News of the Week (February 26 - March 1)

News of the Week (February 26 - March 1)

Lemonade; Duolingo; Cava; Sweetgreen; Hims; Workday; Okta; Axon; SoFi; Disney; Market Headlines; Macro; Portfolio

In case you missed it:

1. Lemonade (LMND) – Earnings Review

Lemonade is a digitally-native insurance company. It aims to leverage AI to automate pieces of the tedious onboarding & claims processes and to sharpen underwriting models. Its goal is to delight customers with a superior experience (file a claim in seconds) to keep them loyal and coming back for more products.

a. Demand

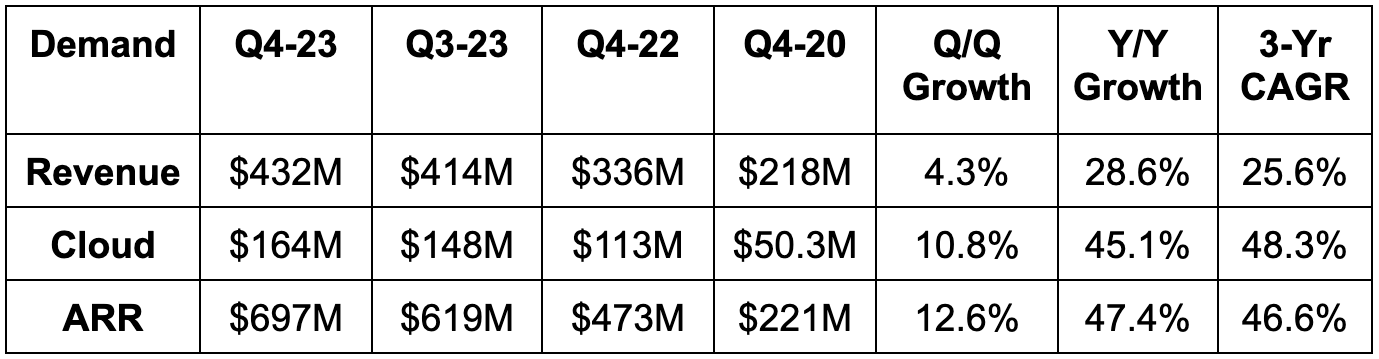

Beat In Force Premium (IFP) guidance by 2.7%.

Beat Gross Earned Premium (GEP) guidance by 3.4%.

Beat revenue estimates by 3.6% & beat revenue guidance by 7%.

Net interest income and a small decline in ceded premium rate are why revenue growth led premium growth.

b. Profitability

Beat EBITDA estimate by 28% & beat EBITDA guide by 33%.

Overall non-GAAP operating expenses (OpEx) fell by 5% Y/Y. GAAP OpEx fell slightly Y/Y.

All three major OpEx buckets fell Y/Y in dollar terms. Headcount fell 8% Y/Y.

Beat -$0.80 GAAP EPS estimate by $0.19.

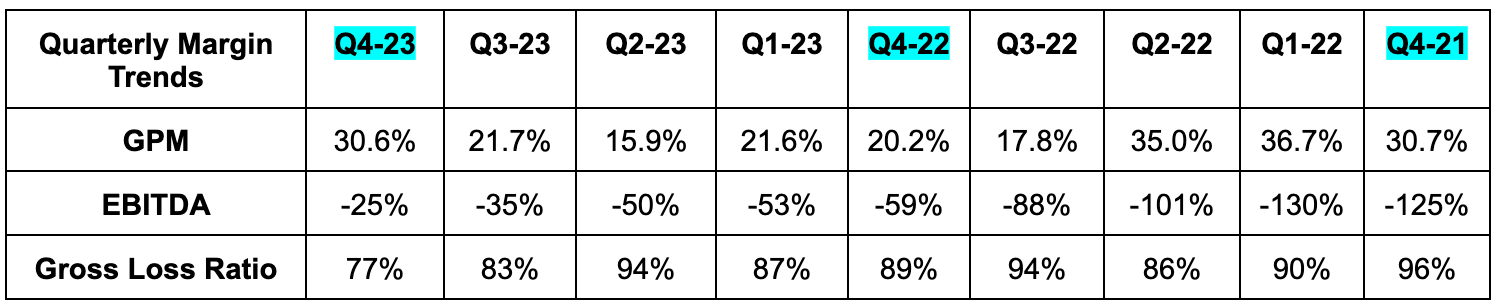

Beat 26.2% GAAP gross profit margin (GPM) estimate by 290 basis point (bps; 1 bps = 0.01%). GPM is tightly correlated with loss ratios.

c. Balance Sheet

$945 million Cash & equivalents.

No debt.

Share count rose by just 1.2% Y/Y.

d. Annual Guidance & Valuation

Lemonade’s annual revenue guidance missed by 2.6% while its annual EBITDA guidance beat expectations by 2.7%. Its annual IFP guidance was 1.1% ahead of expectations. As revenue is a byproduct of its ceded premium rate and investment income, the IFP beat is more important to me than the revenue miss. It guided to 26% Y/Y IFP growth vs. old guidance calling for 25%+ Y/Y IFP growth. It expects to accelerate top line growth throughout the year as the regulatory pricing approval backdrop improves. Much more on this in the next section.

“In 2023, we intentionally slowed growth to minimize sales of products in areas where we are still underpriced… 20% growth outpaced the industry, yet was slower for us vs. previous years and future years if things go to plan.” — Co-Founder Shai Winninger

The company reiterated plans to turn free cash flow positive in 2025 and EBITDA positive in 2026. It also reiterated no cash raises until it turns profitable and can raise from a point of strength with compelling rates, rather than from a point of weakness and need.

