News of the Week (March 18 - 22)

News of the Week (March 18 - 22)

Lululemon; Nike; Adobe; The Trade Desk; Disney; Progyny; Apple; SoFi; Market Headlines; Macro; Portfolio

Today’s Article is Powered by my Favorite Brians Over at Long Term Mindset:

1. Lululemon (LULU) – Earnings Review

a. Demand

Lulu beat revenue estimates by 0.3% and beat revenue guidance by 1.6%. Its 22.8% 2-year revenue compounded annual growth rate (CAGR) compares to 23.2% Q/Q & 23.3% 2 quarters ago.

Americas revenue was 81% of total vs. 86% Y/Y and rose 7% Y/Y.

China Mainland revenue was 9% of total vs. 6% Y/Y and rose 56% Y/Y.

Rest of World revenue was 9% of total vs. 8% Y/Y and rose 32% Y/Y.

For the full year, Women’s revenue grew by 13% Y/Y, men’s grew by 15% & accessories by 40%.

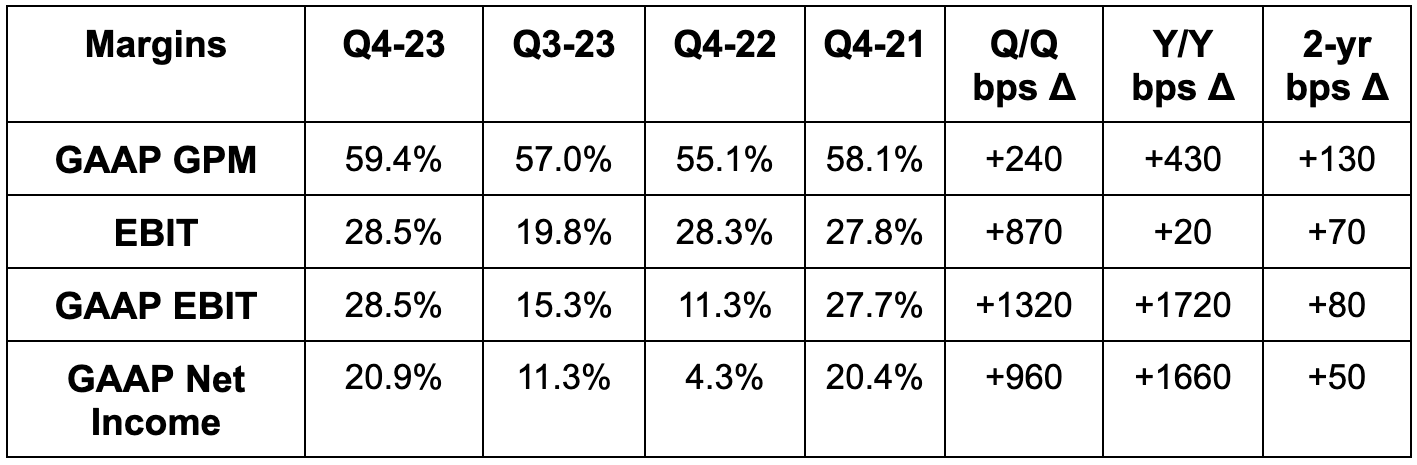

b. Profits

Beat $5.02 GAAP earnings per share (EPS) estimates by $0.27 & beat guidance by $0.40.

Beat GAAP gross profit margin (GPM) estimate by 70 basis points (bps; 1 bps = 0.01%).

Beat GAAP earnings before interest & tax (EBIT) estimates by 2%.

Operating margin rose 110 bps Y/Y in 2023; EPS rose by 27% Y/Y in 2023.

c. Balance Sheet

$2.2 billion in cash & equivalents.

Inventory fell 9% Y/Y.

Share count fell 1% Y/Y.

$400 million in available credit capacity.

d. Guidance & Valuation

Lulu’s annual revenue guidance missed by 1.7% while its $14.10 EPS guidance missed by $0.16 (or 1%). It reiterated its 2026 financial targets and even hinted at doing a bit better than them. The EPS guide excludes potential benefits of share repurchases, but that would likely only add a penny or two to the result. Other annual guidance notes include:

Flat Y/Y gross margin.

10 bps of EBIT margin leverage. This implies a 23.3% margin vs. 23.1% expected for a moderate beat. EBIT margin will be down in Q1 due to brand marketing investments discussed in the next section.

LULU will open 5-10 stores in the U.S. (15-20 optimizations too) and 35-40 elsewhere (mostly in China).

Inventory levels will fall through the first half of the year and resume modest growth during the second half.

