Table of Contents

Welcome back to earnings season! Over the next several weeks, I will be sending 40 detailed reviews on popular, high-quality companies. Upcoming reviews include Robinhood, Meta, SoFi, AMD, Palantir and so many others coming thereafter.

Reviews already sent:

If you'd like all of those reports, consistently thorough weekly news, my real-time performance/portfolio updates and access to a large Discord channel of seasoned investors, subscribe below.

This is where investors (including Fortune 500 executives) come for signal over noise and to invest with good reason.

a. Key Points

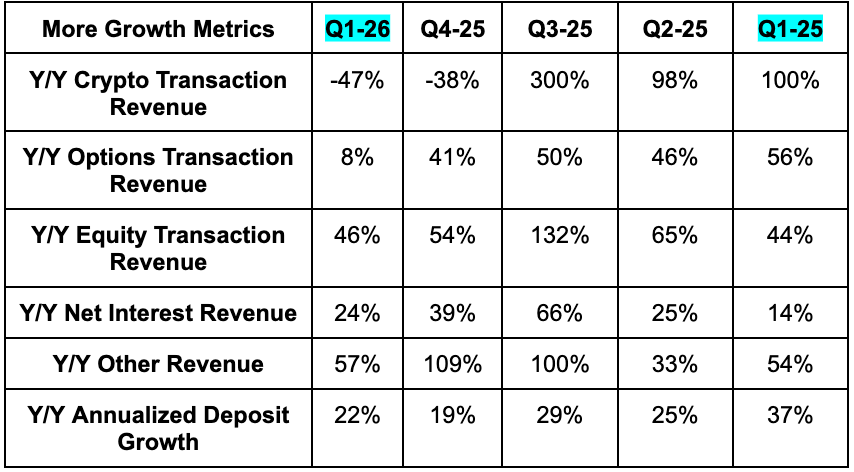

- Prediction markets continue to rapidly grow.

- Tough quarter for crypto revenue growth.

- Robinhood Banking is scaling very nicely.

