A few notes on the data shown below.

- 2026 Consensus Estimate Trend measures the trailing 12-month change in analyst EPS expectations for 2026.

- PEG ratio takes the forward P/E and divides by the 2-year forward EPS compounded annual growth rate (CAGR).

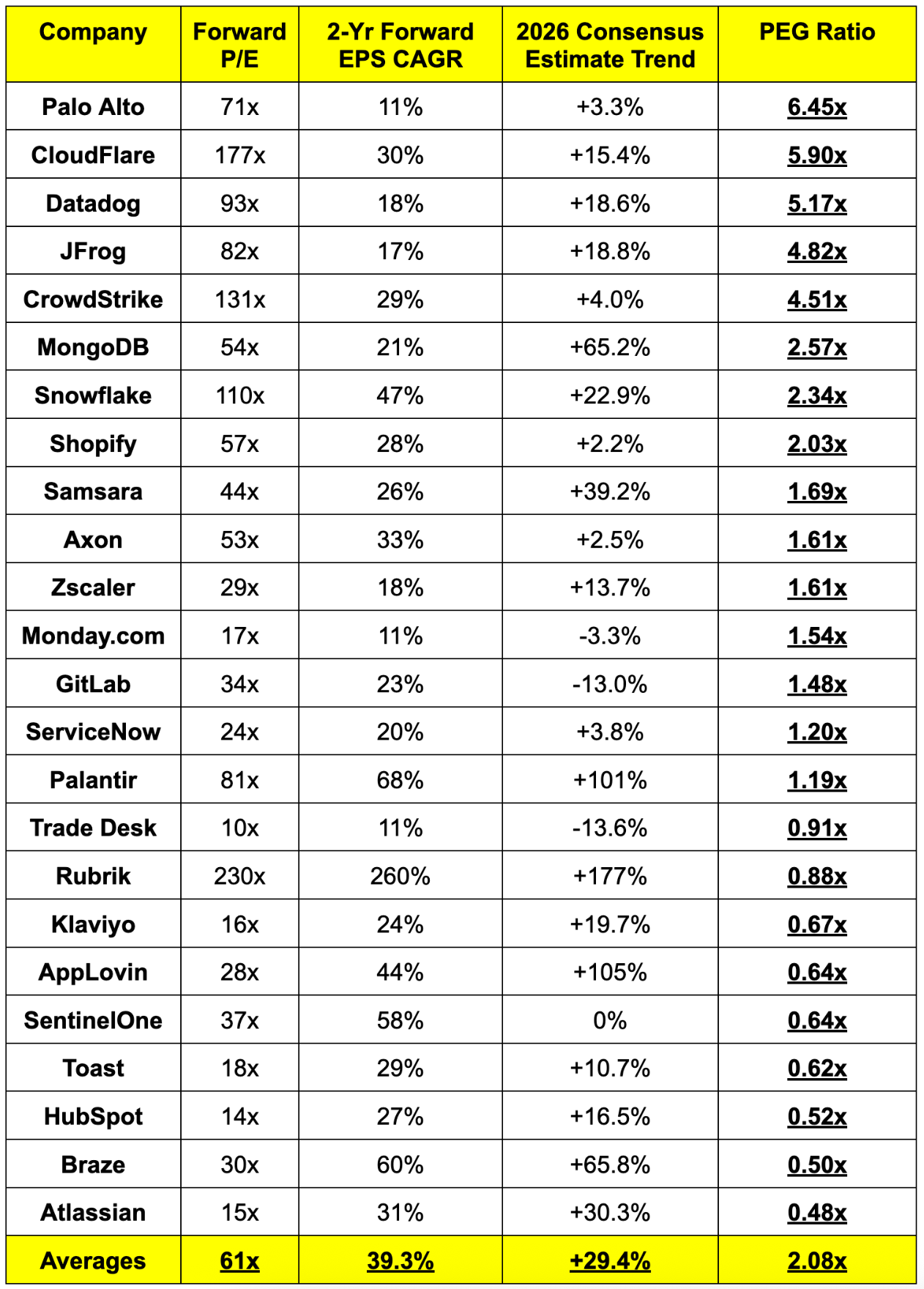

a. High Growth Enterprise Software

Quick Takeaways:

- Don't let anyone tell you software names will never get a premium again. A few of these are wildly expensive.

