Other reviews to read from this season:

- Palantir

- SoFi

- Amazon

- Meta

- Lemonade

- Robinhood

- Alphabet

- ServiceNow

- Apple

- Duolingo

- Spotify

- Microsoft

- Taiwan Semi

- Netflix

- Tesla

& my current portfolio & performance vs. the S&P 500.

1. Shopify (SHOP) – Earnings Review

Shopify offers a full suite of services to take the headache out of managing a business for their merchants. They call it the commerce operating system, with tools that range across web building, payments, cross-border compliance, advertising, and so much more.

My Shopify deep dive can be found here. You may want to read a few of the more recent earnings reviews for a more current overview of the product suite, but that offers a great overview of the overarching business and approach.

a. Key Points

- Strong North American acceleration.

- AI is providing real merchant and financial value today.

- The free trial subscription solutions headwind is now behind the company.

- Growth from AI shopping surfaces is soaring.

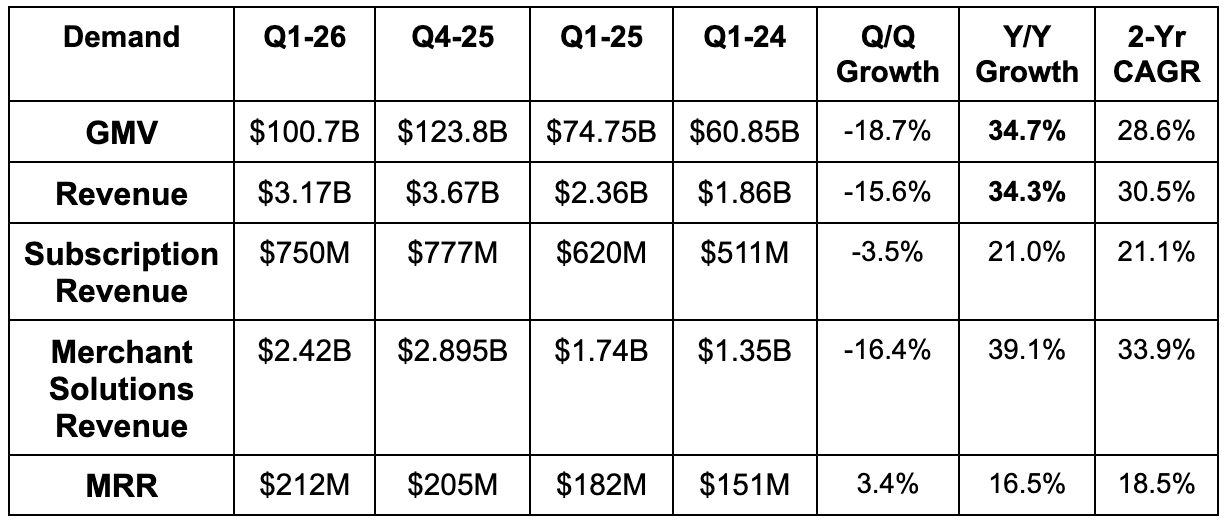

b. Demand

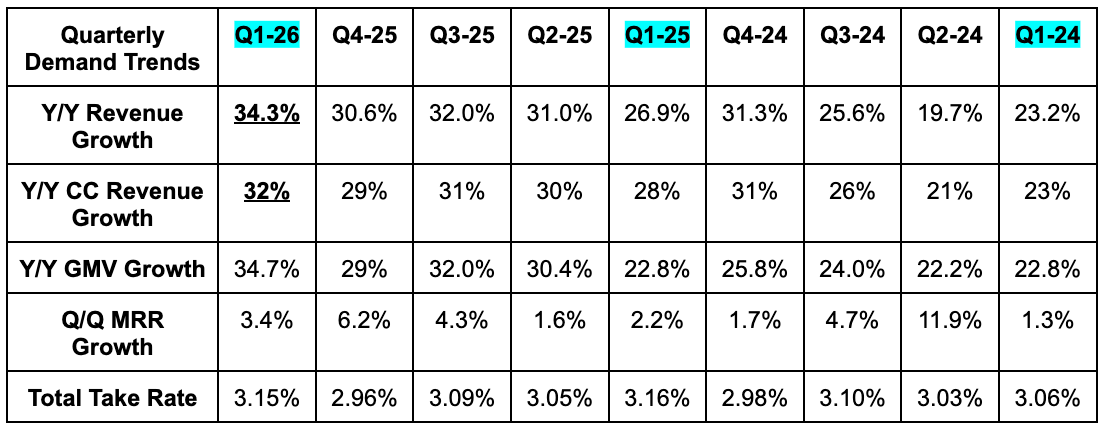

- Beat revenue estimates by 2.5% & beat low-30% revenue growth guidance.

