Table of Contents

1. Broadcom (AVGO) – Earnings Review

A quick introduction to Broadcom's business can be found here.

a. Key Points

- AI chips drove the outperformance.

- Reiterated 2027 guidance while hinting at upside.

- Margin pressure is related to revenue mix-shift as Semiconductor Solutions becomes a larger portion of the business.

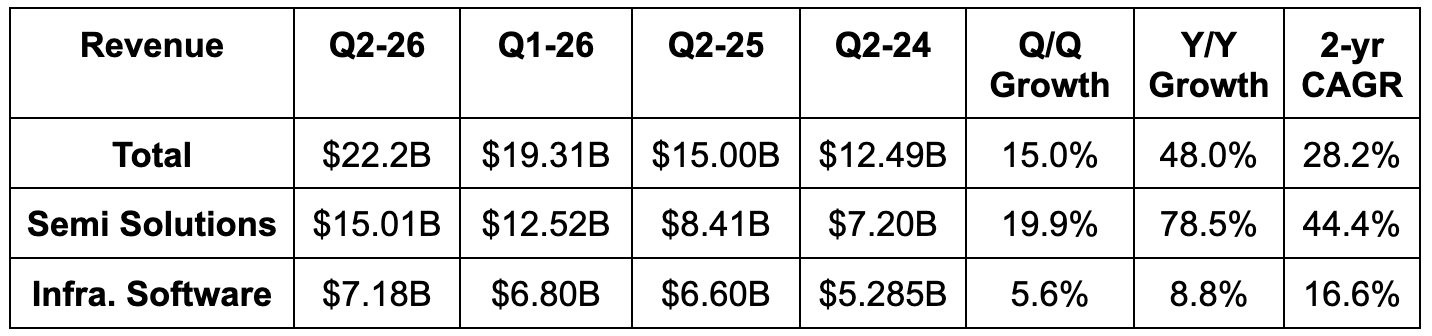

b. Demand

- Slightly beat revenue estimate & beat guidance by 0.9%.

- Semiconductor Solutions revenue beat estimates by 2.5%.

- Infrastructure Software revenue missed estimates by 1%.

