Table of Contents

Welcome back to earnings season! Over the next several weeks, I will be sending 40 detailed reviews on popular, high-quality companies. Upcoming reviews include Robinhood, Meta, SoFi, AMD, Palantir and so many others coming thereafter.

Reviews already sent:

Other recent content includes:

If you'd like all of those reports, consistently thorough weekly news, my real-time performance/portfolio updates and access to a large Discord channel of seasoned investors, subscribe below.

This is where investors (including Fortune 500 executives) come for signal over noise and to invest with good reason.

a. Key Points

- Tesla's auto business returned to Y/Y growth.

- The company plans to spend $25B in 2026 CapEx to support several areas of expansion.

- Optimus is still on track to begin production this year.

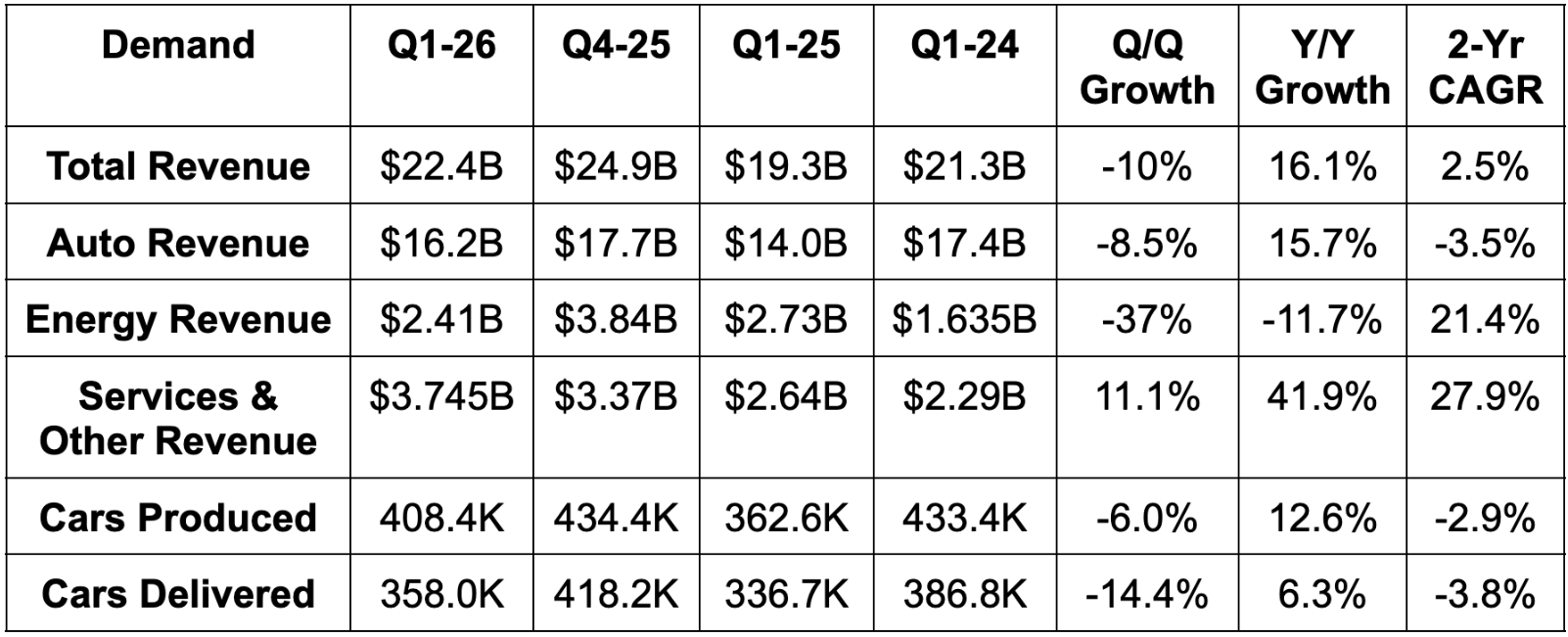

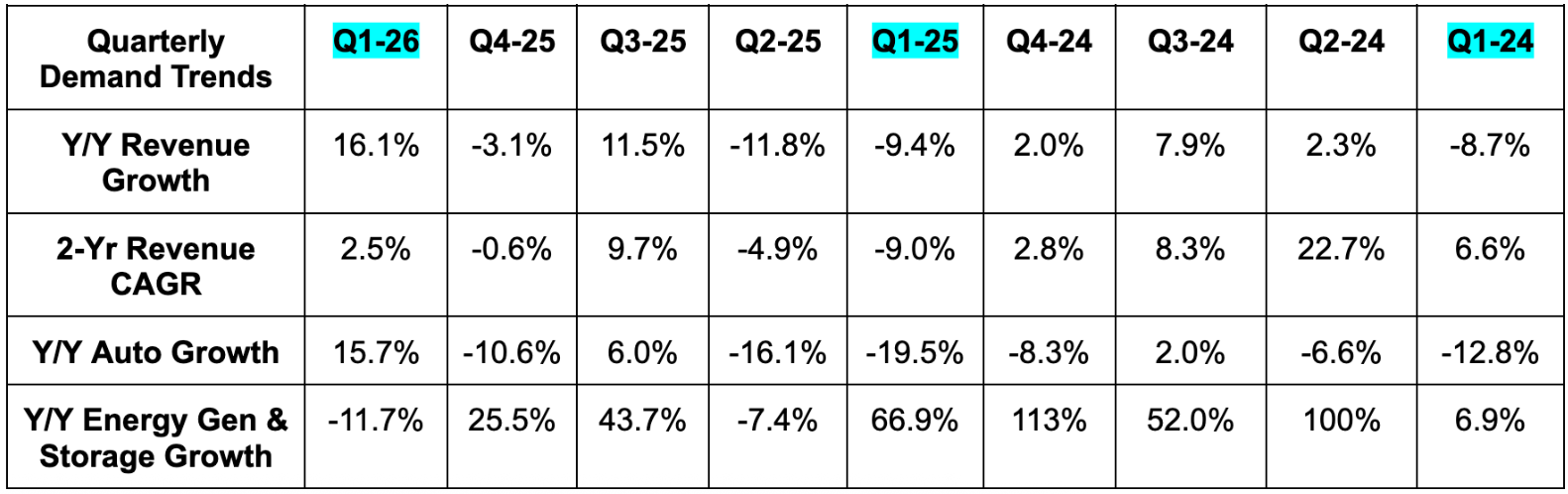

b. Demand

- Missed revenue estimate by 1.3%. This is based on the consensus number from Bloomberg as of this afternoon. Tikr and other sources had the revenue estimate at $22.3B, which would have made this a slight beat.

- Beat auto revenue estimate by 2.5%.

- Beat services revenue estimate by 17.8%.

- Missed energy revenue estimate by 35%. This segment is lumpy on a quarterly basis. Tesla reiterated expectations for positive Y/Y segment growth.