- Surprised to see how expensive JFrog & Palo Alto are.

- Palantir continues to look more reasonable. The sales multiple is still near 35x, which is obviously very lofty. But their margins are so good and their growth is so fast that this net income lens makes them look modestly priced.

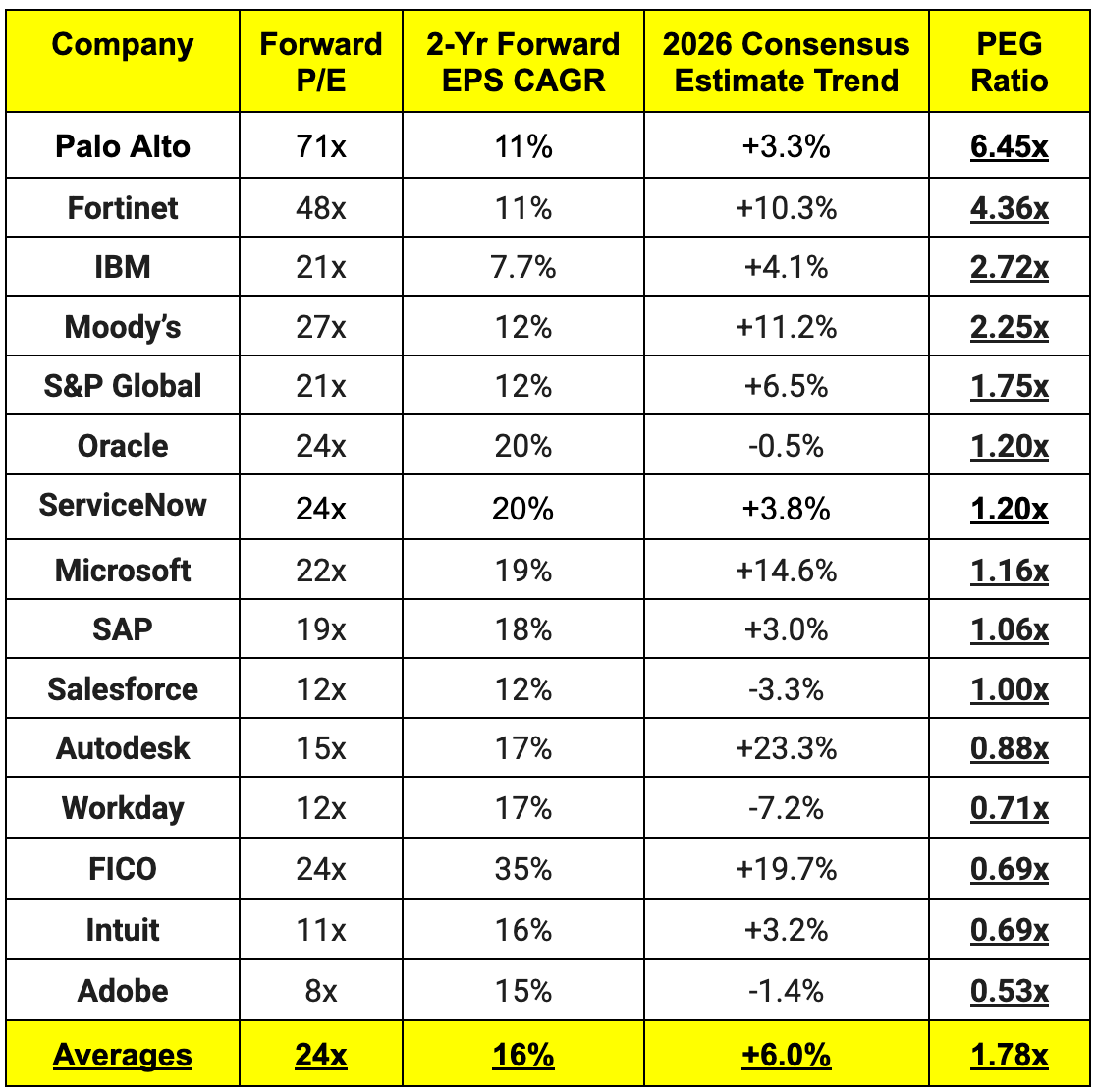

b. Mature Growth Enterprise Software

Quick Notes:

- I included Palo Alto and ServiceNow in this group too, as I think both are hybrids that belong here and with the fast growth enterprise software companies.

- I think this really paints the picture of which companies the market thinks are most vulnerable to AI disruption. Cybersecurity continues to be seen as a safe haven. Most app layer software businesses continue to be seen as fragile.

