Recent reviews and content published this season:

- Axon Deep Dive.

- Cloudflare Earnings Review.

- Robinhood & Shopify Earnings Reviews.

- Datadog Earnings Review.

- Palantir Earnings Review.

- AMD & PayPal Earnings Reviews.

- Alphabet & Uber Earnings Reviews.

- Hims Earnings Review.

- Amazon Earnings Review.

- My Current Portfolio & Performance.

- Access 8 other reviews from earlier in the earnings season.

1. Axon (AXON) – Earnings Review

I published an Axon Deep Dive a few weeks ago. This digs into the business model and investment case in intricate detail. It can be found here.

a. Key Points

- Strong outperformance driven by broad-based product strength.

- New products are ramping nicely.

- The AI Era Plan did $750M in 2025 bookings.

- 2028 financial targets are well ahead of sell-side consensus.

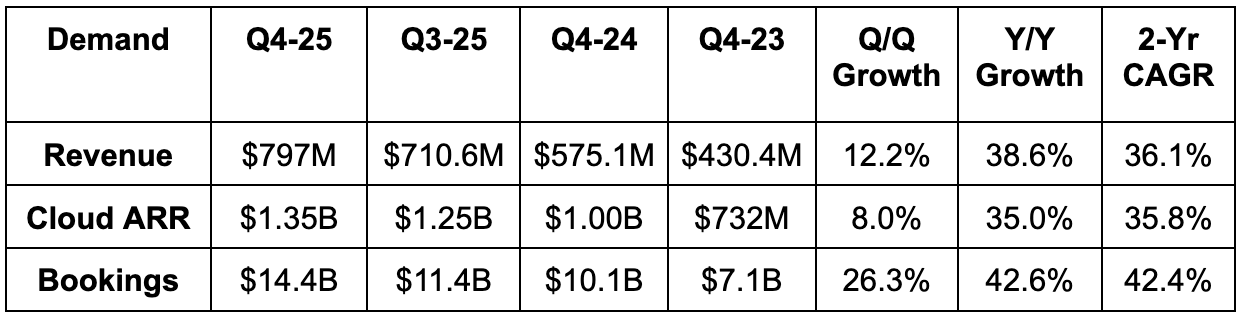

b. Demand

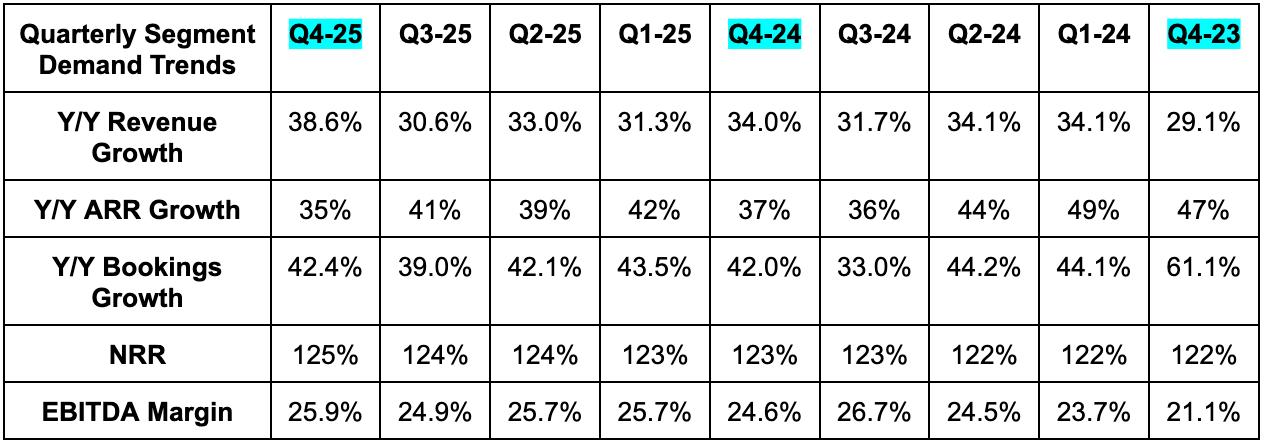

- Beat revenue estimates by 5.6% and beat guidance by 5.9%.

- Met annual recurring revenue (ARR) estimates.