“Our approach to guidance this year is measured as always, but it's realistic and it's in line with our own internal expectations… While there is always the aspiration for outperformance, especially this early in the year, we would urge listeners caution about assuming that our guidance is overly conservative. It is not.” – CFO Tim Bixby

Lemonade trades for about 6x 2024 gross profit. Gross profit should grow by roughly 20%-25% Y/Y.

e. Call & Release Highlights

The Backdrop:

2023 was a historically challenging year for insurance. Severe weather events skyrocketed in terms of damage and frequency. Spiking cost of capital severely weighed on reinsurance demand overall. Soaring inflation levels greatly weighed on the profitability of books across the sector. As a reminder, claims float freely and rise with inflation while premium changes in the U.S. must be approved by regulators. Regulators are slow, and the time lag leads to unit economic deterioration while the process unfolds. Lemonade’s automated and light-weight operations have meant it enjoys a faster pace of rate approvals than most, but this has still been a thorn in its side. All of these factors have led to multiple large insurers pulling out of large markets like California.

Lemonade, since 2022, has committed to only pursuing profitable growth across markets and geographies. It has pulled back in some places and leaned into growth in others. The result for 2023 was cutting growth spend, allowing premium growth to slow and enjoying an acceleration in its path to profitability. That’s what made 2023 such a “pivotal year” for Lemonade, despite the industry chaos.

Now for 2024? Inflation is easing, rate approvals are flowing in and cost of capital is almost surely peaking. These factors (especially rate approvals) are exactly what Lemonade needs. The green shoots are how it can turn the growth engines back on for home and car insurance in states like California. It will be more aggressive with growth in 2024 vs. 2023, but still not nearly as aggressive as during the years before.

The plan is to double growth spend from a depressed $55 million 2023 level to $110 million in 2024. It also plans to add 50% more IFP this year vs. 2023 with the added growth spend carrying a 3x return on investment over the next couple years. This is why the pace of EBITDA loss improvement in 2024 is expected to moderate.

Lemonade’s goal for 2024 is to still improve EBITDA losses while exponentially boosting growth spend. That boost in isolation would have led to worsening Y/Y EBITDA losses. GenAI advancements have allowed it to triple the % of automated customer service email responses in just months. This will drive more cost savings and continue shrinking losses.

“As the universe of products and geos where we are rate-adequate expands, we will grow in lockstep. We're excited to step on the gas once more… We are on a trajectory of steadily gaining velocity, as we smoothly accelerate our growth rate back to our target baseline of 25% CAGR, and beyond.” – Shareholder Letter

“We reflect back on this tumultuous period quite sure that we are emerging from these shocks the better for having endured them. We are leaner, more resilient and with fewer competitors than we would have had without the turbulence.” – Co-Founder/ CEO Dan Schreiber

Synthetic Agents and EBITDA vs. Free Cash Flow:

If the “Synthetic Agent” concept is new to you, I’d highly recommend reading about the program in section 9 of this article. It’s an important concept for Lemonade’s growth, liquidity and overall investment case. One does not fully understand Lemonade, the company, until one understands this program.

In 2024, Lemonade expects to boost the 50% of its growth spend currently being financed by General Catalyst (GC) to 80%. GC seems to be pleased with how the partnership is progressing, as it just added another $140 million in growth funding. Notably, this financed spend is still incurred as a sales & marketing operating expense on Lemonade’s income statement. It still impacts EBITDA and net income. BUT… it does not impact cash flow. Lemonade expects its FCF to meaningfully and positively diverge from EBITDA improvement as a result. While the 2024 EBITDA loss improvements are set to moderate, the cash burn improvement is expected to stay rapid.

This program is how its cash position rose from $942 million to $945 million over the last 6 months despite GAAP losses. It has effectively and expeditiously fixed its balance sheet and liquidity crunches. This is no small thing. Lemonade is no longer in any material danger of running out of cash; its net cash position should bottom around $860 million by year’s end (it thinks).

“This isn't a mission accomplished moment, not by a long shot, but the progress in 2023 was tangible and material, and it increases our confidence that we're on track not only to turn cash flow positive next year with plenty of cash in the bank, but to build a large, enduring and profitable business thereafter.” – CEO Dan Schreiber

Europe:

Things are now going very well in Europe for Lemonade. It was a slow start, but momentum is accelerating significantly. Gross profit is improving briskly and premium growth was 100% Y/Y on that continent. Impressively, 30% of its new customers this quarter came from Europe vs. 3% 18 months ago. That’s partially due to European regulation being friendlier than in the USA. Lemonade can more freely adjust premiums without constant and slow pre-approvals across the pond. This leaves it significantly less vulnerable to the risk that catastrophic events (CAT) and inflation pose to its loss rates and margins. So? While it has had to pull back on growth in the states, the same has not been true in Europe. The letter explicitly took the time to praise Lemonade’s team there and to talk up near-term tailwinds. It will launch home insurance as its second European product line in the UK and France this year.

Gross Loss Ratio (GLR):

Lemonade’s GLR encouragingly dipped below 80% for the first time in two years. It expects continued improvement in this important ratio, but not linear improvement. It’s likely that there will be more quarters of elevated loss ratios while the book is still small and more vulnerable to severe weather than larger competitors. Notably, for this quarter, CAT was only a 500 bps drag on GLR vs. 1,000 bps Y/Y. GLR fell by 600 bps Y/Y excluding this impact. Loss ratios for each individual product also fell between 900-1,800 bps Y/Y. Good to hear.