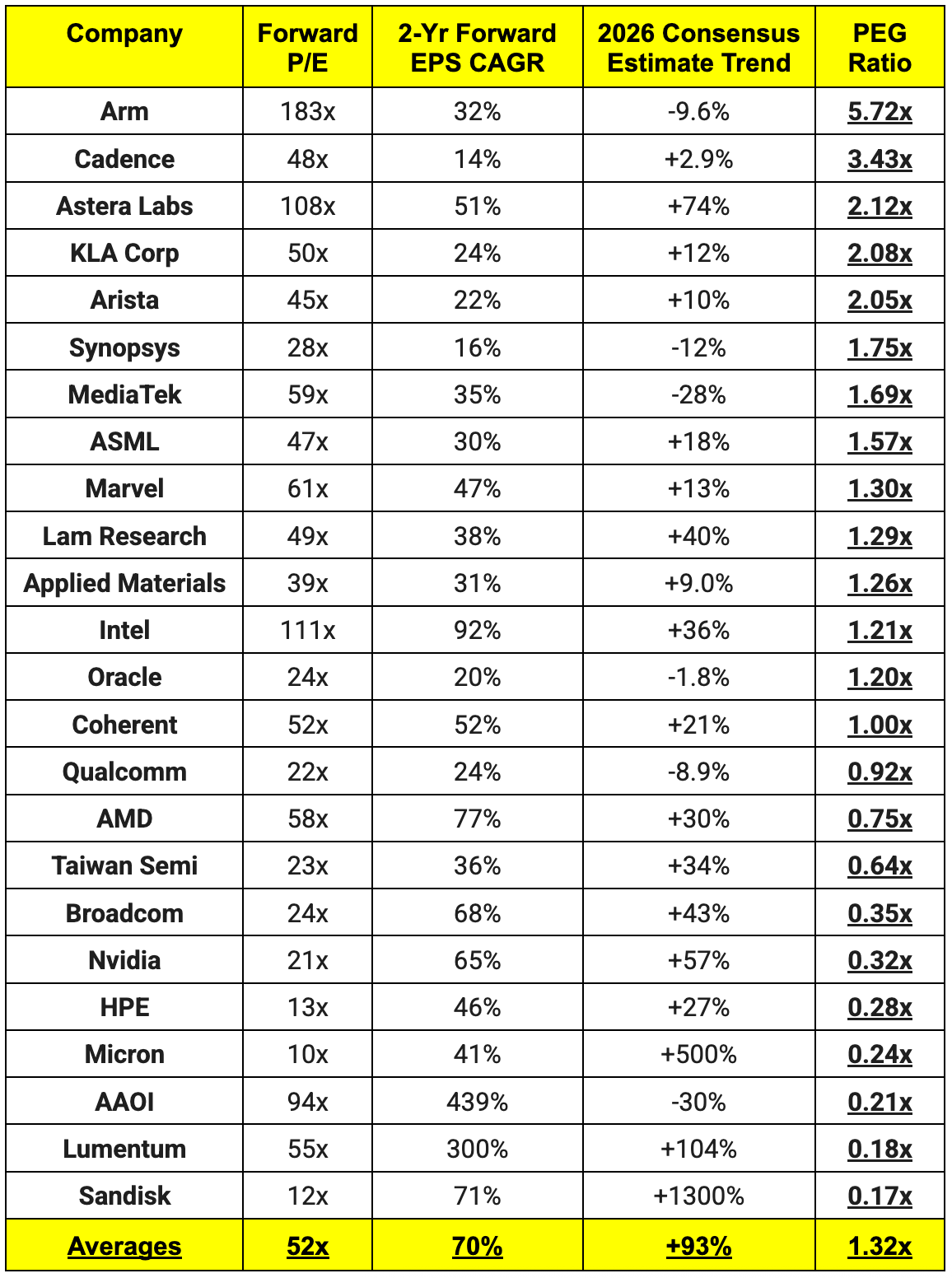

c. AI Infrastructure

Quick takeaway – Shortages and strong demand are creating a durable cocktail of historic pricing power for a lot of these companies. While a sales multiple view would make them look a lot more expensive, fantastic margins and strong growth are generating enough net income to make them look very cheap from this point of view. That will likely continue for as long as this AI infrastructure supercycle keeps rocking. All of the CapEx commentary we've gotten from mega-caps so far points to a healthy demand environment in 2027.

