Table of Contents

Other Recent Earnings Reviews:

- Nvidia

- Snowflake

- MongoDB & The Trade Desk

- Sea Limited & On Holding

- CrowdStrike & Broadcom

- Axon & Mercado Libre

- Coupang & Zscaler

- Nu & Cava

- Hims

Other recent content:

- My updated portfolio & multi-year performance vs. the S&P 500.

- Axon Deep Dive

- 20+ more earnings reviews from this season (search by ticker).

We will be adding audio recordings for articles next week. Thank you for the feedback.

1. Oracle (ORCL) – Earnings Review

a. Oracle 101

Oracle provides a slew of software and hardware tools for on-premise and cloud environments. It has 3 main segments which are closely integrated.

Oracle Cloud Infrastructure (OCI) is its fully managed business for infrastructure services (virtual machines, storage, managed high-performance compute data centers etc.). This segment also includes platform services to build apps in its safe, controlled environment (serverless and container-based).

Strategic Software As A Service (SaaS) includes Oracle NetSuite. This is a set of applications for enterprise resource planning (ERP), customer relationship management (CRM), human capital management (HCM), e-commerce and more. It’s hard at work on launching more industry-specific software apps across areas like healthcare. It also has a more customizable, feature-rich product that is similar to NetSuite called Oracle Fusion. This one is geared towards larger customers.

The last segment is its broad range of database products including both relational and document-oriented offerings across structured, semi-structured and unstructured data. Creating valuable apps from GenAI infrastructure requires great models and rich, organized information access to properly season those models. That’s where its database capabilities come into play.

Oracle closely integrates with the 3 big hyperscalers, allowing its databases to run anywhere. This also means that customers can migrate their on-premise databases to the cloud via OCI or through any of these hyperscalers, diminishing user friction. Oracle believes that this data cloud interoperability provides innate data transfer cost advantages. Cost is estimated to be “several times cheaper” for model training than any competitive product, according to leadership.

Oracle has re-emerged as a digital infrastructure titan. While the company did take longer to roll out its high-performance compute product suite, it has since achieved fantastic traction.

b. Key Points

- Solid quarter across its three growth pillars.

- Reiterated no capital raises beyond the $50B for this year.

- Increasingly utilizing creative contract structures to untether data center growth from CapEx growth.

- GPU-based capacity delivered this quarter came with a 32% gross margin vs. its 30% long-term guidance.

