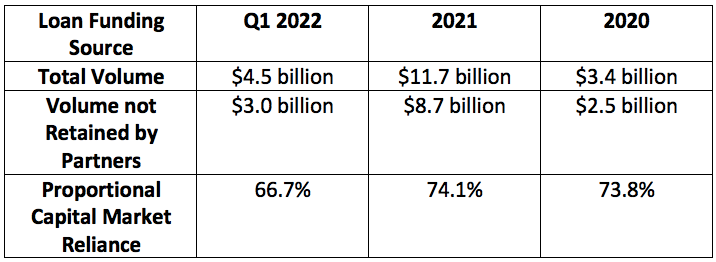

Loan funding source:

Upstart’ proportional capital market reliance fell sharply in Q4 2021 which marked an encouraging reversion of a consistently rising trend. For context, its reliance sat at 76.7% over the first 9 months of 2021, yet fell to 74.1% for 2021 as a whole (while including a 9 month 76.7% weighting). Section 6 of my Upstart Deep Dive explains why it is so important for partners to retain more loans. Lower capital market reliance is a good thing and that process is now playing out.

More quarterly demand context:

Q3 2021 conversion rate was impacted by a fraud incident that forced Upstart to implement heavier manual controls on a temporary basis. This quarter, falling conversion rate was via rising loan prices as rates rapidly moved higher.

The impact of the pandemic on Upstart’s business was aggressive, abrupt and short-lived.

Q2 2020 -- highlighted in red -- is the quarter with the heaviest negative impact by far.

The quarters highlighted in yellow feature periods when volumes were recovering but still off-trend.

Quarters highlighted in green feature the easiest comps via pent-up demand unwinding as the world recovered and things like stimulus checks (a large Upstart demand headwind) fade away.

Upstart waits to disclose concentration risk from Credit Karma and its originating conduits until its quarterly filing is published.

I’ll include that information on Saturday after the document is released.

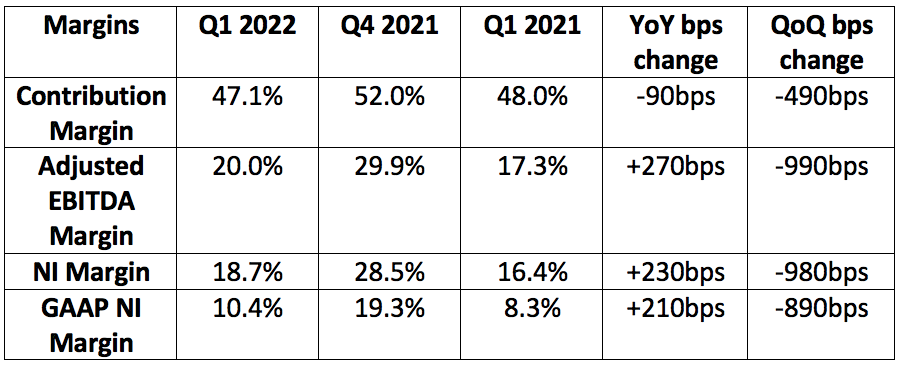

2. Upstart Profitability

Upstart guided to:

A 46% contribution margin -- it posted a 47.1% margin beating expectations by 110 bps.

$20 million in GAAP net income (NI) -- it posted $32.7 million beating expectations by 63.5%.

$0.60 in earnings per share while analysts were looking for $0.53 per share. Upstart posted $0.61, beating its expectations by $0.01 and analyst estimates by $0.08.

$57 million in adjusted EBITDA while analysts were looking for $55.2 million. Upstart posted $62.6 million, beating its expectations by 9.8% and analyst estimates by 13.4%.

More margin context:

Upstart's contribution margin compression is solely a factor of its newer auto business outperforming demand ramp expectations. Its products debut at contribution margin troughs before improving thereafter with more data and scale.