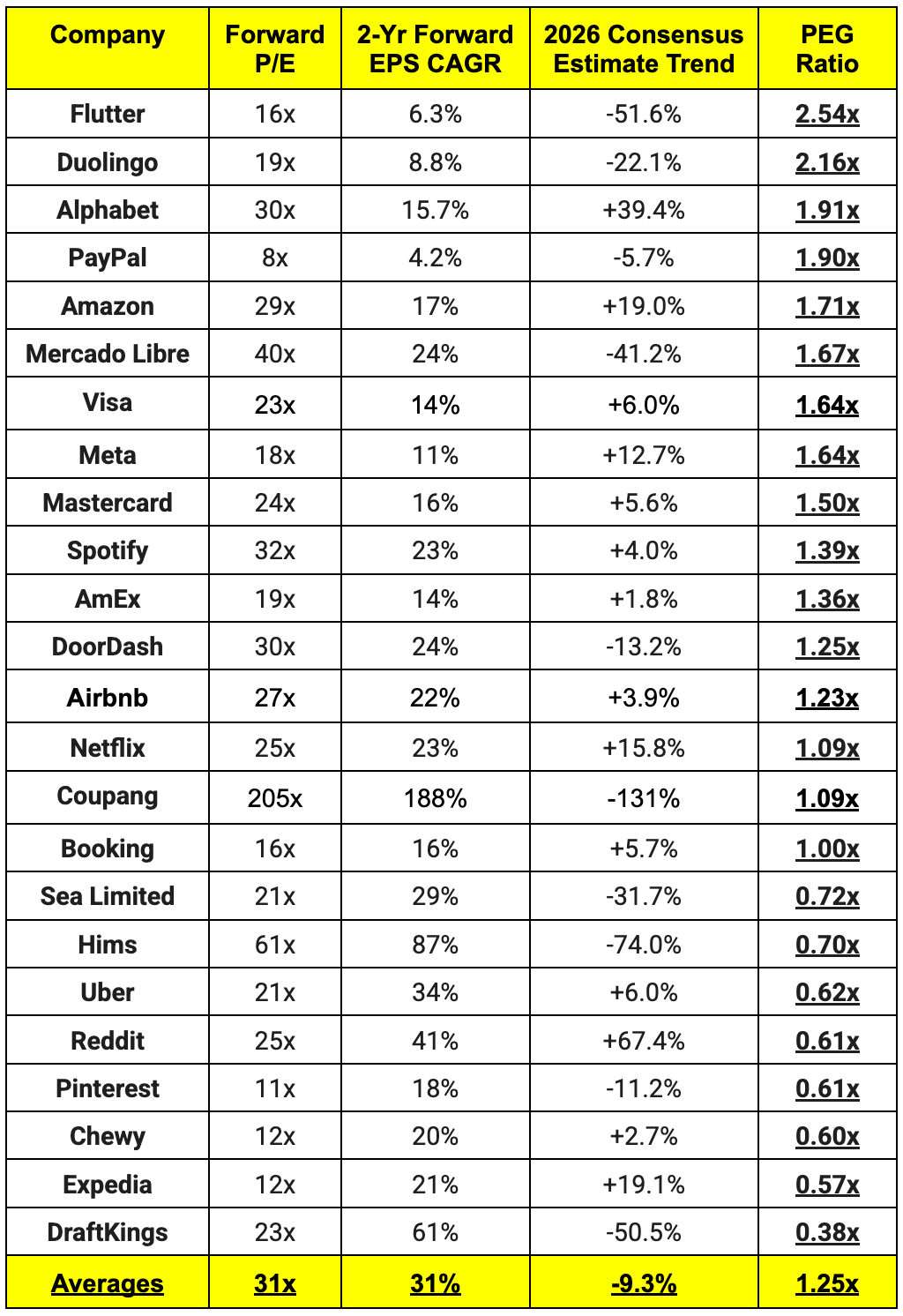

d. Consumer Internet

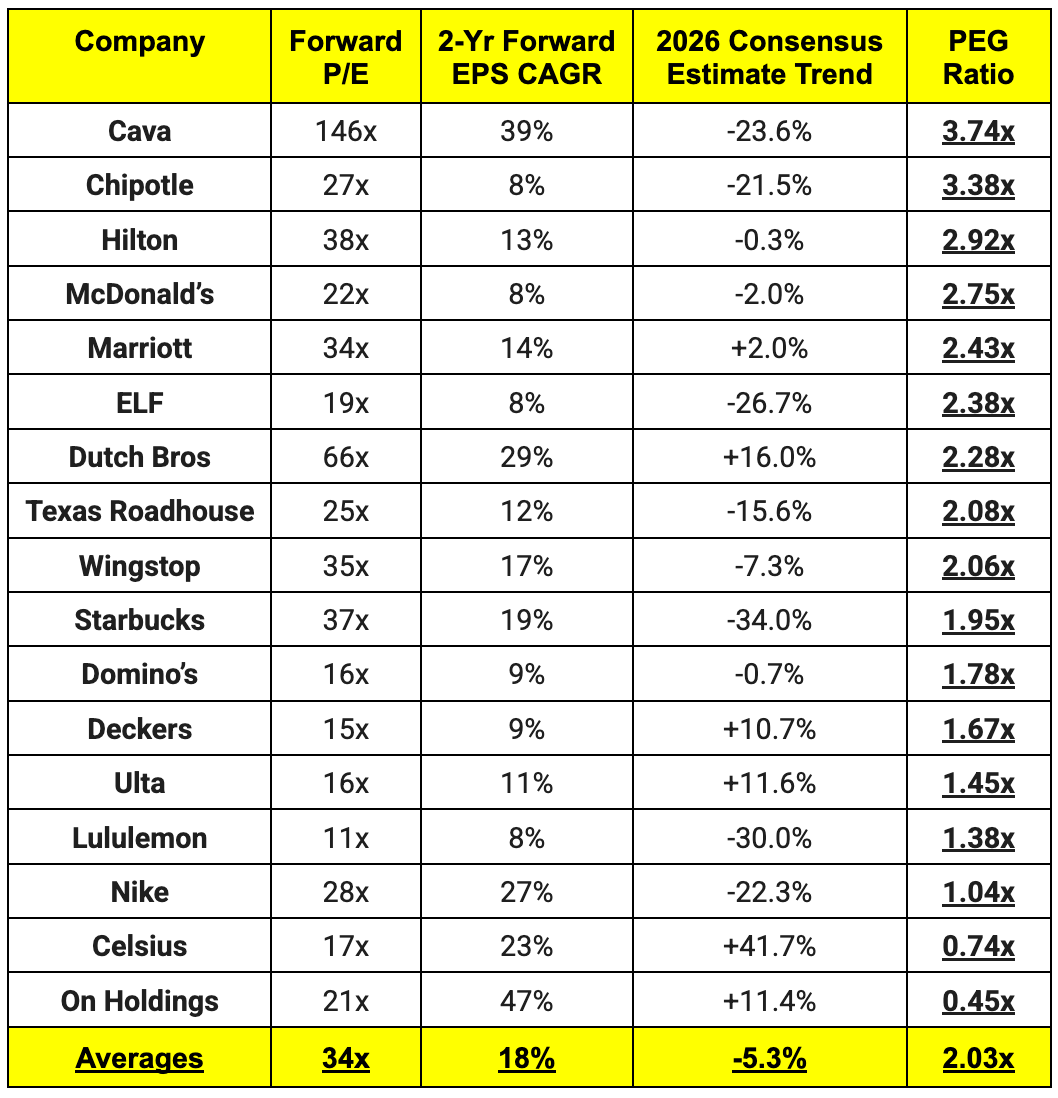

