News of the Week (April 22 - 26)

News of the Week (April 22 - 26)

ServiceNow; Spotify; Visa; Amazon; PayPal; SoFi; Lemonade; Enphase; Chipotle; Intel; Meta; Amazon (again); Snowflake; The Trade Desk; Shopify; Macro; Portfolio

Busy week! In case you missed it, below you can find detailed Tesla, Meta, Alphabet and Microsoft earnings reviews.

1. ServiceNow (NOW) – Earnings Review

ServiceNow is one of the largest enterprise software firms in the world. It automates workflows, tech stacks and projects to augment customer efficiency. For this reason, it calls itself the “leading digital workflow company.” Workflow automation buckets include: service management, operations, asset management, security, customer management, employee management and creator management. These are further grouped into workflow buckets like “customer workflows” and “creative workflows.”

Key acronyms here include Information Technology Operations Management (ITOM) and Information Technology Service Management (ITSM).

All products and services are neatly tied into its “Now Platform.” To bolster automation capabilities, ServiceNow has been hard at work on GenAI innovation. Its Vancouver Platform release got the ball rolling by consolidating all model and app work into an intuitive set of products. It recently built on that debut with a “Washington D.C. Platform” release this year (more on this later) These platforms are a foundation for its GenAI apps and a key example of these apps is “Now Assist AI.” This is ServiceNow’s GenAI assistant/companion being infused across most of its products. “Plus SKUs” are how ServiceNow bundles all of its GenAI work into subscription packages. It upcharges clients for access to these SKUs as its approach to GenAI monetization has been more aggressive than most others. These Plus SKUs do things like automate customer service, expedite issue resolution, guide workflows and provide more conversational fetching/querying of a firm’s data.

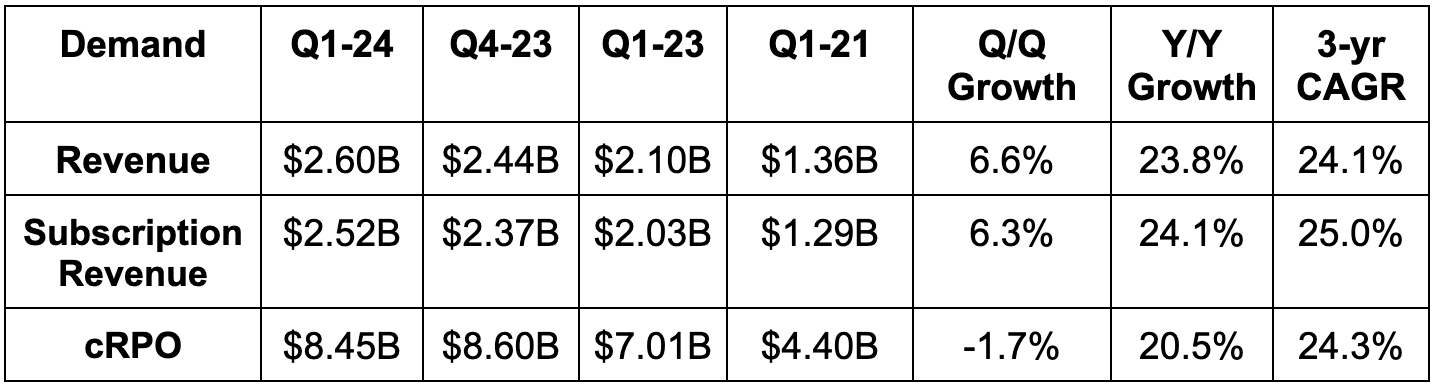

a. Demand

Met subscription revenue guidance. Its 24.1% 3-year revenue CAGR compares to 25.0% Q/Q and 25.8% 2 quarters ago.

Secured 8 deals worth $5 million or more in average contract value (ACV) vs. 4 deals Y/Y.

Slightly beat revenue estimates.

Beat 20% Y/Y current remaining performance obligation (cRPO) estimates. cRPO is a key leading indicator for demand.

Gross revenue retention (GRR) remained at a strong 98%.

b. Margins & Profitability

Beat EBIT estimates by 5.0%; beat EBIT margin guidance by 140 bps. Timing of marketing spend, OpEx efficiency gains and revenue outperformance drove the beat.

Beat $3.13 EPS estimate by $0.32.

Beat FCF estimates by 26%. Note that quarterly free cash flow generation is heavily influenced by in-period collections and is somewhat seasonal. Annual FCF generation is a better thing to track for this specific profit metric.

c. Balance Sheet

$8.8B in cash, equivalents and investments.

$1.5B in debt.

Diluted shares grew by 2.0% Y/Y.

Basic shares grew by 1.0% Y/Y.

d. Guidance & Valuation

ServiceNow slightly raised its annual subscription revenue guide. Guidance implies 21.5%-22% Y/Y growth and the raise is despite $17 million in incremental FX headwinds. In Q1 2024, NOW started utilizing an FX hedging program to reduce volatility from currency fluctuations. Still, this doesn’t completely hedge out all risk, hence the added FX headwinds in the new guide. It reiterated 84.5% subscription gross margin, 29% EBIT margin and 31% FCF margin guidance.

