Table of Contents

1. On Holding (ONON) – Earnings Review

ONON is a premium athletic shoe and clothing company quickly gaining ground against Nike and Adidas. They have several popular running shoe products, with 8 of them contributing at least 5% of overall revenue. This is not a one-trick pony. In terms of sports, they’re popular for runners and in tennis, with expansion into more activities going well. It’s founder-led, with a focus on operational excellence and creating the next category trends through impactful, focused innovation – like LightSpray. As a reminder, LightSpray is On Running’s new automated manufacturing technique. It uses robotic arms to (as the name indicates) spray a light material right onto the sole of the shoe to form a single-piece, laceless model. Impressively, it takes a robot 3 minutes to make a shoe and is comparatively quite cheap. That combination should be fantastic for On’s long-term margin ceiling.

a. Key Points

- Strong quarter for rising brand awareness and market share.

- Demand was healthy across all regions.

- LightSpray is expected to scale in 2026.

- 2026 should be another year of fast growth with strong margins.

b. Demand

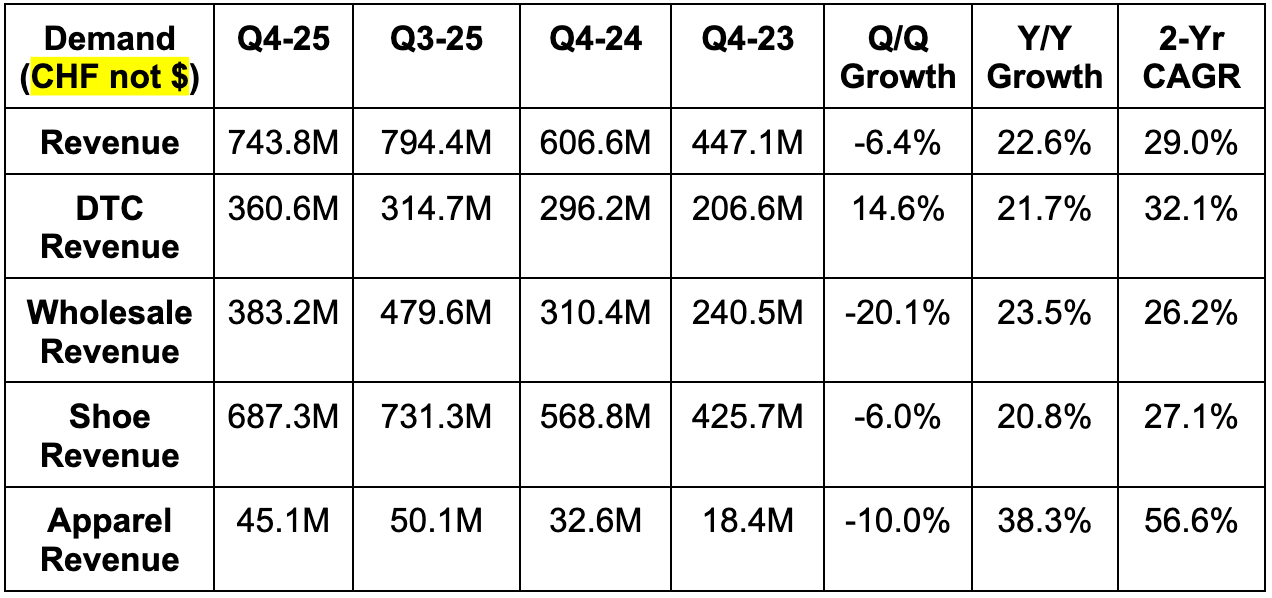

- Beat revenue estimates by 2.2%.

- Wholesale revenue beat estimates by 6.5%.

- Direct-to-consumer (DTC) revenue missed estimates by 1%.