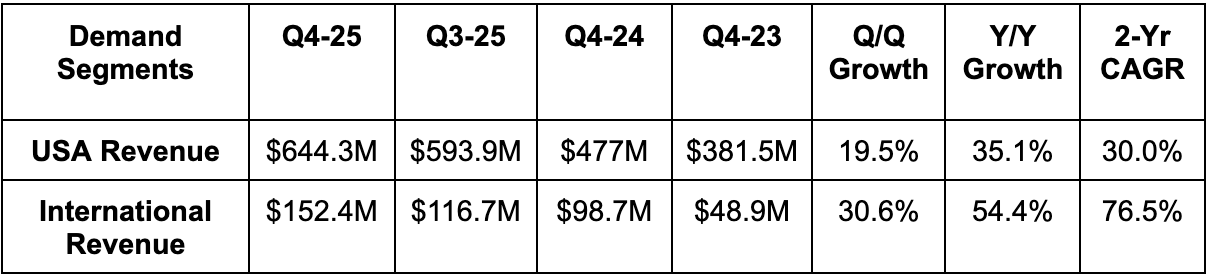

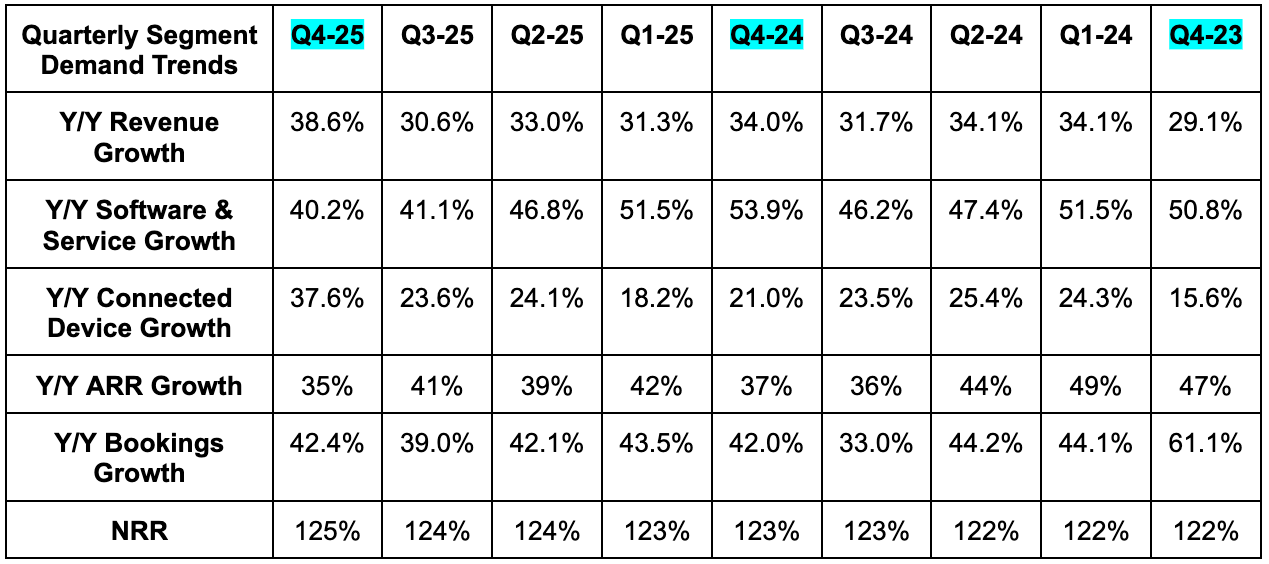

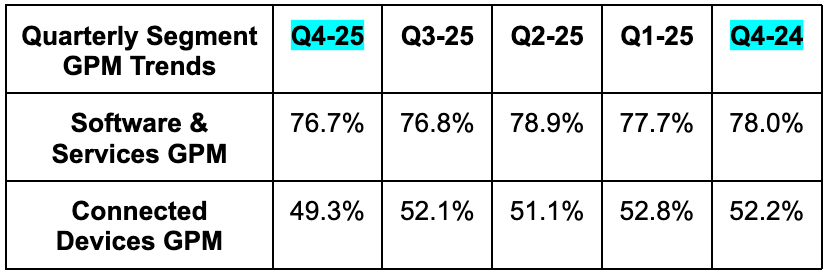

Software & services revenue was driven by ongoing adoption of more premium offerings. Connected devices revenue was powered by every single major product in that suite.