For next quarter, 20.5% Y/Y cRPO guidance needs a bit of added context. ServiceNow had a banner Q3 2023 for U.S. Federal Government wins. These contracts are generally longer in duration, which is a cRPO headwind of about 2 points for next quarter. Its 99% U.S. Federal renewal rate, thus far, bodes very well for these high value customers being retained for the long haul.

NOW trades for 53x 2024 earnings, with earnings expected to grow by 25% Y/Y.

e. Call & Release

The Platform Play:

For the last year, we’ve talked about how platform plays in enterprise software are winning. Platforms allow companies to consolidate vendors, streamline interdepartmental communication, cut costs and improve outcomes. They’re a powerful force multiplier for efficiency, and ServiceNow is that platform within digital workflows. The results speak for themselves. 15 of its 20 largest deals included 7 or more modules. ITSM and ITOM (already defined) were each included in 16 of its 20 largest deals. Security and Risk was in 11 of its largest 20 deals; creator as well as employee workflows were in half of its 20 largest deals. These customers continue to renew at a gross retention rate near 100% and continue to lean on more of its products to modernize their tech stacks. Need more evidence? NOW enjoyed 50% Y/Y growth in customers paying them $20 million or more annually.

Leadership spoke about 15 years of “decentralizing technology governance.” The 21st century has pushed all departments to invest in information technology – not just for software developers. That meant disparate usage of 3rd party vendors, heightened cybersecurity risk and low quality outcomes. It’s very hard to go back and properly integrate these vendors. It’s a lot easier to use fewer vendors who can do much more for you on their own. That’s the ServiceNow value prop – just like Salesforce in customer resource management (CRM)... just like CrowdStrike in endpoint security.

GenAI Amplifying This Platform Play:

Unsurprisingly, ServiceNow is directly integrating its Now Assist AI companion across all product categories to ensure they work as well together as humanly (or I guess artificially) as possible. The GenAI boom is becoming another avenue for more powerful cross-selling. As explained in the intro, Now Assist AI is driving significant utility and potential for how to improve and automate tedious digital workflows. GenAI was in 7 of its 10 largest contracts as clients looked to “de-risk” their tech stack siloes with ServiceNow’s unifying suite. This is why its Plus SKUs (including its GenAI services) are setting new records for ACV.

“Every business workflow in every enterprise will be engineered with GenAI at its core. We are the single pane of glass that enables end-to-end digital transformation… They can radically simplify the tech stack with us.” – CEO Bill McDermott

ServiceNow’s overarching platform, including Now Assist AI for ITSM, is helping Hitachi resolve client issues more expediently while saving millions. More with less… with Service Now.

Equinix is using Now Assist AI for Human Resource workflows to raise agent productivity by 30%.

Product News:

ServiceNow launched the “Washington, D.C.” platform this quarter. This is essentially a large batch of GenAI-inspired upgrades to the Now platform. It builds on the progress of the previous Vancouver platform release. It more seamlessly ties together NOW’s product categories to drive better interdepartmental work and communication. It offers the “workflow studio” as a unified workspace to manage productivity across teams. It allows for seamless database refreshes without complex coding; it goes deeper in terms of intelligently automating customer service and order management workflows.

ITOM for AI operations is another newer product to discuss. This, as the name indicates, laces Now Assist AI into ITOM to prioritize, rank and contextualize IT alerts with recommendations for remediation.

ServiceNow debuted StarCoder2 as part of a collaboration with Hugging Face and Nvidia. This provides access to large language models (LLMs) to automate code creation. It also deepened an already tight Nvidia partnership to include new GenAI tools for the telecom space, among other things. Finally, it added its new GenAI tools to a close Microsoft partnership for shared customers.

Going Global:

New AoraNow partnership in Japan to accelerate its traction there. This was a banner quarter for new business in that nation.

New $500 million investment earmarked for Saudi Arabia, which includes plans for two data centers.

Added significantly more business with Novartis during the quarter.

“NEOM” in the Middle East is using the Now Platform to “build the first cognitive city.”

Added Australia’s Health Department, Italy’s IT division and a local division of Sao Paulo’s government in Brazil as customers during the quarter.

“In terms of geopolitics, we focus on what we can control. We build great products and services and have a winning culture. That’s why we perform well when others don’t.” – CEO Bill McDermott

f. Take

Another rock solid quarter from one of the highest quality enterprise software names on the planet. No drama. Just more execution. I see how the stock reacted to the report; I do not think long term shareholders should be concerned with that move in the least. Well done, ServiceNow.