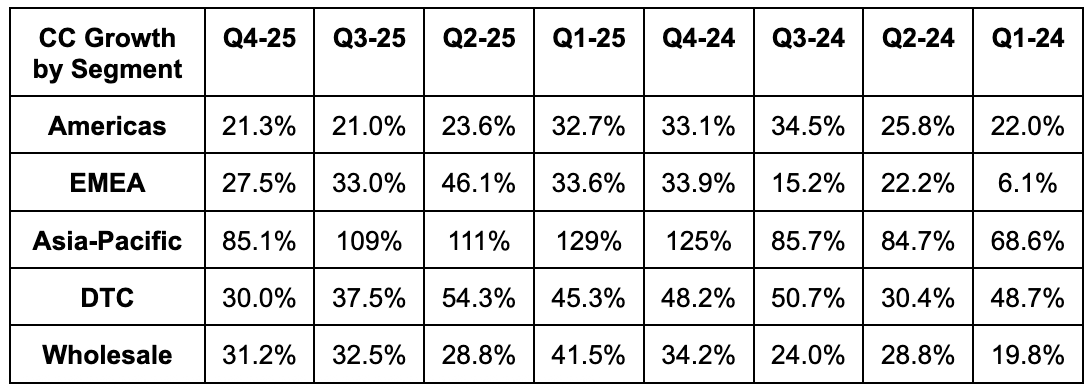

- By geography, Americas revenue beat by 1%, Europe, Middle East & Africa (EMEA) revenue beat by 6% and Asia-Pacific (APAC) revenue beat by 4%.

- Revenue from shoes beat CHF 667M estimates by 3%; revenue from apparel missed CHF 47M estimates by CHF 2M; revenue from accessories missed CHF 13M estimates by CHF 2M.

- 2025 sales from accessories and apparel rose from 5.1% of revenue to 7.0% Y/Y. Good progress.

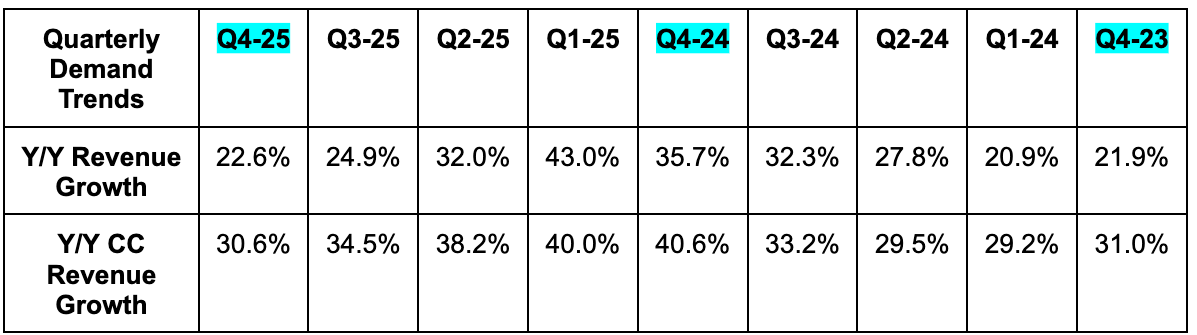

- Good to see year-over-year constant currency (CC) growth comps get seven points harder sequentially, while growth only slowed by four points sequentially.

- For the full year, CC revenue growth accelerated from 33.2% to 35.6%.

- Growth within their 15-35 year-old demographic was faster than any other.

There is no single country or two to call out as a standout. Why? Because every region for the company was strong. From China, where in-store holiday traffic doubled Y/Y... to every part of Europe... to Latin America, North America, and everywhere else... this brand is rocking.