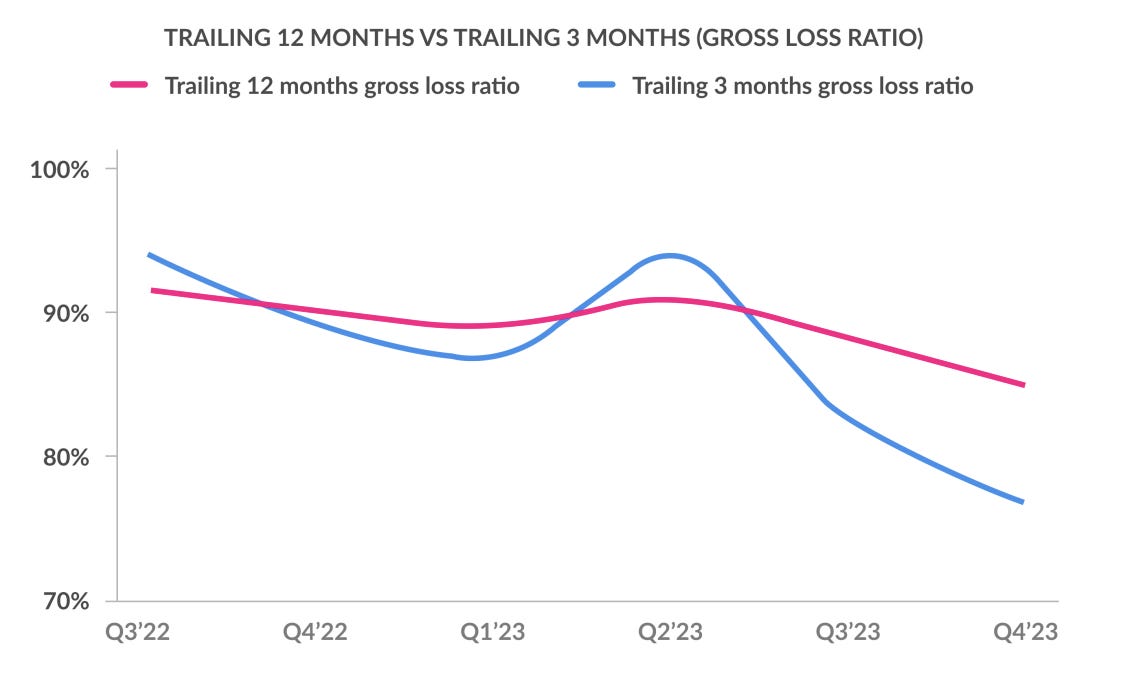

Lemonade talked in detail about loss ratio seasonality as well. We don’t need to get into the weeds here, but going forward, it will disclose a trailing 12 month (TTM) GLR. This is typical within the industry, and smooths out some of the noise from quarterly loss ratio volatility. Its TTM GLR in 2023 was 85% vs. 90% in 2022. As a reminder, this is still elevated vs. industry norms due to new product introductions and brisk new customer growth. New products and users generally start at loss ratio peaks. More of Lemonade’s book is made up of this type of business vs. incumbents.

Lifetime Value Model #9 (LTV 9) & U.S. Home Insurance:

Lemonade continues to sharpen its LTV underwriting models to hone in on the net present value of new business more precisely. The company was born as a digitally native AI-powered insurance company. That’s how it onboards in minutes, pays out claims in seconds and carries a customer satisfaction marking astronomically higher than legacy players. It’s not trying to frantically retrofit siloed and archaic systems to work in modern times; it built those systems to be seamlessly molded with no downtime, no disruption and no headache.

Lemonade’s latest LTV 9 model is a compilation of 50 ML models. It has “revealed components of risk clusters that seemed monolithic to older models,” but aren’t. This is powering greater risk selection and that improvement will continuously improve over time. The new model has uncovered that its Renters business is more successful than it thought and Pet is about as expected; Car and especially Lemonade Home are struggling compared to expectations. These struggles are entirely related to regulatory rate approvals as the LTV model only considers current premiums, and not prospective changes to those premiums. Lemonade is confident that it knows exactly which customers to pursue when approvals finally come in states like California and New Jersey.

For now, this means it’s pulling back mainly on new home policies with 13% of new premiums from home in 2023 vs. 27% in 2021. Most of this is because of California with 1% of its new home premiums coming from that state last quarter vs. 37% in 2021. That’s the largest piece of the intentional growth slowdown in 2023. Again, temporary and due to slow regulators and high inflation. While this is frustrating, the headwinds will eventually shift to tailwinds. That’s already beginning to happen, with the coinciding initial re-acceleration in IFP growth set to take place throughout 2024 and 2025.

While this process unfolds, Lemonade will debut a new 3rd party paper home insurance program. This will entail onboarding users through Lemonade’s best-in-class interface and using other insurers to actually underwrite the policies. It already does this with its earthquake and term life insurance.

Car Insurance:

Based on expected rate filing approvals, car insurance should be about 15% of new premiums in 2024 before doubling to 30% of new premiums in 2025. There is strong demand for this product as regulatory headwinds fade. In states where car insurance can be properly priced and Lemonade is pursuing growth, premiums rose by 50% Y/Y. Furthermore, unleashing the car business should boost the proportion of new plans sold to existing users. In those same states where it’s freely growing the business, cross-sell rates are 30% vs. 25% elsewhere. That will assist with marketing intensity and profitability.

Final Notes:

Its newer Chewy pet insurance partnership is “going well.”

Gross margin should continue to expand going forward.

