Welcome back to earnings season! Over the next several weeks, I will be sending 40 detailed reviews on popular, high-quality companies. Upcoming reviews include Tesla, Robinhood, Meta, SoFi, AMD, Palantir and so many others coming thereafter.

Reviews already sent:

Other recent content includes:

If you'd like all of those reports, consistently thorough weekly news, my real-time performance/portfolio updates and access to a large Discord channel of seasoned investors, subscribe below.

This is where investors (including Fortune 500 executives) come for signal over noise and to invest with good reason.

Table of Contents

a. ServiceNow 101

Throughout this piece, I will reference various products in the ServiceNow product suite. If you’re not familiar with something, definitions can be found in my ServiceNow 101 article here.

b. Key Points

- Middle East conflict holding revenue back a bit.

- Margins will be pressured by M&A in the near-term.

- Mixed guidance.

c. Demand

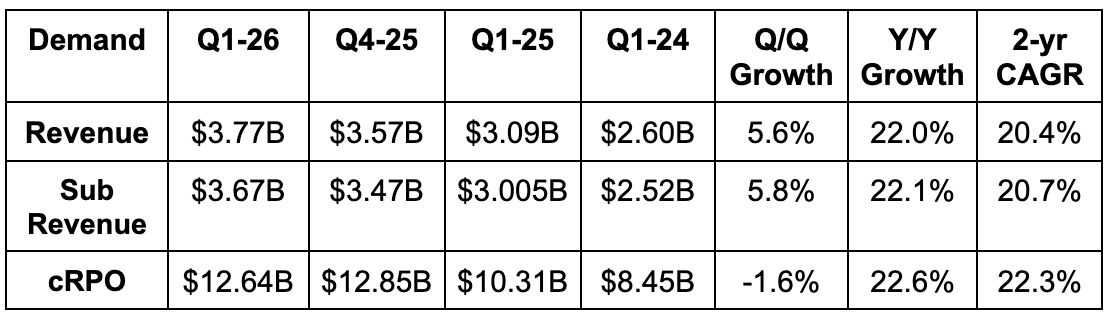

- Beat revenue estimates by 0.8%.

- Inorganic contributions from Veza (closed Mid-March) and Pyramid M&A were "tiny" and revenue was still ahead of expectations excluding them.

- Beat subscription revenue estimates by 0.5% & beat guidance by 0.4%.

- 19% constant currency (CC) subscription revenue growth was modestly ahead of 18.75% CC growth guidance.

- Subscription revenue growth was held back by ~150 bps via a shift from self-hosted to hosted revenue.

- Slightly beat current remaining performance obligation (cRPO) estimates.

- 21% Y/Y CC cRPO growth beat 20% guidance and beat 20.6% growth estimates.

- RPO rose by 25% Y/Y.

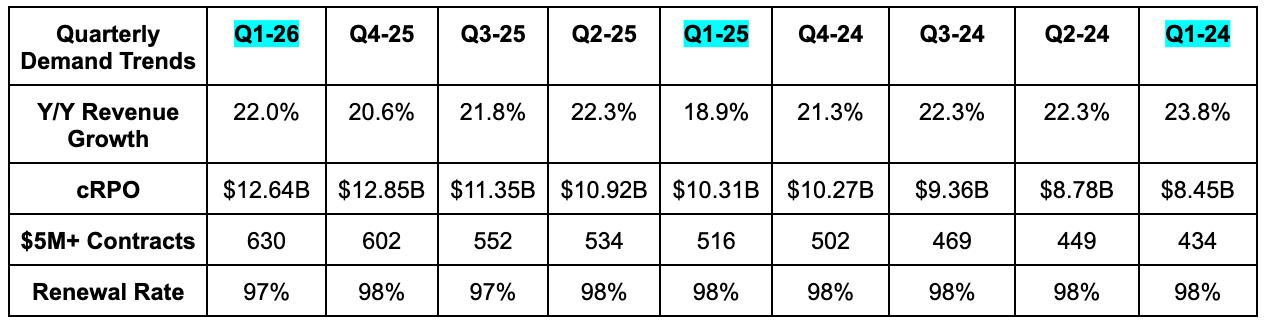

- Interestingly, the U.S. public sector outperformed internal expectations despite weak channel checks throughout the quarter.

- Subscription revenue growth was held back by delayed on-premise deal closings in the Middle East due to the ongoing conflict. All business in that region is on-premise (so lumpy recognition). Without this, subscription revenue would have been $200M higher. For evidence that this is truly timing based, a few of the deals that slipped from Q1 have already closed.

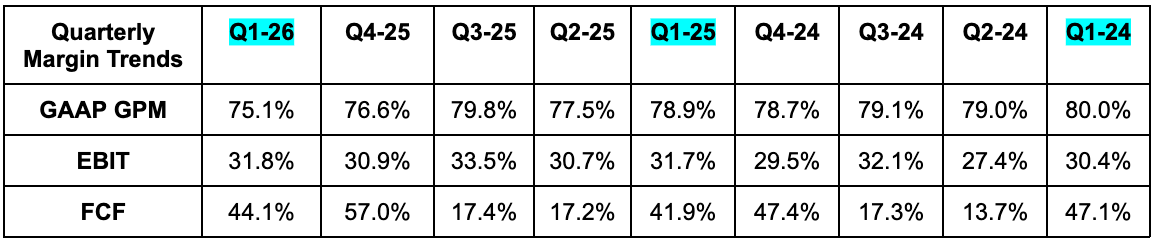

d. Profits & Margins

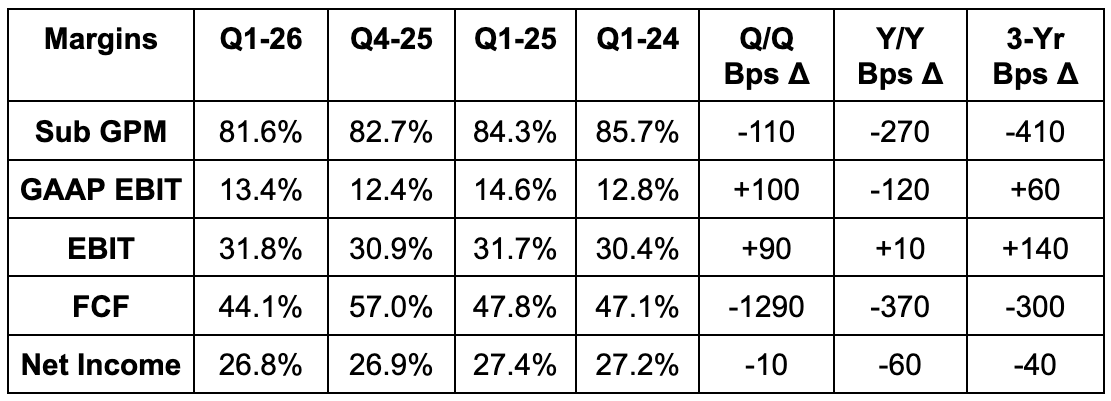

- Missed 82.5% subscription GPM estimates by 90 basis points (bps; 1 basis point = 0.01%).

- Beat EBIT estimates by 1.6% & beat EBIT margin guidance by 30 bps.

- Missed FCF estimates by 5%.

- Met $0.98 EPS estimates.

- Missed $0.53 GAAP EPS estimates by $0.08.

e. Balance Sheet

Subscribe to read about the rest of the quarter and my take on the battleground stock.