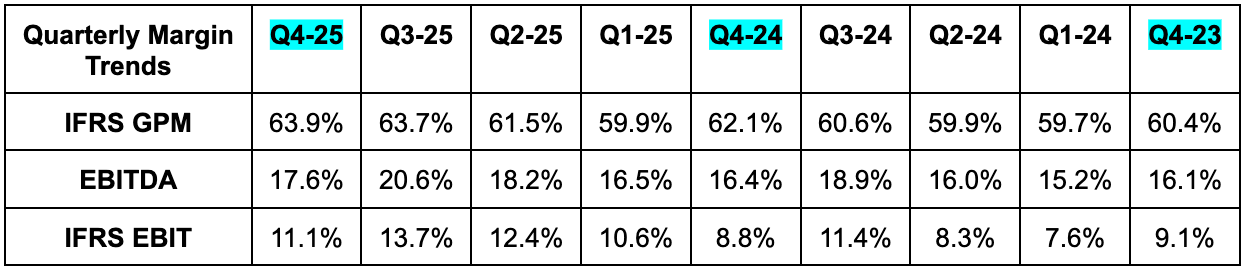

c. Profits & Margins

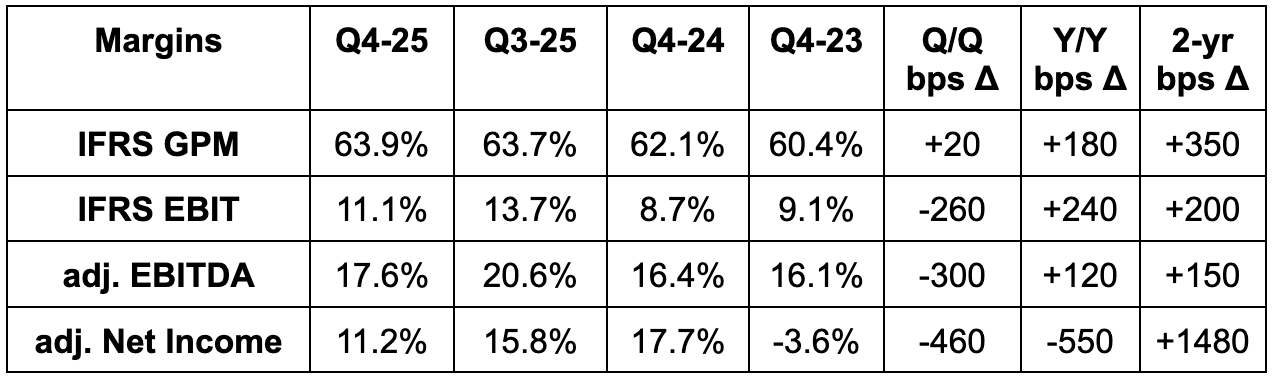

- Beat 62.7% GPM estimates by 120 basis points (bps; 1 basis point = 0.01%).

- Beat EBITDA estimates by 13.4%.

- Selling, general, and administrative expenses rose by 21.3% Y/Y to modestly trail revenue growth. While the company did enjoy some leverage here, that's not currently the main focus. They remain in growth mode and are motivated to plow operating profit back into the business to support innovation, brand awareness, and scaling. Margins could easily be expanding even more quickly if they wanted them to be.

- Beat CHF 0.21 EPS estimates by CHF 0.04.

- EPS fell from CHF 0.33 to CHF 0.25 Y/Y. This metric is heavily influenced by volatile foreign exchange (FX) movements. This quarter, that line item lowered net income by CHF 13M vs. a CHF 38M benefit last year.

GPM continues to benefit from this company's strict approach to full-price sales, ongoing supply chain, operational efficiencies, and healthy demand. Additionally, while foreign exchange is currently slowing down revenue quite a bit, the net impact on GPM is actually positive, and that's modestly amplifying the leverage we're currently seeing.

The company is already well beyond the 2026 targets it set at its 2023 investor day, which called for a 60%+ GPM and an 18%+ EBITDA margin.

d. Balance Sheet

- CHF 1.02B cash & equivalents.

- Net working capital grew 14.3% to CHF 570.3 million.

- Inventory was roughly flat Y/Y.

- They are very comfortable with inventory quality & quantity. The company told investors a lot of it includes highly anticipated product launches coming in 2026 that they're confident will rapidly sell out. They built up inventory ahead of these debuts to make sure they could take advantage of the excitement.

- No debt.

- 1.6% Y/Y dilution.

- Capital expenditures were 3.8% of sales vs. 3.3% Y/Y in Q4. The increase was to support store expansion, supply chain optimizations, and their roadmap.