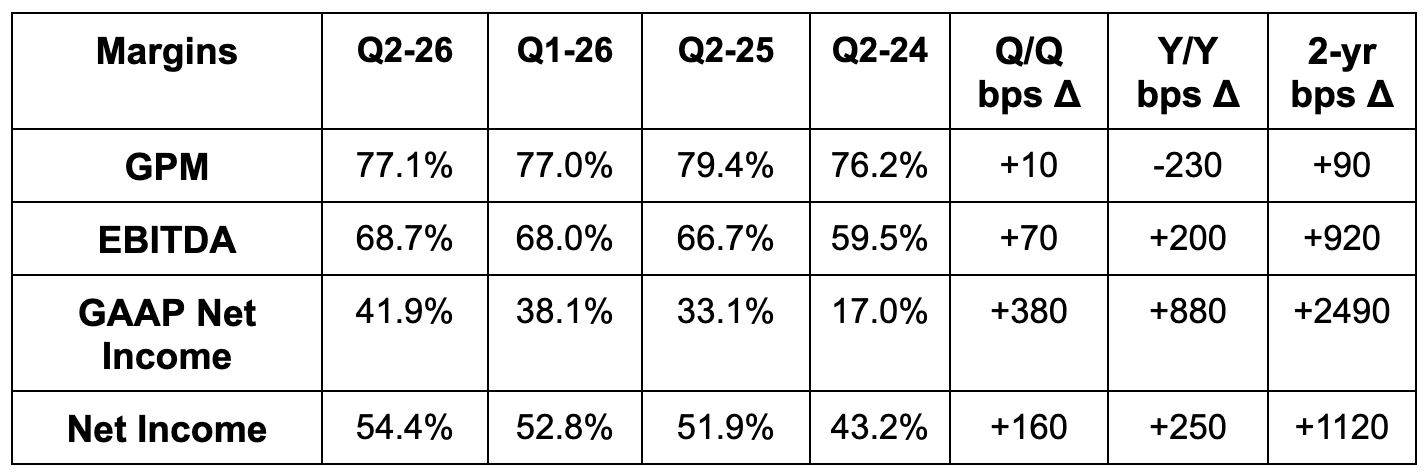

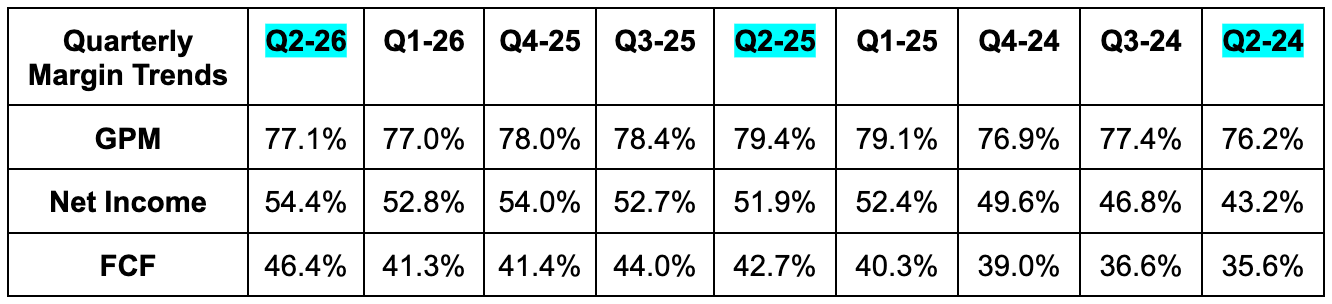

c. Profits

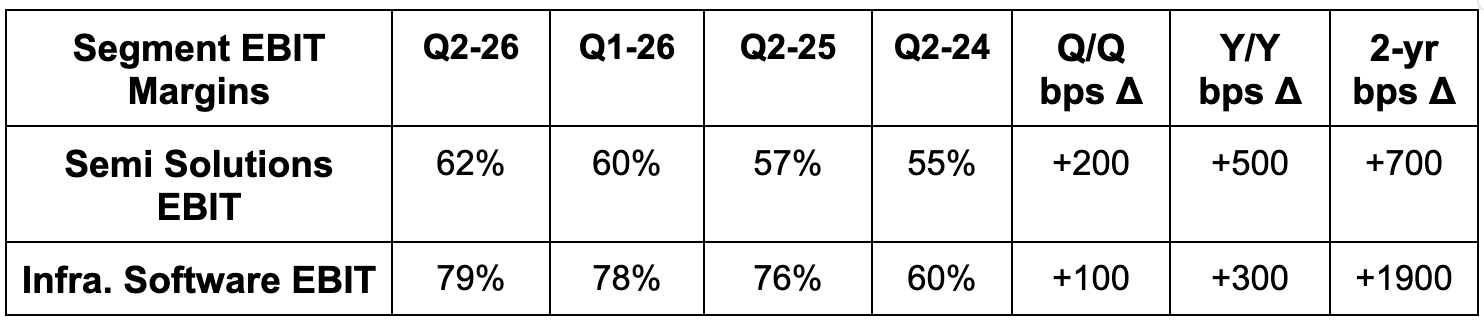

- Met GPM estimate & met guidance. The Y/Y decline in GPM was due to product mix. Semiconductor Solutions GPM rose from 69% to 70% Y/Y and Infrastructure Software GPM was stable at 93% Y/Y. Semiconductor Solutions just became a larger piece of the overall business.

- Beat EBITDA estimate by 0.6% & beat guide by 1.87%. Strong demand, pricing power and OpEx efficiency enabled the margin expansion despite GPM falling materially Y/Y.

- Beat $2.40 EPS estimate by $0.04.