Marketing will be closer to 5% of total sales vs. 4.5% in 2023.

Lululemon expects to be a 15% revenue compounder over the long haul. In 2023, overall revenue grew by 18.6% Y/Y. This will lead to tough comps that get progressively easier throughout the year. This will happen while the inventory missteps are quickly addressed, but it baked little U.S. traffic recovery into annual guidance as this happens. For these reasons, the team’s fantastic track record & overall language surrounding guidance, I expect consistent beats and raises throughout the year. I don’t think guidance was sandbagged quite as aggressively as for Snowflake or PayPal; I do think it involves some modest under-promising amid a fluid backdrop.

Lululemon trades for 28x 2024 earnings. Earnings are expected to grow by 11.5% Y/Y.

e. Call & Release Highlights

More on Slightly Weak Guidance:

Quarter-to-date weakness for Lulu has been exclusively felt in the USA. It has been broad-based across categories, genders and geographies. All international markets are showing strength, but the U.S. is seeing softening consumer behavior. Part of this weakness was related to leadership’s execution. It didn’t have the sizing or color assortments that its customers wanted in its stores, which hurt traffic and conversion rates. While this isn’t ideal, it’s already being addressed. Lulu has restocked accordingly and, again, expects U.S. traffic growth to slightly improve throughout the year as a result. It sees more fabric and product-level innovation driving this as well as early signs of strength for its spring gear. It continued to take more market share in the U.S. and fully expects that to continue in 2024. Share gains show this to be more macro-based than anything.

Lulu’s balance sheet, margins and brand opportunity will allow it “to keep playing offense” in the U.S. while others retreat. Brand awareness is still low across all markets and its outperformance vs. competition is firmly intact. Its stores are also among the most productive in the category. The company remains well ahead on its path to realizing 2026 financial targets, and the team “doesn’t see that changing.”

Membership Program:

Its Essentials Membership Program crossed 17 million members just one year into its launch. Spend and lifetime value objectives have been enjoyed as expected. As this grows, Lululemon will become an increasingly powerful and highly targeted marketing outlet to leverage. The marketing department did so this past holiday season, with exclusive promotions for members. That prompted 250,000 incremental downloads without a boost to marketing spend.

Footwear & Innovation:

Lulu hosted a footwear launch event in February to drive category momentum. It was “pleased with the initial reaction” overall, but especially pleased with its “cityverse” men’s casual shoe. The product is “exceeding expectations” and Lululemon is adding inventory to address the outperformance. The company also hosted its “Further Event,” which showcased 10 athletes setting new personal records for distance run (in their Lulu shoes).

New men’s golf fabric coming this year along with more Soft Jersey styles and more. It has also struggled to keep Soft Jersey inventory fully stocked, but will address that issue in the coming weeks.

Adding more fabrics to the men’s ABC Jogger franchise.

Reporting Changes:

Going forward, Lululemon will report revenue by geography, rather than by channel. It will split reporting segments into the Americas, China and Rest of World.

Margins:

Gross margin was greatly helped by ocean and air freight costs. Markdowns were flat Y/Y, fixed cost leverage was a bit better than expected and the foreign exchange (FX) impact was 10 bps better than expected too. SG&A was 30.9% of sales vs. 29% Y/Y as it got more aggressive with brand investments. More depreciation from 2022 and 2023 distribution center investments weighed on operating and net margins, while savings from winding down its Mirror projects helped.

f. Take

I found this quarter to be disappointing. Lululemon is a consistently stellar performer, but this was not stellar. To the team’s credit, it did tell us about U.S. weakness surfacing on last quarter’s call. Despite that, weakness has been more durable than analysts (and myself) expected as it leaks into the new fiscal year. I also didn’t like the inventory scarcity missteps, but do like that they were quickly addressed.

One quarter doesn't make or break an investment. Near-dramaless excellence has been a cliche for this firm long before I started covering it. That long track record of success pushes me to be more forgiving amid a moderately poor showing (v. expectations) like this was. I expect performance to improve in Q1 and throughout 2024 and I added to my stake after the report. Still, the multiple compression needed to justify me adding again have widened a bit following this blunder. That could easily revert if next quarter goes as I expect it to.

2. Nike (NKE) – Earnings Review

a. Results

Beat revenue estimate by 1.1% & beat its revenue guidance by about the same amount.

Beat $0.71 GAAP EPS estimates by $0.06. GAAP EPS included $0.27 ($405 million) in restructuring charges for the quarter.

Ex-restructuring, EPS rose 24% Y/Y.

There will be restructuring charges in Q4, but a much smaller amount.

