Table of Contents

Welcome back to earnings season! Over the next several weeks, I will be sending 40 detailed reviews on popular, high-quality companies. Upcoming reviews include Robinhood (tonight), Meta, SoFi, AMD, Palantir and so many others coming thereafter.

Reviews already sent:

Other recent content includes:

If you'd like all of those reports, consistently thorough weekly news, my real-time performance/portfolio updates and access to a large Discord channel of seasoned investors, subscribe below.

This is where investors (including Fortune 500 executives) come for signal over noise and to invest with good reason.

a. Key Points

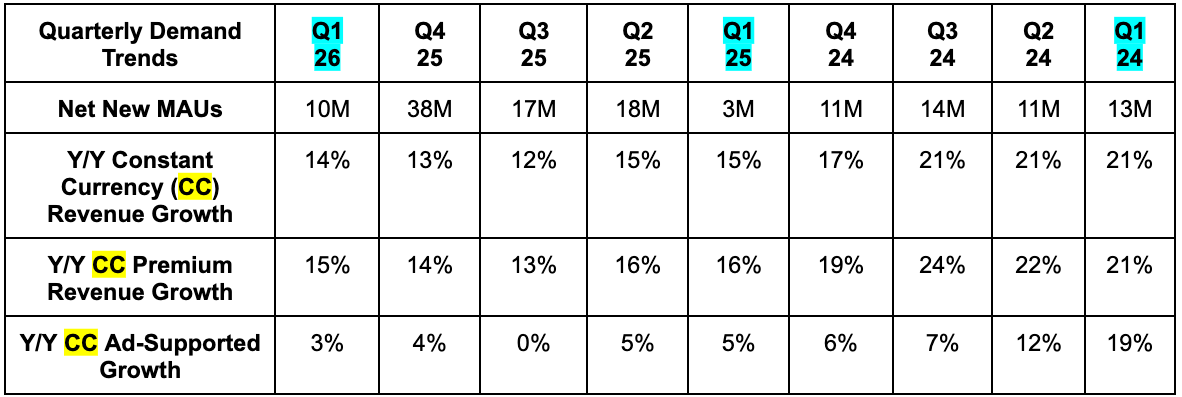

- The premium segment continues to outperform ad-based.

- The advertising gross margin contraction is temporary.

- Spotify is investing in more compute and product marketing.

- Recent price hikes went well.

b. Demand

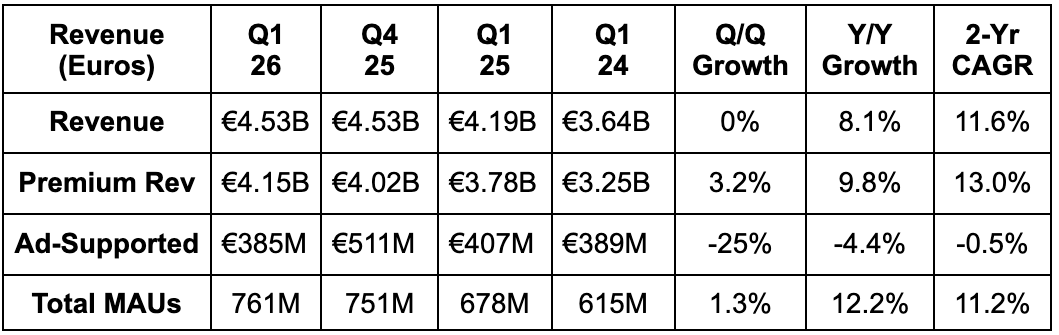

- Met revenue estimate & beat guidance by 0.6%.

- Premium revenue beat estimate by 1%.

- Ad-supported revenue missed estimate by 9%.

- Beat monthly active user (MAU) estimate & identical guidance by 2 million each.

- Met premium subscriber estimate.

- Beat premium average revenue per user (ARPU) estimate by 1.4%.

- More context on demand later in this piece.

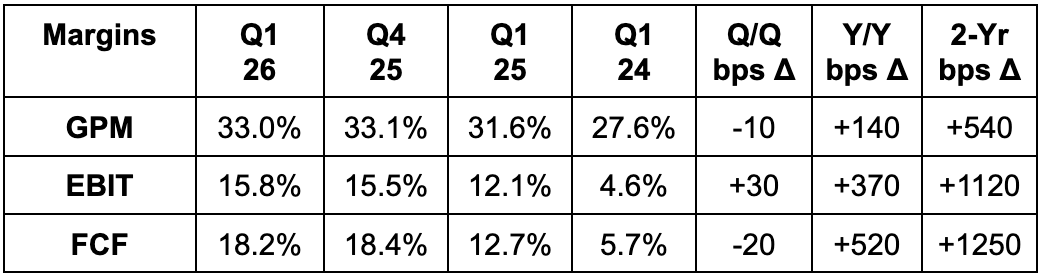

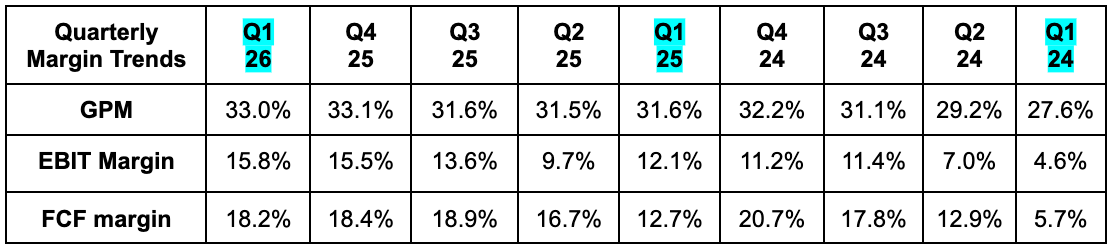

c. Profits & Margins

- Beat 32.8% GPM estimate by 20 basis points (bps; 1 basis point = 0.01%) & beat guidance by 20 bps.

- Beat EBIT estimate by 4.4% & beat guidance by 8.3%.

- Beat FCF estimate by 4.3%.

- More context on margins later in this piece.