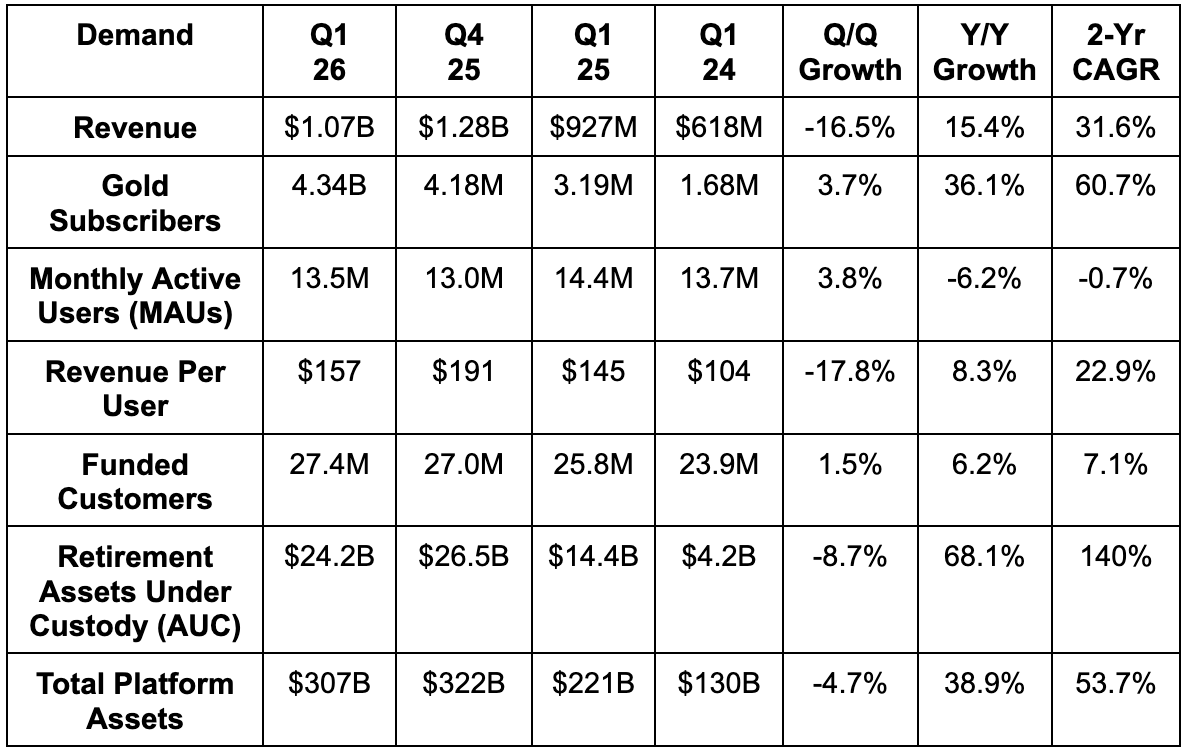

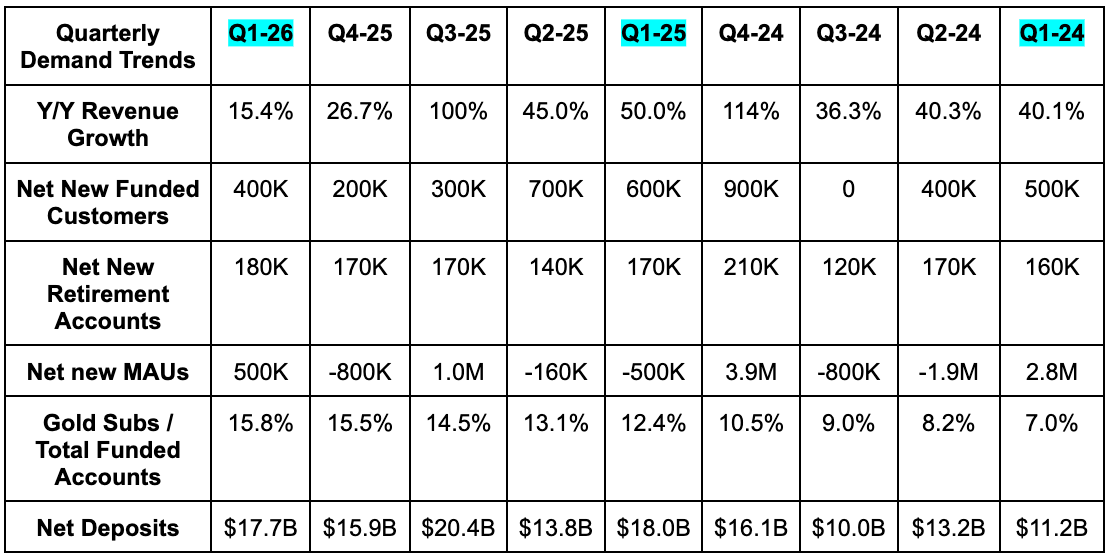

b. Demand Snapshot

- Missed revenue estimates by 6.5%.

- Transaction-based revenue missed estimates by 5.7%.

- Options revenue missed estimates by 8%.

- Equity revenue missed estimates by 2%.

- Crypto revenue missed estimates by 9%.

- Net interest revenue missed estimates by 8%.

- Missed funded account estimates by 100K.

- Missed monthly active user (MAU) estimates by 1.5%.

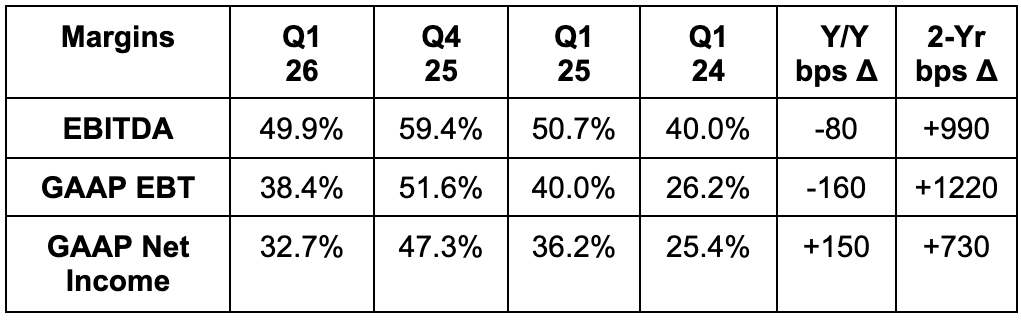

c. Profit Snapshot

- Missed EBITDA estimates by 8.3%.

- Missed $0.39 EPS estimates by a penny. EPS rose by 3% Y/Y.

- OpEx rose by 18% Y/Y to support product and marketing investments.

- Interest-earning asset growth and balance sheet optimization helped offset the interest rate headwind to drive Y/Y net interest margin expansion.