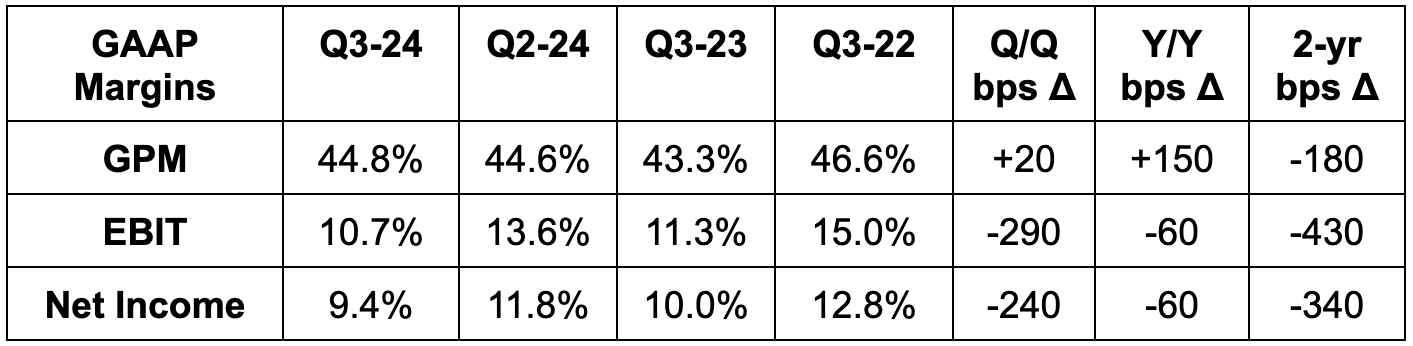

Missed gross margin estimates by 30 basis points (bps; 1 bps = 0.01%) and its guidance by 20 bps.

Strategic pricing and logistics disinflation powered gross margin expansion.

Beat GAAP EBIT estimates by 2.3%.

Sales, General & Administrative (SG&A) costs rose by 7% Y/Y with most of that driven by 10% growth in “demand creation expense.”

b. Balance Sheet

$10.6 billion in cash & equivalents.

$8.9 billion in total debt.

Share count fell by 2% Y/Y. $10 billion left in buyback capacity.

Dividends rose 6% Y/Y.

Inventory fell by 13% Y/Y. Nike reached its lowest levels since 2020.

c. Guidance & Valuation

This year’s updated guidance:

Reiterated 1% Y/Y revenue growth vs. 1.1% Y/Y growth expected.

Reduced ex-restructuring SG&A spend from low Y/Y growth to no growth.

Maintained GPM expansion guidance of 150 bps.

For next year, Nike expects revenue to grow and EBIT margin to expand. Both vague items are roughly as expected.

Nike trades for 24x next 12 month earnings. Earnings are expected to grow about 12% Y/Y during that period.

d. Call & Release Highlights

“We know Nike is not performing in line with our potential. It’s clear we need to make some important adjustments” – CEO John Donahoe

Making Adjustments – Product Newness & Innovation:

Earlier in the fiscal year, Nike made the decision to wind down supply of some legacy franchises and focus on innovation. For example, it cut older Pegasus shoe models to focus on upcoming launches. It accelerated its product roadmap by a full year and set out to vastly tighten and improve its brand storytelling, with an added emphasis on sports. The early reception has been positive to a point of “accelerating these actions” even further.

One key franchise focus will be Air. Nike will soon roll out a new air chamber to enhance the comfort and natural fit of the lineup and this tech will eventually be used across most Air models. Nike continues to see new Air launches work while these launches also improve demand for the rest of the existing product line. This $10+ billion franchise was a vital part of Nike’s past, and that will not change going forward. As evidence of shoe innovation working, most of its 20 top sellers are either relatively new or recently updated models.

Nike’s direct-to-consumer (DTC) business will be the main channel focus. It will still work closely with its wholesalers to refresh their inventory, elevate its brand presence, and grow its overall market.

“Our product portfolio will go through a period of transition over the coming quarters. But altogether, we are relentlessly focused on driving NIKE's next chapter of healthy and sustainable growth.” – CEO John Donahoe

Making Adjustments – Sharpen Organizational Focus:

Nike conducted a broad restructuring in June to reduce redundant costs and reallocate the savings back into its highest priorities. It also reshuffled its support and operational teams this quarter to streamline middle-management layers. Meta, Google and many other companies have done the same over the last couple years. It’s reducing the breadth of its brand story-telling and investing in only its highest impact marketing themes.