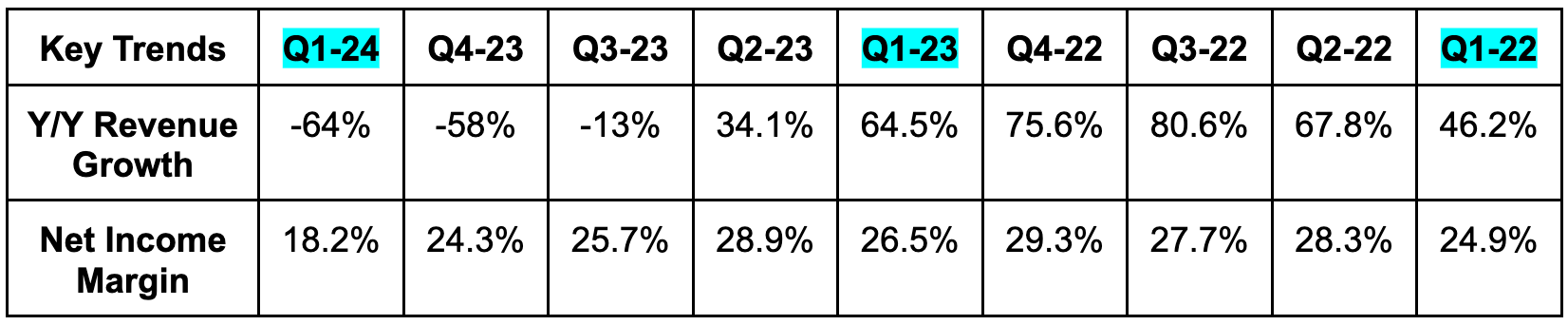

2. Spotify (SPOT) – Earnings Review

a. Demand

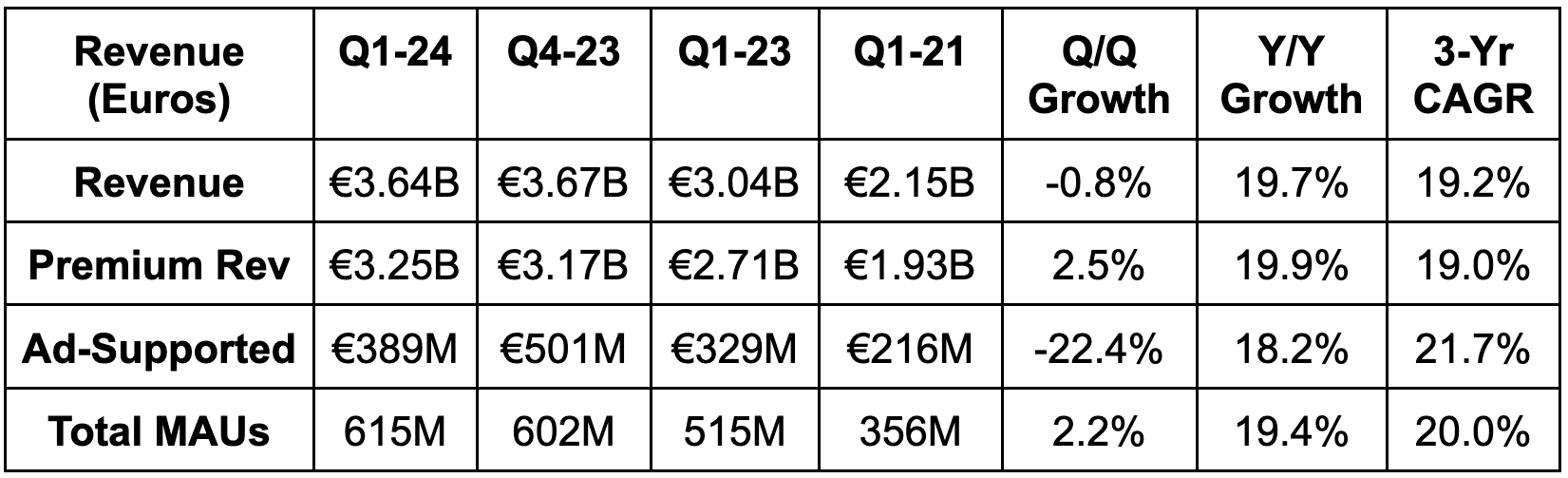

Beat revenue estimates by 1% & beat identical revenue guidance by 1%.

FX neutral (FXN) revenue growth of 21% Y/Y accelerated by 1 point vs. last quarter.

Its 19.2% 3-year revenue compounded annual growth rate (CAGR) compares to 19.1% last quarter and 19.3% 2 quarters ago.

Met premium subscriber guidance.

Slightly missed total monthly active user (MAU) guidance.

b. Profitability & Margins

Beat 26.5% GAAP GPM estimates by 110 basis points (bps; 1 bps = 0.01%) & beat guidance by 120 bps. This was its first quarter of over €1 billion in gross profit.

Beat EBIT estimates by 9.8% & missed EBIT guidance by 6.7%. This was driven by €82 million in “social charges” compared to €8 million in social charges baked into the guide. Sell-side had already adjusted. These are payroll taxes paid to employees. That expense is tied to share price. Share price rose a lot, so charges rose a lot. Maybe my favorite source of an EBIT miss ever.

Operating expenses (OpEx) fell by 9% Y/Y. Without any social charges or restructuring charges, OpEx fell by 13% Y/Y.

Beat free cash flow (FCF) estimates by 15%.

Beat €0.63 GAAP EPS estimates by €0.34.

c. Balance Sheet

€4.7B in cash, equivalents & investments.