Axon delivered $7.4B in annual bookings for 2025. That represents 46% Y/Y growth and is significantly better than the high 30% growth guidance management offered on the Q3 call. That's especially notable because the previous guidance already included three quarters of registered data. That means this large beat was entirely driven by sizable Q4 outperformance. 46% Y/Y growth also follows a year in which they delivered 50% Y/Y growth. For added context, they were generating growth in the mid-20% range throughout 2022 and 2023. The acceleration has been remarkably strong and sustainable. And it's not expected to slow down anytime soon. On the call, Axon President Josh Isner called the strength "beginning of a trend." There are "no signs of this slowing down,” as the company enjoys fantastic traction across growth outlets including AI, drones, next-gen Automatic License Plate Readers (ALPR) and more.

30% Y/Y Taser growth marked a sharp acceleration compared to 17% growth last quarter. According to leadership, this isn't a matter of demand getting stronger sequentially. Demand was great last quarter and it's great this quarter. The sharp acceleration was due to some large deals slipping from Q3 to Q4, exactly like leadership told everyone. Interest in the product should remain strong and timing of contract closures will remain volatile.

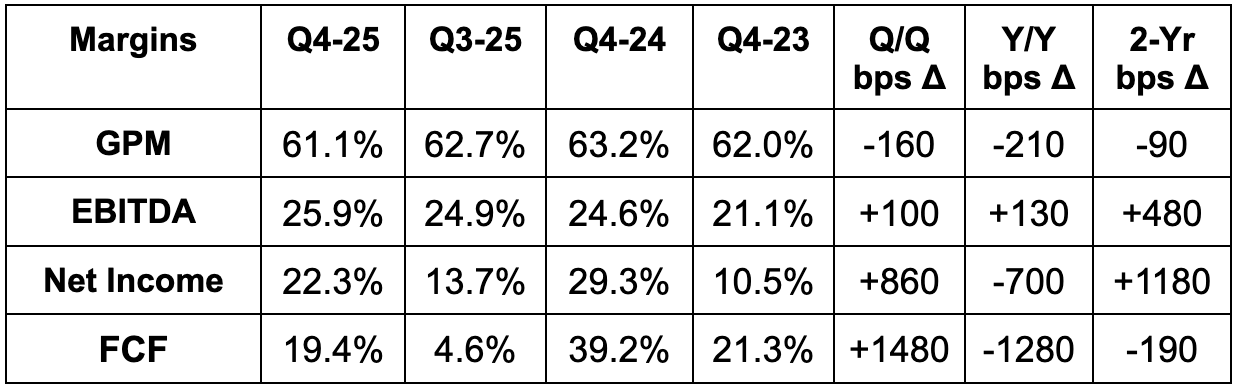

c. Profits & Margins

As discussed in the recent deep dive, a blend of payroll tax accounting and equity portfolio valuation swings both make net income and FCF noisy. This is the one rare case where EBITDA is actually the most useful metric among headline numbers.

- Missed 61.8% GPM estimates by 70 basis points (bps; 1 basis point = 0.01%).

- Tariffs and platform solutions growing as a percentage of connected devices both hurt GPM.

- Faster software & services revenue helped offset some of this pressure. Within the higher margin software & services segment, GPM fell from 78% to 76.7% Y/Y due to higher mix of professional services. The software portion continued to boast an 80%+ GPM.

- Axon expects GPM to gradually rise over time thanks to higher software mix, but this rise will not be linear.

- Beat EBITDA estimates by 13.8% and beat guidance by 14.4%.

- Adjusted OpEx fell to 38.2% of revenue vs. 39.2% Y/Y. Growth in OpEx on a dollar basis was driven by R&D as well as scaling go-to-market.

- EBITDA grew by 46% Y/Y.

- EBITDA margin outperformance vs. expectations and guidance was due mainly to the revenue beat.

- Beat $1.56 EPS estimates by $0.60 (noisy metric here).

- EPS rose 3% Y/Y from $2.08 to $2.15.

- Income tax effect was -$58.3M vs. -$12M for non-GAAP EPS during Q4. If the tax bill grew in line with profit, EPS would have risen by a little over 40%.

Free cash flow conversion fell materially during 2025 due to inventory investments and timing-related items. They expect to "catch up" on a lot of this missed FCF conversion in the coming quarters. Furthermore, leadership continues to target a 60% EBITDA to FCF conversion rate and they think the conversion rate will improve during 2026 and in the years beyond.

d. Balance Sheet

- $1.7B cash & equivalents.

- $1.8B convertible notes.

- 5.6% Y/Y dilution (partially M&A-driven).