Other reviews from this season to read:

- Nu

- Mercado Libre & Datadog

- AMD & Uber

- Axon

- SoFi

- Amazon

- On Holding

- AppLovin & Cloudflare

- Duolingo

- Meta

- Starbucks

- Lemonade

- Robinhood

- Hims & The Trade Desk

- Alphabet

- Sea Limited

- Shopify & Coupang

- ServiceNow

- Apple

- Spotify

- Palantir

- Microsoft

- Taiwan Semi

- Netflix

- Tesla

a. Key Points

- AI security bookings crossed $100M.

- Some go-to-market disruption from two sales leader departures.

- Rough early look at fiscal year 2027 (much more later).

b. Demand

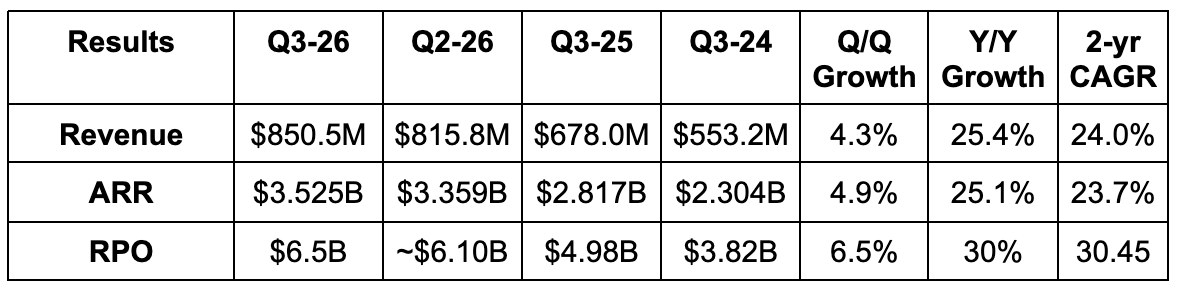

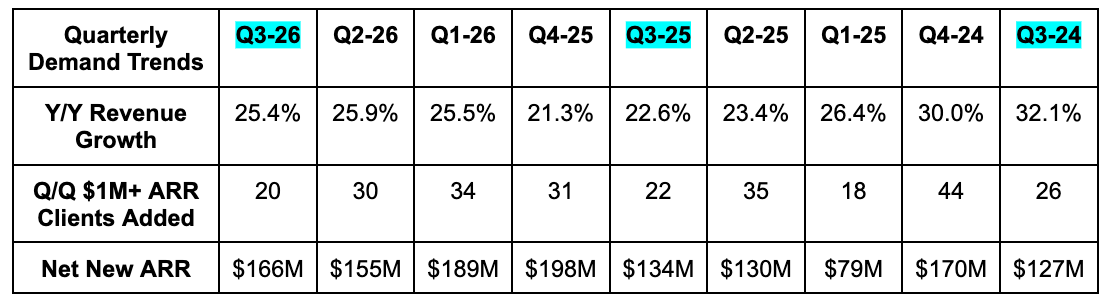

- Beat revenue estimate by 1.8% & beat guidance by 1.9%.

- Revenue growth was 31% Y/Y in the Americas, 16% in Europe + The Middle East, the 16% Y/Y in Asia Pacific + Japan (APJ).

- Beat $148M net new ARR estimate by $18M.

- Organic ARR growth ex-Red Canary was 21% Y/Y.

- Net new ARR got a boost from an 8-figure federal government up-sell

- 24% Y/Y net new ARR growth was 14% ex-Red Canary.

- Beat remaining performance obligation (RPO) estimate by 1.9%.

- Set a new overall record for $1M annual contract value (ACV) deals signed in a quarter.

- $1M+ APJ deals rose by 150% Y/Y.

Like so many other software companies, Zscaler is actively shifting from seat-based monetization to various forms of consumption-based product delivery. This quarter, 30% of its new ACV came from non-seat-based sources, and this bucket grew by 100% Y/Y. We’ve seen other companies disclose higher proportions than 30%, but still good progress.

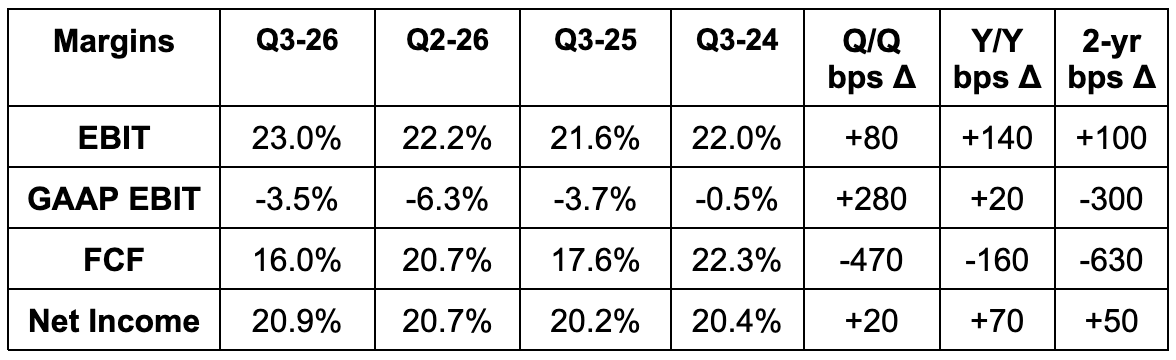

c. Profits & Margins

- Beat EBIT estimate by 4.1% & beat guidance by 4.1%

- Sales and marketing leverage helped drive Y/Y margin expansion.