No debt; $1.27 billion in convertible notes that will soon mature.

Basic shares +2.3% Y/Y. Diluted shares +5.3% Y/Y.

d. Next Quarter Guidance & Valuation

Beat revenue estimates by 1.3%.

Beat 26.7% GAAP GPM estimates by 140 bps. That’s a large beat here.

Beat EBIT estimates by 45%. €13M in social charges are baked into the EBIT guide.

16 million MAU adds; 6 million premium subscriber adds.

“We are well positioned to deliver on our 2022 investor day goals.” – Founder/CEO Daniel Ek

Spotify trades for 60x 2024 earnings. It did not earn any net income last year.

e. Call & Letter

Monthly Active Users:

The source of the MAU miss was understandable. Spotify continued to pull back on marketing spend throughout 2023 and into 2024. That pullback in 2023 was masked by strong product debuts, better-than-expected marketing efficiency, historically strong MAU adds, and competition exiting key markets towards the end of the year. Those temporary tailwinds went away this quarter as it continued to be prudent with marketing spend. That played out while it dealt with some operational disruption from layoffs earlier this year. It thinks this disruption is now in the rear-view and it expects MAU additions to accelerate for the rest of 2024. As Ek pointed out, Spotify has demonstrated a great ability to evolve focus areas as changing times demand it. The firm leaned into top-of-funnel growth when money was free; it re-set its cost base effectively as macro got tougher; now it’s ready to get a bit more aggressive in marketing spend once more. Not nearly as aggressive as it was in 2021, but still more aggressive.

“The MAU growth we achieved in 2023 not only surpassed our most ambitious forecast, but also set a record for the most significant user growth in Spotify's history. While we anticipate continued robust growth going forward, 2023 was a truly standout year and should not be an expectation for every subsequent year.” – Founder/CEO Daniel Ek

Premium Business:

While MAU results were a tad light, premium subscriber growth was not. Total subscribers met expectations with its Family and Duo (2 people) plans leading the strength. These plans come with lower churn vs. individual subscriptions, making this trend positive for multiple reasons. Revenue per premium user continued to accelerate by a full 200 bps Q/Q. This was helped by price hikes, but also hurt by geographic mix toward lower propensity to spend nations.

A key theme of the call was “pricing-to-value.” Spotify, over the last few years, has transformed itself from a mono-line music business, to one that’s now a powerful podcasting and (already) audiobook player. It has debuted video, short-form music discovery and its AI DJ to more intelligently match content with tastes. It also just launched “Song Psychic” to get conversational answers to questions via custom song (a little weird). These additional product consumption avenues create two compelling opportunities for better monetization. First, more value justifies higher prices. It will keep adding value and will keep pricing to that value. Simple enough. Secondly, the incremental offerings create more flexibility with subscription packaging. It allows Spotify to offer bundles and á la carte style purchasing as well (like its $9.99 audiobook-only plan).

“You will see more tiers that create incremental consumer flexibility to opt into the type of deal they believe offers the greatest value for them… We’re no longer a one-trick pony.” – Founder/CEO Daniel Ek

There’s another interesting product expansion opportunity here. Spotify is quickly being pulled into the digital education space, just like it was with audiobooks. If you recall, Spotify entered audiobooks first in Germany, where music labels had more aggregated rights to audiobook content. Publishers were adding their own books and seeing great traction. So? Spotify developed a product offering internally to ensure the processes were slicker and more intuitive… and to ensure it got a larger piece of that pie. The audiobook introduction is already raising weekly engagement levels by more than 1 hour. More engagement = more value = more pricing power. The same thing is now playing out in education. Podcasters are “hacking the system in a positive way” to game it and do more things. They’re teaching guitar and DJ classes and are having great early success. Spotify is now developing internal products to manage and host this in a higher quality way.

Premium revenue growth was 20% Y/Y (21% FX neutral (FXN) growth).

Premium subscribers rose by 14% Y/Y while revenue per subscriber rose by 5% Y/Y.

Growth was above 13% everywhere and accelerated in all geos besides North America and Europe.

Gross margins were strengthened by price hikes. Still, improving music and podcasting profitability were two additional, more consistent tailwinds. Gross margin is still being held back by investments to build out its audiobook business.

Ad-Based Business:

While advertising is still a much smaller piece of Spotify, its growth rate (18% Y/Y) is quickly approaching the premium arm. That’s even as programmatic, biddable impressions still make up a small portion of its ad revenue. Continuing to raise that proportion of highly targeted, granular impressions will directly prop up ad rates. That tailwind is basically entirely in front of Spotify… as it also continues to quickly grow impressions. Good combination. While the pricing environment for music is strong, podcasting remained softer, just like last quarter. Nonetheless, strong impression growth allowed both music and podcasting to enjoy healthy growth in excess of 10% Y/Y.