Overall multi-product Lemonade customers represent 4.5% of total vs. 3.7% 18 months ago. That percentage is now nearing 10% of total customers in Illinois. That was the first state in which it had its entire product suite available.

f. Take

The stock may have tumbled nearly 30% following the report, but the company continues to surgically manage its balance sheet, growth and path to profits. It continues to prove itself to be a viable business and continues to lead the insurance industry’s customer service quality by a mile and a half. Headwinds will shift to tailwinds in 2024 and Lemonade will “step back on the gas pedal” to capture that opportunity. Expect continued demand re-acceleration, improving margins and no pressing balance sheet issues in 2024 thanks to its synthetic agents program. What else did you want? I’m pleased, yet still consider this too speculative and too far from profitability to make it a core holding. I added a little bit to my stake this week, but it will remain smaller for the time being.

2. Duolingo (DUOL) – Earnings Review

“We've been able to demonstrate that we can turn our incredible product into a profitable business.” – Co-Founder/CEO Luis von Ahn

a. Demand

Beat revenue estimates by 2.3% & beat revenue guidance by 3.1%. FX neutral (FXN) revenue growth was 43% Y/Y.

Duolingo English Test (DET) revenue rose 29% Y/Y; in-app purchase revenue rose 52% Y/Y; advertising revenue rose 21% Y/Y; subscription revenue rose 50% Y/Y.

Its 46.2% 3-year revenue CAGR compares to 44.8% Q/Q & 46.9% 2 quarters ago.

Beat bookings estimates by 13.0%. FXN bookings growth was 49% Y/Y.

Beat subscription bookings estimates by 16.0%.

Beat daily active user (DAU) estimates by 7.2%.

This is its fastest fourth quarter for sequential bookings and subscriber growth since going public in 2021. Ramping scale and accelerating growth make a fantastic and rare combination.

b. Profitability

Beat EBITDA estimates by 15.0% & beat guidance by 18.5%.

Beat GAAP EBIT estimates by 30.0%.

Beat $0.16 GAAP EPS estimates by $0.13 (so net income was an 80% beat).

For the full year, sales & marketing was 14% of revenue vs. 18% Y/Y; R&D was 37% of revenue vs. 41% Y/Y; G&A was 25% of revenue vs. 32% Y/Y. Gross margin rose a bit Y/Y in 2023 with expansion held back by lower advertising gross margin.

Duolingo generated $144 million in 2023 FCF, which rose 212% Y/Y.

c. Balance Sheet

$747.6 million in cash & equivalents.

No debt.

Diluted share count is expected to grow by just 1% in 2024. Comp dollars rose 29% Y/Y in Q4.

d. Annual Guidance & Valuation

Duolingo’s annual revenue guide was 3.3% ahead of expectations with its annual EBITDA guide 8% ahead of expectations. It expects ad revenue growth to remain challenged, subscription revenue growth to remain excellent, user growth to remain in the mid-50% range, DET growth to be lumpy but strong and in-app purchase growth to be lofty. It also sees an incremental EBITDA margin of 35% for the year, which is at the high end of its long term target. It will enjoy Y/Y leverage across all three OpEx cost buckets.

“Recent performance reaffirms our belief that we can achieve our long term bookings growth target of 25%+ and an EBITDA margin target range of 30%-35%.” – Co-Founder/CEO Luis von Ahn

Duolingo trades for 68x 2024 EPS with estimates set to rise in the coming weeks. EPS is expected to grow by about 45% Y/Y. It trades for about 45x 2024 FCF, with FCF set to grow by roughly 39% Y/Y.

e. Call & Letter Highlights

A Banner 2023 & a Thriving Formula:

Duolingo delivered accelerating user additions all year, rapid revenue growth, torrid margin expansion and exponential FCF growth. Was all of this from accelerating spend on external marketing? No, no it was not. Sales & marketing dollars spent were flat Y/Y in Q4 despite the 50%+ bookings growth. How is it doing this? While competition focuses on external marketing, DUOL focuses on constant product iteration and perfection. It obsessively split tests every aspect of its business to let small improvements to the interface add up over time. A wonderfully and increasingly engaging product is the end result. This was its mission from the beginning.

This approach, paired with delaying monetization similarly to the early Facebook model, allowed it to build a leading market share for online language learning. That leading market share has meant leading data scale to guide split testing, season its learning algorithms and ensure product efficacy and entertainment remain best in class. That’s why 90% of its user growth comes organically. It inserts itself in viral social media moments to affordably collect highly valuable impressions and leans on word-of-mouth to power its success.

For Q4 specifically, demand and profit strength were broad-based, geographically even and far better than expected across the board. Its family plan and successful New Year’s campaign were highlighted as two contributing factors.

2024 Priorities:

2024 will be more of the same for Duolingo, with a few new objectives. It will add engaging new lesson types like DuoRadio shows. This is one of the ways GenAI helps Duolingo’s model. It allows it to rapidly shrink the timeline to train this algorithm from years to months. GenAI continues to automate more pieces of its content creation to enhance the diversity of learning… and to diminish the costs associated with teaching. And aside from automating content creation, GenAI is also allowing it to debut newer tools like “Explain My Answer” to continue improving teaching efficacy. This will be a large 2024 objective as it looks to stay ahead of the innovation curve.

Another DUOL goal is to make the app more social, as that has been shown to directly boost engagement. That’s partially because of the family plan and how better social features also mean better communication between, for example, a caring mother and a child. With regard to the family plan, bookings rose 100% Y/Y while retention and lifetime value boosts remained intact. Still, just 18% of its overall subscribers are from this family tier, and the firm expects that to materially rise in 2024. It created a new family plan team towards the end of 2023 to nurture this momentum.

Other items for 2024 include experimenting with its three subscription tiers based on name, pricing and tooling. And overall, it will maintain a “relentless focus on improving the product and engagement.”