EBITDA and contribution margin divergence is related to rising rates lowering the fair value of the loans on its balance sheet. This does not impact contribution margin.

Upstart's personal lending contribution margin was 51% during the quarter.

Commonstock is a friendly community of passionate investors who believe that transparency can elevate discussion and performance. This platform strikes the perfect balance between collaborative debate and uplifting camaraderie. I like to think of it as a more focused, verifiable, productive and kind version of FinTwit -- without all of the noise.

There's a reason why I have linked my portfolio to the service and am a daily active user.

Come join us to see what all of the hype is about. Sign up is free and you'll be glad you did.

3. Upstart Guidance

a. 2022

b. Q2 2022

Upstart sharply missed analyst expectations of $58.8 million in EBITDA by guiding to $33 million.

Upstart sharply missed analyst expectations of $0.56 per share by guiding to roughly $0.34.

Implied forward valuation -- The firm now trades for roughly 13X its implied forward EBITDA guidance.

4. Co-Founder/CEO Dave Girouard Call Highlights

On partner momentum:

Upstart is adding an average of one new lending partner per week. It had 10 total in 2020.

11 lenders have now dropped all FICO minimums vs. 7 QoQ and none as of last year.

“Partner pipeline momentum has never been stronger... No partners have seen any loan underperformance in light of macro.” — Co-Founder/CEO Dave Girouard

On Macro:

“In recent weeks, it has become apparent that 2022 is shaping up to be a tough one for financial services... the 200 basis point rise in the 2-year yield led to a 300 basis point rise in the average prices of our loans which lowered approval and conversion rates... We've been through several disruptions through the years and have gained market share each time. Despite this challenging environment, we'll still grow by 47% and generate positive cash flow.” — Co-Founder/CEO Dave Girouard

Rising rates push the return requirements higher for Upstart partners and investors as their access to capital becomes more expensive. Its partner banks are more insulated from this risk as they can use deposits to fund loans. Conversely, capital markets are quite vulnerable to aggressive moves in treasury yields and that leads to them demanding higher APRs from borrowers -- which lowers conversion.

Girouard told us that the vast outperformance of Upstart's loans brought on by stimulus checks has reverted to in-line performance. No lending partners or institutional investors have experienced underperformance.

“We expect less volume than we would have a few weeks ago due to higher pricing in the market place as base rates and risks rise for investors. We’re not terribly interest rate sensitive but in this case the rise has been much more significant.” — Co-Founder/CEO Dave Girouard

If things got bad enough, this could eventually weigh on Upstart's take rate -- that hasn't happened yet.

Upstart is planning on adding in more customization features to its underwriting model to allow partners to set their own macroeconomic assumptions.

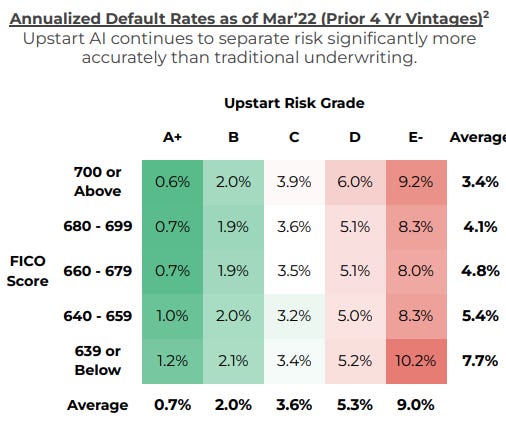

Visualizing Upstart's underwriting quality vs. legacy models -- the image below depicts Upstart's risk grades as being more predictive of risks than FICO bands:

On auto refinancing and Upstart Auto Retail:

“We're moving into phase two for Upstart Auto Retail. Early progress has exceeded our most optimistic win rate expectations. The team is working to quickly smooth out final issues and integrations for a rollout to 25% of the population this quarter. “ — Co-Founder/CEO Dave Girouard

Upstart auto retail will begin to be a material contributor to volumes by the end of the year.