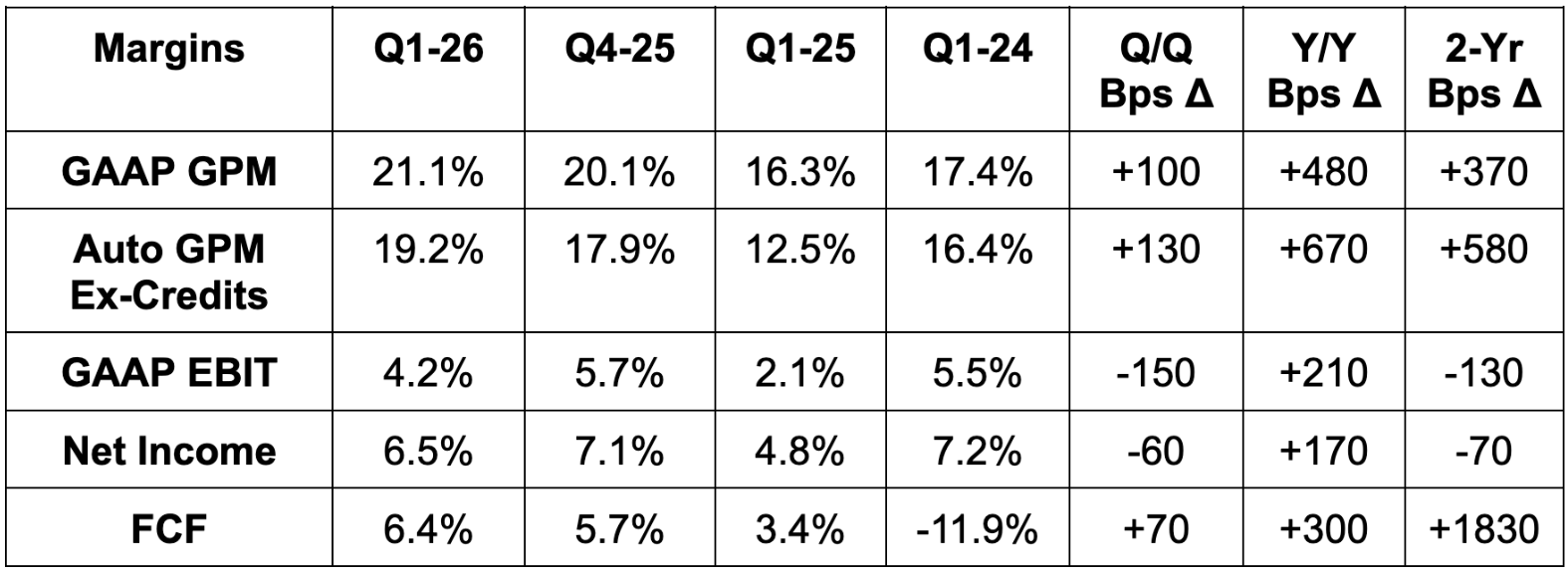

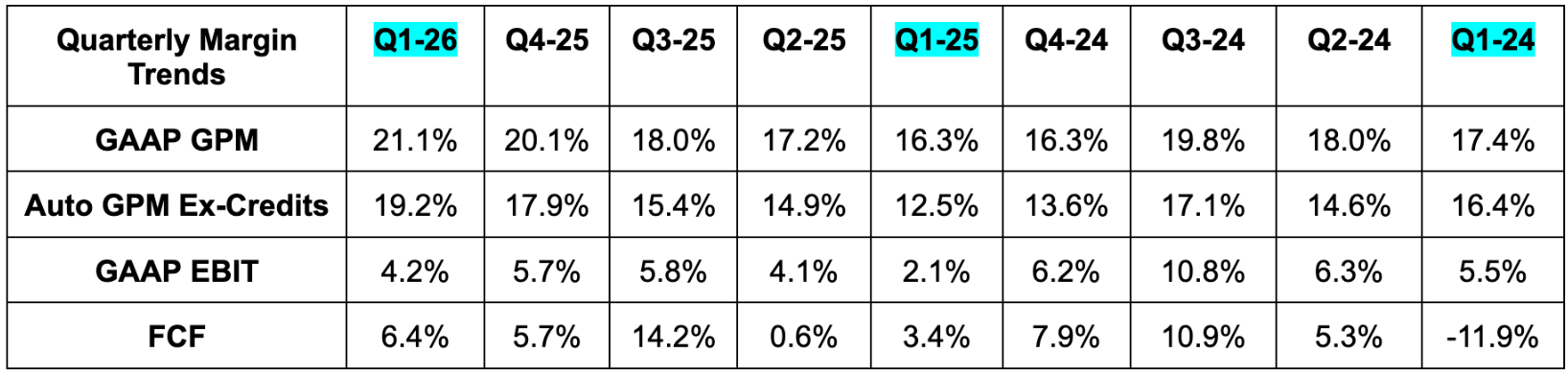

c. Profits & Margins

- Beat 18% GAAP GPM estimate by 310 basis points (bps; 1 basis point = 0.01%)

- Beat 15.3% auto GPM ex-credits estimate by 390 bps. Excluding $230M in one-time help, this margin would have been 17.7% instead of 19.2%.

- Beat GAAP EBIT estimate by 26%.

- OpEx rose due to a full quarter of stock comp from their 2025 CEO compensation plan and more AI-related spending.

- Beat $0.38 EPS estimate by $0.04.

- Beat -$1.9B FCF estimate by $3.3B.