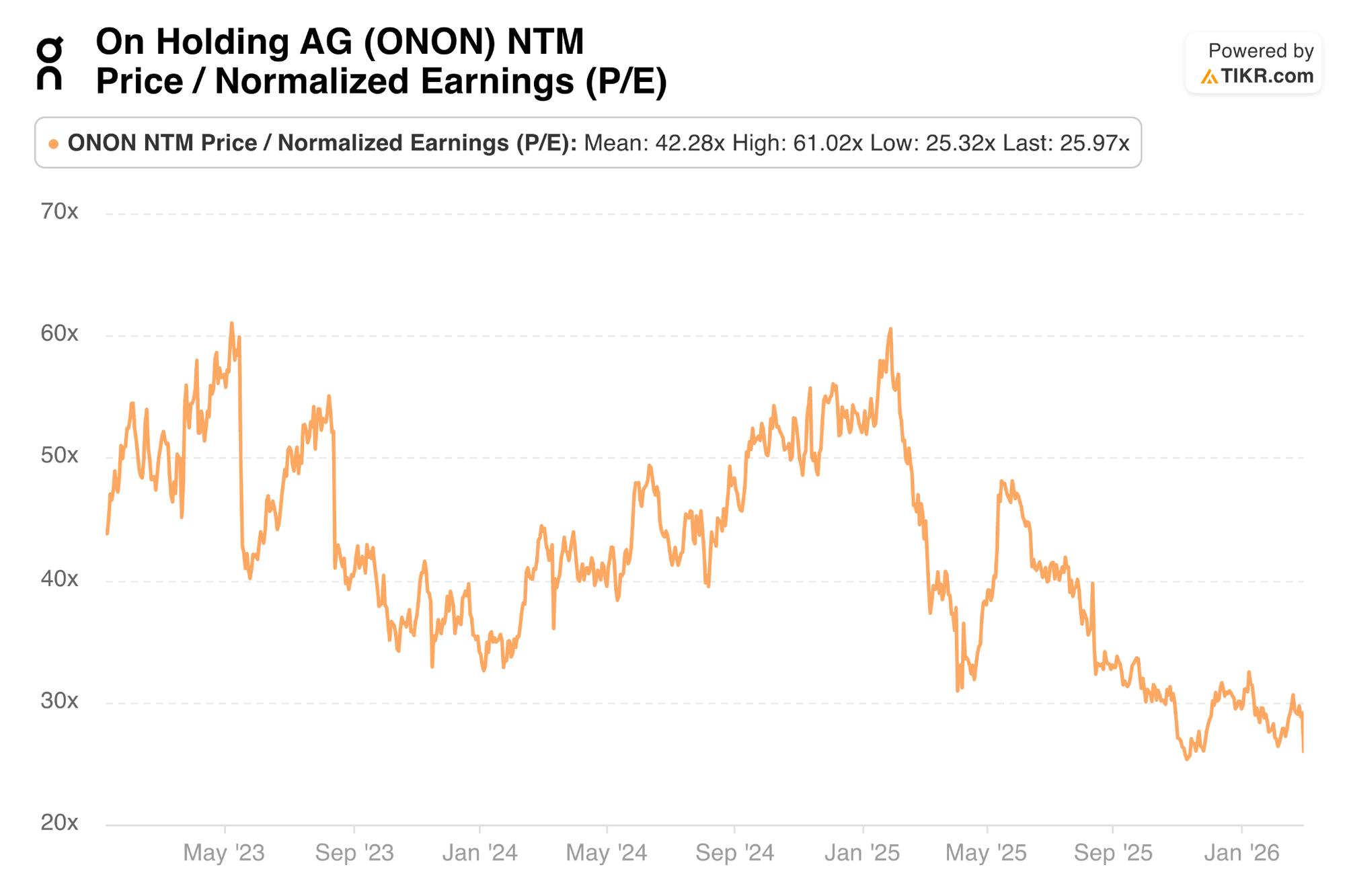

e. Guidance & Valuation

The revenue guidance from On Holding for 2026 represents just 14% Y/Y growth. This includes a massive 9-point+ FX headwind, with constant currency (CC) growth expected to be 23%+. This compares to 25% CC growth estimates. It also guided to a 63%+ GPM, which is at least 60 basis points better than consensus expectations. This is helped by the same structural factors we discussed in the margin section, again with a bit of added juice from foreign exchange trends. Furthermore, GPM guidance includes additional tariff impacts and doesn't consider any potential relief from the 20% rate falling to 15% as part of recent policy developments. If that were to come to fruition, there would be more margin upside.

Next, its 18.8% EBITDA margin guide met consensus expectations.