c. Demand

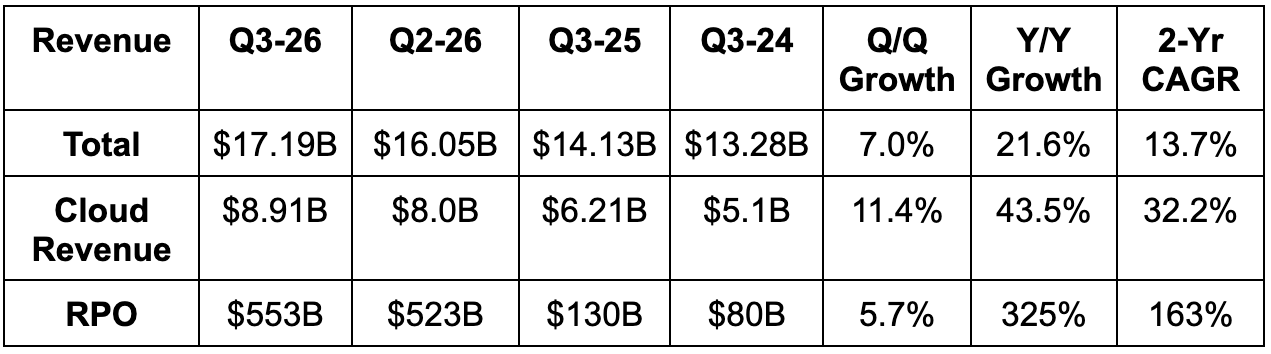

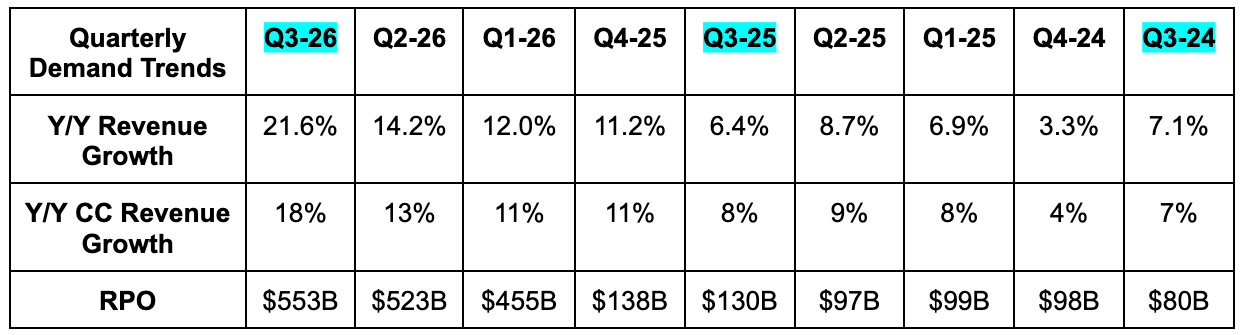

- Beat revenue estimate by 1.7%. 18% constant currency (CC) revenue growth beat 17% CC growth guidance.

- 43.5% cloud revenue growth beat 42% growth guidance.

- Beat Remaining Performance Obligation (RPO) estimate by 4.7%.

- The large Q/Q and Y/Y increase was again driven by large AI contracts with leaders like OpenAI.

- This was the first quarter in 15+ years where revenue growth and EPS growth were both north of 20% Y/Y. Currency tailwinds did help a bit, but still very notable.

d. Profits & Margins

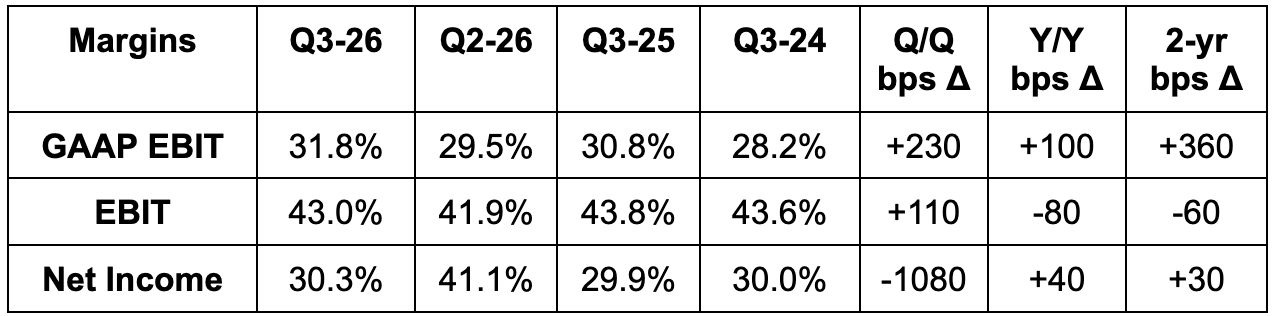

- Beat EBIT estimate by 2.8%.

- Beat $1.23 GAAP EPS estimate by $0.04.

- Beat $1.69 EPS estimate by $0.10.

e. Balance Sheet

- $39B in cash & equivalents.

- ~$134B+ in total debt.

- 28% Y/Y dividend growth.

- 1.3% Y/Y dilution.

Last month, Oracle announced they would raise $50 billion between debt and equity financing this year. They already issued $30 billion in bonds with great demand, but have yet to offer the planned $20 billion in equity (4.4% of the current market cap).

f. Guidance & Valuation

- Q4 revenue growth guidance roughly met estimates.

- They also expect 46% constant currency (CC) Y/Y cloud growth and 48% Y/Y cloud growth in dollar terms.

- Q4 $1.98 EPS guidance beat estimates by $0.03.

- For the full year, they continue to expect $67B in revenue and $50B in CapEx.