“Restructuring our organization to sharpen our focus, we believe, will fuel our next phase of growth.” – CEO John Donahoe

Geographic Performance:

Nike’s quarter was the polar opposite of Lululemon’s. Nike’s results for the quarter were strongest in North America, in line in China, and weak in Europe. It blamed Europe weakness on macro volatility and softening consumer demand. Lighter markdowns and a strong holiday season in North America drove the outperformance here.

North American revenue rose 3% Y/Y with EBIT up 18% Y/Y.

EMEA revenue fell 4% Y/Y with EBIT down 6% Y/Y.

China revenue rose 6% Y/Y with EBIT up 3% Y/Y.

e. Take

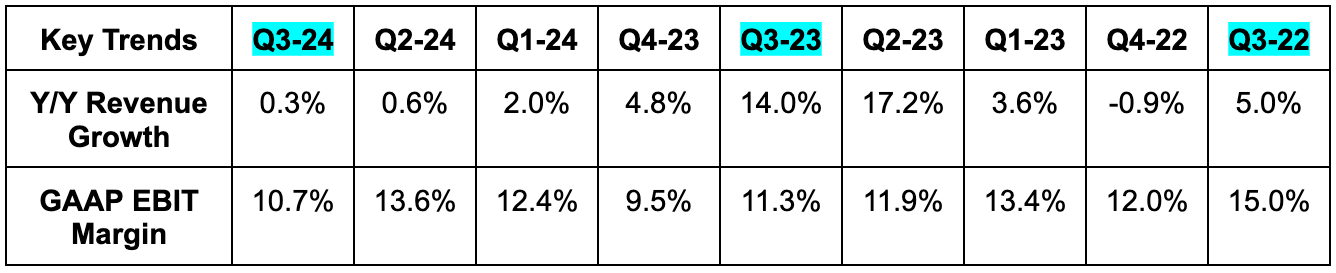

Nike continues to work through a difficult product refresh transition. Its guidance assumes negative revenue growth for the first half of the year, which is a disappointment. That will mean about 18 months of flat Y/Y revenue growth. This is still an iconic brand and still has significant potential to make results look better. I reject the notion that On Running and Hoka are rapidly ruining its competitive edge and moat. I just think this team needs to execute better and likely needs a bit of macro cooperation too.

Long-Term Mindset is a FREE weekly newsletter emailed each Wednesday. Each issue contains five pieces of timeless content to encourage you to think long-term. All issues can be read in less than 1 minute. There’s a reason why we are consistent readers and think you should be too. Subscribe here.

3. Adobe (ADBE) – Earnings Review

Adobe is a software giant that invented the .pdf file (co-founder John Warnock specifically). It provides programs to create and imagine, handle customer interactions and process documents. Revenue is split into two main buckets: Digital Media and Digital Experiences. Digital Media is made up of its “Creative Cloud” and “Document Cloud.” The Creative Cloud includes Photoshop and Illustrator. It’s what empowers creation, iteration and perfection of digital design. The Document Cloud, including the ubiquitous Adobe Acrobat, allows for secure PDF management and collaboration – among other things.

Finally, its Experience Cloud includes Adobe Analytics and other products like “Campaign.” Campaign is its (intuitively-named) marketing campaign tool. Experience Cloud covers end-to-end customer interactions with a real-time customer data platform (CDP) to ensure those interactions are optimized. It also publishes some greatly appreciated macro data on overall commerce spend.