- 32% constant currency (CC) revenue growth beat 31% growth estimates.

- Revenue growth was 33% in North America compared to 28% growth last quarter, as their largest market accelerates Q/Q.

- Beat Merchant Solutions revenue estimates by 2.9%.

- Beat subscription solutions revenue estimates by 0.9%.

- Subscription solutions growth was held back by free trial lengthening last year. Shopify has now lapped this headwind, and growth will normalize next quarter.

- Beat gross merchandise value (GMV) estimates by 2%.

- European GMV was highlighted as a standout with 35% CC growth. This follows mid-30% growth throughout 2025, as Shopify builds on the momentum.

- Offline GMV rose by 33% Y/Y vs. 29% growth last quarter and 23% Y/Y growth last year. Really nice acceleration.

- Business to Business (B2B) GMV rose by 80% Y/Y vs. 84% growth last quarter and 100%+ Y/Y growth last year.

- Beat gross payments volume (GPV) estimate by 1.4%.

- Shop Pay (their checkout accelerator) generated 59% Y/Y volume growth as it rapidly takes share from PayPal and others.

- Beat $211M monthly recurring revenue (MRR) estimates by $1M.

c. Profits & Margins

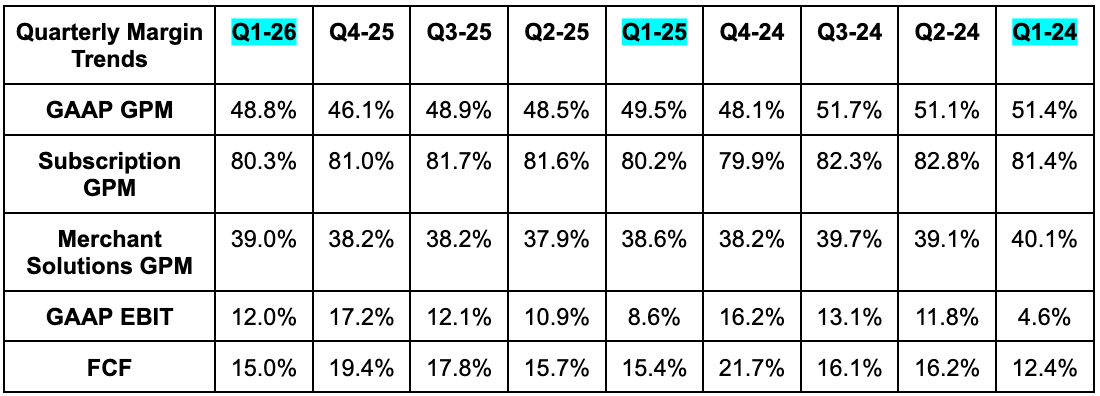

- Beat 48.4% GPM estimates by 40 basis points (bps; 1 basis point = 0.01%).

- Beat 38.2% merchant solutions GPM estimate by 80 bps.

- Missed 80.7% subscription solutions GPM estimate by 40 bps.

- GPM outperformance was thanks to revenue outperformance and, to a lesser extent, a temporary tailwind from a change in developer revenue share structure.

- The economies of scale are driving GPM leverage, while hefty investments in AI product improvements are offsetting some of this expansion by design.

- Beat GAAP EBIT estimates by 16% & beat operating expense guidance.

- OpEx rose by 32% Y/Y, which was higher than expected due to variable costs associated with revenue outperformance.

- OpEx was 37% of revenue vs. 41% Y/Y.

- Loan loss rate fell Y/Y.

- Headcount is not growing much and that’s expected to be a theme going forward.

- They’re enjoying material marketing performance improvements (Especially in Europe) that are prompting more aggressive spending.