The Spotify Audience Network (SPAN) is Spotify’s way of serving as a conduit between buyers and platform publishers across most podcasting apps. This enjoyed 10% Q/Q growth in participating publishers following expansion into 5 new countries last quarter.

f. Take

As I’ve been vocal about on social media recently, this company has impressed me deeply over the last year. There aren’t many non-mega-cap firms that can slash their cost base without a negative demand impact. Spotify proved that they’re one of those companies… like Airbnb in 2020… like Uber and Shopify in 2022-2023… like Block right now… they have firmly placed themselves in that rare category. Spotify competes with multiple mega-cap tech firms with somewhat similar products. Differentiation here, to me, seemed tough to establish. Spotify did not get that memo and has figured out a way to outcompete richer companies with larger consumer networks than it currently has. Surprising… impressive… strong. Congratulations to shareholders on what has become a remarkable turnaround.

3. Visa (V) – Earnings Review

Visa is arguably the most important company in the world for gauging spend volume appetite for consumers and corporations. That’s what we’ll focus on in this report. Taking the credit and balance sheet risk is not its business model. It merely provides a scaled network to host complex payments flows. For this reason, it’s not a valuable gauge for credit health like Bank of America, American Express, Capital One, etc.

a. Demand

Visa beat revenue estimates by 1.9% & beat vague “mid-to-high single digit” revenue guidance. Its 15.3% 3-year revenue CAGR compares to 14.9% Q/Q and 19.1% 2 quarters ago.

Service revenue rose by 7% Y/Y.

Data processing revenue rose by 12% Y/Y.

International transaction revenue rose by 9% Y/Y.

Other revenue rose by 37% Y/Y as it had a strong quarter for things like consulting and marketing fees.

“Overall payments volume grew 8% and cross-border volume grew 16%, driven by stable consumer spending.” – CEO Ryan Mclnerney

b. Profitability & Margins

Visa beat $2.43 GAAP EPS estimates by $0.08 and beat its vague EPS growth guidance. Legal charge growth is the source of the Y/Y EBIT margin contraction. That’s why GAAP OpEx rose by 29%, while non-GAAP OpEx (which excludes this noise) rose by just 11% Y/Y.

Its GAAP effective income tax rate was 4 points lower vs. the Y/Y period, which is why the GAAP net income margin contraction is much smaller than for GAAP EBIT margin.

GAAP EPS rose by 12% Y/Y.

Non-GAAP EPS rose by 20% Y/Y when excluding the impacts of litigation, equity investments and amortization of acquired intangibles.

c. Balance Sheet

$20.8B in cash, equivalents and investment securities.

$20.6B in debt.

Share count fell by 2.8% Y/Y via continued buybacks.

Dividends rose by 12.4% Y/Y.

d. Guidance & Valuation

Reiterated low double digit annual revenue growth guidance. This is slightly better than 9.7% Y/Y growth expectations.

Reiterated low teens annual EPS growth guidance. This is roughly in line with 13% Y/Y growth expectations.

Lowered payment volume growth guidance from low double digits to high single digits.

Quarter-to-date, U.S. payments volume slowed to 4% Y/Y from 6% last quarter. This was predominantly due to Easter holiday timing. The team sees no sharp changes in consumer spend appetite.

Visa trades for 28x 2024 earnings. Earnings are expected to grow by 13% Y/Y.

e. Call & Release Highlights

Volume:

Slowing payment volume in Asia, and especially Mainland China, was called out by the team. That is why it lowered payment volume expectations for the year. It sees this as purely macro-related. Aside from that, volume growth was wonderfully resilient. Total FXN volume growth of 8% is stable compared to 8% Y/Y last quarter. Debit is stable at 9% Y/Y growth; credit is stable at 8% Y/Y growth. Currency headwinds led to actual growth slowing from 9% Y/Y to 7% Y/Y this quarter. In the U.S. specifically, total growth accelerated from 5% Y/Y last quarter to 6% Y/Y this quarter. Credit is steady at 6% Y/Y growth; debit accelerated from 5% to 6% Y/Y growth. That’s ideal, as it means customers are spending money that they actually have, rather than levering up their personal balance sheets.

Internationally, growth slowed from 12% Y/Y to 8% Y/Y due to currency headwinds. On an FXN basis, growth slowed from 12% Y/Y to 11% Y/Y.

Cross-border volume rose 16% Y/Y to maintain robust growth compared to last quarter’s 16% Y/Y result.

One may wonder, “how far can the Visa growth engine go?” Well… there’s no reason to think this runway is anything but long (even now). 50% of all transactions are still done via cash or check, and this company is perhaps the most powerful cash displacer in the world. Continued GDP growth and investments in fintech and next-gen payment rails to insulate them from competitive risks are two more reasons for optimism. This gigantic company could easily be a lot more gigantic over the long haul.

Partners:

8 of the 10 largest co-branded card programs in the USA are Visa partnerships. It just renewed its Alaska Airlines partnership and added Qatar Airways, Royal Air Maroc, and British Airways this quarter too. A Marriott extension, Robinhood’s Gold Card, SAP’s Taulia for virtual cards, and Trade Republic were highlighted as more partner wins during the quarter.

Tap-to-Pay:

Momentum for this payment form-factor is strong. Tap to pay rose by 5 points to 79% of total face-to-face transactions. Adoption rates in Japan doubled to 30% while New York City became the first major city in the USA to approach 50%.