a. Demand

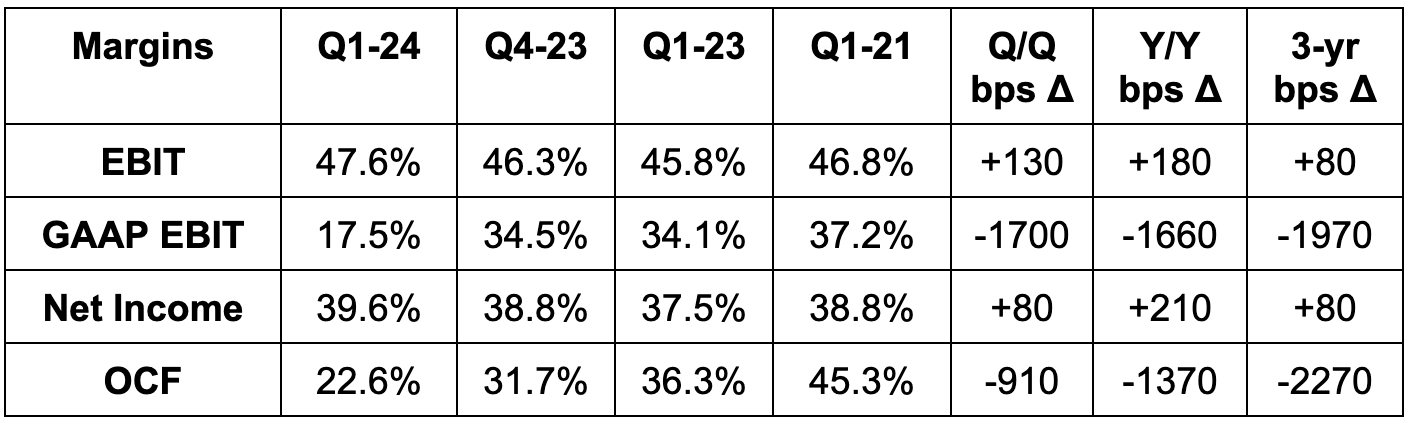

Beat revenue estimates by 0.6% & beat guidance by 1.0%. Its 9.8% 3-year revenue CAGR compares to 13.9% as of last quarter & 14.8% 2 quarters ago.

Beat Digital Media net new annual recurring revenue (NNARR) guidance by 5.4%.

Beat digital media revenue guidance by 0.9%.

Creative Cloud revenue rose 11% Y/Y; Document Cloud revenue rose 18% Y/Y.

Beat digital experience revenue guidance by 0.8%.

Remaining performance obligations (RPO) rose 16% Y/Y to point to strong forward-looking demand.

“We are successfully monetizing our innovations with particular strength in Q1 in the enterprise segment across our Digital Media and Digital Experience businesses. This strength is reflected in our strong RPO growth of 16 percent year over year.” – CEO Shantanu Narayen

b. Profits

Adobe beat $4.38 EPS estimates & its identical guidance by $0.10 each. EPS rose by 18% Y/Y. It sharply missed GAAP EPS estimates. GAAP net income & cash flow margins were hard hit by a $1 billion charge related to Figma M&A termination. There was less of a GAAP EBIT hit as the charge was largely incurred on the tax line. Excluding this, GAAP EPS was $3.55 vs. $3.37 expected. Operating cash flow (OCF) margin would have been 42.0%.

c. Balance Sheet

$6.9B in cash & equivalents.

$3.6B in debt.

Share count fell slightly Y/Y. Authorized a sizable $25 billion boost to its buyback capacity (nearly 10% of the market cap).

d. Valuation & Guide

No full year guidance offered in the presser this quarter. It doesn’t always update annual guidance during the FY Q1 call, but it has in the past.

Q2 revenue guidance missed estimates by 0.6%.

Q2 GAAP & non-GAAP EPS guides roughly met estimates.

e. Call & Release Highlights

Digital Media – Document Cloud:

Acrobat Web Monthly Active Users (MAUs) continued to grow at a robust 70% Y/Y clip to cross 100 million this month. Slick Microsoft Edge and Google Chrome extensions are helping drive paid conversions, while its Acrobat Mobile product is helping too. The company is steadily making document collaboration and link sharing much more intuitive. This drove 300% Y/Y growth in PDFs sent using these tools.

Its newer GenAI “Acrobat AI Assistant” should be a compelling growth driver going forward. It conjoins Adobe’s Firefly (GenAI model series) with its massive data scale to unleash real-time document summaries, conversational querying and automated report generation. I’ve said it before and I will keep saying it: GenAI models are a dime a dozen without a data edge to train those models better than others can. GenAI favors incumbents with scale. That is Adobe. The AI assistant intuitively integrates with its Reader workflows to drive more use cases. This is currently in beta testing and will fully roll out this year. It will be monetized via “monthly add-on offerings.”

Digital Media – Creative Cloud:

Adobe Express (used to be called Adobe Spark) makes content creation easier across channels. It has a deep content library for clients to use and detailed tools to customize its plethora of design templates. Adobe Express for Web also innately ties its Firefly AI models into workflows to automate tedious parts of content creation. The combination of Creative Cloud and Firefly freed IBM to shrink the creation of 1,000 marketing variations down from months to minutes with a 26x boost to engagement vs. benchmarks. Powerful stuff.

Customers are free to customize and build on top of these modes to leverage their own data and natively integrate these services into their own, internal workflows. Adobe Express for Mobile is now in beta testing to emulate these same perks on our phones. It sees this debut and the innovation engine driving accelerated adoption over the coming quarters. Its Firefly-powered GenAI Photoshop, Generative Fill and Generative Expand tools reached their highest engagement levels since the May 2023 launch, evidencing this traction.

Adobe and TikTok announced a new partnership to make content creation on that platform easier.