Advanced English Content:

80% of the global language learning market is in English. Duolingo doesn’t think its content is advanced enough for many English language learners. That’s now set to change with the introduction of 17 advanced English courses throughout the app. Since launching, usage of this content has been “up and to the right.” Besides offering more challenging content, Duolingo thinks it needs to get better at understanding how much learners already know when entering a course. This is easy for other languages, as pre-existing knowledge is more uniform compared to English. With English, widely ranging experience with the language makes that process more difficult. DUOL will lean on its Bird Brain algorithm to try to improve in this area. The Bird Brain model crafts lessons based on individual learners and their skill sets. Marketing spend will accelerate for these 17 new courses in 2024 to build awareness, with the financial impact ramping in 2025.

Duolingo Max:

We didn’t learn much about its newest subscription tier. All it told us is that it’s seeing “a lot of demand at higher prices for the offering.”

Math & Music:

A few months into launching Math and Music in the main app, Duolingo thinks its user base for these subjects is as least as large as any others. This will not show up in financials for 2024 as it continues to prioritize product-market fit. Monetization could likely begin in 2025. There will be many, many other courses after these two and its Duolingo ABC literature product.

Marketing King:

Duolingo’s Super Bowl commercial was 5-seconds long, internally-created and cost 10% of the average spend on a Super Bowl ad. It paid just over $1 per thousand impressions on this highly valuable slot. Who says Super Bowl ads are a waste of money?

f. Take

There’s nothing to pick at here… Only continued masterful execution to celebrate. This team has been perfect since going public; this was more perfection. This is clearly the language learning king. To be a 5x-10x from here in the coming years, it will need to be known as the online learning king overall. Language learning TAM alone is not large enough to foster decades of brisk compounding and to build the 100 year company it wants to be. It’s making steady progress with math and music, and I expect that progress to do nothing but pick up steam. So far… so great.

3. Cava & Sweetgreen – QSR Earnings Reviews

As many of you know, these are the two quick service names on my watch list. Here, we’ll explore both quarters and how they impacted my desire to start new positions in either.

The complete deep dives into both businesses can be found here.

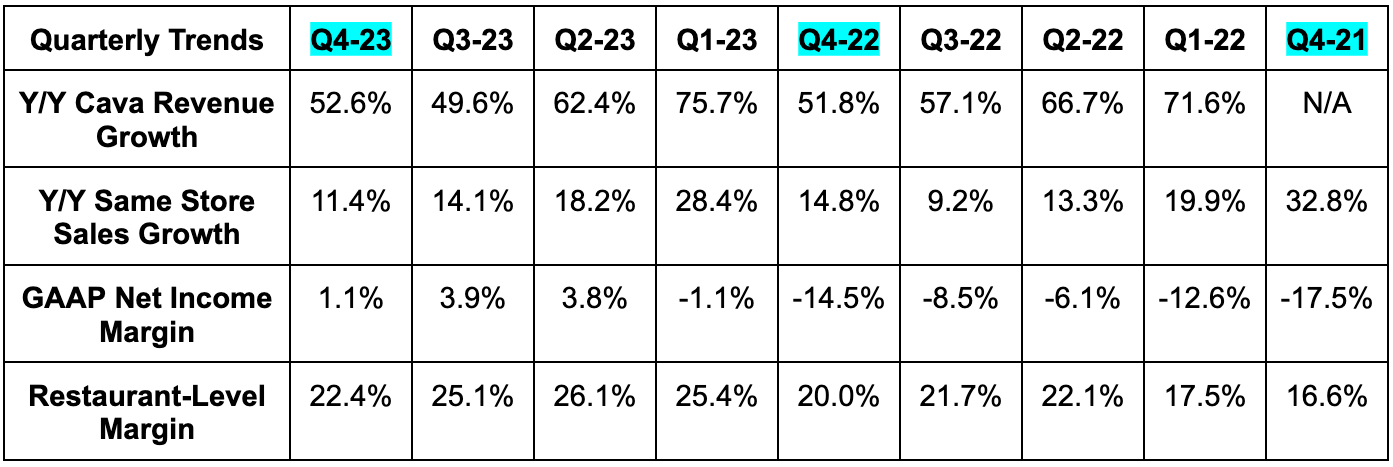

a. Cava (CAVA) Earnings Review

Results:

Beat revenue estimate by 0.7%.

Digital revenue was 35.9% of total sales vs. 35.5% Q/Q & 35.5% Y/Y.

Beat EBITDA estimate by 38%.

Beat -$2.6 million GAAP EBIT estimate by $5.4 million.

Beat $0.01 GAAP EPS estimate by $0.05.

Food, beverage and packaging costs were 28.8% of sales vs. 31.9% Y/Y. This was due to lower input costs and strong premium menu item mix. Labor was 27.8% of revenue vs. 27.3% Y/Y due to ramping investments in its talent. Occupancy was 8.3% of revenue vs. 9.3% Y/Y. This leaves us with the strong EBITDA margin expansion Y/Y, which was bolstered by “strong performance for new stores.” Finally, for the full year, Cava generated $97 million in operating cash flow vs. $6 million Y/Y.

Note that 11.4% same store sales growth was via 5.2% price hikes and 6.2% traffic growth. Traffic growth is expected to slow to a low single digit % in 2024 as comps get much tougher.

Balance Sheet:

$340 million in cash & equivalents.

$75 million undrawn credit revolver.

No debt.

Exponential Y/Y share growth due to the IPO.

Guidance & Valuation:

Annual EBITDA guidance is 9% ahead of estimates. Its $89 million EBITDA guide implies 20.6% Y/Y growth and moderate margin expansion for 2024.

For 2024, it expects to open 50 stores (11 already opened in 2024) and 3-5% same store sales growth. The 3-5% same store sales growth guide includes 3% price hikes and 0%-2% traffic growth following historically strong 10%+ traffic growth in 2023.