Open Banking:

Open Banking simply means better data sharing and more consumer choice for storing and moving funds. Visa, through a purchase of Tink two years ago, has been hard at work on Open Banking in Europe. It signed Adyen and Revolut and is now setting its sights on the U.S. market. To get things jump-started, it has already signed open banking partnerships with Capital One, Fiserv and others.

Legal Settlement:

Last month, Visa settled a major lawsuit with merchants. It set restrictions on interchange fees among other things. Details about the settlement can be found in section 5 of this article.

f. Take

This was another strong quarter for a wonderfully consistent and elite enterprise. More of the same. In terms of the read-through to the economy, consumer spend levels are slowing, yet remain in quite good shape. Easter serving as the source of this weakness also makes slowing even less concerning, while talks of spend resilience are great to hear. Great quarter, great company and good news for the overall economy.

4. Portfolio Earnings Preview for Next Week – Amazon (AMZN), PayPal (PYPL), SoFi (SOFI) and Lemonade (LMND)

a. Amazon (AMZN)

Amazon should report excellent Q1 numbers next week. Google Cloud and Azure were both strong, Visa’s commentary on robust ecommerce spending was notable. There are no excuses for this company not to deliver, and that’s exactly what I expect it to do. How does the stock react? Not sure. The setup here isn’t as difficult as it was for Meta, but it’s far more difficult than it was for Tesla. The bar for execution is high. The countless margin tailwinds we discuss frequently, uniformly positive sell-side channel checks for its e-commerce marketplace and robust cloud spending should all lead to more success for this titan.

b. PayPal (PYPL)

PayPal needs to show the world that its initial 2024 guidance was greatly sand-bagged. It needs to raise transaction margin dollar guidance; it needs to keep layering on higher margin revenue for Braintree clients; it needs to expand private label success across the globe; it needs to monetize Venmo much better, and it needs to maintain its fair share of branded checkout. Cost cuts can only let profits compound for so long. Structural, long term profit growth will require these items if it’s to happen. I am cautiously optimistic here, as 0% annual transaction margin dollar and EPS growth just doesn't make sense. It assumes none of the needed product releases from 2023 have any impact at all. And furthermore, branded is still growing well in excess of U.S. GDP, which is a high margin business. Shifting its Braintree “growth-at-any-cost” philosophy to one that embraces rational pricing and software cross-selling should also help a lot. Focus is finally well-placed. If it has any success in fixing the broken business model whatsoever… there should be upside. I’m cautiously optimistic. If this quarter doesn’t go well… if the initial annual guidance doesn’t turn out to be the kitchen sink… I will seriously consider exiting this position.

c. SoFi (SOFI)

I’m not at all concerned about Q1 results here. CEO Anthony Noto conducted an interview 90% of the way through calendar Q1 where he basically reiterated all guidance. The only uncertainty here is surrounding 2024 guidance. Sentiment here is pretty poor at the moment, and a beat and raise can go a long way in changing that. Don’t be surprised if we see another gap up Monday morning and a subsequent sell-off. This is a highly liquid name, with a massive share count. The pattern of spikes and sell-offs will continue to play out… until it doesn’t. When? Not sure. But for now, all I care about is this company continuing to grow quickly, expand margins and march towards its 2026 targets.

d. Lemonade (LMND)

As we’ve discussed in the newsletter, insurance premium inflation stinks for consumers, but is great for Lemonade. Insurers struggle with inflation as claims rise with rising prices, but premiums are anchored until slow regulators approve updates. The insurance premium inflation we’ve seen recently hints that those updates are now coming. If that’s happening, it would open up more geographies (like California) for Lemonade to lean into growth.

This company continues to trade around cash value and is quickly shrinking its burn rate. Balance sheet risk has vanished as its margins improve and its growth engine churns. All it will take is temporary macro headwinds to fade for that growth engine to pick up once more. This is arguably the best $1 billion company I’ve ever seen in terms of being able to closely control their revenue growth. It has also been surgical in its modeling of margin trends for the last several years. If they feel less need to control costs and growth due to the reasons cited… large revenue beats and meeting profit targets should be what plays out. If brightening macro doesn’t occur, I see in-line revenue and outperforming profit. The initial 2024 guide was quite conservative… we’ll see if they over-deliver like I expect.

5. Earnings Round-Up – Enphase (ENPH); Chipotle (CMG); Intel (INTC); Caterpillar (CAT)

a. Enphase

Enphase is a player in residential and commercial solar energy. Its sector is wildly cyclical and rate sensitive.