- Beat FCF estimate by 4%. Higher CapEx weighed on FCF.

- Beat $1.01 EPS estimate by $0.07.

d. Balance Sheet

- $3.6B cash & equivalents.

- $1.7B senior notes.

- 3.8% Y/Y dilution.

e. Guidance & Valuation

Q4 2026:

- Reiterated Q4 revenue guidance which slightly missed estimates.

- Raised Q4 EBIT guidance by 1.4% which beat by 1.2%.

- Raised Q4 ARR guidance from $3.73B to $3.7445B. The $14.5M ARR raise was smaller than the $18M Q3 ARR beat. That has been happening for this company for the last few quarters. $7M of this $14.5M raise was from higher Red Canary expectations.

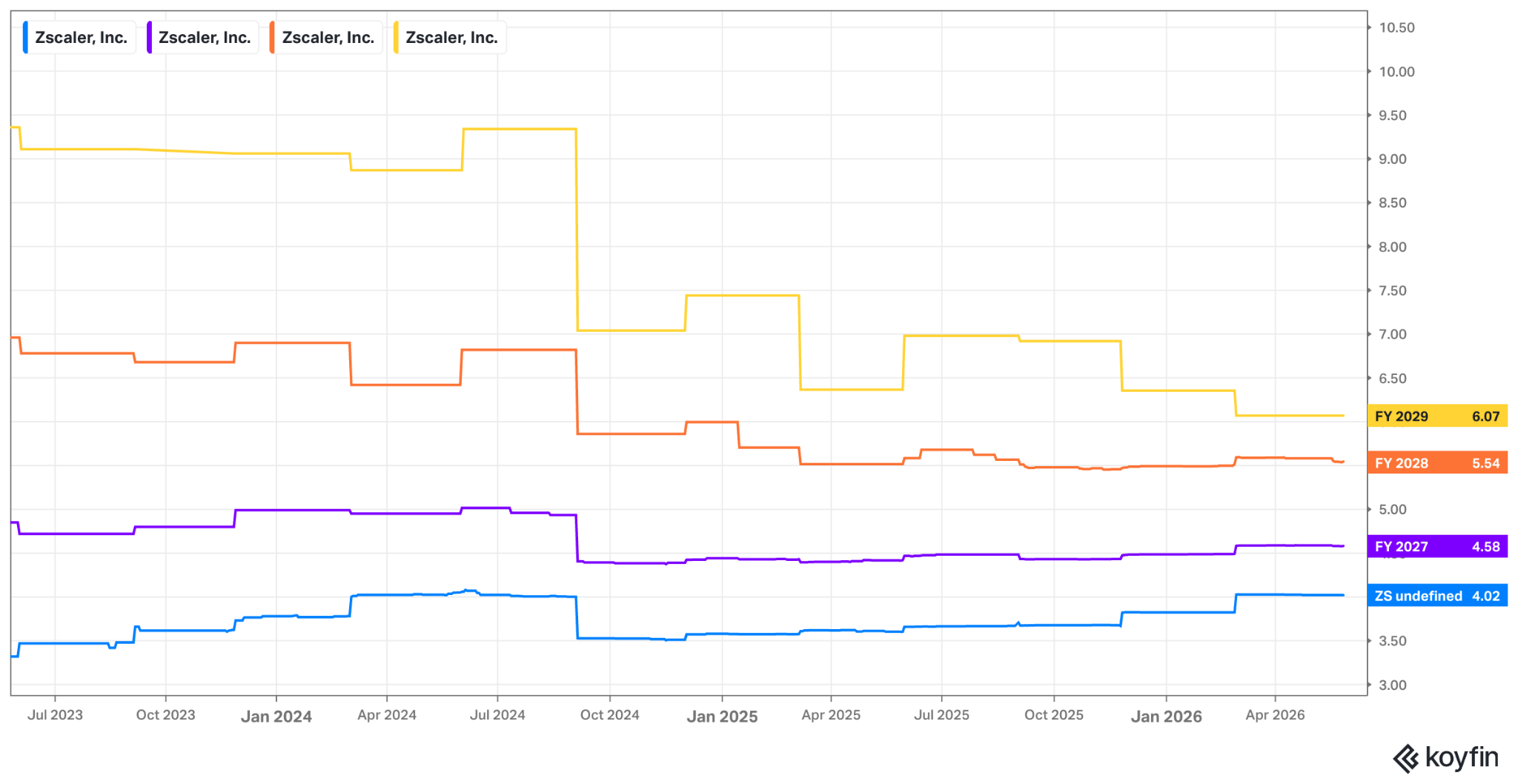

2027:

For 2027, Zscaler expects 16.5% Y/Y revenue and ARR growth. This represents $618M in net new ARR compared to $734M for 2026. Red Canary growth will be slower than the rest of the business, which is slowing things down, but still not good. Specifically, both ARR & revenue growth targets are 3 points slower than consensus expectations. Much more on this later. Additionally, they think CapEx will rise 2 points as a percentage of revenue, which will pressure FCF margin. Q4 2026 FCF margin will be hurt by this memory inflation and some component order pull-forwards to avoid some of that inflation. 2027 will be negatively impacted by memory inflation.