Finally, for 2024, it expects a 23.0% restaurant-level margin. That guide compares to 24.8% for 2023. The contraction is as previously telegraphed and as expected. Why? Cava stores over-earned a bit in 2023 and into Q4 as well. As we discussed in the deep dive, rapid same store sales growth means better labor leverage, better fixed cost utilization and less waste on a temporary basis (premium item outperformance helped too). It takes time for Cava to add the stores, capacity and talent needed to catch up to spiking same store growth. Catch-up investments have now taken place while Cava also expects a 120 bps headwind from new labor initiatives. New California labor laws discussed later are adding more pressure. Corporate-level operating scale and efficiencies are why its EBITDA margin will expand in 2024 while this margin line doesn’t. Restaurant-level margin focuses exclusively on stores, not the overall company.

Cava trades for 75x 2024 EBITDA. EBITDA is expected to grow by 22% Y/Y.

Call & Release Highlights:

Real Estate:

Cava had a fantastic year with footprint expansion. It rapidly grew store count as it continued converting locations from the Zoe’s acquisition. Those conversions are now complete, with the chain adding 72 locations for the year to reach 309. This will require a lot of new real estate opportunities to continue fueling its guidance of 15%+ annual unit growth. Cava got ahead of this potential bottleneck and built a cushion into its real estate pipeline to diminish the risk of any delays from permits and equipment availability. Because of this, it will have no trouble meeting its unit growth target for 2024. And for 2025? It’s already hard at work scouting out new locations. Great team.

Upgrading Channels:

Cava debuted its revamped loyalty program this quarter. All members are now onboarded into the new app, with more intuitive and easier means to earn points. The program also seamlessly integrates digital and physical ordering environments. Cava is now experimenting with different forms of rewards in a few test markets. These experiments are going well, so they will expand to more markets this quarter and should be rolled out nationally by year’s end. It also plans to accelerate catering growth now that the microservices initiative (discussed in detail in the deep dive) is complete. For in-store, it discussed Project Soul. This is the next iteration of its physical store design with a “more inviting space” for in-person dining. All of these programs are expected to drive same store sales growth and keep traffic churning.

“We noted broad-based same restaurant sales strength across vintages, regions, and both suburban and urban locations.” – CFO Tricia Tolivar

Virginia Factory:

Cava’s construction on its second production facility in Virginia is now complete. The two facilities combined will support up to 750 stores and its CPG expansion efforts. These factories will produce dips and spreads, which removes those tedious tasks from in store work and improves end product consistency.

Final Notes:

Cava debuted new food safety protocols this quarter and moved to a new 3rd party auditor for food safety with stricter rules too.

Cava will forgo incremental menu price hikes in California following the passing of new legislation there, which mandates a $20 per hour minimum wage for fast food workers. This will be a 30 bps restaurant-level margin headwind for 2024.

Cava ended the year with 55 Academy GMs to train and groom its next crop of store leaders. It also filled 75% of its open GM roles internally in 2023. It continues to intentionally foster a culture promoting internal career mobility and fair wages/benefits. Its employee net promoter score (NPS) set new records (per Denison Consulting) as a result.

Take:

Great quarter; great team; great company. Great. Still too expensive for me to want to own this name. The lofty price tag is the sole factor keeping me out of Cava.

b. Sweetgreen (SG) – Earnings Review

“We ended the year with increasing momentum giving us optimism for the year ahead.” – Co-Founder/CEO Jonathan Neman

Results:

Beat revenue estimates by 0.7% & beat revenue guidance by 2.7%. Its 26% 2-year revenue CAGR compares to 27.0% Q/Q & 33.0% 2 quarters ago.

Digital owned revenue was 34% of total vs. 40% Y/Y.

Sweetgreen had 221 stores at year’s end vs. 186 Y/Y for 18.8% growth. It has opened 4 stores so far this quarter.

Beat restaurant profit guidance by 15%.

Beat -$0.27 GAAP EPS estimates by $.03.

Beat -$4.3M EBITDA estimates by $2.2M & beat guidance by $2.5M. For the full year, it lost $2.8 million in EBITDA vs. -$49.9 million in 2022.

Annual Guidance & Valuation:

Revenue guidance beat by 0.1% while its $10.5 million EBITDA guidance beat by $1.0 million. It will open 25 new stores in 2024 representing 11.8% Y/Y growth. It expects 3%-5% same store sales growth and an 18.75% restaurant level margin vs. 17.5% in 2023. It sees stock comp falling to about $35 million in 2024 and $15 million in 2025 vs. nearly $80 million for 2022.

“After a sluggish October, our momentum increased each month in the quarter… January was impacted by weather throughout much of the country. As weather has normalized, our sales trends have strengthened.” – CFO Mitch Reback

Balance Sheet:

$257 million in cash & equivalents.

No debt

Share count rose by 1.4% Y/Y.

Call & Release Highlights:

Infinite Kitchen:

Infinite Kitchen is Sweetgreen’s automated robotics technology to greatly improve store workflows and reduce manual labor. It now has 2 Infinite Kitchens installed, with plans to add 10-11 in total in 2024 between new openings and retrofits. Ideally, it could go faster as this positive evidence builds. Otherwise, the margin benefit will take years to play out. The 2nd Infinite Kitchen in Huntington Beach added to leadership’s conviction that this tech is highly margin accretive. The quicker, more uniform customer service is also boosting average ticket size by 10%+ while diminishing employee churn.