e. Quick Service, Apparel & Hotels

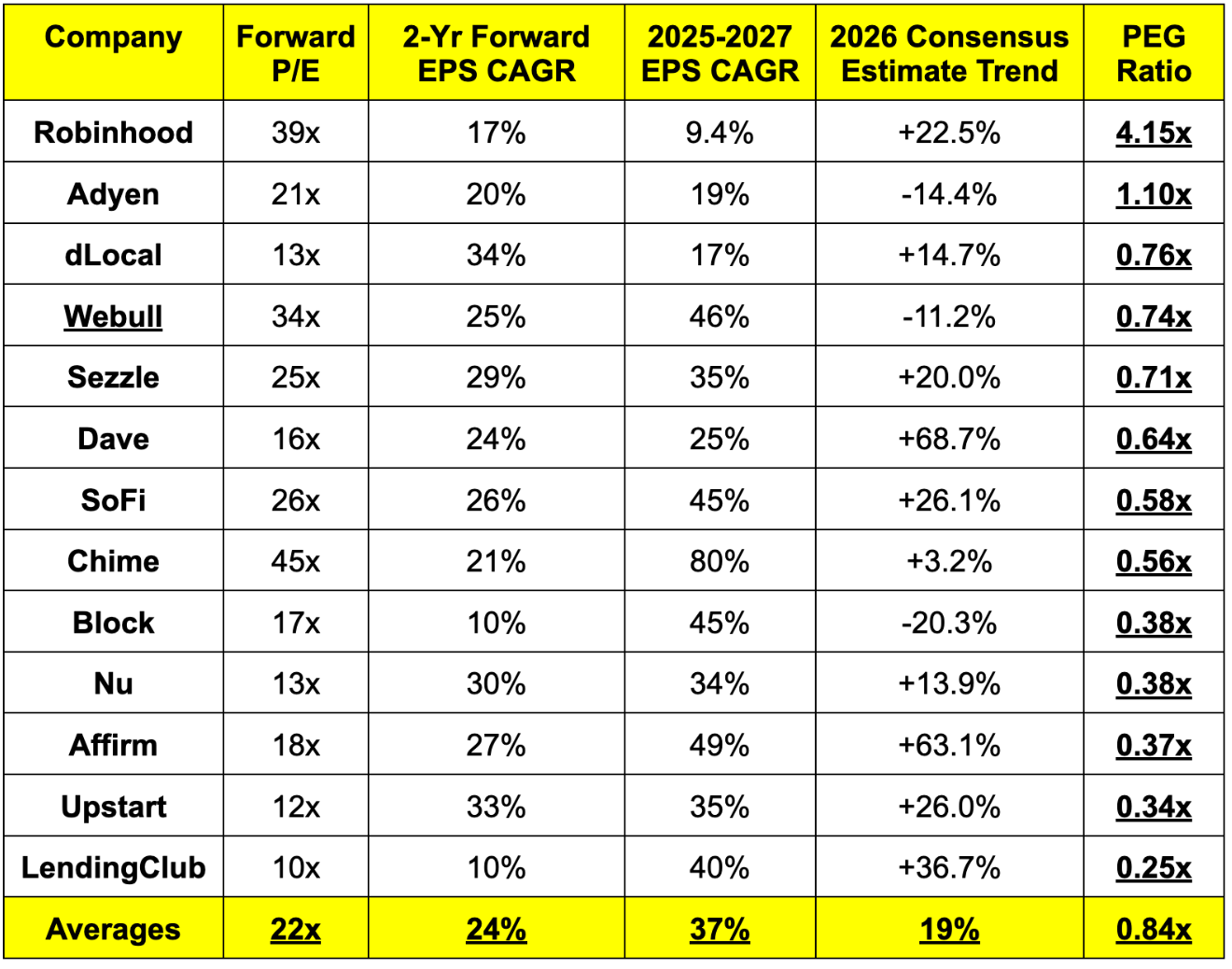

f. Fintech

Quick takeaway – Outside