- Missed FCF estimate by 13%.

d. Balance Sheet

- $19.6B in cash & equivalents.

- Inventory up 91% YTD. Days of inventory on hand rose from 68 to 86 Q/Q. They think they have sufficient supply through 2027 and are working on getting what they need for years beyond that.

- $65B debt.

- 1% Y/Y dilution.

e. Guidance & Valuation

Q3 revenue and EBITDA guidance were 3.0% and 2.8% ahead of expectations, respectively. Revenue guidance represents 84% Y/Y growth. This includes $16B in AI semiconductor revenue and $4.5B in non-AI semiconductor revenue, representing 200% and 12% Y/Y growth, respectively. It also includes 31% Y/Y growth expectations for infrastructure software. Finally, they expect Q3 GPM to fall from 78.4% to about 74% Y/Y due to product mix-shift. They were quick to say this has nothing to do with demand deterioration or pricing power and that the EBIT margin would be stable on a Y/Y basis despite this headwind.

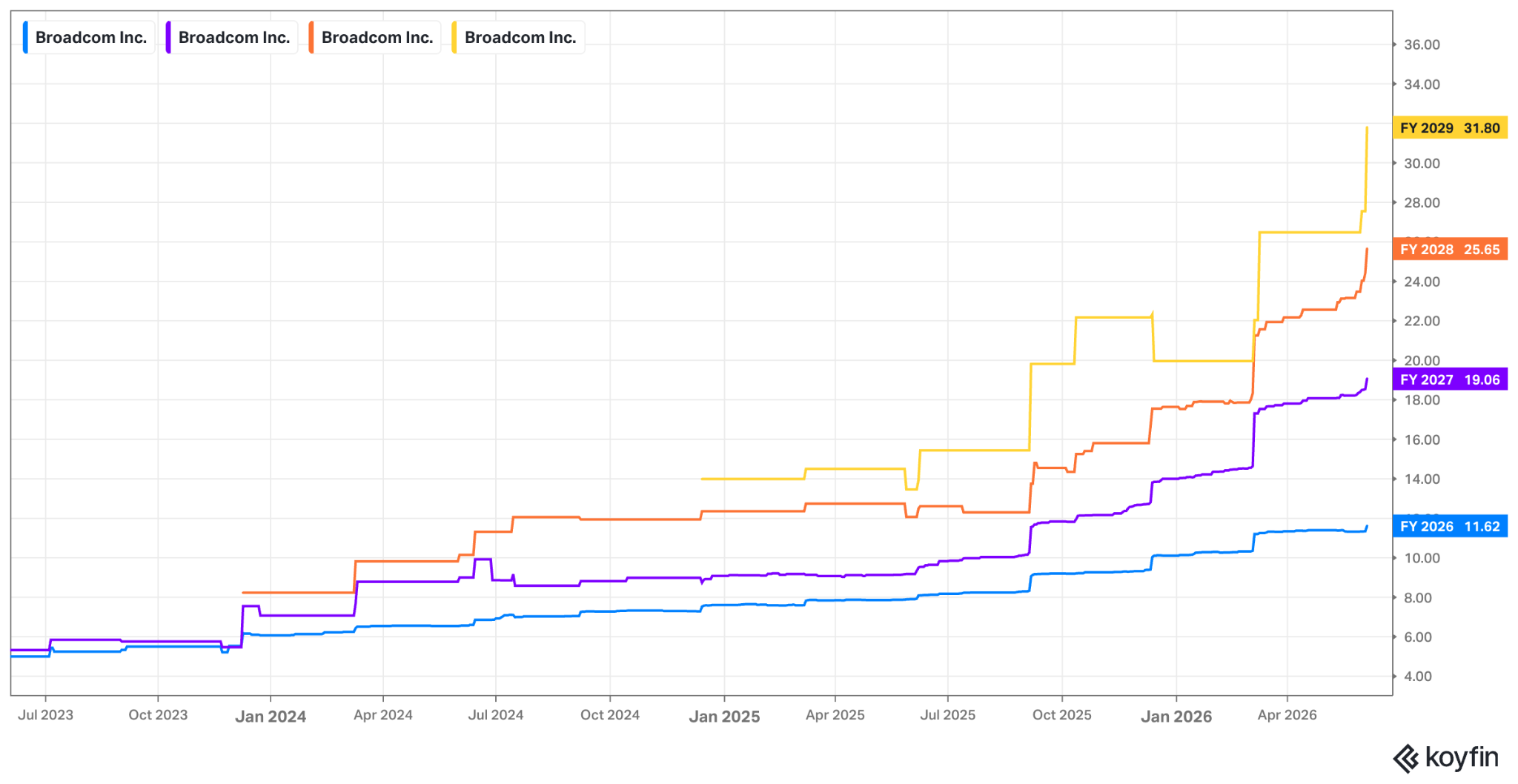

For 2027, they continue to see $100B+ in AI semiconductor revenue, representing 79% Y/Y growth. Many wanted Broadcom to raise this expectation, given all of the positive commentary surrounding AI demand. I think they were smart not to. Cycle health can change very quickly, and Broadcom shouldn’t