- For next year, they now see $90B in annual revenue, which is 3.8% ahead of expectations.

Oracle trades for 20x forward EPS (no cash flow right now). EPS is expected to grow by 23% this year and by 7% next year.

g. Call

Oracle’s Thoughts on the Death of SaaS:

Leadership spent a lot of time talking through negative Software as a Service (SaaS) sentiment, and why they think it's sharply overblown. Like everyone else, they're confident that AI technology will profoundly reshape the way we all conduct work and deliver products. They just also think they're building the tools and the overall ecosystem to secure a large piece of that future landscape. Here we’ll discuss why they’re so bullish on the future.

They're using the technology to greatly accelerate their pace of application creation, while also embedding roughly 1,000 agents throughout existing products. They're offering customers tools to customize their own agents, without any upcharges. And they're doing all of this while offering customers a way to unify their database and application needs under one roof, driving interoperability, lower costs, and simplicity. Many of these customers are already parking their data in an Oracle database public cloud. They don't want more vendors, they want fewer. If Oracle is able to deliver impactful product innovation that keeps pace with all the change and disruption taking place, they should be able to continue providing unique value to their customers. And thanks to all of this first and third party data that they have at their disposal (not just Wikipedia, Reddit and other commoditized public data sources), they have a good chance of holding their ground.

Leadership spoke about conversations with customers not coming remotely close to mirroring the sentiment seen on Wall Street at the moment. There are no customers even contemplating ripping out any existing Oracle applications in favor of vibe-coded alternatives. The mountains of proprietary data, decades of compliance experience, highly complementary data and infrastructure services, and brisk AI innovation (that they don't have to do themselves) all continue to help Oracle drive high retention. AI is pushing customers to ask Oracle how they can embed more of this technology into the products they know and love. It is not tempting them to rip and replace with untested, unsupported, and unproven alternatives, conversationally created in 48 hours. Shocker (I say very sarcastically).

AI Halo Effect?

The dynamic discussed above is creating a platform-wide halo effect, where AI fosters incremental demand across its other product categories in a few ways. The need to embrace this new technology is pushing customers to migrate and modernize their existing data and application infrastructure, which helps Oracle’s products. Already housing so much of a customer's data is making Oracle an easy and convenient choice for running other AI-related workloads and using its infrastructure and data tools. All of the AI model training and inference taking place in its ecosystem is allowing rapid implementation of AI-driven upgrades to its applications. Examples of this include Fusion’s AI Agent Studio, which is being offered to customers as a free upgrade, permitting them to customize their own agents within the familiar Fusion interface. And its reliable infrastructure-related services are helping it win trust and business across its data and application pillars as well.

As we already discussed, customers want fewer vendors, and Oracle offers great products across all three of these highly complementary buckets. Finally, because Oracle thinks its infrastructure build-outs are cheaper than competitors, it sees more budget being unlocked for application purchases, including its own. Simply put, AI helps everywhere. And because Oracle does so many things, it’s confident in readily using all of this AI advancement to benefit its customers and its own business in numerous ways.

As a key aside, it's this overarching platform and the valuable products forming it that provide Oracle with confidence in winning a respectable piece of the AI agent opportunity that so many are vying for.

- The company took several shots at Salesforce throughout the prepared remarks, pounding their chests about having applications that drive revenue, rather than offering forecasts and click optimization.

- Coding agents are helping Oracle shrink software developer teams while accelerating product delivery.

Multi-Cloud Database:

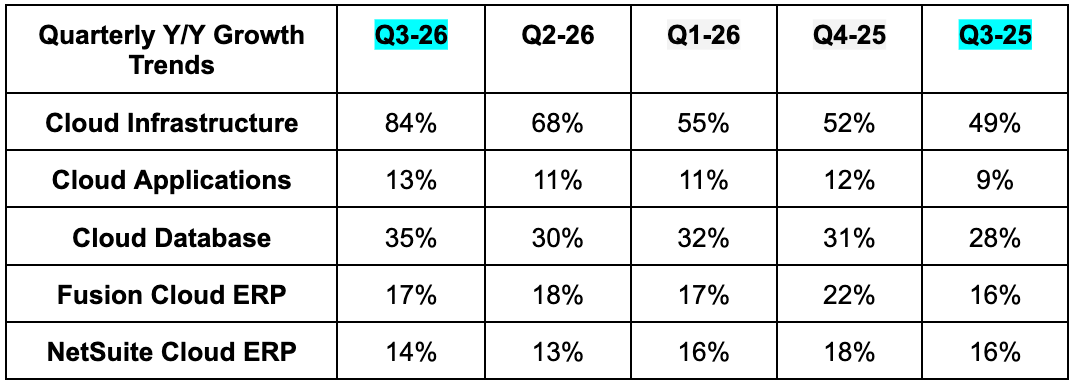

The decision to allow Oracle Database Services to run in every public cloud, rather than just OCI, has proven to be a great one. It has unlocked a boatload of demand that drove 531% Y/Y growth for the quarter. A lot of this is driven simply by years of building interest in this product being offered through key partners like Azure, AWS, and GCP. They're now actually integrating across regions around the globe, and as that happens, demand predictably follows. Global region coverage now extends for all partner clouds, with 33 Azure regions live, 14 Google Cloud regions live, and 8 AWS regions live (with plans to grow that to 22 by the end of next quarter).

AI Infrastructure:

AI infrastructure revenue grew 243% Y/Y, driven by both GPU and CPU-related demand. Supply remains scarce for both product types.

Leadership spent a lot of time talking about how they're getting more efficient in thinking about and spending capex as they scale their data center footprint. They reviewed how Oracle's modular, Lego-like design allows them to standardize construction across any size of data center, in a way they view as more efficient than any other competitor. This efficiency is also why their GPU-based data center capacity laid this quarter remained two points above their long-term 30% GPM guidance. And CPU-based capacity continues to have margins in excess of that level.

They've reduced time from rack delivery to revenue generation by 60% over the last few quarters, and are also enjoying growing fixed cost leverage associated with growing into their quadrupled rack manufacturing capacity Y/Y. Additionally, the company is embracing a "bring your own hardware" form of data center build outs that shrinks the negative cash flow associated with expansion, while shifting to some upfront customer payments to accomplish the same thing. A key theme throughout the prepared remarks was the relationship between capex and negative cash flow untethering, as they get creative in how they structure these gigantic relationships. Contracts using this structure represented $29B in new business signed this quarter as a strong sign that customers are entirely fine with the changes.

Next, Oracle leadership discussed 90% of their data center contracts being executed on, or ahead of schedule this quarter. In a world frantically trying to find supply and dealing with bottlenecks everywhere you look, that is strong execution. Alongside the cost advantages that leadership discusses every quarter, this continues to help Oracle gain the confidence of its partners in choosing OCI.

TikTok:

As broadly reported, Oracle now owns a 15% stake in the U.S. TikTok business. This won't impact revenue going forward, but they will record non-operating income based on that business's results and their proportional interest starting next quarter.

More Notes:

- Talked about several notable application wins against Workday and SAP, as well as a few wins that displaced SAP during the quarter. All main Fusion apps grew by a mid-teens percent rate. Netsuite grew by 11%.

- Simplified go-to-market, discussed last quarter, is leading to more multi-product wins across its main product categories.

- They were asked about their concentration of data centers in Texas and Wyoming, and if that's concerning to them from a latency point of view, as these AI factories are not close to where that compute is being consumed. They're not. Most of these use cases are asking strategic, complex questions or jumpstarting highly intricate tasks that take a while. As leadership put it, customers don't care if that output happens 0.4 seconds sooner than it otherwise would. They're looking to build multi-year strategic roadmaps and design innovative products.

- Oracle plans to lay off up to 30,000 employees as part of a new restructuring to get more efficient in their bid to fund growth, with their already highly levered balance sheet. That is 19% of their total workforce, and is yet another blow to the employment market. We all need to stay laser focused on unemployment metrics to gauge whether or not names, and especially economically sensitive names, are vulnerable to negative estimate revisions.