of Robinhood, profit growth for this cohort is discounted more heavily here than for pretty much any other. It's tied to credit & balance sheet risks, but still notable.

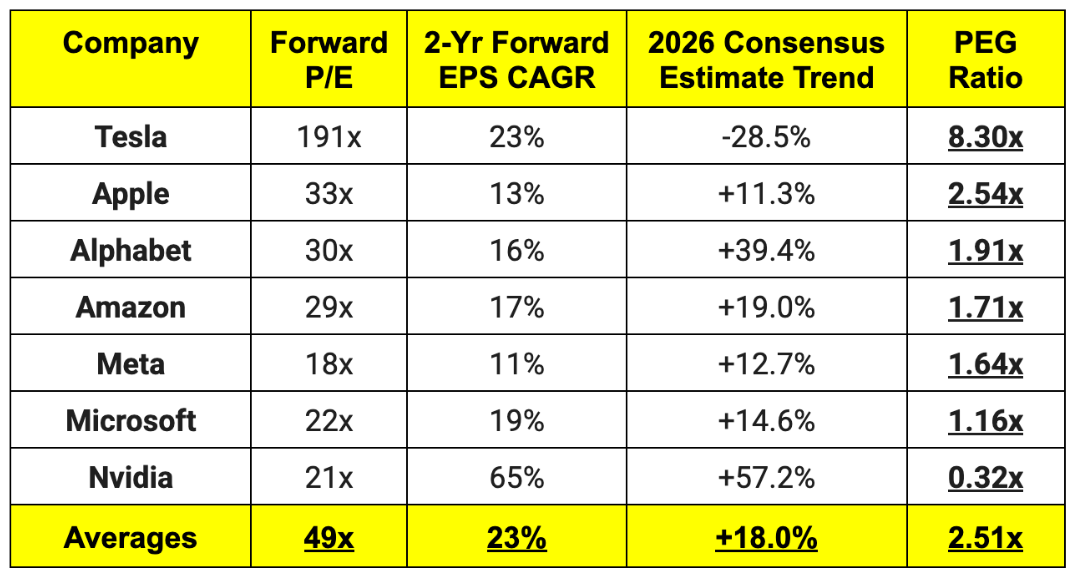

g. "Mag7"