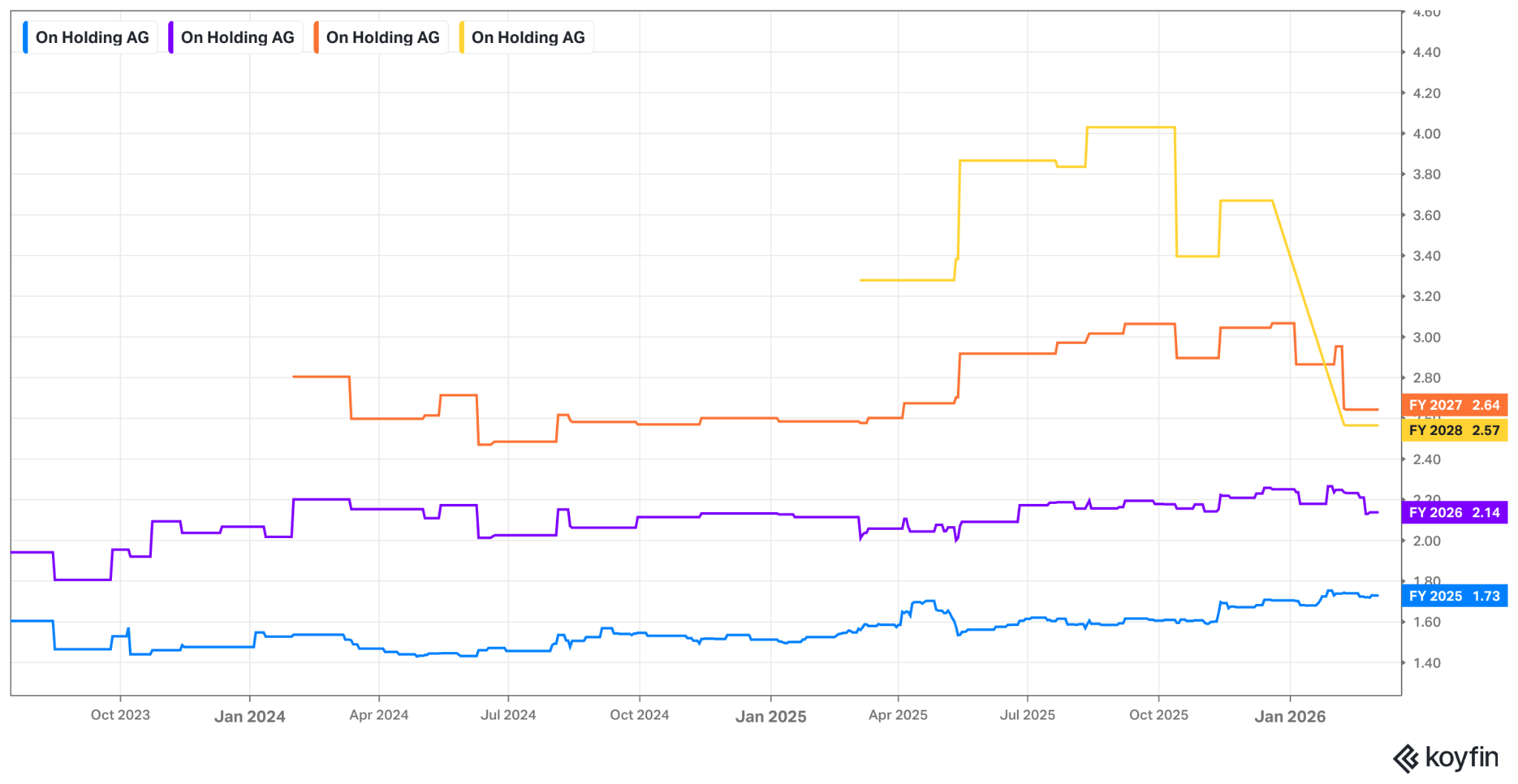

As a reminder, ONON guided to a 26%+ constant currency revenue CAGR from 2023 to 2026. The minimum revenue guidance they offered for 2026 represents a three-year CAGR of 30.5%. And if history is any indication, barring a macroeconomic collapse, they will do much better than this initial annual outlook.

Part of the negative earnings reaction was probably related to the lack of raised constant currency growth guidance for 2026. They had already given investors 23%+ for 2026 during the Q3 call. So this was a reiteration. I think it's important to recognize they're reiterating the same growth rate, despite the 2025 base now being higher than they originally expected on the Q3 call. They were rightfully quick to point that out because it means the CC revenue dollar guide for 2026 was raised.

f. Call & Release

Why They’re Winning – Structural Tailwinds:

Leadership believes three structural tailwinds continue to power the firm's impressive and consistent profitable compounding. We talk about the first two quite a bit. They continue to steadily grow global brand awareness, with that now reaching 30% vs. 20% Y/Y. And they also continue to boost their direct-to-consumer retail store footprint. The company now has 67 retail stores around the world compared to 49 Y/Y. Much more on how these doors are performing later. These two items, as we often talk about, work wonders in buffering the cyclicality that its space naturally features. Other companies like Lululemon and Nike that are more mature in their growth curves cannot use more stores and extended customer awareness to offset inevitable pockets of weaker consumer spending. ONON can.