Results:

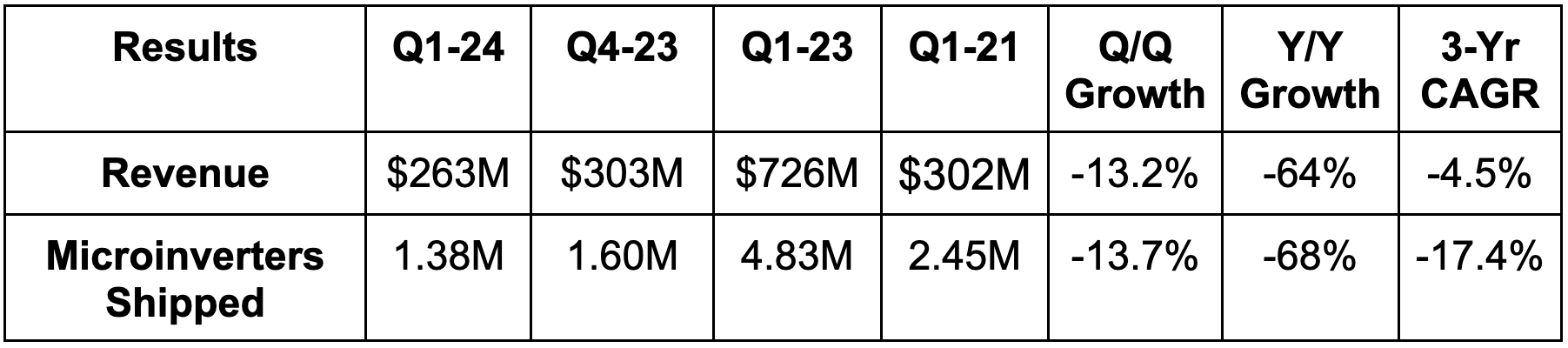

Missed revenue estimate by 5.3% & missed guide by 6.1%.

Missed GAAP EBIT estimate by 51% & missed guide by 17%.

Missed EBIT guide by 14%.

Missed $104M FCF estimate by $54M.

Next Quarter Guidance & Valuation:

Revenue Missed by 11%.

Missed 46.5% GAAP GPM estimate by 300 bps.

Missed $19M GAAP EBIT estimate by $19M.

Enphase trades for 38x 2024 earnings, with earnings expected to shrink by 34% Y/Y.

Balance Sheet:

$1.6B in cash & equivalents.

$1.2B in debt.

Diluted shares -3.7% Y/Y.

b. Chipotle (CMG)

Results:

Slightly beat revenue estimates by 0.3%.

Beat EBIT estimates by 7.2%.

Beat $11.71 GAAP EPS estimates by $1.30.

Annual Guidance & Valuation:

Chipotle raised its comparable store sales guidance from mid-single digits to high single digits.

Chipotle trades for 57x 2024 earnings, with earnings expected to grow by 24% Y/Y.

Balance Sheet:

$727M in cash & equivalents.

$700M in investments.

Share count fell slightly Y/Y.

c. Intel (INTC)

Results:

Missed revenue estimates by 0.5% but met revenue guidance.

Beat 44.5% GPM estimates & beat its same guide by 60 bps.

Beat $0.13 EPS estimates by $0.05.

Beat EBIT estimates by 23.4%.

Next Quarter Guidance & Valuation:

Revenue guidance missed by 4.3%.

GAAP EPS guidance missed $0.01 estimates by $0.06.

EPS guidance missed $0.26 estimates by $0.16.

GPM guidance sharply missed 45.4% estimates by 190 bps.

Intel trades for 30x 2024 earnings, with earnings expected to grow by 3% Y/Y.

Balance Sheet:

$21 billion in cash & equivalents.

Inventory flat Y/Y.

$56.3B in debt;

Share count rose 2.1% Y/Y.

d. Caterpillar (CAT)

I only had time to listen to the prepared remarks here (finished this article at 1:00am last night), but there were some interesting nuggets to share. As a heavy machinery industrial, this company is macro-sensitive and impacted by interest rates. Higher rates weigh on fixed business investment; that weighs on CAT. This quarter, the theme was North American resilience. On the heels of an excellent 2023, it sees that market’s growth slowing, yet remaining quite robust. The only pocket of weakness it’s seeing is in Europe.

6. Meta Platforms (META) — Follow Up Call

CFO Susan Li hosted Meta’s quarterly follow-up call this week following earnings. There was a lot of repetition, but some new ideas to cover.

Li told investors that Meta’s “year of efficiency” learnings would be carried with it throughout the 2024 and 2025 CapEx ramp. As I said in the review, this is not Meta throwing margin preservation as a focus area in the garbage. It will walk and chew gum here.

Furthermore, this CapEx is positioning Meta for years, not quarters to come. This spend will handle AI training clusters and inference workloads through the next several versions of its Llama models. Importantly, this CapEx capacity is also somewhat flexible in terms of use case. This goes back to the new data center format that Meta is utilizing which frees more seamless scaling and shifting of workloads. That way, if Meta overestimates what it needs for its GenAI model and app work, it will be able to seamlessly re-allocate the compute to AI ranking and recommendation models. This will not be wasted money; there are many positive return on investment areas to use this compute, regardless of how correct they are about GenAI.

We also got a bit more color on the revenue guide and Reels monetization. The aggressive ramping in ad load and impressions for Reels happened in 2023. There’s a bit more work to do to bring that load to parity with Feed and Stories, but the bulk of the catch-up is now in the past. When pairing that with much tougher comps and FX swinging from a tailwind to a headwind, we are left with the slightly soft Q1 revenue guide. Still, it remains adamant that ad demand (including for Chinese sellers) remains strong, along with app engagement.

