Table of Contents

Welcome back to earnings season! Over the next several weeks, I will be sending 40 detailed reviews on popular, high-quality companies. Upcoming reviews include ServiceNow, Tesla, Robinhood, Meta, SoFi, AMD, Palantir and so many others coming thereafter.

Taiwan Semi was sent this afternoon.

Other recent content includes:

If you'd like access to all of those reports, consistently thorough weekly news, my real-time performance/portfolio updates and access to a large Discord channel of seasoned investors, lock in your annual deal below.

This is where investors (including Fortune 500 executives) come for signal over noise and to invest with good reason.

a. Key Points

- Price hikes in the USA went as expected.

- A large $2.8 billion exit fee, collected from Warner Brothers, propped up net income and free cash flow during the quarter.

- Reed Hastings will not run for executive chairman re-election.

- Live Sports continue to be a great source of subscriber growth.

- Watch hour growth was stable sequentially.

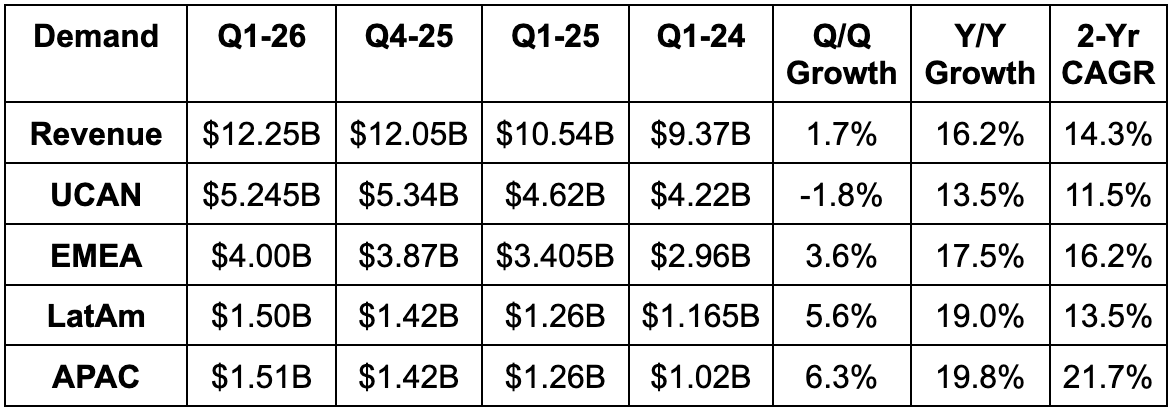

b. Demand

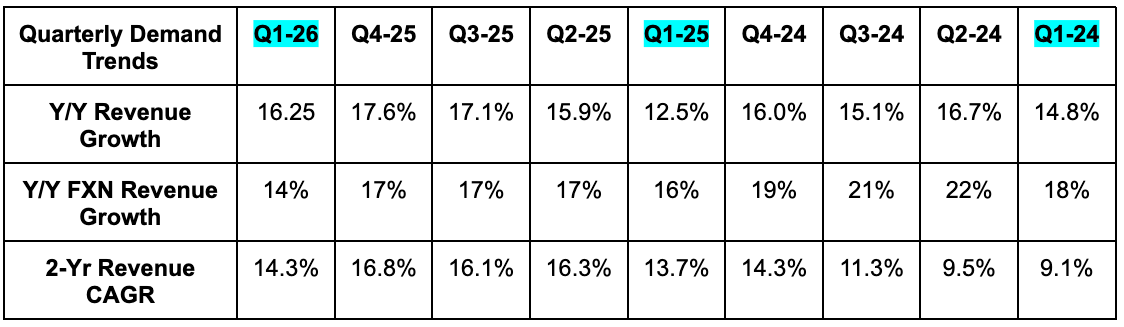

- Beat revenue estimates by 0.6% & beat guidance by 0.7%.

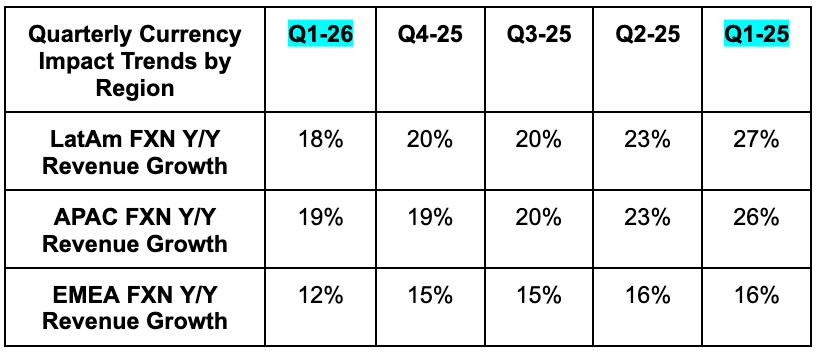

- Revenue outperformance was helped by modestly outperforming subscriber growth and foreign exchange.

- By geography:

- USA + Canada (UCAN) revenue missed estimates by 0.6%.

- Europe, Middle Eastern and African (EMEA) revenue beat estimates by 1.2%.

- Latin American (LatAm) revenue beat estimates by 3%.

- Asia-Pacific revenue beat estimates by 2.1%.

- Netflix said it is now approaching 1 billion total consumers under a subscription. They also spoke about being under 45% penetrated within their 800 million household total addressable market and only 7% penetrated in terms of the revenue opportunity within those households.

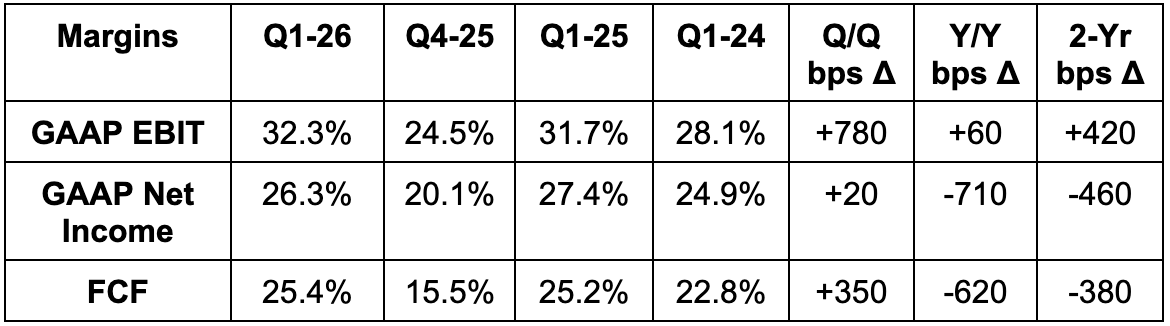

c. Profits & Margins

- Slightly beat EBIT estimates & beat guidance by 1%.

- EBIT rose by 18% Y/Y.

- EBIT beat was driven by revenue outperformance.

- Beat $0.76 EPS estimates by $0.47. This includes a large $2.8B fee collected from Warner Brothers as a penalty from that company exiting their agreement with Netflix.

- Beat FCF estimates by 78%, with the large beat driven by the same fee described above.

If we exclude the Warner Brothers $2.8B fee and assume a stable Y/Y tax rate, Netflix would have earned about $0.75 per share and missed estimates by a penny. If we assume a similar impact on FCF, the result was 3% below expectations. The net income and free cash flow margins in the table below exclude the $2.8B collection and the tax noise associated with it for more normal comps.

d. Balance Sheet

Upgrade below to read through guidance, valuation, notes from the call, my take on the quarter and thoughts on the investment.