Housekeeping:

- My detailed Zscaler Earnings Review can be found here.

- Salesforce and MongoDB earnings reviews will come tomorrow.

- Snowflake 101 (intro to the business) can be found here.

- 31 other earnings reviews to read from this season.

Table of Contents

a. Key Points

- Strong beats across the board.

- AI products are materially helping growth.

- M&A expands market positioning.

- Pace of innovation keeps accelerating.

b. Demand

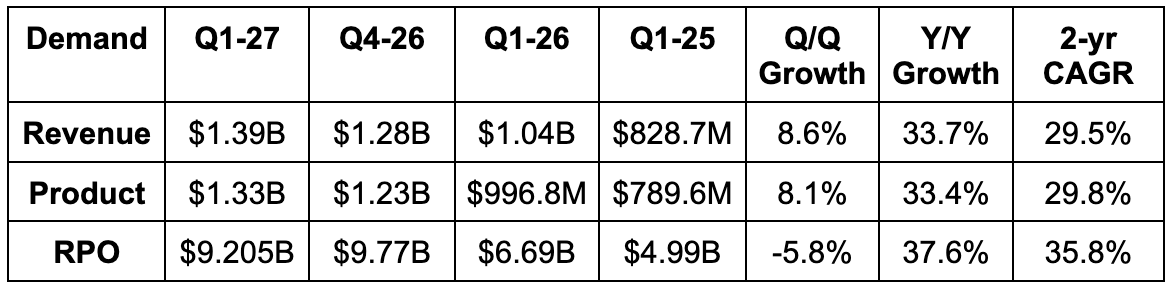

- Beat revenue estimates by 4.9%.

- Its 29.5% 2-year revenue compounded annual growth rate (CAGR) compares to 28.5% last quarter and 28.4% 2 quarters ago.

- Beat product revenue estimate by 4.7% & beat guidance by 5.2%.

- Beat 125% net revenue retention (NRR) rate by 1 point.

- Remaining performance obligation (RPO) missed estimates by 2.4%. This is because SNOW is seeing growing interest in customers renewing during Q4, which means more backlog growth will come during that quarter than during previous years.

- Despite this, RPO growth accelerated from 34% Y/Y last year to 38% Y/Y this year.

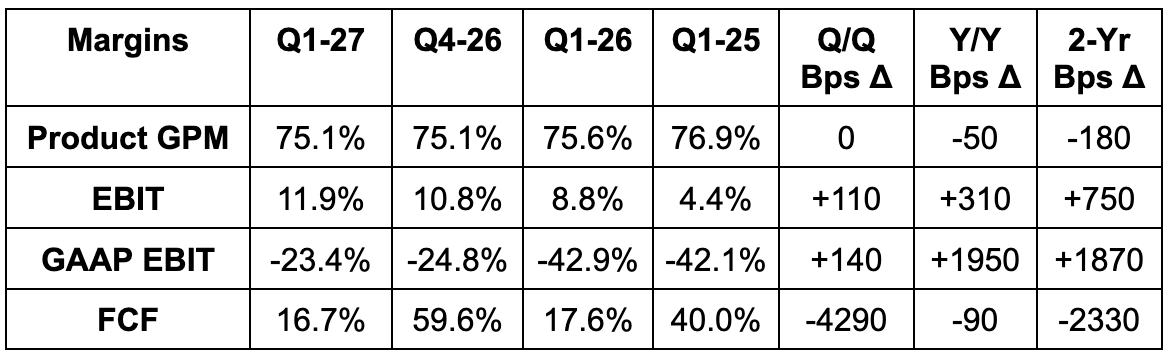

c. Profits & Margins

- Beat EBIT estimates by 38% & beat 9% EBIT margin guidance by 3 points.

- This was related to revenue outperformance, slower hiring and some modest R&D cost leverage.

- SNOW added 190 people this quarter (173 from acquiring Observe).

- Beat $0.32 EPS estimates by $0.07.

- Beat FCF estimates by 8.2%.