Auto-refi instant approval rate doubled sequentially.

Auto remains contribution margin negative as it scales.

Upstart continues to retain auto loans on its balance sheet to build stakeholder confidence in its underwriting. This is expected for its newer products.

More notes:

The micro-loan product is in beta-testing. It will launch this quarter vs. previous expectations of by year's end.

Its small business lending product is in its initial testing phase. Early results on the underwriting quality vs. alternatives are "promising."

90% of small banks have no online small business loan application.

5. CFO Sanjay Datta Call Highlights

On Macro:

Last quarter, Sanjay told us that Upstart was insulated from modest interest rate fluctuations. The violent interest rate fluctuations we've gotten since then -- however -- did have a material impact on Upstart's pricing as partners quickly became more risk averse and as capital become more expensive.

Note that rising rates also meant the carrying value of Upstart's loans actually shrank this quarter. This led to its other revenue segment contributing negative $3 million vs. positive $5 million QoQ.

Visualizing stimulus checks impacting default rates:

Per the investor presentation:

Loan demand continues to recover as stimulus fades.

Rising delinquency rates stabilized over the last 60 days.

Worsening macro is prompting Upstart to add new layers of conservatism into its 2022 outlook. More conservative with guidance is always a good thing.

On the balance sheet:

Upstart's loans, notes and residuals held on the balance sheet soared from $260 million to $600 million QoQ. This was a factor of the abruptly tightening macroeconomic environment to ensure liquidity for loans as partner recalibrate. This was my least favorite part of the report.

“We used our balance sheet as a market clearing mechanism. When rates rise so quickly, it’s fair to say our platform’s ability to react to the clearing price is not as quick as we’d like. As rates move and investors set new return benchmarks… there can be a delay in reaction which is when we step in to bridge things with our balance sheet. This is not a long term or large activity. Responding more nimbly to changing rates is something that we’ll invest in to automate.” — CFO Sanjay Datta

A few notes on this:

It's likely that the most aggressive of the rate moves are largely behind us and this issue won't recur in the near term. Still, it's a clear negative that Upstart has to plug funding gaps like this when macro abruptly changes.

I would hope recalibration investments are a high priority given how unappealing it is for Upstart to hold these loans rather than being able to use the liquidity for R&D.

Roughly 75% of the loans that it purchased for sale were from R&D investments in its younger auto segment... not this market clearing issue.

Loans purchased for sale were well below 10% of Upstart's total volume.

Upstart's preference is to hold 0 loans on its balance sheet.

On capital market demand:

Sanjay reiterated that the company thinks partner retention and whole loan purchases will make up a larger portion of loan volumes this year as asset-backed securitization (ABS) markets cool off from historical strength in 2021.

Upstart does not anticipate needing to retain any residuals on these loan pools in the future in order to get the demand cleared. Some were concerned about this.

Upstart fortunately does not anticipate triggering any cumulative net loss (CNL) thresholds for its large capital market deals.

6. My Take

This was Upstart's worst quarter as public company by a sizable margin. It simply got too excited in its ability to overcome macroeconomic headwinds and the revenue guide down is the result. With that being said, Upstart's credit performance continues to hold up well, it continues to rapidly onboard new partners and more of those partners continue to drop all FICO minimums. This will be a tough year for the firm, but the thesis remains intact.

In light of the heavy after-hours sell-off, I will likely be adding to my stake tomorrow morning. STILL, despite the wildly negative share price reaction, I will leave more room to average in to more multiple compression -- I AM NOT GOING ALL IN. At likely ~20X 2022 earnings and with 47% growth expected despite chaotic macro, I think there's a lot to like about the deal. There's also many reasons to continue exercising caution and to creep into the name at a SLOW pace. If it can endure these next several quarters, there will be brighter days ahead; I remain somewhat optimistic in its ability to do so, but this quarter certainly raised some new concerns.