It’s testing AI-powered enhanced speech, GenAI music models, new editing tools and “auto-dubbing” models for video creation.

Won Nintendo, Accenture and Starbucks for this segment during the quarter.

GenAI advances drove a quarterly record for new Creative Cloud subscriptions.

“You can expect to see the product advances here drive ARR acceleration in the second half of the year.” – President of Digital Media David Wadhwani

Digital Experiences – Adobe Experience Platform (AEP):

Adobe was named a leader in Digital Experiences by Garnter for the 7th straight year and by Forrester for the 4th straight year. Momentum for AEP and its native apps led to that bucket crossing $800 million in annual revenue. Budget scrutiny is leading to customers prioritizing marketing agility and best-possible customer interactions. Adobe’s end-to-end customer experience management (CXM) and real-time CDP allow it to provide clients with a detailed view of each individual customer across channels. This drives better segmentation, better targeting and better return on ad spend (ROAS). Tools like its Journey Optimizer, for example, help ensure client touchpoints are tasteful, timely and relevant. Its GenStudio app combines all aspects of content creation under one umbrella to expedite creation further. For this segment , GenAI is exponentially bolstering content variation potential, making every marketing campaign and customer interaction feel deeply personal – at an immense scale.

Later this month, Adobe will unveil new experience models, a new AEP assistant and more at its Adobe Summit.

f. Take

This was a fine quarter. Nothing to be overly excited or concerned about for shareholders. I didn’t love the annual guidance removal, but it has done so before in the past while annual results shaped up to be fine. The first wave of GenAI monetization is happening at the chip, server and infrastructure equipment layers. The next wave will likely involve consumer apps stemming from this wave. The apps need this foundation to be laid before being brought to market. This is why SMCI and Nvidia are the clearest present examples of direct financial GenAI benefits. Those benefits, in my view, will greatly spread over time. Adobe is poised to capture its fair share. For now, we have steady double-digit top-and-bottom-line compounding and more wonderfully boring execution.

4. The Trade Desk (TTD) – NBC & Disney

a. NBC

Through an NBC Universal partnership, 2024 Olympic advertising inventory will be available on TTD’s platform. Why does this matter? Live sports dominate the hearts and minds of our species. The Olympic games trail perhaps only soccer in terms of global appeal. This provides yet another programmatic growth lever to bolster TTD’s momentum. It will also allow the firm to showcase its superior ROAS outcomes to prospective clients in less tapped global markets. Monumental? No. Irrelevant? Also no. We’ll take all of the tailwinds we can get.

Notably, this could make TTD’s revenue cyclicality a bit more pronounced depending on how well this goes. Olympic game years line up perfectly with election cycles. So? Even years will now feature two large events (with the elections being more material) that will help TTD’s growth. Odd years will not. Just something to keep in mind.

b. Disney Partnership

Disney has long been a close connected TV (CTV) partner for TTD. That partnership got tighter this week. To unify ad impressions across all streaming assets, add deeper audience segmentation and bolster CPMs, Disney will use The Trade Desk and Google. This will give The Trade Desk access to more high value inventory. The new relationship also includes TTD’s Open Path product to help Disney connect its supply inventory directly to the buy side. This is good news for TTD. I think it’s even better news for Disney, as it shows the firm’s understanding of who it needs to partner with to make streaming as successful as possible.

5. Disney (DIS) – Proxy Fight

Speaking of Disney… The proxy battle set for a May resolution continues to heat up. George Lucas announced support for Iger and the current board while the Institutional Shareholder Service (ISS) recommended shareholders vote for Trian and Nelson Peltz’s demands (including board seats). ISS surely influences a lot more shares than Lucas. I view this as a win-win for shareholders. Disney could fend off activists and continue executing with a larger shareholder microscope over its actions. I also already view Disney as on a great track to deliver a turnaround. See updated free cash flow guidance, the asset reshuffle and its tightened film pipeline for evidence. If Trian wins, that would still likely drive short-term shareholder excitement. I’d likely take advantage of that excitement by exiting my position with a quick & sizable gain. I don’t think Peltz is qualified to be on this board and I don’t like any of his ideas for the company. But? I do like capital gains.

Peltz winning would turn this into more of a trade for me.

Do you love Twitter (sorry, not X) as much as I do? Do you only want investing-related content on that app? Do you get frustrated by all of the noisy content you scroll through to find the nuggets you actually care about? Same! Blossom is here to fix that. This is focused FinTwit meets serious investors meets portfolio tracking. It’s a thriving social media platform for us nerds and it just launched in the USA. It’s entirely free to use and something that I now post on daily. Check it out here and sign up. See ya there.