- Beat FCF estimates by 8%. Beat $0.33 EPS estimates by $0.03 or 9%.

d. Balance Sheet

- $5.7B cash & equivalents.

- $4.9B in investments.

- No debt.

- 0.6% Y/Y dilution.

e. Guidance & Valuation

- Guided to “high-20%” revenue growth compared to 26.5% growth estimate.

- Growth rates are supposed to be similar compared to Q1, but the foreign exchange tailwind will shrink from 200 bps to 50 bps, which is why the company did not again guide to a low-30% growth rate.

- Guided to “mid-20%” gross profit growth compared to 24% growth estimate.

- Ongoing GPM contraction is as expected and via structural mix shift to its lower-margin merchant solutions category.

- Operating expenses as a percentage of revenue are expected to be 35.5% vs. 38% Y/Y.

- Guided to “mid-teens” FCF margin compared to a 16% margin estimate.

- FCF margin is going to get a 50 basis point tailwind from a reclassification of its capital loans based on changing Canadian regulation.

f. Call & Release

AI Positioning – Overview:

As the results above justify, Shopify's team remains exceedingly confident in the company's long-term AI positioning. The sharp acceleration we've seen over the last several quarters is a byproduct of all this work, making Shopify an even better partner for merchants as they future-proof their businesses against disruptive risks. This is just more of the same for the company. Their fixation on taking care of merchants, creating win-win scenarios, and alleviating operational headaches that a merchant might face all continue to resonate – across non-AI use cases and emerging AI-powered possibilities.

As leadership put it, fast change creates confusion, anxiety, and doubt. Despite this, Shopify has repeatedly embraced change, "absorbed its complexity," and distilled it into something that’s easy for merchants to use. I think the last few quarters prove that this time will be absolutely no different.

Why So Well Positioned in AI – Data:

Like many other scale platforms, leadership is confident that Shopify’s two decades of commerce data and large market share within global e-commerce are differentiating attributes that cannot be vibe coded. They've spent decades mastering the weird, granular, and countless edge cases that a wildly diverse array of merchant customers have experienced. Shopify has learned from this all, helped their merchants navigate it, and built capabilities from it all that can only be fortified through experience and challenges.

Their AI sidekick (intuitively named Sidekick) is a great example of the company leveraging this massive base of data in ways that help merchants succeed. As Shopify seasons this product with more data and upgrades it with more partner models, usage is exploding higher. Weekly active shops using this spiked 4X higher Y/Y, while apps created using it soared 200% sequentially to 12,000. As Harley put it during the call, this is becoming a merchant's "co-founder," with its complementary "Pulse" "product" getting increasingly intelligent and serving up timely recommendations to optimize decision-making and merchant outcomes.

It's important to note that Pulse is not only differentiated because of Shopify's massive amount of proprietary signal, but also all of the other products Shopify offers on top of it. Pulse and Sidekick are able to offer so many actionable recommendations because Shopify has so many products to utilize within their autonomous workflows. The platform-wide positioning matters a lot. Without it, these AI products would be much more elementary, and the ability to leverage them to spearhead tangible, real-world use cases that increase financial success wouldn't exist.

Why So Well Positioned in AI – Demand Creation:

Shopify's second main AI differentiator is the numerous levers it pulls on its merchants' behalf to help locate more demand and sell more products. That's the beauty of aligning interests with your customers. Creating better outcomes for them not only insulates you from competitive and technological risks, but it gets you paid as well. These demand creation sources put merchants at a disadvantage when they're not using Shopify, which is exactly what leadership wants.

Starting with new AI channels, Shopify has always been determined to help merchants "sell anywhere.” If there's a new channel that could even potentially emerge as a material source of merchant demand, Shopify wants to be there, and be there first. They want the risk to be that a given channel may not pan out, rather than missing out on a channel or being late to one that does. I think it's the right approach, as it insulates them from a fluid commerce landscape. AI has been more of the same in terms of Shopify's desire to blaze the innovation trail. They are the only platform with direct integrations and product discovery across ChatGPT, Microsoft Copilot, and Google Gemini, from a single, accurate, and current Shopify Catalog. This product library has become a required tool for commerce agents to understand product availability, descriptions, and how to match relevant listings with a given chat interaction. And interestingly, non-Shopify merchants are also seeing how this product drives commerce growth across AI services, which is turning it into another top-of-funnel tool in Shopify's toolkit.