It thinks Infinite Kitchens cost about $500,000 to implement and yield a 700 bps boost to its restaurant-level margins. That was a brand new disclosure, which analysts had been looking for. Based on a $2.9 million average unit volume (AUV), this leaves us with a payback period of just under 2 years. It has a clear path to a 20% restaurant-level margin without this program, with more upside as these robots are added to stores. The somewhat cumbersome process of adding these to stores is leading to SG slowing new location openings from 35 to 25 in 2024. This plan will avoid some retrofitting costs before the company re-accelerates location growth in 2025. That slowing is already playing out with SG opening just 1 new store in Q4.

Traffic Initiatives:

Sweetgreen’s 1% Y/Y store traffic growth returned to positive territory this quarter. A 5% price hike represented the rest of the same store sales growth.

Its culinary innovation continues to work. Protein plates, which debuted in October, are still exceeding internal expectations for mix shift. These are directly boosting the percentage of its revenue coming from dinner. It plans to lean into advertising spend in 2024 while maintaining G&A leverage.

Footprint:

Sweetgreen successfully entered Milwaukee, Tampa and Rhode Island in 2023. It’s pleased with all three launches and is happy with the performance of these units. That is important considering some batches of its pandemic-era openings have fallen short of targets. In 2024, it will enter Seattle. It’s already opened one of the planned new stores and it is performing “in line with top urban locations.” That’s notable because the location is in a suburb where AUV is generally lower than in dense cities.

Costs for the year:

Food, beverage and packaging was 28.4% of 2023 sales vs. 29.2% Y/Y.

Labor and related was 29.3% of 2023 sales vs. 32.2% Y/Y.

Occupancy was 9.3% of 2023 sales vs. 10.2% Y/Y.

G&A was 23.2% of 2023 sales vs. 36.7% Y/Y as it controls stock comp and support center costs.

Take:

This is the best quarter Sweetgreen has posted in a long time. It was free from operational blunders and executional drama. That’s exactly what I wanted. It takes more than one quarter to establish a trend and will take more than one quarter for my confidence and trust in the team to build. For now, I will keep it on the watch list with more interest than I had a week ago.

4. Earnings Round-Up – Hims, Workday, Okta & Axon

a. Hims (HIMS)

Results:

Beat revenue estimate by 0.3% & beat guide by 0.4%.

Beat EBITDA estimate by 33% & beat same guide by 33%.

Beat 82.0% GAAP GPM estimate by 70 bps.

Other income was the source of the positive GAAP EPS.

Annual Guidance & Valuation:

Revenue guide beat estimates by 8%.

EBITDA guide beat estimates by 47%.

Hims trades for 35x 2024 EPS and 100x 2024 GAAP EBIT. EPS will rise by 62.4% Y/Y and GAAP EBIT will inflect positively.

Balance Sheet:

$225M in $ & equivalents.

No debt

Basic shares +2.7% Y/Y; diluted shares +7.6% Y/Y.

b. Workday (WDAY)

Results:

Met revenue estimate and beat revenue guide by 0.6%.

Met subscription revenue guide.

Beat EBIT estimate by 2.0% & beat guide by 2.5%.

Beat $1.47 EPS estimate by $0.10.

Annual Guidance & Valuation:

Reiterated annual subscription revenue guidance & reiterated 2024 EBIT margin leverage guidance.

WDAY trades for 43x fiscal 2025 EPS and 40x fiscal 2025 FCF. EPS is expected to grow by 14% Y/Y. FCF is expected to be roughly flat Y/Y.

Balance Sheet:

$7.8B in cash & equivalents; $3B in debt.

Basic shares +2.3% Y/Y; diluted shares +4.5% Y/Y.

c. Okta (OKTA)

Results:

Beat revenue estimate by 3.0% & beat revenue guide by 3.2%.

Beat EBIT estimate by 25.1% & beat EBIT guide by 25.1%.

Beat $0.51 EPS estimate by $0.12; Beat FCF estimate by 63%.

Annual Guidance & Valuation:

Revenue beat by 1.2%.

EBIT beat by 8.3%.

$2.26 EPS guide beat by $0.29.

Okta trades for 48x 2024 EPS. EPS is expected to grow by 41.3% Y/Y.

Balance Sheet:

$2.2 billion in cash & equivalents.

$1.2 billion in senior notes.

d. Axon (AXON)

Results:

Beat revenue estimate by 2.6% & beat revenue guide by 3.2%.

Beat EBITDA estimate by 7.3%% & beat EBITDA guide by 8.7%.

Beat GAAP EBIT estimate by 2.5%.

Beat $0.85 EPS estimate by $.27.

Beat $0.49 GAAP EPS estimate by $0.26.

Annual Guidance & Valuation:

Annual revenue guidance was 1.6% ahead of expectations while annual EBITDA guidance was 1.7% ahead of expectations.

Axon trades for 52x 2024 EBITDA and 72x 2024 EPS. EBITDA is expected to grow by 31% Y/Y with EPS expected to grow by 29.7% Y/Y.

Balance Sheet:

$1.3B in cash & equivalents.

$677 million in convertible senior notes

Diluted shares rose 4.4% Y/Y.

Basic share rose by 0.3% Y/Y.

Do you love Twitter (sorry, not X) as much as I do? Do you only want investing-related content on that app? Do you get frustrated by all of the noisy content you scroll through to find the nuggets you actually care about? Same! Blossom is here to fix that. This is focused FinTwit meets serious investors meets portfolio tracking. It’s a thriving social media platform for us nerds and it just launched in the USA. It’s entirely free to use and something that I now post on daily. Check it out here and sign up. See ya there.