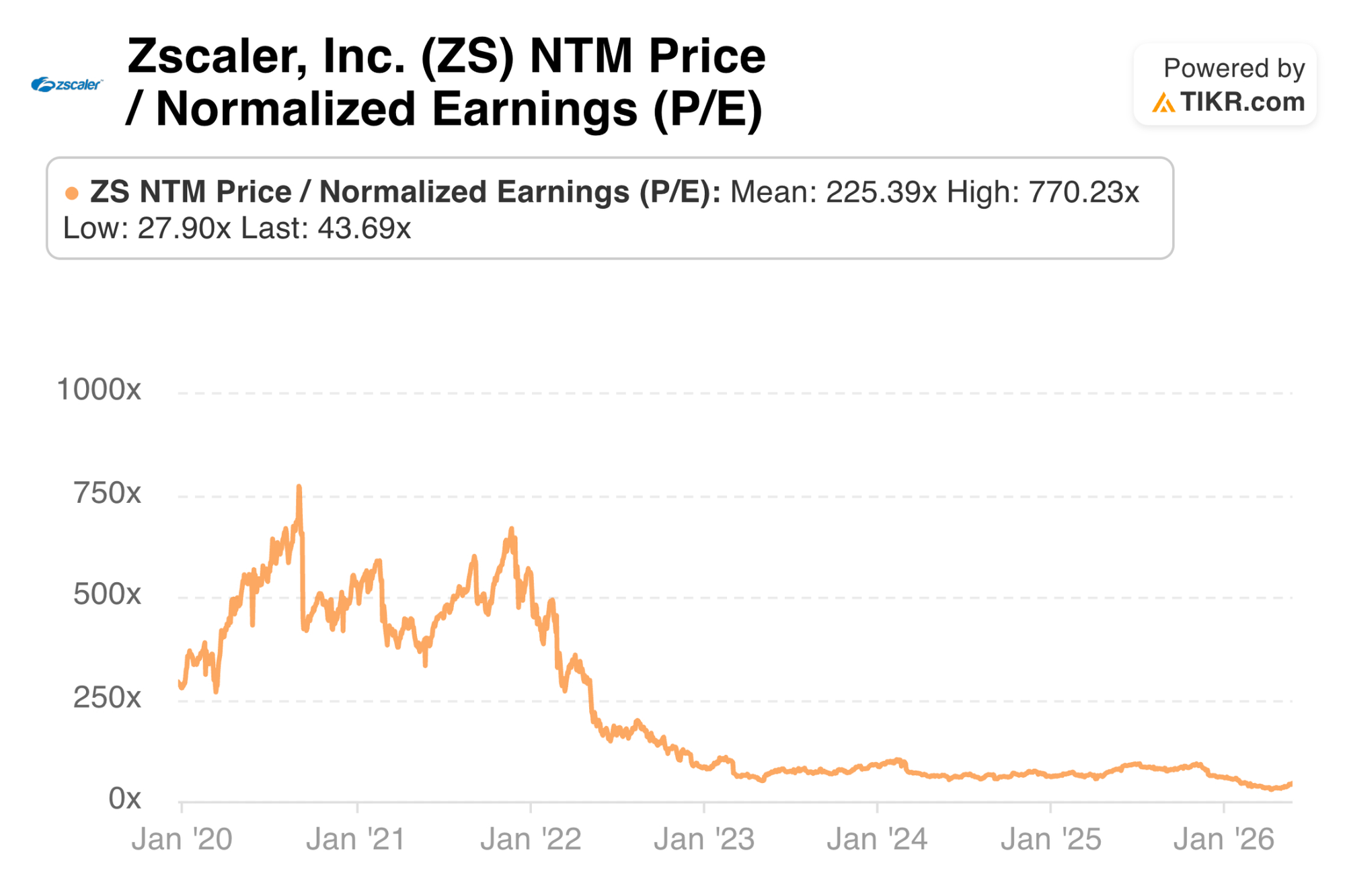

ZS (around $150) trades for about 35x forward EPS and 28x forward FCF following this report. EPS is expected to grow by 22% this year and by 14% next year. FCF is expected to grow by 24% this year and by 25% next year. I expect modest negative EPS estimates for next year given the poor revenue growth commentary. I expect larger negative FCF revisions given the higher CapEx note.