Encouragingly, early signs for AI's popularity as a commerce interface for customers are convincingly positive. AI traffic coming from its various partners rose 8X Y/Y and orders from AI-powered searches rose 13x Y/Y. New buyer conversion rates on AI channels are also 2X higher than other channels, showcasing how modern technology and personalized experiences can power better results. It's important to note that there are various formats for how customers actually check out and pay for products that are sourced through Shopify's catalog as a chatbot output. In OpenAI's case, checkout happens through Shopify within ChatGPT. Gemini uses Google's established checkout products to handle more of the process itself. Regardless, management consistently talks about how unit economics are roughly similar across various AI partners, as well as AI services vs. non-AI services. Margin pressure right now is coming from aggressive AI spending. It is not coming from explosive growth in agentic commerce.

Elsewhere in demand creation land, Shopify campaigns are performing very well. It's helping customers tap into highly sophisticated performance marketing algorithms without massive upfront spend or risking budget exhaustion without conversions. Campaigns live on this platform rose 3X Y/Y, which is also feeding Shopify more data to sharpen targeting, improve outcomes, and spin the flywheel faster. Impressively, this product is already 25% of total GMV for merchants, and with new partnerships across ChatGPT, Pinterest, and Microsoft, it's still only the beginning.

Next is the company’s consumer-facing Shop App. As this source of demand grows, consumers enjoy a unique selling surface that no other company can match. Wix doesn't have a scaled consumer-facing platform like Shop App, growing GMV at a 70% Y/Y clip and users at a 40% Y/Y clip. Nobody else in their field does. Just Shopify. And as part of this, their user verification tool, called "Sign In with Shop," is proving to be a valuable asset for autonomous agents, understanding permissions, identities, and desired scope of work. This is growing at a 3X year-over-year clip and should continue to see agentic commerce provide tailwinds to enjoy.

Why So Well Positioned in AI – Powerful Yes Simple:

The last AI differentiator is how Shopify offers all of this selling, support, and success in a simplistic manner. As we alluded to earlier, they do not add complexity when they add new ways for merchants to make money or control operating costs. They "absorb this complexity" at every turn – from allowing customers to add new markets across the globe to unlocking payments options (both with a few clicks). So business people merely see a pretty front end that they can easily navigate. For customers who want that complexity and even more customization, Shopify offers a headless option that lets them do pretty much whatever they want to. For customers needing support and without large teams of web developers, their Lego-like web design, seamless onboarding, and straightforward addition of new products are all deeply appealing.

They're extending these capabilities with their co-developed Universal Commerce Protocol (UCP) with Alphabet. For review. This offers a standardized framework for agents accessing what they need across product catalogs, checkout pages, logins, and any other app it might need to complete a multi-stage task. It creates a uniform architecture for agentic communication and collaboration that makes embracing and unleashing this new base of workers doable. Stripe just recently joined the coalition alongside Amazon, Meta, Microsoft, and Salesforce.

Winning The Big Boys of Today & Tomorrow:

Shopify's enterprise-facing go-to-market is enjoying fantastic momentum. This quarter, they signed LVMH, Mulberry, and more popular brands like Rag & Bone, Lands' End, Orvis, and Rue Gilt Group. Merchants generating $2M+ in GMV are expanding rapidly, while merchants generating $100M+ in annual GMV are accelerating.

More Notes:

- AI is now writing 50% of Shopify code while boosting productivity and project output per employee.

- Leadership acknowledged recent applications for money transfer licenses that could allow it to add more financial services to their product umbrella. They declined to offer any detail beyond that.

g. My Take on the Quarter & Stock

Subscribe below to read my take on Shopify and the quarter. Also read a full Coupang review and detailed earnings reviews on the following companies:

- Palantir

- SoFi

- Amazon

- Duolingo

- Meta

- Lemonade

- Robinhood

- Alphabet

- ServiceNow

- Apple

- Spotify

- Microsoft

- Taiwan Semi

- Netflix

- Tesla

If you'd like to read that and full reviews on 40+ companies this season (and so much more), upgrade below.