get too excited about what it's currently seeing. Growth guidance is already robust and there’s no reason to give another update for a period requiring them to look out as much as 18 months. Leadership explicitly hinted at materially surpassing $100B as a likely outcome, but is waiting to see the periods develop. That makes a ton of sense to me. For 2028, they see “continued revenue growth.”

AVGO trades for 31x forward EPS and 17x forward sales. EPS is expected to grow by 70% this year and by 64% next year.

f. Call & Release

Semiconductor Solutions – Custom Accelerators/XPUs:

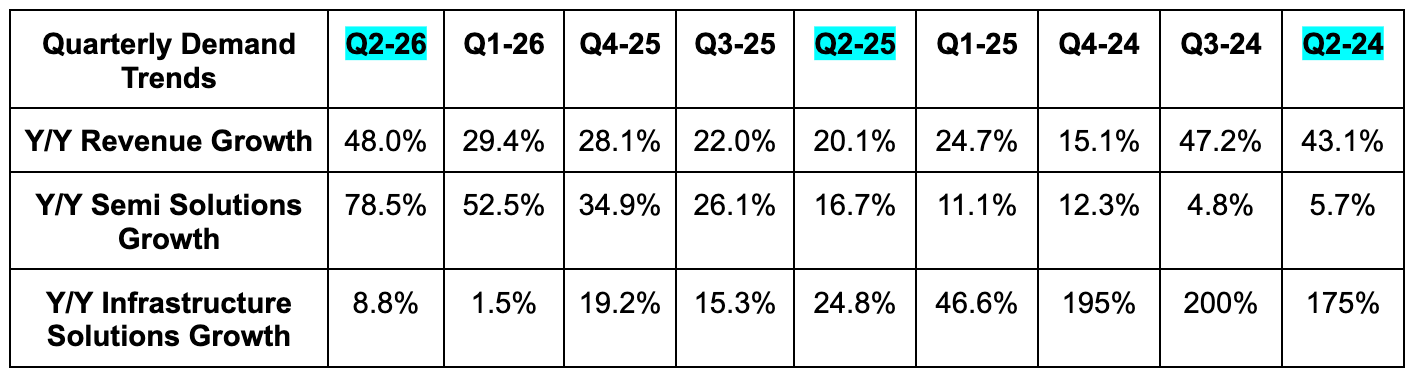

The AI portion of this bucket continues to go bananas. It grew by roughly 140% Y/Y to reach about $6.5B and drove most of the company’s overall revenue outperformance. Demand was called “insatiable” and it looks like that will remain the case in the coming quarters. Overall AI bookings crossed $30B this quarter to nearly triple the revenue number. This is directly informing the view that Broadcom AI semiconductor solutions revenue will double during the second half of the year when compared to the first half. And, as mentioned above, they expect full year AI semiconductor revenue to rise 180% Y/Y to $56B. The engine keeps on hummin’.