6. Progyny (PGNY) – Investor Conference

On 2024 Guidance:

Last week, Progyny told us that a treatment mix-shift anomaly it saw in the early part of Q1 fully normalized. It had been seeing a small skew away from fresh full cycles with IVF, which are higher-value treatments for the company. That small skew has since vanished. Another week passed with that same normalization trend continuing. Scheduling trends through the end of Q1 look very normal, with the statistical anomaly already a thing of the past. Considering biology & fertility needs don’t evolve on a whim and considering its overall utilization rates remain very strong, this is not surprising. Importantly, its treatment schedule backlog through the end of 2024 (not just the end of Q1) points to that normalization continuing. This was a new and important detail.

Its brand new client cohort is behaving very similarly to previous cohorts and it remains confident in utilization rate gains from 2023 being sustainable. This is also important considering the ~150,000 legacy tech layoffs from last year. This led some to think treatment demand was pulled forward for workers thinking they would soon be fired. If that did happen, it would have temporarily and artificially boosted utilization a little, which is the strongest indicator for Progyny’s revenue and profit generation. Importantly, that didn’t happen. Utilization gains for 2023 were consistent across all sectors, cohorts and geographies. This was not specific to tech.

Alabama & Red State Regulation:

I’ve covered this regulatory item in detail in previous issues. If you’d like to read about it, the information can be found here.

Since we last discussed the regulatory landscape, it has become even more favorable for Progyny. Alabama’s governor passed a law to guarantee fertility treatment protection. This is among the most socially conservative states in the union, and they just told you fertility treatment is here to stay. Republican leaders in the House of Representatives all support IVF protection and so do both presidential candidates. Protection for these services has rare bipartisan support. In Texas, where embryos were deemed to be property rather than a person to protect IVF, rulings have been appealed and already upheld.

This is a non-issue for Progyny. And even if it weren’t, all states with vulnerable fertility laws make up 3% of the nation’s total treatment volume. To make this even less concerning, that 3% could easily travel to other states for continued service. But again, non-issue.

New Products:

Progyny’s preconception, maternity and menopause products are in pilot testing. Like the Rx product early on, utilization is very light as Progyny looks to build needed marketing programs and a foundation to support future growth. That’s what it’s currently working on. It does not see these products impacting its 2024 results. The impact should begin in 2025.

Client Budgets:

Progyny sees no evidence of budget scrutiny from its client base’s demand. They continue to expand existing benefits at a healthy clip with none of them reducing coverage into 2024.

7. Apple (AAPL) – Antitrust

The Department of Justice and 16 states filed an antitrust suit against Apple this week. It claims Apple “illegally monopolizes” the smartphone space with practices that harm developers and competition. The suit is quite broad in nature with complaints ranging from consumer price gouging, artificial barriers to app store competition and unlawful Near Field Communication (NCF) tap-to-pay chip control within Apple Pay. Most of the time, these cases feature immense bark with very little bite. This specific lawsuit, however, could be a bit more material. It covers nearly every facet of Apple’s moat and is something I think shareholders should pay attention to. While resolutions could be negative for Apple, they could be very positive for other companies receiving potential app store fee or NFC access relief.

This will likely take years to be resolved and what actually happens is highly uncertain. Regardless, there will be a new regulatory risk over Apple for the foreseeable future, and to me, this looks to have more legs than recent suits with other mega-caps like Amazon.

Meta, Microsoft, X and Match Group filed a joint lawsuit against Apple pertaining to its app store policies blocking a developer’s ability to steer users to other app stores.

Apple is in talks with Google about licensing the search giant’s Gemini AI services for its iPhone Operating System (IOS).

8. SoFi (SOFI) – CEO Interview

CEO Anthony Noto was interviewed on Cramer’s Mad Money this past week. I usually don’t pay much attention to these, but the convertible notes offering was the topic. Considering all of the confusion surrounding the deals, Noto offered needed information that I will briefly cover.

Overall, the article I published on the matter was entirely accurate… that is aside from one item. My calculations led me to think the overall impact on tangible book value (TBV) per share would be neutral. Well? The deals actually bolster TBV/share by 8%-10%. That TBV accretion is realized by using an equity item to reduce the convertible note liability. Tangible book value is tangible assets - tangible liabilities. The larger the discount on the convertible notes, the larger the TBV boost. That discount had been shrinking for SoFi, so Noto wanted to pounce while he could. I already had a positive view of the news. This update made it even more positive.