The third structural tailwind leadership talked about is something we don't discuss very frequently. The team sees cultural tastes shifting from "self-indulgent categories" to a philosophy that embraces "health is the new wealth." They think longevity is replacing material possessions as the main gauge of success, and they think their brand is perfectly positioned for that reality. ONON caters to athletes looking for a premium experience and a brand they know will perform well for them while looking good on them. It’s this premium, trusted brand that enables ONON to discount less intensely than their peers while outperforming on internal volume expectations during the holiday season. It's this fixation on premium brand reputation that paves the way for their GPM being so impressive compared to public market peers. And it's the premium brand that allows collaborations with brands like Loewe to easily sell shoes at a $750 price point.

Why They’re Winning – Part of the Conversation:

ONON also thinks their pervasive presence in pop culture is a big part of their success. This is really brought to life by their partnerships with athletes like Hellen Obiri (famous marathon runner) and Ben Shelton, as well as collaborations with world-famous celebrities like Zendaya, FKA Twigs, and others. With Zendaya specifically, leadership spoke excitedly about "shifting from a partnership to a true co-creation," with the sides collaborating on a brand new product expected to launch this year.

Why They’re Winning – Great DTC Stores & Products to Capture the Compelling Opportunity:

As briefly mentioned, accessories and apparel are comfortably outgrowing the core business. That's happening in every single region and every single channel. Tennis was the fastest-growing sport within the apparel segment with Iga Swiatek winning Wimbledon in the company's swag. I also couldn't help but notice this company's logo all over Olympic athletes during the Winter Games in Italy this past month.

- They just signed the youngest world number one ever for the sport of paddle. His name is Arturo Coello and he will be a co-creator for future apparel collaborations.

- ONON is leaning into female-focused innovations across fabrics and silhouettes to capture more momentum on that side of the apparel business.

- The percentage of new customers making their first ONON purchase in the apparel category rose from 6% to 10% of total Y/Y.

ONON is leaning into bigger stores, with openings in 2025 being 40% larger than its existing base. These layouts have more product assortment and are designed to be more experiential and engaging than ONON’s older store formats. So far, this change is already driving 20% better productivity, and it's still early.

To tie the conversation on apparel and DTC stores together, these physical locations already enjoy 15% of total sales from apparel, which is more than double the overall business. That's exactly what the company wants to see. Apparel has turned into a powerful lever for basket size, customer frequency, store productivity and lifetime value gains.

- 60% of apparel sales are through DTC channels, compared to 40% for ONON as a whole.

- Its new store in Tokyo became one of its top 10 most productive locations in only a few months. Its Seoul location did as well.

- They think higher DTC market share means better customer relationships (they're right), which should allow them to personalize experiences and enhance engagement.

Why They’re Winning – Superior Innovation:

Financials are structurally benefiting from its cutting-edge and resonating innovation engine. Their Zurich lab houses the only advanced foam competence center outside of Asia. This gives the company a layer of vertical innovation that fuels more flexible product roadmaps and faster iterations to unlock truly exciting developments. For example, Cloudsurfer 3 will use these advanced materials to get 15% lighter and 20% softer vs. the Cloudsurfer 2.

And while that's compelling, LightSpray manufacturing technology is the star of the innovation show right now. Its ability to cut hundreds of steps in the manufacturing process vastly enhances scalability and creates a far more efficient assembly process. Soft launches of this technology performed extremely well, as Hellen Obiri broke a 22-year-old NYC marathon record wearing it to greatly help with the buzz. While 2025 was the year of beginning the manufacturing process and creating a few thousand units to test and learn, 2026 will be the year of scaling from thousands to millions... first with its Cloudmonster franchise. They just opened a facility in South Korea last week, which 30X'd LightSpray production capacity in preparation for an aggressive ramp.

Wholesale and the responsible pursuit of sustainable growth:

ONON is in just 50% of the stores for its existing wholesale partners. It has a 2x opportunity within that piece of business alone, which doesn't even consider adding more apparel and accessories to these relationships. It could be growing these doors and new wholesale partners a lot more rapidly if it wanted to. It just doesn't. It's more interested in preserving brand quality than making sure its logo shows up in every single department store across America. They aren't Nike and they don't want to be Nike. They want to be more exclusive. That means intentionally slowing down wholesale growth and controlling which partners get access to your goods.

Regardless of this, their 2026 wholesale order book looks very strong, and they expect brisk expansion for wholesale throughout 2026. It's just worth noting that this health could look even better if this company were more short-sighted. I think it's a very good thing they're not.

Investor Day:

They will likely host another investor day early next year to set new three-year targets. As a reminder, they'll welcome their new CFO (Frank Sluis) in May, so they want time to plan out multi-year goals and strategies.