In terms of specific customers, Anthropic is on track to ramp from 1 gigawatt of TPU-based compute (created in partnership with Google) this year to 5 gigawatts next year. Their OpenAI relationship is also progressing nicely, as they're on track to reach scaled production of the chip they’re working on together by late 2026. This will scale to 1.3 gigawatts in 2027 before reaching the 10 gigawatt cumulative milestone by 2029. Broadcom and Meta are also on track to deploy 3 gigawatts by the end of 2028, with that starting next summer.

The most interesting customer update was Google. This past April, the two signed an expanded agreement to co-develop new generations of Google’s TPU-based compute and to work together on AI networking as well. This agreement was called “very substantial” but the relationship still has some investors worried. That’s because Alphabet plans to “diversify their sources” within the TPU supply chain to perhaps use competitors such as Marvell and MediaTek for part of this project. Leadership made it sound like this was an inevitable byproduct of explosive growth and Alphabet needing to find other partners to help them build more chips, but there are still mumblings of market share deterioration that followed this report.

- Broadcom expects its “other two customers” to begin accepting shipments late this year, with meaningful ramps next year. They have a $6B backlog between these two companies.

- Broadcom formed the AI XPV Platform with Apollo and Blackstone during the quarter. The purpose of this is to deliver 20 gigawatts of compute over the next three years, using world-class balance sheets and resources from these partners to help fund the build-out.

Leadership was asked about the broadening out in model training and enterprise AI usage and if these things are creating new opportunities outside of the massive customers AVGO serves. The short answer is no. While more companies are now embracing this technology and popular new agents, all of that demand goes through the cloud and current consumer internet clients. The vast majority of token consumption is happening on these platforms, and Broadcom has no interest in seeking other, smaller customer relationships.

For non-AI semi solutions, the company is enjoying a notable bottoming in demand levels across end markets. Revenue was $4.2B, which was up 6% Y/Y and coincided with strong bookings growth ($6B+) that “offers a clear indication the company is on the path towards a full cyclical recovery.”

Semiconductor Solutions – Networking:

Broadcom feels that it’s a full technological generation ahead of the competition in AI networking. This is true for scale-up (more compute within the same rack) and scale-out (connecting more racks), where its Tomahawk 6 switch leads as the processing throughput and latency specialist. It’s also true for scale across (connecting more data centers), where Broadcom’s Jericho switches provide memory bandwidth and routing capabilities beyond what Tomahawk can. While a lot of AVGO’s impressive networking demand began to pop-up within the XPU environments they support, that’s now broadening to general compute environments as well. That trend supported roughly 140% Y/Y growth to reach about $4.3B in total revenue for the segment. When combined with the semiconductor solutions AI business, total AI revenue rose by 143% Y/Y to reach $10.8B.

Infrastructure Software:

Bookings for this segment were called strong, while ARR rose by 17% Y/Y compared to 19% last quarter and “double-digit” growth last year. The company recently debuted the updated VMWare Cloud Foundation 9.1, which is expected to deliver better infrastructure utilization efficiency, enterprise AI inference support and security too. The customer response was called “extremely strong.” Finally, they’re seeing zero impact from AI-related disruption on this software portion of the business. Renewals are good, the backlog is healthy and steady growth is the expectation.

More Notes:

- Following NVIDIA CEO Jensen Huang's remarks on rising revenue potential per gigawatt of compute, leadership was asked about this on Broadcom's call. CEO Hock Tan said they're not seeing this, and don't expect to in the future. Growth will be led by volume of gigawatt deployment, rather than monetizing pieces of those deployments more aggressively.

g. Take

Subscribe below to read my take on Broadcom and the quarter. Also read a full Rubrik review and detailed earnings reviews from this season on 35 other companies like Meta, Snowflake, Spotify, and Lemonade.