Beyond this item, Noto specified that “refinancing other more expensive debt” with the new notes offering means paying off $500 million in 7% interest rate debt. This could boost annual interest expense savings from $40 million to $60 million. As stated in the previous article, interest savings will mean the dilution from the transactions will not lead to material earnings power erosion. It will reduce diluted EPS by less than one penny.

Of note, the offering was not at all done to combat any loan book health deterioration, while Noto reiterated the guidance offered in January. We’re now basically through calendar Q1, meaning the risk of missing quarterly guidance when it reports next month is very, very low.

Beyond this news, Galileo added post-purchase buy now, pay later to turn outstanding card debt into this type of credit vehicle.

9. Market Headlines

Tesla is cutting Chinese production amid weaker demand.

Amazon’s AWS will feature Nvidia’s newest Grace Blackwell 200 (GB200) superchip, extending the close collaboration between the two firms. Amazon may be working on its own chips, but it will also continue to lean heavily on Nvidia’s. Blackwell is Nvidia’s upgrade to the Hopper series. Amazon also extended its Accenture partnership to help their clients use and scale GenAI.

Uber settled a lawsuit with Australian cab drivers. Minneapolis also seems poised to walk back the restrictive regulation we discussed last week following Lyft & Uber both exiting that market.

10. Fed Statement & Powell Presser

Rate Policy Updates:

Fed Funds Rate left unchanged at 5.25%-5.5%; the decision was unanimous.

Fed continues to want more evidence of inflation retreating to 2% before cutting. Still, it expects 3 rate cuts for 2024 (so it believes that evidence will come).

Fewer Fed officials see more than 3 cuts vs. the previous meeting. Estimated 2024 rate moves from 4.4%-4.9% to 4.6%-5.1%.

Now sees 3 cuts in 2025 vs. 4 previously & getting to 3.1% in 2026.

It sees a neutral rate of 2.6% vs. 2.5% previously.

Inflation (no change to 2% target; more progress; more progress needed):

2024 Core PCE expected to be 2.6% vs. 2.4% previously & 2.8% as of February.

2025 Core PCE projections of 2.2% are unchanged. Sees Core reaching target by 2026.

Poor January inflation data was likely seasonal. Poor February data did not alter the Fed’s opinion on seeing a clear, yet “bumpy” path to 2% inflation. If this poor data persists, that would change things.

Strong disinflation progress through 2023 gives them the luxury to wait and see. YTD inflation hasn’t added or removed confidence in path to 2%.

Long term inflation expectations remain well anchored.

Powell sees real time market rent disinflation eventually translating into disinflation for the Fed’s lagging rent indicators.

Employment:

Language surrounding job gains improved.

Wage disinflation signs strong; labor supply scarcity improving & more progress needed.

Now sees 4.0% unemployment this year vs. 4.1% previously (currently 3.9%).

Output:

Fed officials materially boosted 2024 GDP projections from 1.4% to 2.1%.

Restrictive policy weighing on rate sensitive sectors & fixed business investment levels.

Balance Sheet:

“We discussed slowing the pace of declines in securities holdings. No decision yet, but the general sense is that it will be appropriate to slow the pace of balance sheet runoff fairly soon.” – Powell

Powell is focused on money market reserves as its signal to slow down passive QT.

Fed wants a “reserve cushion” & is not looking to drain reserve levels as much as they can. Doesn’t want to repeat 2019 mistake of going too far & having to pivot back to QE.

Balance sheet over time will be “mostly” treasuries. Still likely some MBS holdings.

This presser and statement were candidly more dovish than I was expecting following the January and February inflation data we got.

More Data from the Week:

Initial Jobless Claims were 210,000 vs. 212,00 expected. This compares to 212,000 last report.

Philadelphia Fed Manufacturing Index for March was 3.2 vs. -2.6 expected. This compares to 5.2 last month.

Manufacturing Purchasing Managers Index (PMI) for March was 52.5 vs. 51.8 expected. This compares to 52.2 last report.

Services PMI for March was 51.7 vs. 52 expected. This compares to 52.3 last month.

Existing home sales for February were 4.38 million vs. 3.95 million expected.

The U.S. Leading Index M/M for February was 0.1% vs. -0.1% expected and -0.4% last report.

S&P Global Composite PMI for March was 52.2 as expected. This compares to 52.5 last month.

11. Portfolio

I added to my new SentinelOne stake and boosted by Lululemon position by 9% this week following earnings.

Added some $S as well hope it gets under $20 so I can DCA but Powell positioning and how market has been acting this year is making me not too confident in that keep up the good work

Hi! Nothing on Nvidia GTC?