5. SoFI (SOFI) — CFO Interview

On the Outlook:

All 2024 and 3-year guidance was reiterated. As a bit of an update, CFO Chris Lapointe did tell us that debit interchange revenue “continued to accelerate” into Q1. It’s gearing up for double digit Q/Q growth for that high margin financial service as unaided brand awareness continues to briskly rise and SoFi continues to delight end users. Good news for both the revenue and profit contribution of that segment. Other tailwinds like the re-opening of the IPO market and alt investments will help more in 2024 too.

It also expects to continue enjoying material operating leverage across all cost buckets in 2024. This includes sales & marketing, where building brand awareness has meant diminished CAC. Strong cross-selling trends are pulling CAC down further. When pairing these factors with stock comp leverage, headcount leverage, finishing the expensive Galileo cloud migration & more, that’s how SoFi already expects to be at its long term EBITDA margin target by end of year. Notably, the EPS CAGR from 2023-2026 DOES NOT rely on a 0% effective tax rate through 2026. SoFi expects to use the tax benefit from historical operating losses in 2024. Its effective tax rate will normalize thereafter.

Lending Outlook & Balance Sheet:

Lapointe reiterated how nimble SoFi’s operations and capital allocation approach both are. Still, he told us that it would “take a lot” of positive change to its macro assumptions to “throttle up” lending growth in 2024. It wants a lot more clarity here with rates and economic health. It doesn’t see this clarity coming in 2024. That’s why tech & fin service growth as a % of the overall business is so important. Those two segments are not as cyclical as lending.

As an aside, I think SoFi’s Lantern product is highly underrated. This is its loan referral marketplace that allows it to monetize rejected applicants. Lending appetite will shrink in 2024 for SoFi as it takes a conservative macro view. But? Lantern means that it can still take advantage of robust demand elsewhere… without assuming lower quality credit risk. Let Pagaya do it for you.

My favorite quote on the call was Lapointe telling us that “demand from borrowers is better than we’ve seen over the last few years.” Still, it doesn’t expect to use its excess balance sheet capacity on this excess demand in 2024 due to the pessimistic lending outlook. It sees its risk-based capital ratio staying above 14% this year, vs. the 10.5% regulatory minimum.

There’s plenty of balance sheet optimization left to do for SoFi to juice its net interest margin. It has about $6 billion in warehouse-funded loans that it can replace with lower cost deposits over time. This shift, along with its coupon pricing power in excess of benchmark rate movement, will allow NIM to remain over 5% in the years ahead. The banking charter continues to deliver a large reduction in cost of capital… despite offering a best-in-class APY on deposits used to fund loans. Specifically, SoFi pockets 200 bps when using deposits to fund loans vs. warehouse credit. That lead continues to grow and means about $400 million in excess margin. This is the beauty of connecting a thriving direct deposit business with a lending business. This is the beauty of the charter.

Credit Quality:

SoFi continues to expect life of loan loss rates to peak at 7%-8% in 2024. It has been telling us this for years; it is sticking to this promise. Some of its worst-performing credit will roll off the book this year, while its loss rates are holding up better than for most. That’s what gives it confidence that 7%-8% represents a peak… despite this assumed peak including an overly negative macroeconomic forecast.

Tech Platform:

Not much was discussed on this topic today. It has had “great success” over the last few quarters with winning new customers. It completed a proof of concept with a top 5 U.S. bank and the Experian partnership is “progressing nicely.” Galileo is also now in 17 countries throughout the Americas. The team “couldn’t be more excited about the customer pipeline” and is confident in the growth re-acceleration that it has told us to expect.

6. Disney (DIS) – India

Disney and Reliance have completed their media merger. Disney will own 37% of the combined entity with Viacom18 owning 47% and Reliance 16%. Disney was struggling there. It was bleeding cash and subscribers. Reliance had outbid it for key cricket rights & a lot more. Now they're teammates. The merger could morph DIS's India operations from a cash incinerator into an actually positive piece of the business. That nation is highly compelling in terms of its massive and growing population, growing middle class and business-friendly government. This is a much more rational approach to the large opportunity.

7. Market Headlines

PayPal named Geoff Seeley as its new Chief Marketing Officer. He was Cash App’s chief marketing officer before this move and has also been Airbnb’s head of marketing. Good hire.

Uber introduced spending limits for its new teen accounts.

Apple ditched efforts to build a car. It’s focusing more on AI.

8. Macro

Inflation Data:

The Personal Consumption Expenditures (PCE) index for January rose by 0.3% M/M as expected and vs. 0.1% last month.

The Core PCE index for January rose 0.4% M/M as expected and vs. 0.1% last month.

The Core PCE index for January rose 2.8% Y/Y as expected and vs. 2.9% last month.

Consumption & Employment Data:

Net home sales for January were 661,000. This compares to 680,000 expected and 651,000 last month.

Initial Jobless claims were 215,000. This compares to 209,000 expected and 202,000 last report.

Personal Spending rose 0.3% M/M for January as expected. This compares to 0.1% growth last month.

Output Data:

Core Durable Goods Orders for January fell by 0.3% M/M. This compares to 0.2% growth expected and a 0.1% decline last month.

Durable Goods Orders for January fell by 6.1% M/M. This compares to a 4.9% decline expected and a fall of 0.3% last month.

Chicago’s Purchasing Managers Index for February was 44.0. This compares to 48.1 expected and 46.0 last month.

GDP for Q4 is currently sitting at 3.2%. This compares to 3.3% expected and 4.9% last quarter. GDP should keep falling as the benefits of supply chain recoveries fade.

9. Portfolio

I added to Lululemon, Lemonade and Progyny this week.

Hi Brad, Any thoughts on turnaround story for $AAP AutoParts, I know its not you style or comfort zone but it looks turn around story with new management? Any chance you have a look to it?

f. Take:

Outstanding reviews and commentary!