7. Amazon (AMZN) – Affordable Grocery Subscription & Sports

Also mentions Uber (UBER), Lyft (LYFT), DoorDash (DASH) and Disney (DIS).

Amazon debuted a $9.99 per month grocery delivery subscription. It allows Prime Members to order from Amazon Fresh, Whole Foods and some local partners for unlimited monthly delivery. While Amazon can’t tie this into ride sharing like Uber can, this will still be an increasingly meaningful competitor to focus on here. And candidly, this is an even bigger threat for mono-line businesses like Lyft and Doordash, which can’t bundle products for unique value as powerfully as Uber does.

In other news, Amazon Prime Video will stream NHL games in Canada next year and is negotiating with the NBA on expanded content rights. Amazon has the ability to use live sports as a loss leader. It can easily cross-sell margin accretive products and bundles to subscribers to make this loss leader a rational maneuver. With live sports commanding as much passion and attention as they do, Amazon is poised to use its fortress balance sheet to take more and more of these watch hours. As an aside, this is exactly why I think Disney’s ESPN still must partner with a mega-cap tech player (as well as the rumored NFL deal).

8. Snowflake (SNOW) – Innovation?

A key concern surrounding Snowflake for the last few quarters has been pace of innovation. Leadership will explicitly tell you that they need to move faster, which is why Sridhar Ramaswamy was brought in as the new CEO. This week, Snowflake launched a new LLM that serves as positive evidence for the pace of innovation picking up steam. Snowflake “Arctic” is the name of the new product that is specifically built for enterprise data. It was created with efficiency in mind and trained in the most cost conscious way possible. It’s also open source, which means customers can easily use it to create models more affordably. It also means 3rd party developers will invariably improve Arctic over time through their own work. That will make this an even lower cost model. It’s the same idea as for Meta’s Llama series.

Arctic is great for standard query language (SQL) generation like you’d expect from a data lake and warehouse player. It also ranks very highly in code following… even compared to larger parameter models. Bulls should be pleased with this small, yet important debut.

9. The Trade Desk (TTD) — Retail Media Partner

The Trade Desk and foodpanda announced a new partnership. foodpanda is a food and grocery delivery company that operates in Hong Kong, Taiwan and a few other Asian markets. As part of the relationship, The Trade Desk is providing tools from its Retail Media suite to unleash foodpanda’s first party data. The goal is to sharpen targeting and measurement, while making more of foodpanda’s impressions openly biddable to raise returns. Together, they’ll also offer foodpanda’s ad customers real time conversion data to tweak and optimize campaigns on the fly. In a beta test last year, the partnership delivered an 81% boost to conversions for Unilever’s Knorr brand. 87% of the total conversions from the campaign were also new customers for Knorr.

This partnership is just one piece of positive news in a sea of momentum for TTD’s retail media business. Whether it’s Macy’s, Walmart, Walgreens, Home Depot or any more, the company is powering the modernization of customer acquisition for most of the sector at this point. While foodpanda isn’t as large as other partners mentioned, it still did $11 billion in 2023 revenue.

10. Shopify (SHOP) — Bullish Analyst Note

Deutsche Bank sees strong Shopify Plus momentum and overall strong app sage data from Bloomberg as driving upside to its guidance this quarter.

10. Macro

Output Data:

The Manufacturing Purchasing Managers Index (PMI) for April was 49.9 vs. 52.0 expected and 51.9 last month.

The Services PMI for April was 50.9 vs. 52.0 expected and 51.7 last month.

Core Durable Goods Orders M/M for March rose by 0.2% vs. 0.3% expected and 0.1% last month.

Durable Goods Orders M/M for March rose by 2.6% vs. 2.5% expected and 0.7% last month.

Consumer & Employment Data:

Continuing Jobless Claims were better than expected and fell from 1.796M to 1.781M vs. the last report.

New Home Sales for March were 693,000 vs. 668,000 expected and 637,000 last month.

Michigan Consumer Expectations and Sentiment for April both missed and fell M/M.

Inflation Data:

The Personal Consumption Expenditures (PCE) Price Index for March rose by 0.3% as expected and compared to 0.3% last month.

The Core PCE Price Index for March rose by 0.3% as expected and compared to 0.3% last month.

Michigan 1-year inflation expectations came in at 3.2% for April vs. 3.1% expected and 2.9% last month. 5-year expectations came in at 3% for April as expected and compared to 2.8% last month.

10. My Portfolio

No transactions to share this week.

Awesome! Thank you for weekly updates and commentary. I really appreciate it every Saturday morning! 2x things, first I believe you said at some point in the last month you would be going to a paid subscription? When is that taking place and how much? 2nd, FROG, did I miss when you removed that from your portfolio? Was there a reason? It’s been a good hold these last 2 years since I made the purchase, and wondering if you saw weakness I'm missing? Or if it was a personal allocation decision…? Thank you again!